Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- The major Tsy futures contracts showed through their respective Wednesday bases during early Asia-Pac trade as regional participants reacted to the latest FOMC decision. Asia-Pac news flow (including the latest round of North Korean missile launches, China’s continued focus on its zero COVID policy and softer than expected Chinese Caixin services PMI data) allowed the space to stabilise, before drifting lower again into London hours. Cash Tsys are closed until London hours, owing to the observance of a Japanese national holiday, which thinned out liquidity in Asia.

- The yen remained best G10 performer, amid fluctuating risk sentiment and post-FOMC musings, in thinner-liquidity environment due to a public holiday in Japan. The Fed's monetary policy decision sparked a volatile reaction in USD/JPY, with participants on constant intervention watch after officials repeatedly emphasised their round-the-clock FX monitoring policy. Heightened geopolitical tensions in Asia may have increased the yen's safe-haven allure after North Korea test-launched a suspected ICBM, triggering the J-Alert warning system in three Japanese prefectures.

- The central bank marathon continues, with the Bank of England and Norges Bank set to decide on rates. There is plenty of central bank rhetoric scheduled on top of that, particularly from a slew of ECB members, including President Lagarde. Weekly jobless claims, trade balance, factory orders and final durable goods orders are due out of the U.S. today.

MNI BOE Preview - November 2022: Downside risks to 75bp

Executive Summary

- The MNI Markets team expects a 75bp hike at this week’s MPC meeting, albeit with risks of a smaller 50bp hike.

- UK markets have moved back to close to their prevailing levels ahead of the September MPC meeting but with inflation still in double digits and still flagging concerns in the Bank’s DMP surveys, and still a great deal of uncertainty surrounding the magnitude of fiscal consolidation, we think that the majority of the MPC will not want to disappoint a strong analyst and market consensus of a 75bp hike.

- With growth already starting to falter, however, we do think there is a risk that the Bank delivers a smaller 50bp hike (but do not see the need for a larger 100bp hike at this stage).

US TSYS: Futures Cheapen As Asia Reacts To Fed, Regional News Flow Helps Limit Losses

The major Tsy futures contracts showed through their respective Wednesday bases during early Asia-Pac trade as regional participants reacted to the latest FOMC decision.

- To recap, the Fed delivered the widely expected, unanimous 75bp rate hike yesterday, although the statement pointed to a Fed that would assess “the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation,” even as it looks to attain a sufficiently restrictive stance of monetary policy. This gave the statement a dovish feel, although Chair Powell’s press conference was more hawkish, resulting in some late NY vol. as he flagged a “ways to go” for the Fed, in addition to expectations for a higher than previously foreseen terminal rate level, even as he pointed to likely discussions re: the potential slowing of the pace of hikes over the next couple of meetings.

- Asia-Pac news flow (including the latest round of North Korean missile launches, China’s continued focus on its zero COVID policy and softer than expected Chinese Caixin services PMI data) allowed the space to stabilise, before drifting lower again into London hours.

- TYZ2 is -0-16+ at 110-03+, just off the base of its 0-06+ range on light volume of ~65K. Cash Tsys are closed until London hours, owing to the observance of a Japanese national holiday, which thinned out liquidity in Asia

- Thursday’s London docket is headlined by the latest BoE decision (with consensus looking for a 75bp hike after the recent fiscal saga and related vol. surrounding UK markets & BoE pricing.), with the NY docket including the ISM services survey, Challenger job cuts, weekly jobless claims data and factory goods orders.

AUSSIE BONDS: Bear Flattening, With Offshore Drivers Front & Centre

Aussie bonds took their cues from offshore matters on Thursday, with the major bond futures initially cheapening through their respective overnight session bases as Sydney reacted to the latest U.S. FOMC monetary policy decision.

- The space then stabilised off lows on the back of risk-negative Asia-Pac macro news flow, which centred on the latest North Korean missile launch, China’s focus on continuing with its zero COVID strategy and a slightly softer than expected Chinese Caixin services PMI print.

- That left YM -12.0 & XM -11.0 at the close, with wider cash ACGB trade seeing 9.5-11.5bp of cheapening as the curve bear flattened.

