Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

US

FED: Federal Reserve bank supervision chief Michael Barr pledged Monday to use "all of our tools for any size institution, as needed, to keep the system safe and sound," ahead of testimony to the Senate Banking Committee on oversight of failed Silicon Valley Bank.

- Bank regulators' and Treasury's swift actions after the collapse of SVB "demonstrate that we are committed to ensuring that all deposits are safe," he said. "We will continue to closely monitor conditions in the banking system and are prepared to use all of our tools for any size institution, as needed, to keep the system safe and sound."

- The Fed's one-year emergency lending facility for banks along with its discount window and banks' own resources provide "ample liquidity for the banking system as a whole," he added. SVB's failure was a result of mismanagement and Fed supervisors repeatedly warned executives of deficiencies, Barr said.

- Biden said in a statement: "Ensuring a robust, resilient, and sustainable domestic industrial base is essential for the national defense."

- Biden: "I hereby determine... that printed circuit boards and advanced packaging, their components, and the manufacturing systems that produce such systems and components are industrial resources, materials, or critical technology items essential to national defense."

- Biden claims that "...without Presidential action," US industry "cannot reasonably be expected to provide the capability for the needed industrial resource, material, or critical technology item in a timely manner," arguing that invoking the DPA is, "the most cost-effective, expedient, and practical alternative method for meeting the need."

UK

BOE: Economic activity recently has been stronger and nominal wage growth weaker than the Bank of England had expected, Bank of England Governor Andrew Bailey said Monday. although he offered no fresh steer on whether a further rate hike was likely to be needed.

- Bailey, speaking at the LSE, said that if there were signs of more persistent inflationary pressures further policy tightening would be required but the recent data have been mixed.

- "The evidence has pointed to more resilient activity in the economy, and likewise employment; signs that nominal wage growth has been rather weaker than expected," he said, with inflation surprising at first on the downside and then in February on the upside of BOE expectations, with the Monetary Policy Committee hiking 25 basis points at its March meeting.

- Bailey reaffirmed the Bank's belief that there would be a sharp fall in inflation this year, likely starting in a couple of months, and he noted that the effects of previous rate hikes had yet to feed through in full.

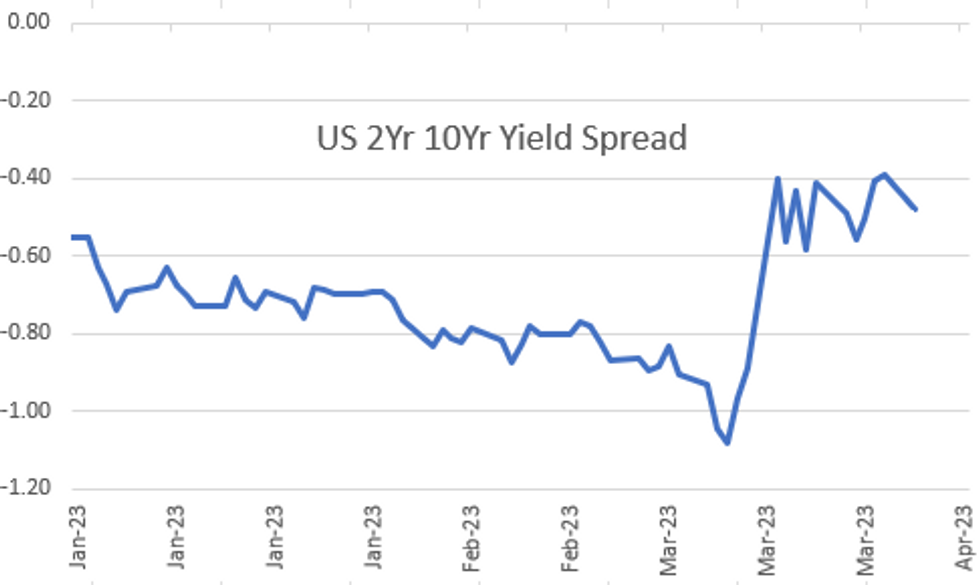

US TSYS: Bear Flattening Extends, Bank Cares Moderate

Tsy futures drifted near late session lows Monday, yield curves bear flattening (2s10s -9.438 at -49.302, well off early high of -40.518) as regional bank share panic moderated to a degree.

