Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI INTERVIEW: Fed’s Wright Optimistic On Further Disinflation

- MNI BRIEF: MN Fed Kashkari Puts 40% Odds On Larger Tightening Scenario

- MNI US DATA: Stronger Than Expected House Price Growth In July

- MNI US DATA: Conf. Board Labor Market Differential Consolidates Sizeable Decline

- MNI US DATA: New Home Sales Fall More Than Expected, Relative Supply Building

US

FED: A further drop in inflation should allow the Federal Reserve to stop raising interest rates soon but signs of stalling in that progress could also prompt additional central bank tightening, St. Louis Fed Senior Vice President Mark Wright told MNI.

- “I’m cautiously optimistic that the disinflation will persist and that we gradually glide down to our 2% target. I’m also extremely confident that if the data come in suggesting that we’re not going to do that, then the FOMC will make an appropriate adjustment to ensure that we’ll do so,” Wright said in an interview.

- The hawkish shift in the Fed’s estimates for the path of interest rates represents in part a desire to ensure that financial markets do not unduly loosen financial conditions by prematurely pricing in rate cuts, he said. “Interest rates are at a level to be moderately restrictive which is appropriate for the economic state of affairs,” he said. For more see MNI Policy main wire at 1411ET.

FED: Minneapolis Fed President Neel Kashkari said Tuesday he's putting 40% odds on a scenario where the central bank keeps raising interest rates and perhaps substantially to curb inflation while the odds of a soft landing have reached 60%.

- The soft landing scenario would come with perhaps one more rate increase this year and holding policy in place for a while, Kashkari said in an essay published on the regional bank's website.

- The other scenario is a "high-pressure equilibrium" with a soft landing but inflation stuck around 3% and more robust consumer spending, he said. "In this scenario, the FOMC would then have to raise rates further, potentially going significantly higher to push inflation back down to our target." Policymakers can show patience in figuring out where the economy is going, he said. (See: MNI INTERVIEW: Fed Right To Pause; Fiscal Boost Offsets Rates)

Tsys Near Lows Despite Soft Data, 10Y Yield Taps 4.5622% High

- Treasury futures trading mixed after the bell, inside a moderate range on decent volumes (TYZ3>1.4M). Tsys followed Bunds higher overnight after slightly larger than expected German supply reduction annc (DFA).

- Rates extended gains after a flurry of morning data: New Home Sales came out slower than expected: 675k vs. 699k est; prior up-revised to 739k from 714k, MoM -8.7% vs. -2.2% est. Conf. Lower than expected Consumer Confidence: 103 vs. 105.5 est.

- Little reaction from Tsy futures after the $48B 2Y note auction (91282CJB8) trades on the screws: 5.085% high yield vs. 5.085% WI; 2.73x bid-to-cover vs. 2.94x prior.

- Current Dec'23 10Y futures -.5 at 108-05 vs. 108-17 high, 10YY back near highs after the close at 4.5499% vs. 4.5622% (new 16Y high). Technical resistance just above at 109-03/109-17+ (Low Sep 13 / 20-day EMA), while round number support holds below at 108-00 after falling to 108-00.5 early overnight.

- Curves rebounded in the second half: 3M10Y +2.394 at -92.616, 2Y10Y +1.638 at -57.943.

- Focus on Wednesday Data Calendar: Durables, Cap Goods, 2Y FRN/5Y Note Sale. MN Fed president Kashkari is scheduled to speak on CNBC at 0800ET.

OVERNIGHT DATA

- The S&P CoreLogic 20-city series meanwhile also came in stronger than expected at a seasonally adjusted 0.9% M/M (cons 0.7) or a non-seasonally adjusted 0.6% M/M.

- It leaves the FHFA series 4% above its previous peak as of Jun 2022, whilst the S&P CoreLogic has almost fully reversed its prior decline and is now just -0.4% lower below its peak.

- It comes as existing home supply relative to sales remains tight compared to pre-pandemic levels.

US DATA: Conference Board consumer sentiment was softer than expected in Sept at 103.0 (cons 105.5) with the decline amplified by an upward revised 108.7 in Aug (initially 106.1).

