Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

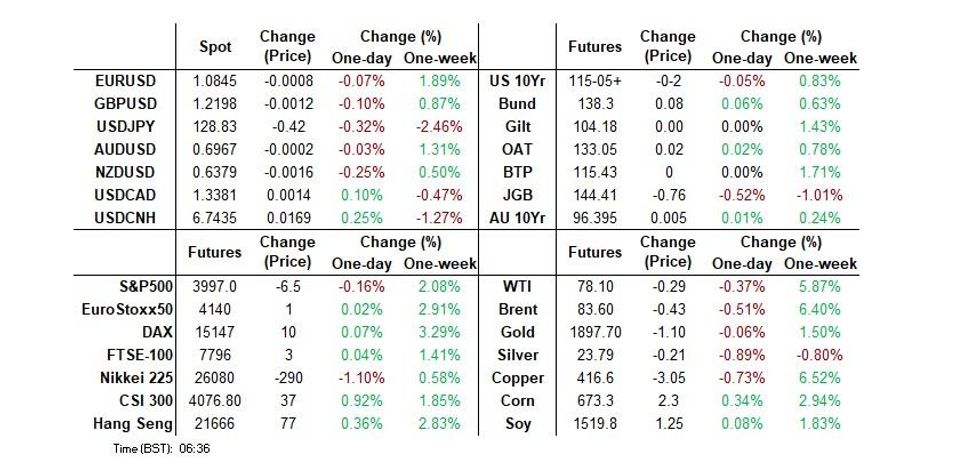

- Speculation surrounding another BoJ policy tweak dominates in Asia, with 10-Year JGB yields through the BoJ's YCC cap, Japanese swap spreads wider and the JPY bid.

- Early USD selling had little follow through, with the USD BBDXY now back to 1228.30, +0.15% firmer for the session. A firmer US cash Tsy yield backdrop has helped (+2.5bps for the 10yr), while U,S, equity futures have also faltered weighing on higher beta plays. Still the BBDXY is down 1.34% for the week and not too far off fresh lows.

- Coming up UK monthly GDP is due, while in the U.S. U. Of Mich. Sentiment is slated, along with Fedspeak from Kashkari and Harker.

US TSYS: Cheaper, JGB Matters Dominate Asian Session

TYH3 deals at 115-03, -0-04+, at the lower end of its 0-09 range on volume of ~101K.

- Cash Tsys are 1-3bp cheaper across the curve, with 10s leading the move.

- Tsys were mixed in early dealing before being pressured as weakness in JGBs spilled over, with 10-Year JGB bond yields showing above the BoJ's permitted 0.50% ceiling.

- Tsys continued to feel the pressure as JGBs moved lower still and Japanese swap spreads widened. Although the move in Japanese fixed income has moderated from session extremes into the Tokyo close, presumably on at least some short cover ahead of next week's BoJ meeting, which has allowed Tsys to find a base.

- Fedspeak from Atlanta Fed President Bostic ('24 voter) hit the wires early in the session. There was little reaction in the space as he reiterated themes observed in recent communique, noting that the slowdown in inflation could facilitate shifting the hiking pace to 25bps from next month.

- Block flow was see across the futures curve in Asia-Pac hours, while the most notable flow came via a 30K lift of the TYG3 112/111 put spread.

- UK GDP and French CPI data headline the European session. Further out UofMich Sentiment provides the highlight in NY. There is Fedspeak from Minneapolis Fed President Kashkari and Philadelphia Fed President Harker.

JGBS: Firming Into The Close, Futures Still Comfortably Lower On The Day

JGB futures are -60 into the bell after extending on the weakness observed in the overnight session.

- A peculiar bid has developed into the close, led by the longer end and presumably some short cover, with the major benchmarks now showing 1bp cheaper to 5bp richer on the day, flattening. The smooth passage of 5-Year supply helped steady the ship earlier in the Tokyo afternoon.

- 2 rounds of unscheduled BoJ Rinban operations helped the space at the margin.

- This came after futures registered a fresh cycle low as speculation re: another BoJ policy tweak intensified, with the next technical levels to watch at vol. band support, situated at 144.14 and 144.02. The contract found a low just above the former in the Tokyo morning.

- 10-Year JGB yields printed above the BoJ’s 0.50% YCC cap, showing as high at 0.568% on the BBG price feed. The measure hovers around 0.510% into the bell.