- Early support for bank shares cooled around midday, KBW Bank index (BKK) gave up a more than half of their gains made on the open to a session low of 79.69, drifted off lows in the second half to approximately 80.75 in late trade. KBW "is a modified cap-weighted index consisting of 24 exchange-listed National Market System stocks, representing national money center banks and leading regional institutions."

- Front month 2Y futures extended lows (103-12.75, -15.75) after the $42B Treasury 2Y note auction (91282CGU9) tailed (second consecutive): 3.954% high yield vs. 3.915% WI; 2.44x bid-to-cover vs. 2.61x prior.

- Meanwhile, 10Y futures at 114-31.5 (10Y yield at 3.5261%). For a technical perspective, early 10Y signals suggest that Friday’s candle pattern - a shooting star formation - represents a possible short-term reversal. If correct, this suggests scope for weakness towards the 20-day EMA, at 114-00.

- Focus turns to Tuesday's Wholesale/Retail Inventories early, home price data and consumer confidence at midmorning. $43B 5Y Note auction (91282CGT2) auction at 1300ET.

OVERNIGHT DATA

Dallas Fed Manufacturing index data (-15.7 vs. -10.0 est, -13.5 prior).

MARKETS SNAPSHOT

Key late session market levels:

DJIA up 316.44 points (0.98%) at 32553.1

S&P E-Mini Future up 25 points (0.62%) at 4026.5

Nasdaq up 8.1 points (0.1%) at 11831.4

US 10-Yr yield is up 14.8 bps at 3.5242%

US Jun 10-Yr futures are down 35.5/32 at 115-0

EURUSD up 0.0038 (0.35%) at 1.0799

USDJPY up 0.85 (0.65%) at 131.57

WTI Crude Oil (front-month) up $3.68 (5.31%) at $72.89

Gold is down $22.15 (-1.12%) at $1956.15

European bourses closing levels:

- EuroStoxx 50 up 34 points (0.82%) at 4164.62

- FTSE 100 up 66.32 points (0.9%) at 7471.77

- German DAX up 170.45 points (1.14%) at 15127.68

- French CAC 40 up 63.17 points (0.9%) at 7078.27

US TREASURY FUTURES CLOSE

- 3M10Y +7.535, -123.628 (L: -136.832 / H: -121.884)

- 2Y10Y -7.89, -47.754 (L: -50.789 / H: -40.518)

- 2Y30Y -11.724, -24.761 (L: -28.438 / H: -13.581)

- 5Y30Y -6.71, 16.662 (L: 13.031 / H: 23.29)

- Current futures levels:

- Jun 2-Yr futures down 13.75/32 at 103-14.75 (L: 103-12.75 / H: 103-31)

- Jun 5-Yr futures down 26.75/32 at 109-20.75 (L: 109-17.75 / H: 110-18.25)

- Jun 10-Yr futures down 1-3.5/32 at 115-0 (L: 114-28.5 / H: 116-06.5)

- Jun 30-Yr futures down 2-0/32 at 130-11 (L: 130-08 / H: 132-19)

- Jun Ultra futures down 2-30/32 at 139-21 (L: 139-16 / H: 143-03)

Shooting Star Reversal?

- RES 4: 118-07 High Aug 23 (cont)

- RES 3: 117-29+ High Aug 26 2022 (cont)

- RES 2: 117-14+ High Aug 29 / 30 2022 (cont)

- RES 1: 116-06+/117-01+ Intraday high / High Mar 24 and bull trigger

- PRICE: 115-08+ @ 16:41 GMT Mar 27

- SUP 1: 115-00 Low Mar 23

- SUP 2: 114-00/113-26 20-day EMA / Low Mar 22

- SUP 3: 113-21+ 50-day EMA

- SUP 4: 113-08+ Low Mar 15

Treasury futures traded higher Friday but stalled at 117-01+. The contract is trading lower today. Early signals suggest that Friday’s candle pattern - a shooting star formation - represents a possible short-term reversal. If correct, this suggests scope for weakness towards the 20-day EMA, at 114-00. The average represents a key support, ahead of 113-26, the Mar 22 low. Key resistance and the bull trigger is at 117-01+.

