Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Australia’s labour market remained tight in June and Q2, and apart from the uptick in the unemployment rate, showed little easing. RBA-dated OIS is sitting flat to 3bps firmer across meetings. Terminal rate expectations have jumped to 4.43% from 4.39% before the data. For reference, the expected terminal rate saw a peak of 4.52% in late June. The A$ has outperformed on crosses.

- Treasury futures have edged lower through the session after it was announced Biden has covid and had cancelled some upcoming appearances, we currently trade at session's worst levels.

- Asian equities are lower today led by a sell-off in technology stocks. We should start to get headlines filtering out of the China Third Plenum soon.

- Later the Fed’s Goolsbee, Logan and Daly appear and the ECB announces its decision (no change expected). There are US jobless claims and July Philly Fed, and UK labour market data.

MARKETS

GLOBAL: June Inflation Results Generally In Right Direction

While prices remain above central bank targets in many countries, they are heading in the right direction given restrictive monetary policy. This is making many MPCs more confident that their next move in rates will be down with the ECB and Bank of Canada already having cut. The first Fed easing is now fully priced in for September and expectations for the RBNZ have been brought forward to later this year. However, the BoJ is expected to hike again later this year, while there is a risk of another RBA increase.

- OECD headline inflation looks set to have moderated further in June with most countries reporting a decline and if not it has been stable. Core has been more mixed though with the US lower, Canada higher and the euro area and UK steady, and it is above headline in many counties due to persistent domestic inflation pressures. Australia’s data prints on July 31 but core has stopped moderating and is running well ahead of the US and euro area.

Source: MNI - Market News/Refinitiv/ABS

- Non-Japan Asian headline and core inflation have been fairly stable since March. Very low inflation in China has weighed on the aggregate, with only Thailand posting lower core. Excluding China June headline remained around 3.6% y/y, for the fourth straight month, and core at 1.9% y/y within most target bands. Rate cuts are expected once the Fed begins easing so as to maintain FX stability.

Source: MNI - Market News/Refinitiv/IMF

- Japan’s June CPI is out on Friday and Bloomberg consensus has both headline and core ticking up. The BoJ was well behind the rest of the world in starting its tightening cycle with the first move in March. Another hike is fully priced in for the September meeting though with just over 50% for July.

GLOBAL: Some Global Inflation Influences Turn

The moderation in headline inflation stalled in the year to May but the OECD countries we have for June saw some further improvement but core was mixed. Non-Japan Asian headline and core aggregates were little changed in May and June. Factors that pressured inflation lower have stabilized or are now inflationary, such as shipping costs and oil.

- Shipping costs were disinflationary until the start of 2024 and have become more inflationary over Q2 as continued Houthi attacks and capacity constraints push up prices. Global container rates remain below 2021’s peak but the July average is up 296% y/y while the Baltic Freight index is +87.4% y/y.

Source: MNI - Market News/Refinitiv

- Oil prices have added upward pressure to headline inflation in 2024 with Brent up 6.6% y/y but they fell on the month in May and June after rising the previous four months. The July average is up 3% m/m but prices have been volatile.

- The New York Fed June global supply chain pressure index is around neutral signaling little impact on inflation in the months ahead. It has been disinflationary for over a year.

- June FAO food prices were flat after rising for the previous 3 months. They are still down 2.1% y/y but their downward pressure on inflation is significantly less than it was in H1 2023 when they troughed at -21.5% y/y in May. Rice prices have been a problem for Asia but they fell in June and are down 1.2% m/m in July to date after rising sharply in May. Harvests are helping to increase supply but processed rice prices are still +19.8% y/y. Oils and dairy have positive annual inflation.

- Metals were higher in Q2 after falling, while iron ore has declined over 2024. Wool prices continue to fall. The GS commodity index is headed for its third straight decline in July and is now up only 1.4% y/y.

Source: MNI - Market News/Refintiv

US TSYS: Tsys Edge Lower Ahead of Jobless Claims, Biden Tests Covid Positive

- Treasury futures have edged lower through the session after it was announced Biden has covid and had cancelled some upcoming appearances, we currently trade at session's worst levels with TUU4 is -0-01¾ at 102-18+ while TYU4 is currently -0-05+ at 111-08+

- Post NY close Former Fed Dallas President Kaplan said he anticipates the Fed may reduce interest rates in September and possibly again in December, but does not expect it to initiate a prolonged rate-cut cycle due to high fiscal deficits and energy prices.