- 10-Year swap rates (a tool of preference for those testing the BoJ’s will re: YCC) have printed above 1.00% for the first time in over a decade today, and the measure is set to close above that level. Some BoJ watchers have started to tout the potential for a removal of the Bank’s YCC programme as soon as next week, although this is by no means a consensus view. Swap spreads were wider across the curve.

- The BoJ monetary policy meeting headlines next week’s domestic docket.

NZGBS: Off Best Levels As JGB Weakness Takes Edge Off Feed Through From U.S. CPI

NZGBs cheapened away from firmest levels of Friday trade on the back of spill over from weakness in JGBS, leaving the major benchmarks running ~7bp richer at the bell, in what was a parallel shift across the curve.

- This came after an initial round of richening tied to catch up to Thursday’s U.S. CPI print.

- Swap rates were 5-7bp lower across the major benchmarks, leaving swap spreads a touch wider to unchanged.

- RBNZ dated OIS came in at the margins, with ~63bp of tightening priced for the Feb 23 meeting, alongside terminal OCR pricing showing between 5.40-5.45%, aided by the post-CPI reaction in U.S. Fed pricing.

- Local headline flow remained subdued at best, as has been the case for most of early ’23, leaving the wider macro cues at the fore.

- Looking ahead, next week’s local docket includes REINZ house price data, card spending readings, non-resident bond holdings and the latest manufacturing PMI survey.

EQUITIES: Major Indices Mostly Higher (ex Japan)

Asia Pac equities haven't seen the same uniformly positive tone that was evident earlier in the week, but there are pockets of strength today. US equity futures are down, which has likely taken some of the gloss off end of week proceedings. We are away from worst levels but still sit comfortably in the red (eminis -0.25% to 3993/94, while Nasdaq futures are down around -0.36%).

- China shares are tracking higher. The CSI 300 +0.80% at this stage. The FT reported the authorities are moving to take 'golden shares' in certain tech companies (stake of 1%) to maintain sufficient oversight.

- Didi apps could also be allowed to return to app stores as soon as next week, in a further sign of reduced regulatory crackdown for the sector.

- The HSI is also higher, but a more modest +0.2% at this stage.

- Japan stocks are lower, with the Nikkei 225 off over 1%, while the Kospi (+0.90%) and Taiex (+0.75%) have maintained gains, but are down from early session highs.

- The ASX200 continues to rally, +0.66%, with firmer commodity prices continuing to support.

FOREX: USD Rises From Fresh Lows, JPY Outperforms

Early USD selling had little follow through, with the USD BBDXY now back to 1228.30, +0.15% firmer for the session. A firmer US cash Tsy yield backdrop has helped (+2.5bps for the 10yr), while US equity futures have also faltered weighing on higher beta plays. Still the BBDXY is down 1.34% for the week and not too far off fresh lows.

- USD/JPY hit fresh lows sub 128.70 in the first part of trading, but has rebounded back above 129.00 and has spent the rest of the session above this level (last 129.20/25). The yen has outperformed the rest of the G10 though, with markets keeping one eye on next week's BoJ meeting.

- AUD/USD is back under 0.6950, around 0.30% down from NY closing levels. We haven't drifted too far away from this level, with higher iron ore prices (near $125/ton) providing some offset. China commodity import data showed softness (ex oil), but trends are expected to be better in 2023.

- NZD/USD has been the worst performer in the space so far today, off 0.50% to the low 0.6360 region. 0.6400 remains a resistance point for now.

- Coming up UK monthly GDP is due, while in the US U. Of Mich. Sentiment is out, along with Fedspeak from Kashkari and Harker.

AUD/NZD: Bullish Momentum Grows, Testing 200-day EMA

AUD/NZD is dealing above $1.09 for the first time since mid-November. Increasingly bulls look to be in control, the pair has broken above its 100-day EMA after several tests and is testing its 200-day EMA in today's dealing.

- Technicals, whilst still mixed, are turning increasingly bullish. The pair is comfortably above its 20 and 50-day EMAs and held above $1.08 before the latest move higher.

- Bulls will firstly look to close above the 200-day EMA at $1.0913, to then target bull channel resistance at $1.0991.

- To halt the momentum bears will look to break out of the bull channel with a break of $1.08.