- It’s back at levels seen through Feb-May.

- Within the survey, the labor market differential consolidated last months surprisingly abrupt decline, only ticking up to 27.3 from a marginally upward revised 26.7 (initial 26.2). This differential is back below levels seen prior to the pandemic.

- Whilst moving from relatively narrow levels, the 13.6% finding jobs hard to get is the highest since Nov’22 and before that Apr’21.

- US AUG NEW HOME SALES -8.7% TO 0.675M SAAR

- US JUL NEW HOME SALES REVISED TO 0.739M SAAR

US DATA: New home sales fell by more than expected in August, down -8.7% M/M (cons -2.2) but with some of the impact offset by a stronger than first thought 8.0% in July (initial 4.4%).

- Sales still came in softer on net though, at an annualized 675k vs consensus of 698k.

- Sales by region ranged from +6.7% to -17% M/M, but didn’t see anywhere near the same level of volatility as in July.

- Despite the latest decline, new home sales continue to paint a markedly more resilient picture to that of existing home sales which are more than 25% below pre-pandemic levels – see first chart.

- Relative supply loosened, with months of supply rising to 7.8 from a downward revised 7.0 (initial 7.3), continuing to come in above the levels seen at this time of year in pre-pandemic periods.

- The new home market continues to see higher levels of relatively supply than in the existing market.

- US SEP PHILADELPHIA FED NONMFG INDEX -16.6

- US SEPT. DALLAS FED SERVICE BUSINESS ACTIVITY -8.6 (-2.7 prior)

- US REDBOOK: SEP STORE SALES +4.0% V YR AGO MO

- US REDBOOK: STORE SALES +3.8% WK ENDED SEP 23 V YR AGO WK

CANADA DATA: Manufacturing & Wholesales Lift In August Advance

- Manufacturing sales are seen to have increased 1.0% M/M in the advance August release, a reasonable increase following the 1.6% in July considering the volatile series has recently swung between monthly increases and declines.

- Wholesale sales meanwhile are pencilled to have increased 2.6% M/M in August after 0.2% in July, focusing here on the underlying measure of excluding petroleum, petroleum products, other hydrocarbons and oilseed & grains.

- Ahead of monthly GDP on Friday, with the full details for July along with the advance August estimate, these latest nominal measures help offset some of the weakness seen in last week’s advance retail sales of -0.3% M/M.

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 421.45 points (-1.24%) at 33589.52

- S&P E-Mini Future down 69.75 points (-1.59%) at 4309

- Nasdaq down 222.9 points (-1.7%) at 13046.51

- US 10-Yr yield is up 1.9 bps at 4.5519%

- US Dec 10-Yr futures are down 1.5/32 at 108-4

- EURUSD down 0.0024 (-0.23%) at 1.0569

- USDJPY up 0.16 (0.11%) at 149.04

- WTI Crude Oil (front-month) up $0.84 (0.94%) at $90.51

- Gold is down $15.11 (-0.79%) at $1900.82

European bourses closing levels:

- EuroStoxx 50 down 38.19 points (-0.92%) at 4129.18

- FTSE 100 up 1.73 points (0.02%) at 7625.72

- German DAX down 149.62 points (-0.97%) at 15255.87

- French CAC 40 down 49.86 points (-0.7%) at 7074.02

US TREASURY FUTURES CLOSE

- 3M10Y +1.296, -93.714 (L: -101.332 / H: -91.853)

- 2Y10Y +2.059, -57.522 (L: -63.617 / H: -57.306)

- 2Y30Y +3.844, -43.647 (L: -51.523 / H: -43.431)

- 5Y30Y +3.588, 7.202 (L: 2.412 / H: 7.307)

- Current futures levels:

- Dec 2-Yr futures up 0.125/32 at 101-9.5 (L: 101-07.75 / H: 101-10.625)

- Dec 5-Yr futures down 0.25/32 at 105-8.75 (L: 105-05.75 / H: 105-14.75)

- Dec 10-Yr futures down 1.5/32 at 108-4 (L: 108-00.5 / H: 108-17)

- Dec 30-Yr futures down 14/32 at 114-13 (L: 114-10 / H: 115-23)

