Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

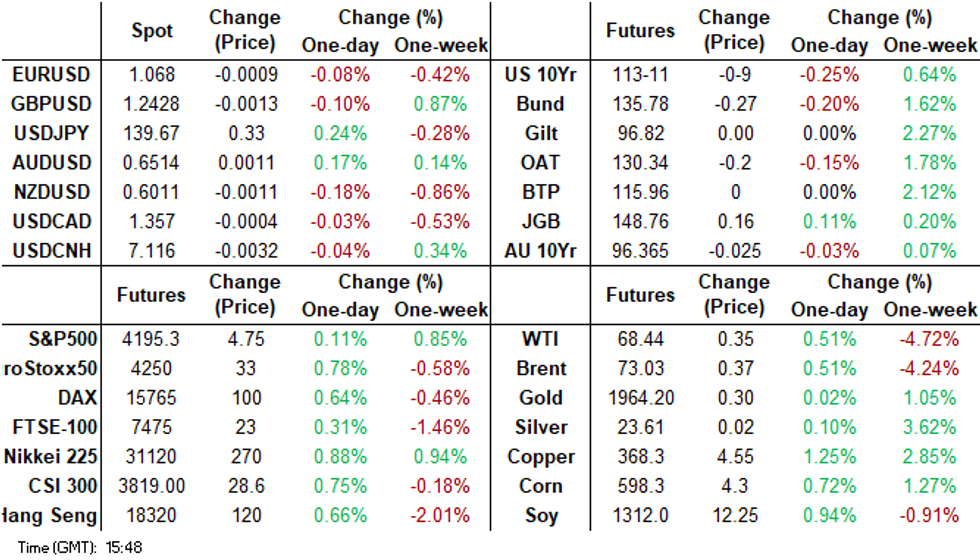

- China's Caixin PMI comfortably exceeded expectations, printing at 50.9, while the US House of Representatives voted in favour of raising the US debt ceiling. Following the announcement, US tsys have weakened, reversing the earlier 1-3bp rally observed during the early Asia-Pacific session and turning into a 3-4bp cheapening across the yield curve, extending up to the 10-year maturity.

- Regional equities are mostly higher, with gains in China/HK in focus. Markets have been buoyed by the surprise Caixin manufacturing PMI beat. USD/CNH dipped initially, but lows close to 7.1000 were support. AUD has outperformed NZD. The AUD/NZD cross hit fresh highs for May.

- Looking ahead, later the Fed’s Harker speaks on the economic outlook. There are also US manufacturing PMI/ISM, Challenger job cuts, jobless claims and final Q1 productivity/ULC. In Europe, ECB President Lagarde speaks and PMIs, preliminary May CPI and unemployment rate are released.

MARKETS

US TSYS: Weaker After Debt Ceiling Passes The House, Heavy Calendar Ahead

TYU3 is currently trading at session lows at 114-04+, down 10+ from the closing levels in NY. While China's Caixin PMI comfortably exceeds the expansion/contraction threshold at 50.9, the main factor behind the move away from session highs was the news that the US House of Representatives voted in favour of raising the US debt ceiling by a margin of 314-117.

- The bill now awaits consideration in the Democrat-led Senate. President Biden has urged it to pass the agreement as soon as possible. However, several senators have indicated their intention to delay the legislation's progress, according to Bloomberg reports.

- Following the announcement, US tsys have weakened, reversing the earlier 1-3bp rally observed during the early Asia-Pacific session and turning into a 3-4bp cheapening across the yield curve, extending up to the 10-year maturity.

- Today’s agenda is also filled with important US data releases, including the ADP Employment report, ISM Manufacturing Index, final figures for Unit Labour Costs and Productivity in Q1, Challenger Job Cuts, and weekly Initial Jobless Claims. These releases will set the stage for Friday's highly anticipated Non-Farm Payrolls report.

JGBS: Richer After Solid Demand At 10-year Auction, US Tsys Pressure

JGB futures have strengthened in afternoon Tokyo trade, +12 compared to settlement levels. This positive movement can be attributed to the solid demand observed in the results of the 10-year JGB auction.