- The cash treasury curve has bear-flattened today, the 2y yield is 1.9bps higher while the 10y is currently trading 1.5bps higher.

- Earlier, Biden was confirmed to have covid, this follows comments he made saying he would potentially drop out if diagnosed with a "medical condition". The betting markets have swung again post this news with Kamala jumping 28pts to 50%, while Biden has dropped 31pts to 38% chance of being the Democratic Party nominee.

- Projected rate cut pricing into year end slightly cooler vs. late Tuesday levels (*): July'24 at -6.5% w/ cumulative at -1.6bp at 5.313%, Sep'24 cumulative -25.7bp (-26.6bp), Nov'24 cumulative -41.1bp (-42.9bp), Dec'24 -63.6bp (-65.4bp).

- Focus turns Weekly Claims, 10Y TIPS Sale & TIC Flows.

JGBS: Cash Bonds Twist-Flatten, National CPI Tomorrow

JGB futures are weaker but well off session lows, -16 compared to the settlement levels.

- Outside of the previously outlined Trade Balance data, there hasn't been much in the way of domestic drivers to flag.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session, with a slight flattening bias.

- Earlier, Biden was confirmed to have COVID-19, this follows comments he made saying he would potentially drop out if diagnosed with a "medical condition". The betting markets have swung again after this news with Kamala jumping 25pts to 47%, while Biden has dropped 26pts to 44% chance of being the Democratic Party nominee.

- The cash JGB curve has twist-flattened, pivoting at the 20s, with yields 1.5bps higher to 1.5bps lower. The benchmark 10-year yield is 0.6bps higher at 1.047% versus the cycle high of 1.108%.

- The swaps curve has bear-steepened, with rates flat to 3bps higher. Swap spreads are wider.

- “Japan sold ¥349.60 billion of 5-year climate transition notes in line with expected cut-off yield with higher bid-to-cover ratio (4.04x) than the previous auction (3.39x), signalling solid investor demand.” (as per BBG)

- Tomorrow, the local calendar will see National CPI data.

JAPAN DATA: Export Growth Softens, Volumes To Europe Down 20% Y/Y

Japan June trade figures showed weaker than expected export and import growth. Exports were +5.4% y/y, against a +7.2% forecast and +13.5% prior outcome. Imports were +3.2%y/y, against a +9.6% forecast, which was also close to the prior outcome. The headline trade position was better than expected at ¥224bn, (

-¥185.7bn forecast. The seasonally adjusted trade deficit of -¥816.8bn was close to expectations.

- Export growth has largely tracked sideways in y/y terms since the start of the year, although this is the weakest prince since Nov 2023. In volume terms, exports were -6.2% y/y, the weakest print since early last year.

- By country, EU export volumes are down -20.1%y/y and running negative to the US and China. Nominal outcomes were more positive for the US (+11% y/y) and China (+7.2%y/y), which were aided by the weaker yen. We still saw a negative outcome to the EU (-13.4%y/y) in nominal terms.

- Given yesterday's reports around potential chip export curbs to China, as the US considers fresh restrictions in the space, the country breakdown of export trends will be an on-going watch point.

- The seasonally adjusted trade balance looks liked it peaked in January of this year.

AUSTRALIAN DATA: Economy Strong Enough To Create Work, Some Signs Of Easing In Q2

The June and Q2 jobs data showed that there was only a slight further easing of the labour market and that the economy is strong enough to create almost enough jobs to cover the strong rise in the labour force (see MNI Economy Strong Enough To Absorb Bulk Of Labour Force Entrants). This increases the risk of another rate hike, especially if Q2 CPI prints around 1%q/q on July 31. A number of indicators that the RBA looks at stabilized in Q2 though.

- The unemployment rate rose only 0.1pp to 4% in Q2 from 3.9%, in line with the RBA’s May forecast. Underemployment though was 6.6% unchanged from Q1 and the June result was lower at 6.5%. Both rates were still 0.6pp higher than their cycle troughs, signaling some easing in conditions.

