Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- President Biden has cut short his scheduled trip to Asia this week as discussions over the US debt ceiling remain ongoing. Biden noted that the latest round of talk was productive. Tsys firmed after Asia participants digested this morning's Fedspeak, Goolsbee and Bostic think that the Fed should pause at its June 14 meeting to allow time to assess the impact of previous tightening.

- Elsewhere, ACGBs sit cheaper (YM -4.0 & XM -1.5) but 1-3bp stronger after the data drop despite the Q1 Wage price Index printing close to analyst expectations. NZGBs closed 8-9bp weaker, near session cheaps for the second consecutive day, as the market digested the prospect of a worse-than-expected debt profile in tomorrow’s Budget 2023 and another sell-side bank ups its terminal OCR expectation.

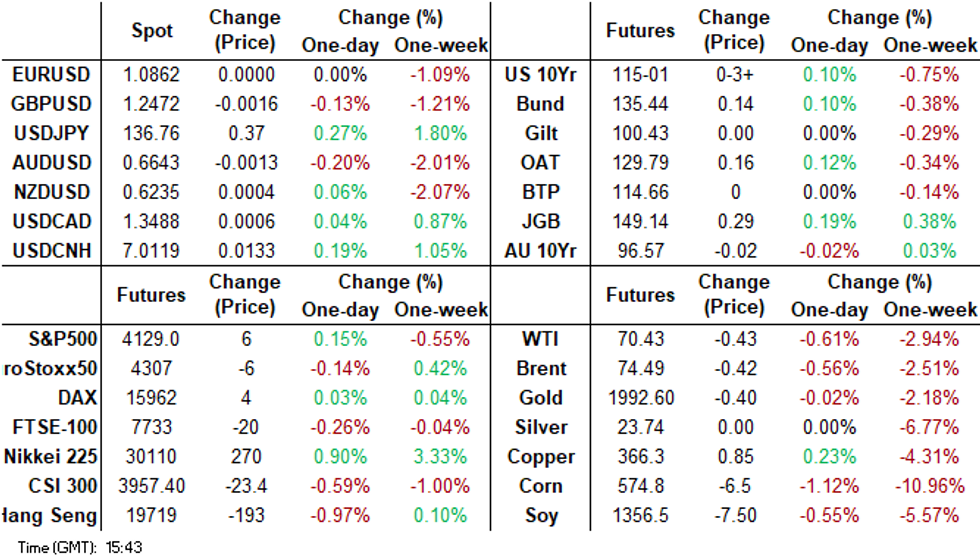

- In the FX space, much of the focus was on the breach of 7.00 by USD/CNH. This follows yesterday's weaker than expected April activity data, with some sell-side names lowering their 2023 GDP forecasts as a result. CNY option volumes rose, although USD/CNY has not breached 7.00 yet. USD/CNH risk reversals have spiked but remain below 2022 highs.

- In Europe today we have the final print of Eurozone CPI, further out US Housing Starts crosses.

MARKETS

US TSYS: Marginally Firmer In Asia

TYM3 deals at 115-01+, +0-04, a touch off the top of the observed 0-06 range on volume of ~62k

- Cash tsys sit 1-2bps richer across the major benchmarks, some light bull steepening is apparent.

- Tsys firmed after Asia participants digested this morning's Fedspeak, Goolsbee and Bostic think that the Fed should pause at its June 14 meeting to allow time to assess the impact of previous tightening but also the effect of higher banking funding costs on the economy.

- Spillover from a rally in JGBs, after a strong 20 Year auction, added a layer of support.

- Tsys held marginally richer for the remainder of the session with little follow through on moves dealing in narrow ranges.

- President Biden has cut short his scheduled trip to Asia this week as discussions over the US debt ceiling remain ongoing. Biden noted that the latest round of talk was productive.

- In Europe today we have the final print of Eurozone CPI, further out US Housing Starts crosses. We also have the latest 20-Year supply.

JGBS: Futures Stronger After 20-Year JGB Auction Shows Solid Demand

JGB futures are stronger in Tokyo afternoon trade, +27 versus settlement levels, reversing overnight weakness despite much stronger than expected Q1 GDP data.

- 20-year supply sees smooth digestion as the cover ratio shifts to the highest level in a year. Japanese investors, particularly domestic life insurers and pension funds, appear to be showing a trend of allocating capital to the super-long end of the JGB curve in response to elevated FX-hedging costs in the new fiscal year. The strong demand observed at the recent 30-year auction further supports this observation.

- At 149.12, JBM3 sits close to its highest level for May. Nonetheless, it remains positioned within a range of 147.92 (the upper limit of April's trading range) and 149.53 (the high point of March 22).