- However, the gains in JGB futures were countered to some extent by weaker US tsys in Asia-Pac trading. The reversal in US tsys occurred following the news of the US House of Representatives had voted to lift the US debt ceiling by a margin of 314-117. The bill now awaits consideration in the Democrat-led Senate. As a result, US tsys weakened, reversing the earlier 1-3bp rally seen during the early Asia-Pacific session and turning into a 3-4bp cheapening across the yield curve, extending out to the 10-year maturity.

- Cash JGBs are richer across the curve with yields 0.6-1.3bp lower. The 5-year zone is the outperformer, with the 4-year zone as the laggard.

- The benchmark 10-year yield is 1.0bp lower at 0.426%, after 10-year supply is well received with the low-price meeting wider expectations and the cover ratio rising to 3.689x from 3.60x at the previous auction.

- The swap curve shifts lower with rates 0.2-0.9bp lower. Swap spreads are wider across the curve.

- The local calendar tomorrow is light tomorrow with Monetary Base for May as the only release.

- Tomorrow will also see BoJ Rinban operations covering 1-5-year and 10-25-year JGBs.

- Ahead of that, the US calendar today sees the release of the ADP Employment report and ISM Manufacturing Index.

AUSSIE BONDS: Follows US Tsys Cheaper, Heavy US Calendar Today

ACGBs are weaker (YM -3.0 & XM -4.5) after US tsys reverse course after the debt ceiling bill passes the US House of Representatives. The bill now goes to the Democrat-led Senate and President Biden has urged it to pass the agreement as soon as possible. In terms of the Senate, Bloomberg is reporting that several senators have said that they won’t allow the legislation to pass quickly.

- Following the announcement, US tsys have weakened, reversing the earlier 1-3bp rally observed during the early Asia-Pacific session and turning into a 3-4bp cheapening across the yield curve, extending up to the 10-year maturity.

- Also potentially weighing on ACGBs was news that Q1 Capex printed higher than expected at +2.4% q/q versus expectations of +1.0%. The 2nd estimate of 2023-24 investment plans at A$137bn also printed above its estimate of A$136bn.

- Cash ACGBs are 3-4bp cheaper with the AU-US 10-year yield differential +2bp at -3bp.

- Swap rates are 4-5bp higher on the day with EFPs slightly wider.

- The bills strip sees pricing flat to -4 with late whites leading.

- RBA dated OIS is 2-5bp firmer for meetings beyond August with April’24 leading.

- The local calendar tomorrow sees Investor Loans data for April slated.

- The AOFM plans to sell A$500mn of the 4.25% 21 April 2026 bond tomorrow.

AUSTRALIAN DATA: Robust Investment Growth & Positive Outlook

Q1 private capex rose 2.4% q/q to be up 6.3% y/y, stronger than expected. Q4 was revised up to 3% q/q from 2.2%. The strength was broad based in both the mining and non-mining sectors and in building and equipment. This growth is welcome as real private GFCF fell 1.7% q/q and -1.3% y/y in Q4 GDP.

- Machinery & equipment rose 3.7% q/q and 5.8% y/y and building & structures +1.3% and 6.8%.

- Capex intentions were increased 2.7% for FY23 and by 6.4% for FY24 signalling a positive investment outlook. Building was unchanged for FY23 but FY24 was 6.4% higher, whereas equipment was +6.1% and +6.4% respectively.

- Weak construction activity has impacted equipment investment in the sector with it falling 23.1% in Q1. But this follows a period of strong capex and investment expectations remain positive.

Source: MNI - Market News/ABS

AUSTRALIAN DATA: Strong May Home Prices Rise As Shortages Worsen

CoreLogic recorded a broad based increase in Australian home prices in May of 1.2% m/m as rising demand comes up against housing shortages. This was the third consecutive monthly rise. The capital-city index rose 1.4% m/m, the highest since September 2021, and is now 3% above the February trough. Rising home prices plus higher mortgage rates are going to drive a further deterioration in affordability, while at the same time rental inflation keeps rising. These developments are concerning the RBA.