- Underemployment fell in June due to a 0.8% m/m rise in hours worked. Q2 rose 1.6% q/q after 0.2% in Q1, another sign that demand is strong enough to need more labour input.

Source: MNI - Market News/ABS

- The RBA likes to look at the youth unemployment rate, as it is often a lead indicator of other labour market trends. It averaged 9.7% in Q2 up 0.3pp. June fell 0.2pp to 9.5% though, lowest since February, to be 2.3pp higher than the mid-2022 trough, signaling material easing but the level remains historically low.

Source: MNI - Market News/ABS

- Vacancies/unemployment continues to moderate with the ratio falling 4.5pp in Q2 to 58.3%, while it is down 23.8pp over the year it remains over double the average in the 10 years to end 2019.

- The quarterly NAB business survey for Q2 is out on July 25 and includes availability of suitable labour as a severe output constraint. In Q1 it was 22pp below the Q3 2022 peak.

AUSTRALIAN DATA: Economy Strong Enough To Absorb Bulk Of Labour Force Entrants

Australia’s labour market remained tight in June and Q2, and apart from the uptick in the unemployment rate, showed little easing. While the number of unemployed rose in Q2, quarterly employment growth was only down slightly so that 80% of the increase in the labour force found a job. Given the stage in the cycle and restrictive monetary policy, this is a strong result. In addition, hours worked rose in Q2 driving underemployment down and the participation rate is close to highs. Strong Q2 increases the risk of an August hike if Q2 CPI prints at 1% or above.

- The June unemployment rate ticked up to 4.05% from 4.00% leaving Q2 only 0.1pp higher than Q1 due to a 32.5k increase in unemployed. The labour force grew by 158.3k in Q2 while there were 125.8k new jobs (Q1 +128.3k). Without the increase in labour supply from immigration, it is likely that the unemployment rate would have remained under 4% this year.

Source: MNI - Market News/ABS

- The NAB business survey is pointing to a sharp reduction in labour demand though, but the jobs data is yet to reflect this.

- June employment printed higher than expected at 50.2k after 39.5k with full-time (FT) driving the increase at +43.3k compared with part-time (PT) +6.8k. Employment growth is now at 2.8% y/y with 3-month momentum 3.3% annualized. PT momentum had been outpacing FT earlier in the year but they are now in line suggesting that employers are feeling more confident about the economic outlook.

- Hours worked rose 0.8% m/m in June to be up 1.4% y/y and Q2 saw a rise of 1.6% q/q after 0.2% in Q1. FT hours momentum outpaced PT in May/June. The quarterly result is likely to weigh on Q2 productivity growth when it is published on September 4. June hours were lower due to illness and increased annual leave.

Source: MNI - Market News/ABS

AUSSIE BONDS: Holding Cheaper After Jobs Beat, Nov-27 Supply Tomorrow

ACGBs (YM -4.0 & XM -2.0) are holding 3-5bps cheaper than pre-Employment data levels.

- Australia's June employment increased by 50,176 month-over-month, exceeding the estimated 20,000. The June jobless rate remained steady at 4.1%, matching expectations. Full-time employment rose by 43,327, while part-time employment increased by 6,849. The participation rate in June was 66.9%, slightly above the estimated 66.8%.

- Given the stage in the cycle and restrictive monetary policy, this is a strong result. In addition, hours worked rose in Q2 driving underemployment down and the participation rate is close to highs. Strong Q2 increases the risk of an August hike if Q2 CPI prints at 1% or above.

- The cash ACGB curve has twist-flattened, with yields 2bp higher to 1bp lower. The AU-US 10-year yield differential is +7bps.

- Swap rates are flat to 3bps lower, with the 3s10s curve flatter and EFPs wider.

- The bills strip has bear-flattened, with pricing flat to -3.

- RBA-dated OIS is sitting flat to 3bps firmer across meetings. Terminal rate expectations have jumped to 4.43% from 4.39% before the data. For reference, the expected terminal rate saw a peak of 4.52% in late June.

- The local calendar is empty tomorrow.

- Tomorrow, the AOFM plans to sell A$700mn of the 2.75% Nov-27 bond.