- EFPs pushed wider at the open before more than reversing the move to narrow sharply, pointing to receiver side flows aiding the stabilsation in ACGBs.

- Bills finished flat to -9, with RBA dated OIS now pricing a terminal rate of just under 4.20%, adjusting higher in sympathy with U.S. Fed terminal rate pricing post-FOMC.

- Local data failed to move the needle for ACGBs.

- Looking ahead, Friday will see the release of the RBA’s SoMP (although most of the major adjustments to the Bank’s economic forecasts were pre-released in Tuesday’s post-meeting statement, as is the norm) and the weekly AOFM issuance slate. A reminder that the AOFM has now announced JLMs for the syndication of the new ACGB May-34, which is set to come to market next week.

AUSTRALIA: Uncertainty Around Friday’s Real Retail Sales Data

On Friday retail sales excluding inflation are published for Q3. This data reading should give us an idea if the strength in nominal retail sales is just higher prices or is underlying strength. Given the RBA’s close monitoring of the household sector to gauge the impact its tightening has had so far, the answer to this is important.

- Economists are expecting retail sales ex inflation to rise 0.4% q/q but there is considerable uncertainty with forecasts ranging from flat to +1.7% q/q. It rose 1.4% q/q and 5.5% y/y in Q2.

- Nominal sales rose 2.3% q/q in Q3 and the quarterly CPI and trimmed mean 1.8%. If we use the new monthly inflation data to deflate retail sales, then the projections are almost as diverse as those of analysts.

- If retail sales are deflated by the monthly headline CPI, then Q3 real retail sales rose 0.5% q/q, close to consensus. Using the trimmed mean measure of inflation, then they rose 0.8% q/q.

- The CPI includes services prices as well and they have tended to be lower on an annual basis than goods prices. We have taken out the categories which are obviously services to create a proxy for retail prices (RPI) and this series usually exceeds headline CPI. If we use this RPI proxy to deflate retail sales then it fell 0.1% q/q in Q3.

Source: MNI - Market News/Refinitiv/ABS

NZGBS: Off Lows But Still Cheaper, Swap Spreads Narrow Again

NZGBs found a base after the initial cheapening witnessed on Thursday, with early trade driven by the space’s reaction to Wednesday’s monetary policy decision from the U.S. Federal Reserve and some pre-NZGB auction concession.

- Asia-Pac macro news flow (centred on the latest North Korean missile launch, weaker than expected Caixin services PMI data out of China and China’s continued focus on pursuing its zero COVID strategy) then allowed the broader core global FI space to find a little bit of a base as the session wore on, with the smooth passage of today’s NZGB supply (covering ’28, ’33 & ’51 paper) also helping the space correct from session cheaps.

- Swap spreads were narrower on the day as the push higher in swap rates lagged the move in NZGB yields, with the spread narrowing theme seen since the official inclusion of NZGBs in the WGBI extending.

- The pricing for the terminal OCR rate observed via RBNZ dated OIS edged higher today, in sympathy with moves in U.S. Fed terminal rate pricing post-FOMC, to print around 5.25%.

- RBNZ Governor Orr’s appearance in front of parliament after the release of the FSR had no tangible impact on the space, with familiar rhetoric deployed.

- Friday’s local docket is empty.