- The AU-NZ 2 government bond yield spread is comfortably off mid-December lows (near -170bp), last around -133bp, but the rate of improvement (in AUD's favor) has picked up pace in recent dealing.

- The 2yr swap spread is also comfortably off 2022 lows, but has shown less upward momentum in recent sessions.

- Relative commodity prices look to be moving in AUD’s favor as well. Copper is 15% firmer from early January lows, and Iron Ore is up ~11% from its lows this month. Metals have definitely been outperforming softer/agricultural commodities in recent weeks.

Fig 1: AUD/NZD Spot Testing 200-Day EMA

Source: MNI - Market News/Bloomberg

FX OPTIONS: Expiries for Jan13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0500(E1.5bln), $1.0600(E1.8bln), $1.0645-60(E2.0bln), $1.0670-80(E2.6bln), $1.0685-00(E2.3bln), $1.0750(E2.4bln), $1.0770-75(E1.2bln), $1.0800(E1.5bln), $1.0820-25(E740mln), $1.0850(E1.5bln)

- GBP/USD: $1.2000(Gbp1.1bln)

- EUR/GBP: Gbp0.8900(E791mln)

- USD/JPY: Y131.00($597mln), Y131.95-00($776mln), Y133.85-00($1.0bln), Y134.40($542mln)

- AUD/USD: $0.6950(A$1.5bln), $0.7000(A$1.3bln), $0.7125(A$1.9bln)

- USD/CAD: C$1.3295-05($560mln)

ASIA FX: IDR & THB Best Performers For The Week, Amid Broad USD Weakness

USD/Asia NDF pairs are mostly away from recent lows, as a modest risk off tone emanates from the G10 space. Spot levels are still firmer for some currencies, reflecting catch up to Thursday's USD weakness post the CPI print. Looking ahead, Monday delivers the China 1yr MLF rate outcome, no change expected (2.75% currently). India wholesale prices and trade figures are also due, along with Indonesian trade data.

- USD/CNH tracked USD/JPY lower in early trade, getting close to 6.7200, but has spent the remainder of the session recovering. We last tracked 6.7465/70. The CNY fixing was neutral, while Dec trade figures were slightly better than expected.

- USD/KRW 1 month was also weaker in the first part of the session before rebounding back above 1240, last near 1244, +0.44% for the session. The BoK hiked by 25bps as expected, but a pause could be on the cards at the February meeting.

- Spot USD/IDR is down a further 1% to 15183, while the 1 month NDF is unchanged at 15162. This is fresh lows in USD/IDR back to late September/early October. Note the simple 200-day MA sits at 15054.

- USD/INR 1 month NDF is slightly higher at 81.50, +0.30% for the session versus NY closing levels. Still, onshore spot remains sub the 100-day MA (81.62), last at 81.395. Yesterday's headline inflation data surprised on the downside, 5.72% y/y, versus 5.90% expected. Core inflation remained sticky though, above 6%.

- USD/THB tracked to fresh lows at 33.10 before finding some support, last around 33.18. Still the baht is 2.55% stronger for the week, only shaded by IDR in terms of best performer within the region for the week. The baht remains a preferred play on the China re-opening theme.

CHINA: Trade Data Slightly Better Than Forecast, Commodity Imports Expected To Improve

China trade figures were a touch better than expected. Exports printed at -9.9% y/y, (-11.1% forecast and -8.9% prior), while imports came in at -7.5% y/y (-10.0% forecast and -10.6% prior). The trade surplus rose a touch to $78.01bn, ($76.90bn forecast, $69.25bn prior).

- The data certainly could have been worse given the domestic covid outbreak spike during the month, Still, export growth is its weakest since early 2020 and generally in line with other North East Asia economies like South Korea and Taiwan.

- Import growth was slightly better but is not too far above recent lows. Commodity import volumes were generally softer, excluding oil. Iron ore dipped 8% m/m. Coal and copper were also down.

- Market sentiment clearly expects better import demand as we progress through 2023, with metal commodities among the clear winners in terms of the China re-opening trade in the commodity space.

BOK: Pause Possible In February But Not A Done Deal

A key sentence in today's BoK statement, "The Board deems it warranted to maintain the restrictive policy stance with an emphasis on ensuring price stability, as inflation is expected to remain high above the target level, although the domestic economic growth rate has slowed." clearly hints at the possibility of a pause, particularly when compared to Nov statement. "The Board sees continued rate hikes as warranted for some time, as inflation is expected to remain high, substantially above the target level, although the domestic economic growth rate has slowed."