- Cash JGBs, beyond the 1-year zone, increase their richening in afternoon trading with yields 1.0-4.7bp lower and the yield curve flatter. The benchmark 10-year yield is 3.0bp lower at 0.367%. The 20-year yield is 4.0bp lower post-auction, sitting -4.7bp on the day at 0.966%.

- Swap rates are lower with the curve flatter and swap spreads generally wider for except the 4-7-year zone.

- The local calendar sees the release of April Trade and weekly International Security Flow data ahead of April National CPI data on Friday.

- Tomorrow also sees BoJ Rinban operations covering 1-10-year and 25-Year+ JGBs along with an auction of Y3.5tn 12-month bills.

AUSSIE BONDS: Cheaper, Slightly Stronger After WPI, Jobs Data Tomorrow

ACGBs sit cheaper (YM -4.0 & XM -1.5) but 1-3bp stronger after the data drop despite the Q1 Wage price Index printing close to analyst expectations. While the annual rate of 3.7% is at the highest level in over 10 years, it is still consistent with the inflation target. Worryingly for the RBA, however, the share of jobs receiving wage rises of between 4-6% rose to the highest level since 2009, according to the ABS.

- The latest round of ACGB Jun-35 supply saw smooth digestion with an increased cover ratio (3.6643x versus 2.2687x at the April 5 auction.

- Cash ACGBs are 1-3bp cheaper with the AU-US 10-year yield differential -4bp at -10bp.

- Swap rates are 1-3bp higher with the 3s10s curve flatter and EFPs unchanged.

- Bills are cheaper with pricing -1 to -4 but off worst levels.

- RBA dated OIS softens 2-3bp after the data but remains flat to 5bp firmer on the day across meetings with Apr’24 leading.

- The local calendar is slated to release the April Employment Report tomorrow with elevated job vacancies and strong immigration levels likely to deliver a robust employment outcome.

- Until then, the global calendar releases Euro Area CPI (Apr) and US Housing Starts (Apr) and Building Permits (Apr).

AUSTRALIAN DATA: Q1 Wages In Line But Some Concerning Trends

The Q1 Wage Price Index (WPI) was close to analysts’ expectations rising 0.8% q/q and 3.7% y/y after 0.8% and 3.4% the previous quarter. While it is at its highest annual growth rate in over 10 years, it is still consistent with the inflation target but there are a number of worrying details. The RBA is forecasting a peak in wages growth in Q4 2023 at 4%. This will be particularly dependent on the increase in the minimum wage and some awards from July 1, which will impact around a quarter of workers.

- The ABS observed that the highest wage growth since September 2012 reflected “low unemployment, a tight labour market and high inflation”. Since high inflation is now a driver of pay growth, developments will be monitored closely going forward.

- The ABS commented that “Wage outcomes over the March quarter 2023 saw a continued lift in the share of jobs receiving wage rises of between 4 and 6 per cent, which is the highest share since 2009.” Also the share of jobs receiving a higher pay rise than the year before rose to 60% in Q1, the highest since the series began in 2003. These are likely to be concerning trends.

Source: MNI - Market News/ABS

- Private sector wages grew at 0.8% q/q and 3.8% y/y after 0.9% and 3.6% in Q4. The ABS noted that a number of industries recorded wage growth above 4% while the others were above 3%. The average pay increase returned to 4.3% in Q1, significantly higher than the 3.4% in Q1 2022.

- The public sector saw a step up, as agreements come up for renewal and wage caps are lifted, rising 0.9% q/q and 3% y/y. On Tuesday, federal public sector workers were offered a 10.5% pay increase over three years after their union asked for 20%. It will include 4% in the first year, 3.5% in the second and 3% in the third.

- The education & training (+1.5% q/q) and professional services (+0.9%) sectors drove the Q1 increase.

Source: MNI - Market News/ABS/SEEKWages

AUSTRALIAN DATA: Jobs Expected To Rise Again Keeping Unemployment Rate Stable

In the May meeting minutes, the RBA noted that March employment was strong and that the “labour market remains tight”, thus there will be a lot of attention on Thursday’s April employment data. Analysts are looking for another rise but more moderate than in March with the unemployment rate unchanged at 3.5%.

- Economists expect a 25k gain in April jobs after rising 53k in April. There is a range of estimates from unchanged to +40k with most centred around 20k - 30k. ANZ is at the low end forecasting 20k, with both NAB & CBA on consensus at +25k and Westpac at the upper end with +40k.

- The unemployment rate is generally expected to be stable at 3.5% but there are quite a number of economists expecting it to rise to 3.6%. ANZ, NAB & Westpac all expect 3.5% with CBA forecasting 3.6%.

- The participation rate is projected to be unchanged at 66.7%.