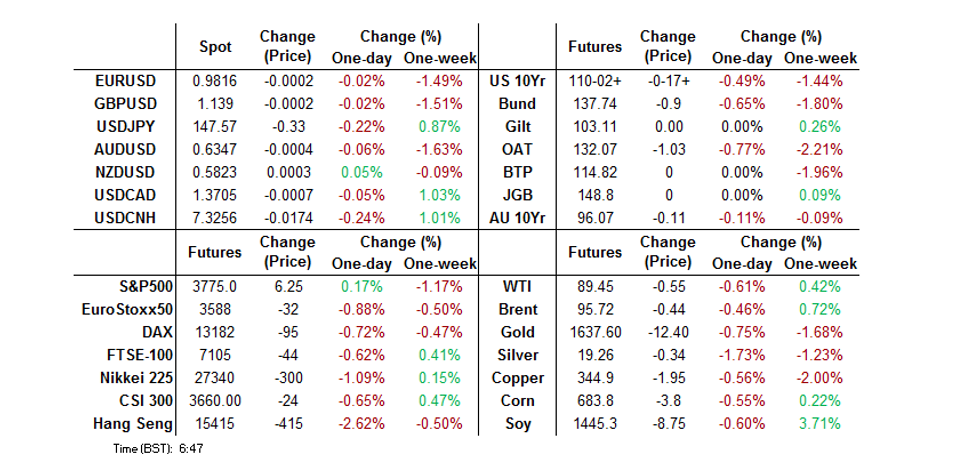

FOREX: USD/JPY Main G10 Mover On Tokyo Holiday

The yen remained best G10 performer, amid fluctuating risk sentiment and post-FOMC musings, in thinner-liquidity environment due to a public holiday in Japan. The Fed's monetary policy decision sparked a volatile reaction in USD/JPY, with participants on constant intervention watch after officials repeatedly emphasised their round-the-clock FX monitoring policy.

- Heightened geopolitical tensions in Asia may have increased the yen's safe-haven allure after North Korea test-launched a suspected ICBM, triggering the J-Alert warning system in three Japanese prefectures.

- USD/JPY sales underpinned broader greenback weakness, with the BBDXY pulling back into negative territory and away from post-FOMC highs. Profit-taking may have facilitated the move, with the U.S. dollar paring gains registered on the back of higher terminal rate expectations articulated by Fed Chair Powell.

- China's Caixin Services PMI printed below expectations (48.4 versus 49.0 consensus forecast), which comes on the heels of a beat in Caixin M'fing gauge earlier this week. Both remained in contractionary territory last month.

- The central bank marathon continues, with the Bank of England and Norges Bank set to decide on rates. There is plenty of central bank rhetoric scheduled on top of that, particularly from a slew of ECB members, including President Lagarde.

- Weekly jobless claims, trade balance, factory orders and final durable goods orders are due out of the U.S. today.

FX OPTIONS: Expiries for Nov03 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9750(E1.0bln), $0.9775(E614mln), $0.9850-55(E790mln), $0.9900-05(E2.2bln), $1.0000(E1.1bln)

- USD/JPY: Y144.00-25($1.6bln), Y147.60($1.1bln)

- GBP/USD: $1.1290-00(Gbp870mln), $1.1700(Gbp536mln)

- EUR/GBP: Gbp0.8625-30(E584mln), Gbp0.8695-00(E521mln)

- EUR/JPY: Y144.00(E504mln)

- AUD/USD: $0.6325(A$520mln)

- NZD/USD: $0.5835-38(N$584mln)

- USD/CNY: Cny7.2450($935mln), Cny7.2500($555mln)

MNI Norges Bank Preview - November 2022: The Return of Gradualism?

Executive Summary

- Board likely choosing between another 50bps “double” hike, or a 25bps step that would mark the end of front-loading

- Punchy inflation, higher interest rates among trade partners and a very tight labour market argue for another sizeable 50bps step this month

- But, slowing real-time economic indicators, eroded household purchasing power and rates already above neutral make a 25bps rate hike the most likely outcome

Full preview including summary of sell-side views here: MNINBPrevNov22.pdf

Sell-side analysts are split almost down the middle between a 50bps move or a slower 25bps clip. This has fed directly into market pricing, with FRA spreads indicating a fine balance of expectations between a 2.50% and 2.75% rate for this month.

There are no new rate path projections or economic forecasts to accompany November’s decision, although unusually the governor Ida Wolden-Bache will be holding a press conference 30 minutes following the decision. The Bank’s schedule show the governor as presenting the Q3 monetary policy report, suggesting no unplanned data or rehashed forecasts will be disclosed. Nonetheless, the press conference gives the bank more opportunity to expand their language in September that “policy is starting to have a tightening effect on the Norwegian economy. This may suggest a more gradual approach to policy rate setting ahead.”

MNI Bank Negara Malaysia Preview - November 2022: Measured & Gradual

Executive Summary

- Although Bank Negara Malaysia was in a better starting position than many of its regional counterparts, it will likely raise the Overnight Policy Rate by a further 25bp this week. Historically elevated core inflation, intensifying peer pressure, the need to rebuild monetary policy buffers and a lengthy hiatus ahead of the next rate review should be enough to budge policymakers towards a standard-sized rate hike.

- On the surface, the latest CPI outturn may have been reassuring. Headline inflation eased more than expected to +4.5% Y/Y, failing to challenge prior cyclical highs. Still, core inflation printed at +4.0% Y/Y, rising to the highest point since at least 2015. Domestic price pressures support the case for continued monetary tightening after the BNM raised its key policy rate by 25bp at each of the last three meetings.

- The fact that this will be the BNM’s final monetary policy meeting this year supports the case for raising interest rates further, as more work needs to be done to contain price pressures, while the near-term fiscal outlook (including counter-inflationary measures) remains clouded by a snap general election in Malaysia.

- Click to see the full preview:MNI BNM Preview November 2022.pdf

ASIA FX: USD/Asia Pairs Mostly Higher, CNH & KRW Outperform

USD/Asia pairs are mixed, mostly higher in line with the firmer USD tone post Powell's press conference overnight. However, CNH and KRW have seen some outperformance. Still to come is the BNM decision (+25bps expected). Tomorrow, we get Philippines inflation and trade, along with Singapore retail sales.

- The tone in China equities has been weaker, weighed by the health authorities stating that the Covid-zero policy zero will be adhered to. A weaker Caixin services PMI has also likely weighed. Still, USD/CNH hasn't tracked higher, the pair is back to a 7.3200 handle, with selling interest evident above 7.3400. Onshore spot is back above 7.3000, but hasn't made fresh cyclical highs.

- USD/KRW 1 month is back through 1420. Onshore equities are lower for the session, but have recouped a large proportion of earlier session losses (sub 2300, now back to +2332). Geopolitical tensions, amid a report North Korean ICBM test, haven't weighed on sentiment. Earlier, BoK FX reserves fell further in October (to $414.01bn) but the pace of losses wasn't as large as September.

- USD/INR is creeping back towards 83.00 (last 82.80/85). There will be some focus on today's RBI meeting to respond to the government after the central bank failed to meet its inflation target for 3 straight quarters, but this is unlikely to shift the RBI's policy bias. The services PMI improved in October to 55.1 from 54.3.

- USD/IDR is at fresh cyclical highs, last at 15682, +34 figs for the session. BI doesn't expect 2022 inflation pressures to be strong as initially feared. Core inflation could be below 4.3%, headline sub 6.3%. The second round for inflation pressures hasn't been large as expected. Foreign investors were net sellers of $23.46mn in Indonesian stocks, with the Jakarta Comp probing the water below its 100-DMA.

- Spot USD/PHP has advanced in the wake of Wednesday's monetary policy decision in the U.S., even as the local central bank vowed to match the Fed's move. We were last at 58.705, + 0.23 figs for the session. Bangko Sentral ng Pilipinas will need to match the Fed's 75bp rate hike at its meeting on November 17, Governor Medalla told reporters today. He emphasized that the impending rate rise will not be "off cycle," since it takes effect after the next scheduled policy review.

- Spot USD/MYR is drifting higher, last around 4.7455. From a technical standpoint, topside focus falls on MYR4.8850, which represents a record high for USD/MYR. Bank Negara Malaysia may increase its Overnight Policy Rate by 25bp today as core inflation continues to accelerate (we have outlined the case for such a scenario in our preview.

EQUITIES: China/HK Equity Rebound Stumbles Again

Asia Pac equities are mostly lower, following sharp falls on Wall St into the close, as Fed Chair Powell delivered a hawkish press conference. US futures are trading modestly higher, +0.20% to 0.30% at this stage, which is helping keep some markets away from worst levels. China health officials an adherence to covid zero policy has also weighed on sentiment.

- HSI is off by close to 3%, unwinding part of the previous two sessions near 8% rally. The tech sub-index has slightly underperformed, down just over 4% at this stage.

