Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

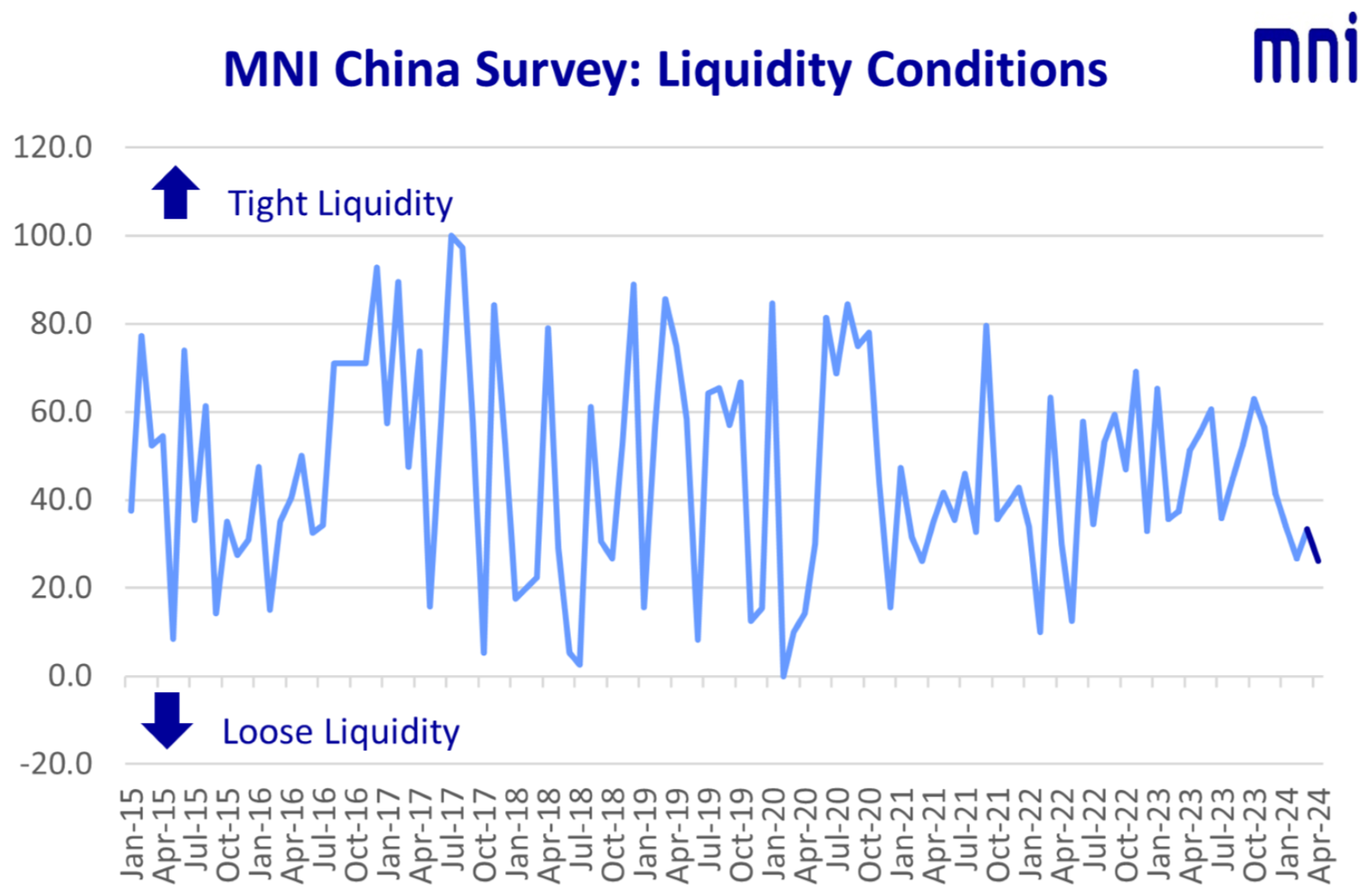

China’s interbank market liquidity reached a 22-month-high in April, leading the PBOC to net-drain for the second consecutive month, the latest MNI Liquidity Conditions Index showed.

“Liquidity is ample, authorities have reduced using 7-day reverse repos injections and kept a relatively low open market operation volume of CNY2 billion to avoid excess funds,” a Shanghai trader told MNI.

Interest rates on one-year AAA negotiable certificates of deposit (NCDs), a measure of short-term interbank lending costs, fell to 2.00% on April 22, below the PBOC’s MLF rate of 3.45%, indicating abundant liquidity.

The MNI China Liquidity Condition Index read 26.2 in April, down from last months’ 33.3, with 52.4% of traders reporting looser conditions. A lower Index reading implies more liquidity.

Zou Lan, head of the monetary policy department at the PBOC, told reporters last Thursday the regulator will strengthen monitoring of idle funds as some bank lending has exceeded the effective needs of the real economy.

“Less use of the MLF reflects ample liquidity – the PBOC has avoided injecting excessively into the system,” a trader in Jiangsu said.

The PBOC conducted CNY100 billion in 1-year MLFs on Aprik 15, draining CNY70 billion after offsetting maturities of CNY170 billion, marking the second straight month of draining after 15 months of net injection. The PBOC drained net CNY990 billion via its open market operation as of April 23, MNI calculated.

ECONOMY

The Chinese economy grew by 5.3% y/y, or 1.6% q/q, in Q1, beating the 4.6% forecast and accelerating from 2023's 5.2% growth, with the MNI China Economy Condition Index rising 57.1 in April, from 54.8 previously, with 40.5% of traders noting an improvement.

“The Q1 economy continued recovering, but real estate investment remained down, and infrastructure investment slowed. Also, data showed financing demand needs more support,” a senior trader based in Beijing told MNI.

China’s manufacturing investment is set to maintain strong growth throughout the year thanks to policy stimulus, but Beijing will push back against making any major concessions in response to accusations of “overcapacity”. (See MNI: Stimulus Seen Boosting China Manufacturing, Overcapacity, MNI: China Overcapacity Rejected, Cooperation Likely)

RATE CUTS

Regarding the likelihood of Q2 interest rate cuts, 42.9% of traders believed the PBOC would not lower rates, while 40.5% expected easing moves, the survey showed.

“Rate cuts may not be a best option in the short term, the spread between overseas and domestic rates as well as between deposit and loans is restricting authorities,” a Beijing trader told MNI.

The MNI China 7-Day Repo Rate Index slid to 46.4 in April, with 28.6% of participants expecting an upward curve, and 35.7% holding the opposite view.

The MNI China 10-year CGB Yield Index read 28.6, down from 32.1, marking the fifth straight monthly fall, with 47.6% traders predicting the yield dipping further.

As MNI has reported, the PBOC will continue to monitor the longer-dated Chinese government bond market, adding supply and control over leverage to help guide the yield closer to the present 2.5% one-year medium-term lending facility rate,. (See MNI: PBOC Wary Of Rapid Long-dated CGB Yield Decline

China is also likely to issue a significant volume of ultra long-term special treasury bonds with tenors of 30 years to support government investment. (See MNI INTERVIEW: China Eyes Significant Special Treasury Issuance)

Click below for the full report:

MNI China Liquidity Index April 2024.pdf

For full database history and full report on the MNI China Liquidity Index™, please contact:sales@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.