- Dec Ultra futures down 22/32 at 119-3 (L: 118-30 / H: 120-30)

(Z3) Bear Trend Remains Intact

- RES 4: 111-12+ High Sep 1 key resistance

- RES 3: 110-20+ 50-day EMA

- RES 2: 110-07+ High Sep14

- RES 1: 109-03/109-17+ Low Sep 13 / 20-day EMA

- PRICE: 108-02+ @ 1500 ET Sep 26

- SUP 1: 108-00 Round number support

- SUP 2: 107.23 1.236 proj of the Jul 18 - Aug 4 - Aug 10 price swing

- SUP 3: 107-05+ 1.382 proj of the Jul 18 - Aug 4 - Aug 10 price swing

- SUP 4: 106-23 1.50 proj of the Jul 18 - Aug 4 - Aug 10 price swing

Treasuries maintain a softer tone and the contract started the week yesterday on a softer note. Last week’s move down resulted in a breach of 109-03, the Sep 13 / 19 low, confirming a resumption of the current downtrend. Moving average studies are in a bear mode position highlighting a clear downtrend. The focus is on 108-00 and 107-23, the 1.236 projection of the Jul 18 - Aug 4 - Aug 10 price swing. Firm resistance is at 109-17+, the 20-day EMA.

SOFR FUTURES CLOSE

- Dec 23 +0.010 at 94.540

- Mar 24 steady at 94.610

- Jun 24 +0.010 at 94.790

- Sep 24 +0.015 at 95.050

- Red Pack (Dec 24-Sep 25) +0.010 to +0.020

- Green Pack (Dec 25-Sep 26) steady to +0.010

- Blue Pack (Dec 26-Sep 27) -0.005 to steady

- Gold Pack (Dec 27-Sep 28) -0.01 to -0.005

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00098 to 5.31843 (+0.00092/wk)

- 3M -0.00554 to 5.38558 (-0.01423/wk)

- 6M -0.00599 to 5.46327 (-0.01628/wk)

- 12M -0.00715 to 5.45973 (-0.02590/wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $93B

- Daily Overnight Bank Funding Rate: 5.32% volume: $260B

- Secured Overnight Financing Rate (SOFR): 5.31%, $1.524T

- Broad General Collateral Rate (BGCR): 5.30%, $579B

- Tri-Party General Collateral Rate (TGCR): 5.30%, $561B

- (rate, volume levels reflect prior session)

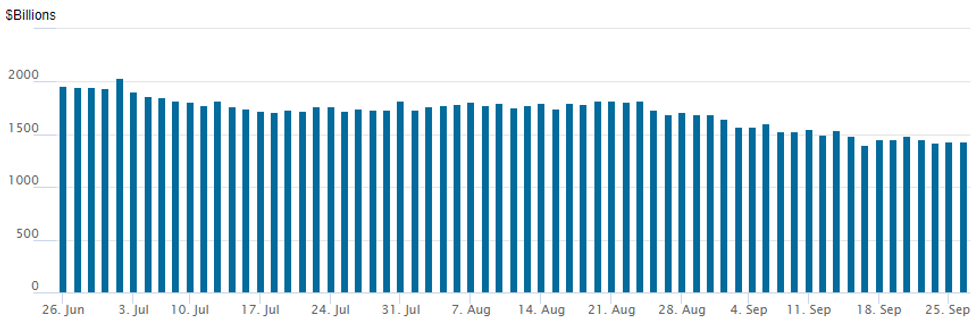

FED REVERSE REPO OPERATION

NY Federal Reserve/MNI

Repo operation inches up to 1,438.301B w/97 counterparties, compared to $1,437.310B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

PIPELINE: $14.45B Corporate Bonds to Price

$5B Citibank 3pt leads corporate issuance Tuesday, $14.45B to price.