AU STIR: RBA Dated OIS Slightly Firmer After Jobs Data Beat

RBA-dated OIS is sitting flat to 3bps firmer across meetings after today’s domestic data drop.

- Australia's June employment increased by 50,176 month-over-month, exceeding the estimated 20,000.

- The June jobless rate remained steady at 4.1%, matching expectations.

- Full-time employment rose by 43,327, while part-time employment increased by 6,849. The participation rate in June was 66.9%, slightly above the estimated 66.8%.

- Terminal rate expectations have jumped to 4.43% from 4.39% before the data. For reference, the expected terminal rate saw a peak of 4.52% in late June.

Figure 1: RBA-Dated OIS – Today Vs. Yesterday

Source: MNI – Market News / Bloomberg

NZGBS: Post-CPI Sell-Off Unwound, 65bps Of Easing Priced By Year-End

NZGBs closed at the session's best levels, with benchmark yields 4bps lower. Local participants seemed content to overlook the 1-2bp cheapening in US tsys during today’s Asia-Pac session and yesterday’s modest bear flattening.

- Today's move effectively unwound the sell-off triggered by yesterday’s Q2 CPI print. As a result, NZGB benchmark yields remain 28-35bps lower than pre-RBNZ decision levels, with the 2/10 curve 6bps steeper.

- The NZ-US 10-year yield differential has narrowed by 4bps to +18bps, its tightest level since late 2022. This differential has oscillated between +20 and +80bps since late 2022.

- Today’s weekly supply was well absorbed with cover ratios printing 2.5x to 3.3x.

- Swap rates closed 4-5bps lower, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed little changed on the day but remains 18-46bps softer than pre-RBNZ decision levels. The market is pricing a 39% chance of a cut in August, and a 79% chance of a cut by October. A cumulative 65bps of easing is priced by year-end.

- Tomorrow, the local calendar is empty.

NZ BONDS: NZ-US 10Y Differential Narrows To Tightest Level Since Late-2022

The NZ-US 10-year yield differential has narrowed by 4bps to +18bps, its tightest level since late 2022. This differential has oscillated between +20 and +80bps since late 2022.

- The recent narrowing in the 10-year yield differential has been primarily driven by a narrowing in the NZ-US 3-month swap rate 1-year forward (1Y3M) spread, which has narrowed more than 160bps since its cyclical high in mid-2023.

- The 1Y3M differential is a proxy for the expected relative policy path over the next 12 months.

- A simple regression of the AU-US cash 10-year yield differential against the AU-US 1Y3M swap differential over the current tightening cycle indicates that the 10-year yield differential is currently close to fair value (i.e., +18bps versus +21bps).

Figure 1: NZ-US 10-Year Yield Differential

Source: MNI – Market News / Bloomberg

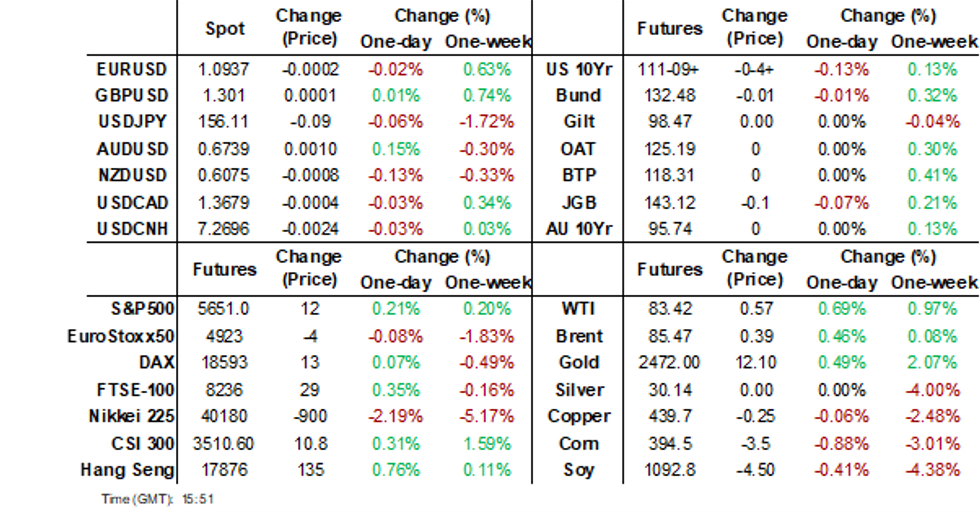

FOREX: USD/JPY Rebounds 100pips From Earlier Lows, A$ Outperforms As Jobs Data Stokes RBA Fears

Outside of AUD gains (post better than expected jobs data), the USD has ticked up against most of the majors. The BBDXY has edged back above 1248, against earlier lows of 1246.65. Yen volatility has been the other focus point.