- The CSI 300 is down by over 1.2%, the Shanghai Composite by 0.63%. Daily covid case numbers are now above 3k, while as outlined above, China health authorities appeared to push back on recent social media posts that suggested a shift in the covid policy could be coming. The Caixin services PMI also came in weaker than expected, 48.4, versus 49.0 forecast and 49.3 prior.

- The Kospi was down sharply at the open, but dips sub 2300 have been supported, with the index last at 2330 (-0.30% for the session). A barrage of missile launches yesterday, plus a possible ICBM test launch today, hasn't dented sentiment. The Taiex has underperformed the Kospi, down over 1.1% at this stage, but in line with tech losses overnight.

- Japan markets are closed today, while the ASX 200 is off by nearly 1.8%.

GOLD: Steadies As USD Rally Pauses

Gold is slightly above NY closing levels, last around $1637.5 (+0.10-0.15% for the session). We got to fresh lows in the early part of trading, amid a firmer USD trend. However, support was evident ahead of $1632, which was also the low at the start of the month. We rebounded back above $1640 before running out of momentum.

- Gold continues to move with broader USD sentiment, although there appears to be decent support between current spot levels and recent lows sub $1620.

- The topside remains capped by moves into the $1670/$1680 region. The overnight high came close to $1670, while the simple 50-day MA comes in just above $1676.

- The hawkish backdrop presented by Powell didn't help gold overnight, but real yields remain below recent highs (last 1.57%), which is likely helping keep dips in the precious metal supported.

OIL: Tight Supplies Underpinning Prices

Oil prices reached a trough in early trading today after giving up gains on hawkish comments from Fed Chairman Powell. WTI is down 0.5% from its close to around $89.50/bbl and Brent -0.3% to $95.85. The drawdown in crude (-3.115mn barrels) inventories in the US reported by the EIA confirmed the tightness of the market, which has been underpinning prices.

- WTI is now trading above its 10-, 20- and 50-day moving averages.

- The demand outlook for oil remains uncertain with central banks still hawkish and the top health body in China saying that its Zero-Covid Policy remains its strategy to fight the virus.

- EIA inventories of gasoline fell 1.26mn barrels, the lowest since November 2014, and distillate (used in heating oil and transport fuels) stocks were still at a record low in the US going into winter.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 03/11/2022 | 0700/0300 | * |  | TR | Turkey CPI |

| 03/11/2022 | 0730/0830 | *** |  | CH | CPI |

| 03/11/2022 | 0805/0905 |  | EU | ECB Lagarde Panels Latvijas Banka Conference | |

| 03/11/2022 | 0810/0910 | | EU | ECB Panetta Speech at ECB Money Market Conference | |

| 03/11/2022 | 0900/1000 | *** |  | NO | Norges Bank Rate Decision |

| 03/11/2022 | 0930/0930 | ** |  | UK | IHS Markit/CIPS Services PMI (Final) |

| 03/11/2022 | 0950/1050 | | EU | ECB Elderson Panels Latvijas Banka Conference | |

| 03/11/2022 | 1000/1100 | ** | | EU | Unemployment |

| 03/11/2022 | - |  | DE | G7 Foreign Ministers summit in Germany | |

| 03/11/2022 | 1200/1200 | *** | | UK | Bank Of England Interest Rate |

| 03/11/2022 | 1230/0830 | * |  | CA | Building Permits |

| 03/11/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 03/11/2022 | 1230/0830 | ** | | US | Trade Balance |

| 03/11/2022 | 1230/0830 | ** | | US | Preliminary Non-Farm Productivity |

| 03/11/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 03/11/2022 | 1345/0945 | *** | | US | IHS Markit Services Index (final) |

| 03/11/2022 | 1400/1000 | *** | | US | ISM Non-Manufacturing Index |

| 03/11/2022 | 1400/1000 | ** | | US | factory new orders |

| 03/11/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 03/11/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 03/11/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 03/11/2022 | 1730/1330 | | CA | BOC Deputy Beaudry gives opening remarks before academic lecture | |

| 03/11/2022 | 2000/1600 | | CA | Canada FM Freeland presents fiscal update | |

| 03/11/2022 | 2030/2030 | | UK | BOE Mann Panels American Enterprise Institute |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.