- Date $MM Issuer (Priced *, Launch #)

- 09/26 $5B #Citibank $1.75B 2Y +73, $750M 2Y SOFR, $2.5B 5Y +118

- 09/26 $3B #CIBC $850M 3Y +110, $350M 3Y SOFR+122, $700M 5Y +137.5, $1.1B 10Y +155

- 09/26 $1.75B *Islamic Development Bank Sukuk 5Y SOFR +52

- 09/26 $1.4B #Constellation Energy $500M 10Y +158, $900M 30Y 180

- 09/26 $1.25B *Swedish Export Credit (SEK) 7Y SOFR +72

- 09/26 $1B #Rabobank $700M 3Y +77, $300M 3Y SOFR+90

- 09/26 $500M #SFIL 5Y SOFR +54

- 09/26 $550M #SoCal Edison 5Y +105

- 09/26 $Benchmark First Abu Dhabi Bank 10.5NC5.5 +170 (book >$3B)

EGBs-GILTS CASH CLOSE: BTPs Hit March Wides To Bunds

The German and UK curves twist steepened modestly Tuesday, with core yields closing within 1bp of Monday's close after several intraday changes in direction.

- Yields opened the session wider in a continuation of the "higher for longer" rates theme, but fell sharply alongside weakness in oil prices, and a more sizeable-than-expected cut in Germany's Q4 issuance plan.

- Meanwhile, BTP spreads closed at post-March wides, with another report (from Bloomberg) pointing to a sizeable upward revision in the 2024 fiscal deficit target to be unveiled Wednesday by the Italian coalition gov't.

- Between Italy and broader risk-off (Eurostoxx down nearly 1%), other periphery spreads were dragged wider.

- Gilts were largely a bystander to broader events, though relatively weak demand details at today's auction was of some note.

- While there is some data Weds morning (eg German and French consumer confidence), attention is still firmly on the Eurozone September flash inflation data out Thursday and Friday - MNI's preview went out today (PDF link).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.6bps at 3.231%, 5-Yr is up 0.6bps at 2.771%, 10-Yr is up 1bps at 2.808%, and 30-Yr is up 0.6bps at 3.004%.

- UK: The 2-Yr yield is down 0.8bps at 4.808%, 5-Yr is down 0.3bps at 4.398%, 10-Yr is up 0.3bps at 4.326%, and 30-Yr is up 0.9bps at 4.805%.

- Italian BTP spread up 7bps at 193.4bps / Spanish up 2.5bps at 109.7bps

FOREX Greenback Resumes Ascent, Fresh Trend Highs For USD Index

- Despite the USD index dipping across European hours and sliding into negative territory on the day, the greenback has regained its poise and resumed its ascent. The DXY is printing fresh cycle highs as we approach the APAC crossover, currently up another 0.25% and extending above the 106.00 mark.

- Weakness for equities have weighed on more risk sensitive currencies with the likes of AUD and GBP among the worst performers, declining half a percent.

- GBPUSD stands out as the pair extends its decline below 1.2200. The recent move down confirms a resumption of the bear trend and maintains the bearish price sequence of lower lows and lower highs. The focus is on 1.2120, a Fibonacci projection.

- EURUSD also spent the majority of the session consolidating around 1.0600 before extending to fresh lows at typing. Price action narrows the gap with 1.0516, the March 15 and a key support.

- In emerging markets, there was some notable weakness for the South African rand, which weakened over 1.5% against the greenback. The move was largely playing catch up following the national holiday on Monday with familiar broader-picture concerns that have weighed on some EM currencies.

- Australian August CPI data will highlight Wednesday’s docket before US Durable Goods. Focus will then turn to Eurozone inflation data later in the week.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 27/09/2023 | 0130/1130 | *** |  | AU | CPI Inflation Monthly |

| 27/09/2023 | 0600/0800 | * |  | DE | GFK Consumer Climate |

| 27/09/2023 | 0600/1400 | ** |  | CN | MNI China Liquidity Survey |

| 27/09/2023 | 0645/0845 | ** |  | FR | Consumer Sentiment |

| 27/09/2023 | 0700/0900 | ** |  | SE | Economic Tendency Indicator |

| 27/09/2023 | 0800/1000 | ** |  | EU | M3 |

| 27/09/2023 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 27/09/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 27/09/2023 | 1230/0830 | ** | | US | Durable Goods New Orders |

| 27/09/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 27/09/2023 | 1530/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 27/09/2023 | 1700/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.