- Still, the BoK board appears somewhat divided. Two members dissented today's move, while 3 see the current rate, after today's decision, at 3.50% as favorable from a terminal rate perspective. In contrast, 3 board members see 3.75% as a possible terminal rate.

- BoK Governor Rhee came across as slightly more in the hawkish camp, stating today's BoK statement doesn't mean rates will be kept frozen. He also pushed back against the idea of rate cuts later this, stating it would be difficult to deliver unless they see evidence of inflation reaching 2%.

- Between now and the next meeting is on 23rd of February. Between now and then the BoK will get Q4 GDP (25th Jan) which is expected to be negative, while Jan CPI prints on the first of Feb. The central bank may also have a better picture of how China growth/external demand is emerging in the early parts of 2023 by then, along with the Fed path.

GOLD: Can't Sustain Move Above $1900, But On Track for 4th Straight Weekly Gain

Gold is struggling to stay in positive territory through today's Asia Pac session. We currently sit just above $1896.50, slightly down relative to NY closing levels. The early move above $1900 ran out of momentum, as the USD recouped earlier losses. Still, the metal is on track for its fourth weekly gain, +1.65% at this stage.

- Through Thursday's US session we saw volatile trade around the CPI release, but ultimately a test above the $1900 level. The high near $1901.50 couldn't be sustained though.

- Upside targets look for a move to $1909.8 (May 5, 2022 high).

OIL: Down From Highs, But China Optimism Ensures Strong Weekly Gain

Brent crude is off slightly for the session, last near $83.70/bbl. This is line with a slightly more risk-off tone in the cross asset space. Still, Brent is tracking +6.5% higher for the week. Technically, we have cleared the 20-day EMA ($81.99/bbl) but resistance remains around the 50-day at $84.41/bbl. WTI is close to $78.20 currently.

- Today's China trade figures will have given oil bulls some optimism, as oil import volumes remained strong in Dec, despite the domestic Covid wave. The China re-opening theme is a key driver of the stronger oil outlook this year, with oil consumption expected to hit fresh record highs this year.

- Elsewhere the US won't rule out the further releases from the SPR to curb domestic prices. The US House also voted to ban oil reserve sales to China, but the bill is unlikely to be taken up by the Democrat controlled Senate.

- Next week sees the World Economic FOrum kick off in Davos on Monday. On Tuesday, the Dec run of monthly activity data for China, along with Q4 GDP is due (which is expected to be negative q/q). The OPEC monthly report is also due on Tuesday. Wednesday delivers the IEA monthly report. Note the EIA weekly oil inventory report is due Thursday, delayed one day due to a holiday in the US on Monday.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/01/2023 | 0700/0700 | ** |  | UK | UK Monthly GDP |

| 13/01/2023 | 0700/0700 | ** | | UK | Index of Services |

| 13/01/2023 | 0700/0700 | *** | | UK | Index of Production |

| 13/01/2023 | 0700/0700 | ** | | UK | Output in the Construction Industry |

| 13/01/2023 | 0700/0700 | ** | | UK | Trade Balance |

| 13/01/2023 | 0700/0800 | *** |  | SE | Inflation report |

| 13/01/2023 | 0745/0845 | *** |  | FR | HICP (f) |

| 13/01/2023 | 0800/0900 | *** |  | ES | HICP (f) |

| 13/01/2023 | 0900/1000 | * |  | IT | Industrial Production |

| 13/01/2023 | 0900/1000 |  | DE | GDP 2022 | |

| 13/01/2023 | 1000/1100 | ** |  | EU | Industrial Production |

| 13/01/2023 | 1000/1100 | * | | EU | Trade Balance |

| 13/01/2023 | - | *** |  | CN | Trade |

| 13/01/2023 | 1330/0830 | ** |  | US | Import/Export Price Index |

| 13/01/2023 | 1500/1000 | *** | | US | University of Michigan Sentiment Index (p) |

| 13/01/2023 | 1500/1000 | | US | Minneapolis Fed's Neel Kashkari | |

| 13/01/2023 | 1520/1020 | | US | Philadelphia Fed's Patrick Harker |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.