EURODOLLAR FUTURES CLOSE

- Jun 23 -0.135 at 94.80

- Sep 23 -0.240 at 95.285

- Dec 23 -0.270 at 95.605

- Mar 24 -0.270 at 95.995

- Red Pack (Jun 24-Mar 25) -0.255 to -0.16

- Green Pack (Jun 25-Mar 26) -0.155 to -0.125

- Blue Pack (Jun 26-Mar 27) -0.135 to -0.12

- Gold Pack (Jun 27-Mar 28) -0.13 to -0.125

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00015 to 4.90871% (+0.24800 total last wk)

- 1M +0.02172 to 4.85229% (+0.00457 total last wk)

- 3M +0.04171 to 5.14314% (+0.10300 total last wk)*/**

- 6M +0.17385 to 5.16114% (-0.06500 total last wk)

- 12M +0.25228 to 5.06114% (-0.22528 total last wk)

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.15371% on 3/9/23

- Daily Effective Fed Funds Rate: 4.83% volume: $92B

- Daily Overnight Bank Funding Rate: 4.82% volume: $271B

- Secured Overnight Financing Rate (SOFR): 4.80%, $1.290T

- Broad General Collateral Rate (BGCR): 4.78%, $513B

- Tri-Party General Collateral Rate (TGCR): 4.78%, $505B

- (rate, volume levels reflect prior session)

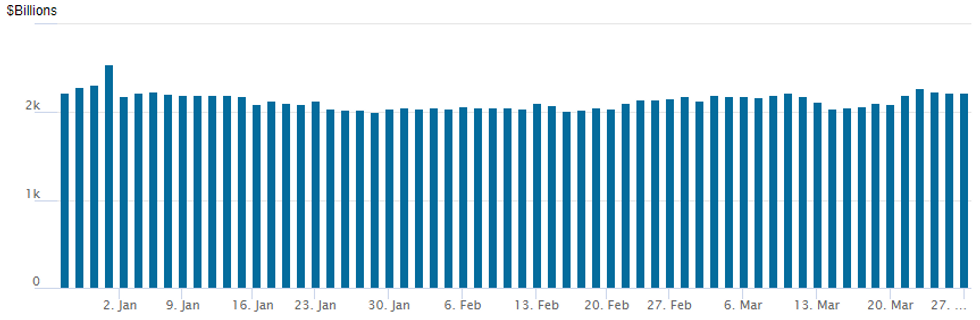

FED Reverse Repo Operations

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $2,220.131B w/ 98 counterparties vs. the prior session's $2,.218.458B. Compares to Friday, Dec 30 record/year-end high of $2,553.716B (prior record high was $2,425.910B on Friday, September 30.

PIPELINE: $3B Mercedes-Benz 4Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 03/27 $3B #Mercedes-Benz $1B 2Y +95, $300M 2Y SOFR, $1B 3Y +105, $700M 5Y +123

- 03/27 $1.25B #Republic of Costa Rica 11Y 6.55%

- 03/27 $1.25B #Phillips 66 $750M 5Y +140, $500M 10Y +182

- 03/27 $1.1B #Pioneer Natural 3Y +132

- 03/27 $1B #General Mills 10Y +145

- 03/27 $1B #Tennessee Valley Authority 5Y +45

- 03/27 $1B #Korea National Oil $550B 3Y +120, $450M 5Y +135

- 03/27 $850M #Public Service of Colorado 30Y +155

- 03/27 $750M #Penske Leasing 5Y +205

- 03/27 $500M #Berry Global 5Y +210

EGBs-GILTS CASH CLOSE: Curves Bear Flatten As Bank Fears Subside

The UK and German curves bear flattened Monday with the latter underperforming, as weekend headlines propped up confidence in the US banking sector.

- First Citizens' takeover of Silicon Valley Bank and a Bloomberg sources piece ("US Mulls More Support for Banks While Giving First Republic Time") drove European equities and yields higher in early trade, with US bank stocks soaring at the US cash open.

- Rates continued rising in early afternoon on BBG sources story saying Exec Board's Schnabel pushed for a clearer signal in the ECB's March statement on further rate hikes.

