Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

MNI (London)

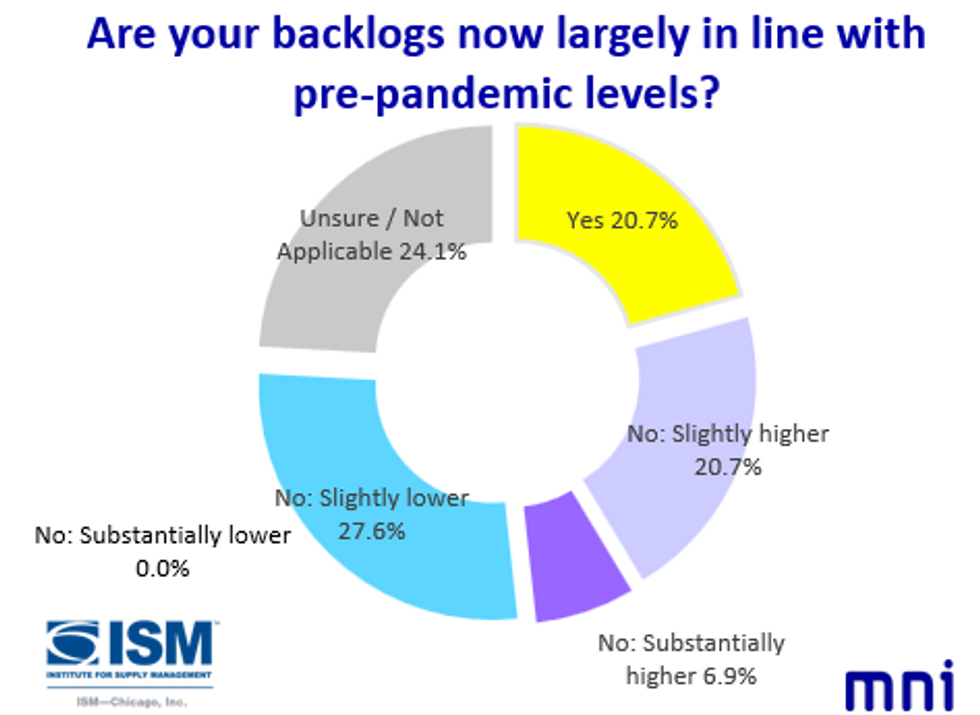

The Chicago Business Barometer™ Survey asked firms in March whether their backlogs are now largely in line with pre-pandemic levels.

- Firms’ responses were relatively mixed. Around one fifth (20.7%) stated that their backlogs were largely at pre-pandemic levels. 27.6% assessed their backlogs as slightly/substantially higher, and a further 27.6% found their backlogs were slightly lower. 24.1% responded unsure or N/A.

- Order Backlogs picked up again in March, rising 5.6 points to 45.6. This was again below the neutral 50 threshold, marking three months of falling backlogs. Lower order backlogs are likely a delayed effect of the continued fall in new orders, which contracted for a tenth consecutive month in the March survey.

- With 27.6% of respondents still flagging higher backlog levels that before the pandemic, overall production is likely to remain somewhat shielded from low new order intake for now.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok