Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

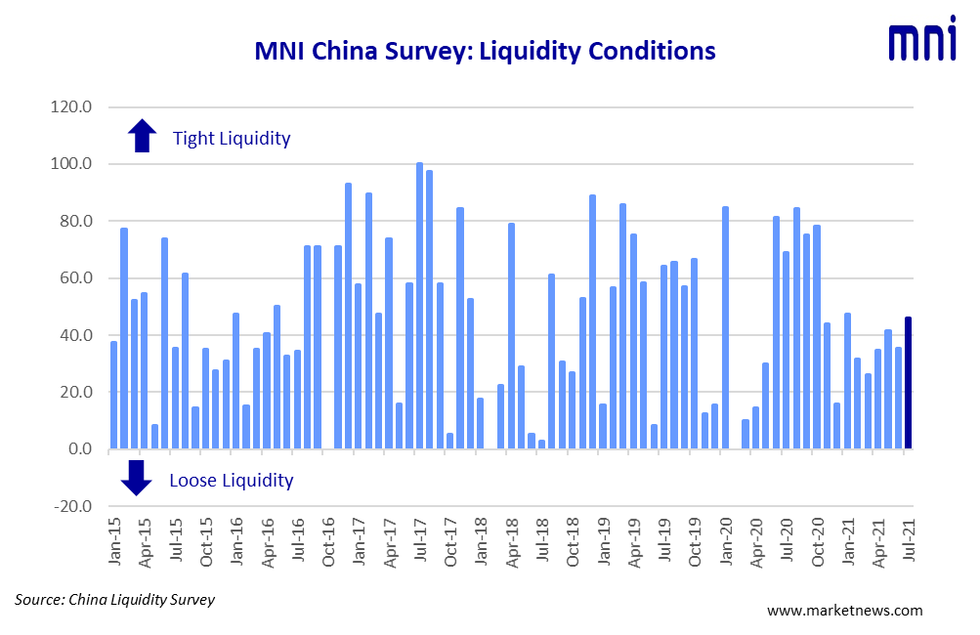

China's interbank market saw short-term liquidity tighten modestly in July despite the surprise reserve requirement ratio (RRR) cut and trader concerns that the economy is starting to slow, the latest MNI Liquidity Conditions Index shows.

The Liquidity Condition Index rose to 46.0 in July, the highest level in six months, up from 35.4 in June. The higher the index reading, the tighter liquidity appears to survey participants. A third of traders reported "looser" conditions, but a quarter saw tighter funding levels, up from zero last month.

One trader from the Anhui region told MNI that the RRR cut helped ease tax payment liquidity shortages, but it is still seen as a move to help smooth future MLF maturities and "reserve some room for a possible policy move."

Another trader pointed to a likely surge in local government bond issuance in the second half of the year, with more than 70% of authorized issuance still outstanding, would also be eased by the RRR cut.

The People's Bank of China cut the RRR by 50 bps on July 15, releasing around CNY1 trillion long-term funds, MNI calculated.

SLOWDOWN

The Economy Condition Index fell sharply to 20.0 in July, down from 47.9. It was the lowest since February 2020, the first post-pandemic reading. Almost two-thirds of respondents saw the economy "worse" this month

One Shanghai based fund manager said retail sales – down for a third straight month in June -- remained weak, with manufacturing also running at a slower pace than this time last year. A Guangdong based trader said some factors driving the recovery, property investments and exports, were slowing somewhat.

The PBOC Policy Bias Index stood at 46.0 in July, down from 52.1 in June, with the overwhelming majority of respondents seeing no change in the monetary policy stance, although one Shanghai-based trader said there could be another RRR cut in Q4 "if downward pressure increases."

The Guidance Clarity Index reads at 58.0 in July, down from the 60.4 in June, with 84.0% of traders saying they understood policies and signals from the authorities, despite the surprise RRR cut.

10Y CGB YIELD LOWER

The 7-Day Repo Rate Index surged to 72.0 from last 43.8, with 56.0% of the participants predicting higher rates ahead. The 7-day weighted average interbank repo rate for depository institutions (DR007) closed at 2.3228% Tuesday.

The 10-year CGB Yield Index, fell to 32.2 in July, slipping from 45.8, with 44.0% of the traders seeing a possible yield drop in the next three months, with the Shanghai trader seeing yields "around 2.8-3.0%" on economy concerns.

DOWNWARD PRESSURE

China's economy is slowing down, and will facing growing downward pressure in coming quarters, with major indicators dropping and visible lack of dynamic factors.

The special question in the July survey asked respondents "How do you see the growth of the economy in H2?". All participants saw a slowdown, although there was a divergence over the degree.

"GDP is likely to fall to 5%-7% in H2, with the recovery still uncertain," a Beijing based analyst told MNI. Many other respondents pointed to slowing investment, whether property or into the manufacturing sector.

The MNI survey collected the opinions of 25 traders with financial institutions operating in China's interbank market, the country's main platform for trading fixed income and currency instruments, and the main funding source for financial institutions. Interviews were conducted Jul 12 – Jul 23.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.