NZGBS: Closed Weaker, ANZ Lifts Expected Terminal OCR

NZGBs closed 8-9bp weaker, near session cheaps for the second consecutive day, as the market digested the prospect of a worse-than-expected debt profile in tomorrow’s Budget 2023 and another sell-side bank ups its terminal OCR expectation.

- ANZ announced a change to its monetary policy outlook with the RBNZ now expected to raise the OCR to a terminal rate of 5.75%. A 25bp hike to 5.50% is expected next Wednesday but they attach a 20% chance of a 50bp hike. This follows the release of Westpac’s updated call of a 6.0% OCR peak earlier in the week.

- Swap rates 1-8bp higher with the 2s10s curve 7bp flatter and the implied long-end swap spread significantly tighter.

- RBNZ dated OIS RBNZ dated OIS is 2-12bp firmer with meetings beyond August leading. 26bp of tightening is priced for the upcoming May 24 meeting with terminal OCR expectations at 5.69% versus 5.60% at yesterday’s close and 5.51% at the end of last week. A cumulative 43bp of easing is priced off the terminal rate by Feb’24.

- Tomorrow sees the release of Budget 2023. The government has signalled that Budget 2023 will focus on alleviating cost-of-living pressures, fast-tracking recovery from Cyclone Gabrielle, and maintaining public services, but not much else.

FOREX: Kiwi Firms In Asia

Kiwi has firmed on Wednesday as ANZ have updated their forecast for the RBNZ terminal rate, the bank now sees the OCR rising to 5.75%.

- NZD/USD prints at $0.6245/50, the pair is ~0.2% firmer today. NZD/USD sits on its 20-Day EMA ($0.6244), bulls look to clear this level with their focus on the 200-Day EMA at $0.6263 as the next upside target.

- AUD firmed off session lows, as US equity futures briefly extended gains, erasing losses of as much as 0.2% to sit unchanged from yesterday's closing levels. The Q1 WPI was close to analysts’ expectations rising 0.8% q/q and 3.7% y/y (Q4 0.8% and 3.4%). Resistance comes in at $0.6712 (50-Day EMA) and support is at $0.6636 (low from May 12).

- Yen is a touch softer, however narrow ranges have been observed thus far today. Q1 GDP printed firmer than expected at 1.6% Y/Y, a print of 0.8% Y/Y had been expected.

- Elsewhere in G-10 EUR and GBP are little changed, both currencies have been trading in narrow ranges with little follow through in Asia.

- Cross asset wise; E-minis are ~0.2% firmer and BBDXY is unchanged from yesterday's closing levels. US Treasury Yields are 1-2bps lower across the curve.

- In Europe today we have the final print of Eurozone CPI, further out US Housing Starts crosses.

EQUITIES: Japan, South Korea & Taiwan Outperform, China/HK Stocks Down Ahead Of Key Earnings

Regional equity trends are once again mixed. China and HK shares track lower, but Japan markets are still outperforming, while South Korea and Taiwan bourses have also rallied today. It has been mixed in South East Asia. US futures are modestly higher, Eminis last around 4131, ~+0.20% higher. Nasdaq futures doing slightly better at +0.25%. Some optimism a debt deal can be reached aiding sentiment at the margins.

- The HSI is down 0.55% at this stage, the index backing away from the 20000 level for now. Carry over from weaker China data yesterday, which has prompted some sell-side analysts to cut their 2023 growth outlooks, has weighed. Market participants will also be watching earnings results from Tencent, which could come later today and Alibaba, which will be out tomorrow.

- The CSI 300 is also lower, off by 0.35% at the break. This puts the index back sub its 200-day MA (3987.09, versus last index levels at 3964.2). Similar headwinds are weighing on China mainland stocks, with a weaker FX rate (USD/CNH breaking back above 7.00) likely a negative as well.

- Japan stocks are still outperforming, the Topix +0.30% higher at this stage, while the Nikkei 225 has breached the 30000 level.

- Taiex is +1.20% firmer, while the Kospi has gained 0.60%, amid some tech related outperformance from Tuesday's US session.

- The ASX 200 is down by 0.50%, while in SEA Thai stocks continue to move lower, off another 0.70% so far.

OIL: Prices Steady But Market Still Nervous

Oil prices are fairly steady during the APAC session after falling on Tuesday driven by data signalling China’s recovery is soft. They have been in a fairly narrow range with Brent currently around $75/bbl after an intraday high of $75.15. It has been unable to hold gains above $75. WTI is $70.91 after a high of $71.06, and it has been unable to hold above $71. The USD index has been trading sideways.

- The IEA revised up its global oil demand expectations in its monthly outlook driven by stronger demand from China which it adjusted up by 200kbd to 2.2mbd. Whereas in contrast, some economists have revised down China’s growth outlook after Tuesday’s disappointing data.