- USD/JPY was biased lower in early trade, touching 155.38, which was a fresh lows back to early June. However, we now sit around 100pips higher, last around 156.40/45, slightly up in USD terms versus end NY closing levels from Wednesday.

- There didn't appear to be a fresh catalyst for the early morning move other than a continuation of USD/JPY's sharp reversal which kicked off late in Asia Pac trade on Wednesday. Futures volumes were firmer in early trade before subsiding somewhat. Note 154.55 was the June 4 low. The 50-day EMA is back near 157.90

- The A$ has outperformed on crosses, with AUD/JPY rebounding back to 105.4, against earlier lows of 104.53. This likely helped USD/JPY rebound. The June Australian jobs data showed a fairly resilient labour market for Q2, with jobs growth largely matching the pace of new entrants to the labour market. This is keeping the door ajar for a potential RBA rate hike in coming months.

- AUD/USD sits up at 0.6735, modestly firmer for the session. The AUD/NZD cross has regained ground back near 1.1100, pre data lows were just under 1.1060. NZD/USD is off to 0.6070, down 0.20%, but still above recent lows.

- Later, the ECB is seen on hold. We have Fed speak from Goolsbee, Logan and Daly. On the data front, US jobless claims and July Philly Fed, and UK labour market data are all due.

ASIA STOCKS: HK & China Equities Off Earlier Lows, Tech & Small Caps Lag

China & Hong Kong equities are mixed today. China equities are off earlier lows although concerns remain over regulatory tightening and economic recovery, AI stocks dropped after a report that the nation’s cyberspace regulator has asked for mandatory reviews of such models, while there are also concerns about the possibility of more severe US trade restrictions, particularly on the technology sector. These factors, combined with a lack of updates or headlines out of the Third Plenum have left investors cautious.

- Hong Kong equities are mixed with the HSTech Index is 0.65% lower while property is performing better with the Mainland Property Index is 0.60% higher, the HS Property Index is 0.20% higher while the HSI has pared already losses to trade 0.20% higher.

- China equity markets are also mixed today, small-cap indices are the worst performing with the CSI 1000 down 0.80%, the CSI 2000 down 1.50%, while the Beijing Stock Exchange Index is down 3.30% after a large rally on Wednesday while the large-cap CSI 300 is 0.12% higher.

- JD Vance, Donald Trump's running mate, has articulated a range of policy views, particularly critical of China. Vance has emphasized the need for the US to focus its military resources on China, arguing that the country poses a significant threat, especially regarding a potential invasion of Taiwan, which he believes would be catastrophic for the US economy due to Taiwan's crucial role in semiconductor manufacturing, per bbg.

- Xi Jinping is set to unveil his long-term economic vision, focusing on technology-driven "high-quality growth" and "Chinese-style modernization" at the conclusion of the Third Plenum. This meeting comes amid weak economic growth, a prolonged real estate crisis, and deflationary pressures. While specifics remain unclear, expected reforms include overhauling the consumption tax, reforming the hukou system, and boosting artificial intelligence. Measures to support the electric car and green energy sectors are also anticipated.

- Looking ahead, focus will again be on any headlines from the Third Plenum

ASIA PAC STOCKS: Asian Equities Head Lower As Tech Stocks Sell Off

Asian equities are lower today led by a sell-off in technology stocks extending the decline for second day amid concerns follows news that the Biden administration may impose stricter trade curbs on companies supplying advanced chip technology to China. Tokyo Electron led the losses, falling as much as 11%, significantly impacting the MSCI Asia Pacific Index, while shares in Samsung and TSMC also saw notable declines. Australia reported employment data earlier, showing a jump in jobs, while the unemployment rate held steady.

