Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

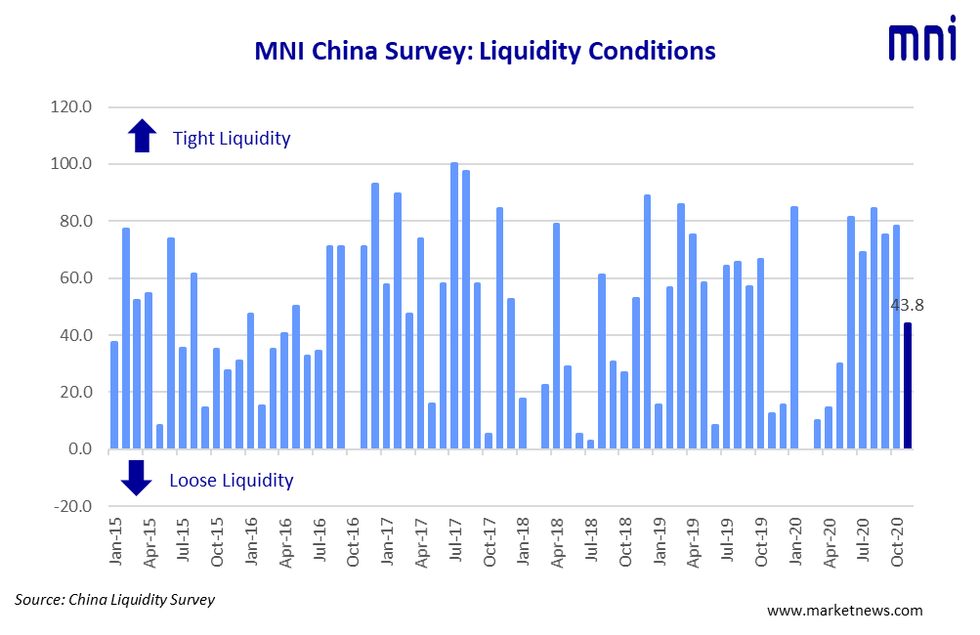

Liquidity across China's interbank market eased modestly in November, recovering from the modest tightening seen in the previous month, the latest MNI Liquidity Conditions Index shows.

The Index fell to 43.8 in November from the 78.1 recorded in October, hitting the lowest reading in the last six months, this survey showed, with almost a third of respondents reporting an easing in conditions over the four-week period.

The higher the index reading, the tighter liquidity appears to survey participants.

"Reduced tax payment and lighter bonds issuance quota both supported the funding," and helped improve liquidity levels, a trader with state-owned bank based in Nanjing told MNI.

The People's Bank of China conducted CNY800 billion MLF in the month to offset a maturing CNY600 billion MLF, a net CNY200 billion drain via open market operations as of November 24, MNI calculated.

RECOVERING ECONOMY

The Economy Condition Index stood at 87.5 in November, down from the six-year-high of 93.8 seen last month. Three quarters of participants answered positively when asked about the current economy based on the latest indicators, which saw better retail sales and higher industrial output.

"Domestic consumption is improving along with the control of the pandemic. Retail sales are resuming, investments are resuming strongly as well. The economy's is able to be maintained," a Shanghai based trader said.

The PBOC Policy Bias Index was unchanged at 65.6 in November, but 12.5% more traders were expecting the easier policy to tackle the pandemic may be removed in future months.

The Guidance Clarity Index came in at 56.3 in November, down from 62.5, with the vast majority (87.5%) of the participants seeing no big changes to policy transparency.

RISING YIELDS

The 7-Day Repo Rate Index slid to 59.4 from last 71.9, with 43.8% of the traders predicting higher rates due to month-end effects and tax payments through November and December.

The 7-day weighted average interbank repo rate for depository institutions (DR007) closed at 2.2940% Tuesday.

The 10-year CGB Yield Index rose for a third consecutive month to 81.3 in November, following October's 75.0, the highest level since January 2017. 68.8% of the traders see yields higher

The MNI survey collected the opinions of 16 traders with financial institutions operating in China's interbank market, the country's main platform for trading fixed-income and currency instruments, and the main funding source for financial institutions. Interviews were conducted Nov 9 – Nov 20.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.