- Later the EIA release official US fuel inventory data. According to Bloomberg, the API reported a 3.7mn crude build. Also in the US, there is a Senate Banking hearing on strengthening Fed accountability and there is April housing data released. There is also the euro area April HICP.

GOLD: Slightly Stronger In Asia-Pac After USD & US Tsys Weighed On Tuesday

In Asia-Pacific trading, gold is $1.70 stronger (+0.1%) at 1990.87, after closing -1.4% at $1989.17.

- At market close on Tuesday, gold hovered near a two-week low as traders monitored negotiations to resolve the US debt-ceiling deadlock and analysed statements from various Federal Reserve officials regarding interest rate prospects.

- Tuesday’s drop, reaching its lowest closing price since May 1, was due to strong US retail sales figures and speculation about a resolution to the debt issue. President Joe Biden and congressional leaders expressed optimism about reaching a deal, despite House Speaker Kevin McCarthy warning of significant differences between the two sides.

- The strengthening of the USD and higher Treasury yields had a significant impact, causing gold to break below the support level at $1,999.6 (the low on May 5) that was established after the release of payroll data, thereby exposing the $1,976.3 level (50-day EMA).

ASIA FX: USD/CNH Breaches 7.00, KRW & TWD Outperform, But SEA FX Weaker

Much of the focus today has been on the breach of 7.00 in USD/CNH. It came not long after the in line CNY fixing. This has weighed on FX sentiment elsewhere in the region, although KRW and TWD have outperformed thanks to resilient local equities. SEA FX is mostly weaker, led by THB on continued election jitters, Tomorrow, the BSP decision is due in the Philippines, with no change expected.

- USD/CNH is continuing to track higher this afternoon, currently around session highs of 7.0130. We aren't too far away from late Dec highs in 2022 of 7.0156. The neutral CNY fixing was the green light for further depreciation pressures, while onshore USD/CNY spot gapped higher as well, although it hasn't breached the 7.00 handle at the time of writing. CNY daily option volumes on Wednesday are currently around 4 times their usual volume at this stage of the session. ~$3.5bn in USD/CNY options have been dealt today according to the latest DTCC data, ~$0.8bn is the average volume for this stage in the session.

- 1 month USD/KRW has spent the session mostly below 1340 and sits at 1337 currently, around -0.30% sub NY closing levels. Onshore equities are higher by 0.6%, as tech has outperformed. This has helped offset the weaker CNH impact. USD/TWD is steady around the 30.80 level, also benefiting from stronger equities, the Taiex +1.8% at this stage. Offshore investors have been buying stocks from both bourses over recent sessions. Today offshore investors have purchased a further $229.9mn of South Korea shares.

- USD/THB continues to track higher, the pair last near 34.20. This is 0.70% weaker in baht terms versus yesterday's close. Technically, we are above the 20 and 50-day EMAs (34.036 and 34.17 respectively). The 200-day EMA sits just under 34.40, and we haven't been above this level since the first half of March. A firmer USD backdrop and higher USD/CNH levels are weighing, but so too is election uncertainty. Move Forward still needs to gain support of the Senate, with its PM candidate not drawing a uniformly positive response at this stage.

- The SGD NEER (per Goldman Sachs estimates) is firmer this morning, however we remain within recent ranges. We now sit ~0.9% below the upper end of the band. USD/SGD printed its highest level since 20 March today, the pair is ~0.1% firmer and last prints at $1.3415/20. April Export Data was firmer than estimates on the M/M printing at 2.7% vs -3.1% exp. The Y/Y print was a touch softer than expected at -9.8% vs -9.7% exp.

- Elsewhere in SEA, USD/MYR has risen around 0.50%, last tracking above 4.5220, while USD/IDR is also higher, last around 14875. USD/PHP dips have been supported, back towards 56.00, the pair last near 56.25. The BSP is expected to be on hold tomorrow.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/05/2023 | 0900/1100 | *** |  | EU | HICP (f) |

| 17/05/2023 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 17/05/2023 | 0900/1100 | | EU | ECB Elderson Panels Beyond Growth Conference | |

| 17/05/2023 | 0930/1130 | | EU | ECB Panetta Presentation on Digital Euro Kangaroo Group Event | |

| 17/05/2023 | 0950/1050 | | UK | BOE Bailey Keynote Speech at British Chambers of Commerce | |

| 17/05/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 17/05/2023 | 1230/0830 | * |  | CA | International Canadian Transaction in Securities |

| 17/05/2023 | 1230/0830 | *** | | US | Housing Starts |

| 17/05/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 17/05/2023 | 1515/1715 | | EU | ECB de Guindos Closes IESE Banking Meeting | |

| 17/05/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.