- Japanese equities have faced significant declines this morning, driven primarily by heightened concerns over potential tighter US restrictions on semiconductor sales to China. Tokyo Electron saw a sharp drop of nearly 11%, marking its worst two-day loss since 2008. These declines mirrored the selloff in US and European semiconductor stocks, particularly following news that the Biden administration may impose severe trade restrictions on companies like Tokyo Electron and ASML Holding NV if they continue providing advanced chip technology to China. Additionally, broader concerns over a stronger yen, which has reached its highest levels since early June further pressured Japanese exporters, the Topix is trading 1.15% lower while the Nikkei 225 2.11% lower.

- South Korean equities have experienced declines this morning, heavily influenced by fears over the potential imposition of stricter US semiconductor sales restrictions to China. Currently the Kospi is 1.40% lower, while the Kosdaq trades 1.37% lower.

- The Taiwanese equity market has gapped lower this morning also driven by heightened concerns over the potential for stricter U.S. semiconductor sales restrictions to China. Comments from Trump have added to the uncertainty, while investors remain cautious ahead of TSMC’s earnings report due out later today, which is expected to provide further insights into the sector's outlook amid the current geopolitical climate, currently TSMC is 3.10% lower while the Taiex is down 2.10%.

- Australian equities are slightly lower today, with the ASX 200 down 0.30%. Earlier, Australia's labor market showed resilience with the economy adding 50.2k jobs vs 20k expected, the participation rate rose to 66.9% from 66.8% while the unemployment rate came in at 4.051% (4.1% rounded) with estimates of 4.1%.

- Elsewhere, New Zealand equities are little changed, Singapore equities are 0.65% lower, Malaysian equities are 0.10% lower, Philippines equities are 0.10% lower while Indonesian equities are 1% higher and Thailand equities are 0.35% higher.

ASIA EQUITY FLOWS: Investors Dump Semiconductor Stocks On Trade Restriction Concerns

- South Korea: South Korean equities saw outflows of $200m yesterday, contributing to a net outflow of $4m over the past five trading days. Similar to Taiwan, SK has been hit with a sell-off in the semiconductor space recently The 5-day average inflow is -$1m, significantly lower than the 20-day average of $138m and the 100-day average of $119m. Year-to-date, South Korea has experienced substantial inflows totaling $19.41b.

- Taiwan: Taiwanese equities had significant outflows of $806m yesterday, resulting in a net outflow of $2.75b over the past five trading days. Semiconductor names have been heavy sold recently, and with the Biden administration proposing more trade restrictions on any company that provides advanced semiconductor tech to China expect flows in the region to remain negative. The 5-day average flow is -$550m, considerably lower than the 20-day average of -$257m and the 100-day average of -$28m. Year-to-date, Taiwan has accumulated inflows of $846m.

- India: India equity markets were closed on Wednesday for Moharrum.

- Indonesia: Indonesian equities recorded outflows of $5m yesterday, resulting in a net inflow of $84m over the past five trading days. The 5-day average is -$17m, below the 20-day average inflow of $16m and the 100-day average of -$8m. Year-to-date, Indonesia has experienced outflows totaling $199m.

- Thailand: Thai equities saw inflows of $19m yesterday, contributing to an outflow of $11m over the past five trading days. The 5-day average is -$2m, slightly better than the 20-day average of -$22m and the 100-day average of -$24m. Year-to-date, Thailand has seen significant outflows amounting to $3.34b.

- Malaysia: Malaysian equities experienced inflows of $51m yesterday, contributing to a 5-day net inflow of $217m. The 5-day average inflow is $43m, higher than the 20-day average inflow of $8m and the 100-day average outflow of -$2m. Year-to-date, Malaysia has experienced minor inflows totaling $147m.

- Philippines: Philippine equities saw inflows of $12m yesterday, with a 5-day net inflow of $22.3m. The 5-day average inflow is $4m, better than the 20-day average inflow of $0m and the 100-day average outflow of -$7m. Year-to-date, the Philippines has seen outflows totaling $502m.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | -200 | -4 | 19406 |

| Taiwan (USDmn) | -806 | -2751 | 846 |

| India (USDmn)* | 399 | 1528 | 3044 |

| Indonesia (USDmn) | -5 | 84 | -199 |

| Thailand (USDmn) | 19 | -11 | -3335 |

| Malaysia (USDmn) | 51 | 217 | 147 |

| Philippines (USDmn) | 12 | 22.3 | -502 |

| Total | -529 | -914 | 19407 |

| * Up to 15th July |

OIL: Crude Continues Climb Following US Stock Build Data

Oil prices continued to climb higher during APAC trading today after they rose sharply on Wednesday following EIA data showing the third straight US crude inventory drawdown. WTI is up 0.6% to $83.34/bbl off the intraday high of $83.53 to be up 2.2% this month. Brent is 0.4% higher at $85.42/bbl following a high of $85.63 but is only up 0.5% in July. The softer USD boosted oil yesterday and today the index is little changed.

- EIA reported US crude inventories fell 4.87mn last week. This is the third straight weekly drawdown worth 20.47mn barrels in total and bringing the level to its lowest since February and below the 5-year seasonal average.

- The Brent prompt spread has widened, signaling that the market remains tight, according to Bloomberg. Expectations for a Fed rate cut in September are improving the demand outlook.

- China’s Customs General Administration reported that June oil import volumes fell 10.7% y/y down from May’s -8.7% y/y. Product imports fell 32.4% y/y after -3.6% but export volumes rose 19% y/y up from 9.5% driven by diesel and kerosene. .

- Later the Fed’s Goolsbee, Logan and Daly appear and the ECB announces its decision (no change expected). There are US jobless claims and July Philly Fed, and UK labour market data.

GOLD: Hovering Just Below Fresh All-Time High

Gold is 0.4% higher in today’s Asia-Pac session, after closing 0.4% lower at $2458.79 on Wednesday.

- This came after bullion hit a fresh all-time high of $2,483.73/oz early in yesterday’s session.

- Gold is up nearly 20% since January, with much of this year’s gains fueled by large purchases from central banks, strong consumer appetite in China and demand for haven assets amid geopolitical tensions.

- Fed speak from Richmond Fed Barkin and Fed Gov Waller leaned dovish. “While I don’t believe we have reached our final destination, I do believe we are getting closer to the time when a cut in the policy rate is warranted,” Waller said.

- Lower rates are typically positive for gold, which doesn’t pay interest.

- According to MNI’s technicals team, the trend condition in gold remains bullish and the breach of key resistance at $2450.1, the May 20 high, this week opens the $2500.00 handle next.

- Analysts note that with positioning and sentiment not at extreme levels, this level could be tested soon enough.

ASIA FX: THB & IDR Trim Recent Gains, USD/JPY Rebound Curbs Gains Elsewhere

USD/Asia pairs are higher for the most part, although gains are fairly modest at this stage. Regional equities have been a drag, with most major indices tracking lower following sharp tech led losses in US markets on Wednesday. The USD has also steadied against the majors, with an earlier USD/JPY dip completely reversed. IDR and THB spot have been the weakest performers, while PHP FX is marginally higher. Later on we should start to get Third Plenum headlines emerge out of China. Tomorrow a press conference is scheduled.

- USD/CNH is near 7.2730 in latest dealings, little change for the session. Onshore spot sits under 7.2600. We did have a down tick in the fixing earlier (sub the 7.1300 handle for the first time since July 8). USD/CNH has mostly followed USD/JPY gyrations, although with a continued low beta. Local equities are mixed but showing modest overall moves. markets await Third Plenum details.

- Spot USD/KRW couldn't hold sub 1380 from earlier dealings. The turnaround in USD/JPY (which recouped earlier losses), along with equity losses, weighed on the won at the margin. The Kospi is off 1.4%. The authorities have vowed to stabilize the property market.

- USD/THB has firmed in early Thursday dealings, the pair last around 35.95/00, close to 0.25% weaker in THB terms. Intra-session lows from Wednesday trade came in at 35.82, fresh lows in the pair back to mid March of this year. The RSI (14), which breach oversold conditions (albeit just), yesterday. This may have encouraged some position squaring in light of recent baht gains. Cross asset moves in terms of regional equity weakness is also likely to be playing a role, while gold prices sit modestly off recent highs. Onshore equities have turned lower in recent sessions. US yields have shown some stability in the first part of trade today as well.

