Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

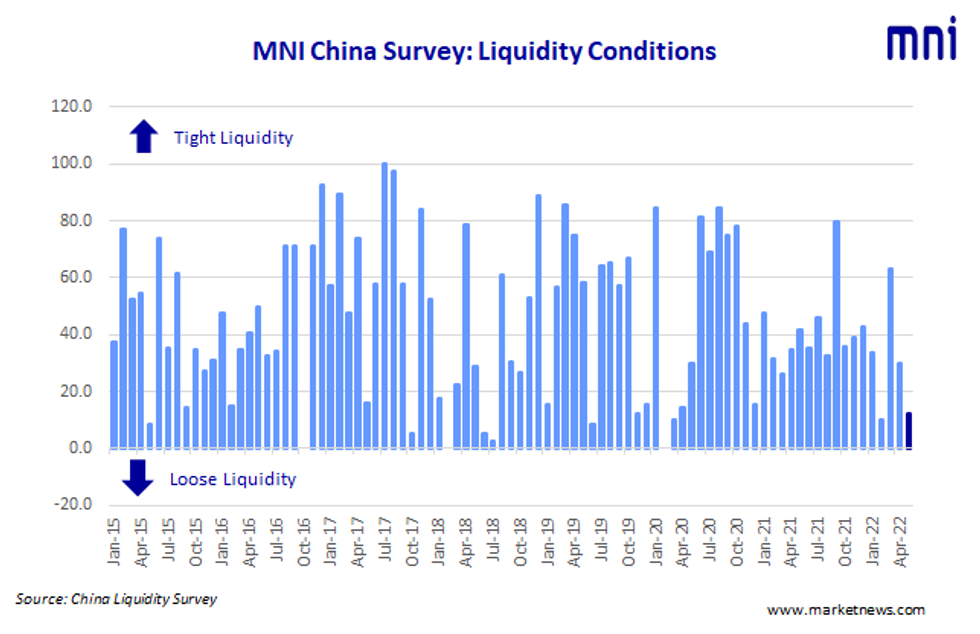

With further lockdowns and Covid-related restrictions across the economy, demand for credit has slowed, leaving an abundance of liquidity in the system, which, along with central bank operations, has pushed short-term money market rates lower, the latest MNI Liquidity Conditions Index shows.

The Liquidity Condition Index slipped to 12.5 in May, down from 30.0 in April, touching the second lowest reading since the breakout of the Covid in early 2020. As many as three-quarters of traders reporting conditions improved on April.

The higher the index reading, the tighter liquidity appears to survey participants.

“Funds are ample enough at present,” a trader with a state-owned bank in Jiangsu told MNI, while a senior trader in Shandong said demand for funds was as low as he could remember in a decade.

The People’s Bank of China conducted CNY100 billion MLF in May, offsetting the equivalent maturity. PBOC drained net CNY10 billion via its open market operation as of May 24, MNI calculated.

INCREASING DOWNWARD PRESSURE

The Economy Condition Index fell to 18.8 in May from 26.7 previously – the first time below 20.0 in five months, with 62.5% of the participants seeing downside economic risks growing. One senior fund manager told MNI, the slowing economy risked a higher unemployment rate ahead.

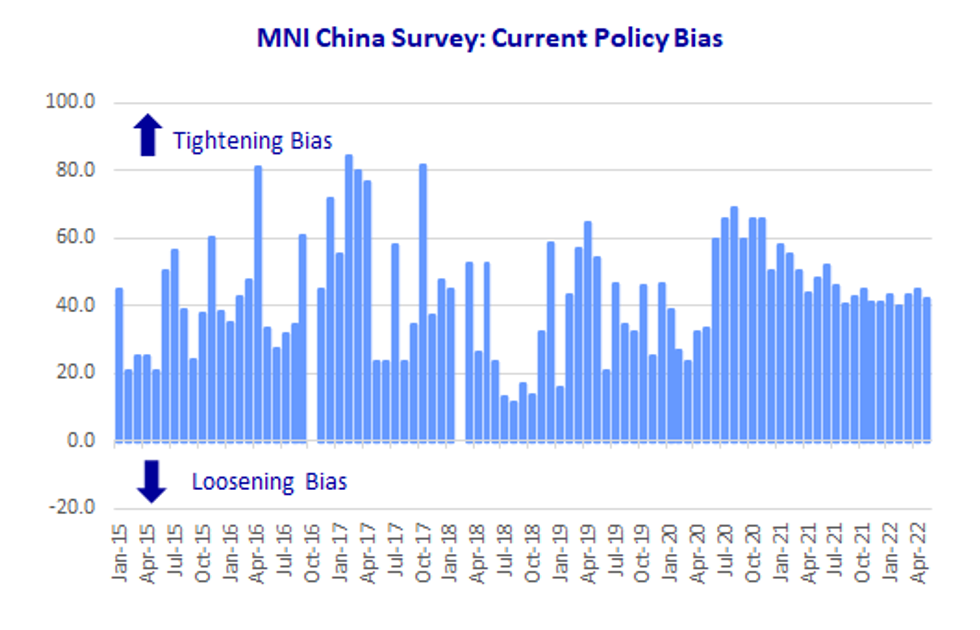

PRUDENT TONE

The PBOC Policy Bias Index edged down to 42.2 in May from in 45.0 April, with 84.4% of the participants seeing policy remaining on hold.

“Current monetary policy will keep stabilizing growth and ensuring employment as the primary goal,” a trader with a leading commercial bank in Zhejiang said.

“The PBOC is focused on guiding the release of credit demand rather than letting the market form looser monetary policy operation expectations,” a Beijing based trader commented.

“The move aims to reduce the comprehensive financing costs of enterprises, to promote the resumption the production in the context of the impact of the epidemic on economic activity.” The Beijing trader added.

The central bank lowered the 5-year Loan Prime Rate (LPR) by 15 bps to 5.45% and maintained the 1–year LPR at 3.7% on May 20, the second cut in five months.

The Guidance Clarity Index stood at 59.4 in May, picking up from the previous 53.3. The continued high level of the reading underlines a satisfaction in the market in understanding the central bank’s actions.

RATES DIVERGE

The 7-Day Repo Rate Index slipped to 40.6 from 53.3, with rates expected to decline due to the abundance of funds. The 7-day weighted average interbank repo rate for depository institutions (DR007) closed at 1.5435% Tuesday.

The 10-year CGB Yield Index was 65.6 in May, up from 53.3 in April, with 40% of respondents seeing higher yields ahead.

The MNI survey collected the opinions of 32 traders with financial institutions operating in China's interbank market, the country's main platform for trading fixed income and currency instruments, and the main funding source for financial institutions. Interviews were conducted May 9 – May 20.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.