- This continued to pressure the short end, with the implied ECB rate hike path seeing near 90% chance of a 25bp raise in May, and just over 50bp cumulative left in the cycle (vs 60% and 20bp at Friday's lows, respectively).

- A beat in German IFO kept sentiment bearish, but didn't really move the needle.

- The bear flattening move petered out a little by mid-afternoon as global bank stocks gave up some of their earlier gains. 10Y BTP spreads likewise failed to decisively break through the 183bp mark vs Bunds.

- BoE Gov Bailey speaks after the cash close, while the schedule early Tuesday includes appearances by ECB hawks Rehn and Muller, and French confidence surveys.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 12.8bps at 2.521%, 5-Yr is up 11.2bps at 2.211%, 10-Yr is up 9.8bps at 2.227%, and 30-Yr is up 9bps at 2.308%.

- UK: The 2-Yr yield is up 10bps at 3.311%, 5-Yr is up 9.2bps at 3.219%, 10-Yr is up 8.3bps at 3.366%, and 30-Yr is up 3.9bps at 3.807%.

- Italian BTP spread down 4.4bps at 183.7bps / Greek down 7.8bps at 188bps

FOREX: JPY Underperforms Amid Pressure In Core Fixed Income

- With core fixed income under pressure and equities trading on the front foot, pressure on the Japanese Yen has resumed on Monday and is the notable underperformer for today’s trading session.

- USDJPY (+0.65%) has had a solid bounce from the overnight 130.41 lows, however, the slightly more optimistic backdrop has more notably supported the crosses with CADJPY leading the way, rising 1.3% to start the week.

- Elsewhere, EURJPY trades buoyantly and technically eyes the key short-term resistance at 143.63 where a break is required to reinstate the bullish theme. Note that moving average studies remain in a bull mode set-up - this suggests the latest pullback has been a correction. A break of 143.63 would initially open 143.98, 76.4% of the Mar 2 - 20 bear cycle.

- USD/CNH also inched higher with the pair briefly clearing 6.8942 - the Mar 22 (and FOMC day) high. Further gains here would open more meaningful resistance at the 100- and 200-dmas of 6.9258 and 6.9326 respectively.

- The moves follow the overnight industrial profits data, which showed January-February profits slipping 23% Y/Y - that's the third fastest pace of decline on record, after only the GFC in '08 and onset of the COVID pandemic in 2020.

- Additionally, the previously announced RRR cut came into effect Monday, pressuring interbank rates (overnight repo rate dropped to lowest since early January). This effect was compounded by PBOC OMOs, further supporting liquidity in Asia-Pac trade.

- Outgoing Bank of Japan Governor Kuroda is due to speak on Tuesday at the FIN/SUM 2023, in Tokyo. There may be further comments from BOE’s Bailey as well as ECB’s Lagarde, due to speak at the opening ceremony of Bank of International Settlements Innovation Hub Eurosystem Centre, in Frankfurt. US consumer confidence highlights a quiet data docket.

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/03/2023 | 2301/0001 | * |  | UK | BRC Monthly Shop Price Index |

| 28/03/2023 | 0030/1130 | ** |  | AU | Retail Trade |

| 28/03/2023 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 28/03/2023 | 0800/1000 | ** |  | IT | ISTAT Business Confidence |

| 28/03/2023 | 0800/1000 | ** | | IT | ISTAT Consumer Confidence |

| 28/03/2023 | 1230/0830 | ** |  | US | Advance Trade, Advance Business Inventories |

| 28/03/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 28/03/2023 | 1300/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 28/03/2023 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 28/03/2023 | 1315/1515 |  | EU | ECB Lagarde Speech at BIS Innovation Hub Opening | |

| 28/03/2023 | 1400/1000 | *** | | US | Conference Board Consumer Confidence |

| 28/03/2023 | 1400/1000 | ** | | US | Richmond Fed Survey |

| 28/03/2023 | 1400/1000 | | US | Senate Banking Committee Hearing | |

| 28/03/2023 | 1430/1030 | ** | | US | Dallas Fed Services Survey |

| 28/03/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 28/03/2023 | 1700/1300 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 28/03/2023 | 1700/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

| 28/03/2023 | 2000/1600 |  | CA | Federal budget (Release around 4pm, as finance minister delivers it to Parliament) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.