- USD/IDR has rebounded in the first part of Thursday dealings, last near the16160 region. This is around 0.35% weaker in IDR terms versus yesterday's onshore close (16100). Yesterday's lows just under this level, and levels last seen in late May of this year. Topside momentum could see a test of the 50-day EMA (around 16195), although the broader backdrop for the pair still looks to be skewed towards fading upticks, amid a shifting Fed backdrop. As expected, the BI held rates steady late yesterday. The bias is to cut but FX stability remains key. The central bank wants to attract inflows, but this may be dependent on when the Fed cuts and by how much this year. The other watch point for offshore investors will be the fiscal outlook. It was announced today that incoming President Prabowo's Nephew will become the Deputy Finance Minister per RTRS.

- USD/PHP has bucked these firmer trends, the pair last under 58.25, which is back near recent lows. Yesterday the BSP announced a step up in FX regulations.

Asia Sovs Tracks US Tsys, BI Unchanged, PH President's Approval Falls

Asian EM sovs yields are flat to 2bps higher and largely track moves in the US Tsys markets with slightly better selling through the belly of the curves. Local currency Philippines debt has outperformed Indonesian debt recently with the divergence in central bank policies with BSP on track for a rate cut as early as August, while fiscal deficit and currency concerns weigh on Indonesian bonds, BI kept rates on hold on Wednesday.

- Philippines inflation continues to fall and now sits at 3.9% from a peak of nearly 9% early last year, while concerns grow over increased planned spending by President-elect Prabowo Subianto’s administration with some reports they are considering scrapping a ceiling on the deficit are adding to market jitters.

- Bank Indonesia opted to keep its benchmark rate steady at 6.25%, alongside unchanged rates for its overnight deposit facility and lending facility. The decision reflects the central bank's focus on maintaining inflation within a target range of 1.5% to 3.5% and stabilizing the rupiah through exchange-rate stabilization measures. Growth forecasts for Indonesia in 2024 are estimated between 4.7% and 5.5%, supported primarily by robust domestic demand.

- Front-end yields have tighten about 2bps verses US Tsys, while the US-ID 10yr spread has widen 1bps, US-PH 10yr spread is little changed.

- In local politics, Philippine President Ferdinand Marcos Jr.'s approval rating declined slightly in June, to 53%. This comes amid a political rift following Vice President Sara Duterte's resignation, despite her approval rating rising to 69%. The survey highlights tensions within their political alliance and sets the stage for a potential electoral contest between the Marcos and Duterte families in 2025.

- Cross-asset: In FX markets the BBDXY is steady while the IDR has slipped a touch this morning to 16,158 down 0.35%, while the PHP has strengthen a touch, up 0.05% to 58.293. Global tech stocks have been hit recently as trade restrictions and geopolitical tension rise, both the JCI up 1% & PSEi down 0.10 look to have missed this sell-off largely due to their small reliance on tech companies in their indices.

- Looking ahead, Philippines has BoP Overall on Friday.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/07/2024 | 0600/0700 | *** |  | UK | Labour Market Survey |

| 18/07/2024 | - |  | US | ECB Meeting | |

| 18/07/2024 | 0900/1100 | ** |  | EU | Construction Production |

| 18/07/2024 | 1215/1415 | *** | | EU | ECB Deposit Rate |

| 18/07/2024 | 1215/1415 | *** | | EU | ECB Main Refi Rate |

| 18/07/2024 | 1215/1415 | *** | | EU | ECB Marginal Lending Rate |

| 18/07/2024 | 1230/0830 | *** | | US | Jobless Claims |

| 18/07/2024 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 18/07/2024 | 1230/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 18/07/2024 | 1245/1445 | | EU | ECB Monetary Policy Press Conference | |

| 18/07/2024 | 1415/1615 | | EU | ECB's Lagarde presents MonPol decision on podcast | |

| 18/07/2024 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 18/07/2024 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 18/07/2024 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 18/07/2024 | 1605/1205 | | US | San Francisco Fed's Mary Daly | |

| 18/07/2024 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 10 Year Note |

| 18/07/2024 | 1745/1345 | | US | Dallas Fed's Lorie Logan | |

| 18/07/2024 | 2000/1600 | ** | | US | TICS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.