- Home prices remained above trend during the 2022 correction and now stand 10% above it.

- Advertised listings reflect the major supply shortage in the housing market. CoreLogic observed that in May there were around 1800 fewer homes advertised in the capital cities than in April. Inventory is down 15.3% y/y and 24.4% below the 5-year average.

- Research director Lawless said “With such a short supply of available housing stock, buyers are becoming more competitive and there’s an element of FOMO creeping into the market.”

- Sydney prices rose 1.8% m/m and Melbourne 0.9%.

- See CoreLogic release here.

Source: MNI - Market News/Refinitiv

NZGBS: Weaker With US Tsys, Heavy US Calendar Today

NZGBs ended the session on a weak note, with yields climbing by 4bp across the benchmarks. The reversal in the local market can be attributed to a cheapening in US tsys, following the news of the US House of Representatives voting in favour of raising the US debt ceiling by a margin of 314-117.

- Additionally, the lacklustre demand observed at the auction of May-28 and May-34 bonds further contributed to the afternoon weakness. Notably, the cover ratios for these auctions declined to 2.64x and 2.75x from their previous levels of 3.40x and 4.13x, respectively. Although the cover ratio for the May-51 auction did experience a significant increase to 4.8x from 2.46x, the corresponding cash bond has traded 2.5bp cheaper following the auction, along with the other offerings.

- Swap rates closed -1bp lower to 1bp higher with the 2s10s 1bp flatter.

- RBNZ dated OIS closed flat to 1bp softer across meetings.

- The local calendar sees Q1 data for the Terms of Trade and Volume of All Buildings tomorrow.

- Ahead of that, the US calendar today sees the release of the ADP Employment report, ISM Manufacturing Index, final figures for Unit Labour Costs and Productivity in Q1, Challenger Job Cuts, and weekly Initial Jobless Claims. These releases will set the stage for Friday's highly anticipated Non-Farm Payrolls report.

EQUITIES: China Caixin PMI Beat Drives Relief Rally

Regional equities are mostly higher, with gains in China/HK in focus. Markets have been buoyed by the surprise Caixin manufacturing PMI beat in China. This goes against the recent run of softer data outcomes and yesterday's official PMIs. US equity futures spiked on the headlines the US House had passed the debt ceiling agreement, but this proved to be short-lived.

- Eminis were last close to 4193, just in positive territory. Earlier highs sat at 4202.50. Nasdaq futures are in the red, down -0.10% at this stage.

- The HSI is up 0.80% at the break, but was above +1% at one stage following the PMI beat. The tech sub-index is holding close to highs, last around +2%. The CSI 300 is near +0.70% at the break, with the index back above the 3700 level.

- Taiex (-0.40%) and the Kospi (-0.30%) are unperforming following tech losses in US trade on Wed.

- The ASX 200 is +0.30%, aided by higher metal prices post the China data. Indian shares are trying to go higher after yesterday's Q1 GDP beat, we aren't too far off recent highs, which may be limiting upside momentum.

FOREX: Firmer US Yields Halts Yen Rebound, AUD/NZD To Fresh Highs For May

The BBDXY has largely respected recent ranges. We last sat at 1245.40, against earlier highs near 1247. Some optimism emerged post the US House passing the debt ceiling agreement, but there wasn't much follow through. If anything, the USD index has slightly underperformed the firmer US yield backdrop. The 2yr sits just off session highs at 4.43%.

- The debt deal and the better Caixin China PMI have aided US yield moves. This has also helped USD/JPY move comfortably off fresh lows sub 139.00 (which printed early), with the pair back to 139.45/50. Better Q1 Capex data is likely to see Q1 GDP revised higher, but the data didn't have a meaningful impact on FX sentiment.

- AUD/USD was sub 0.6500 early, but now sits back closer to 0.6520. Higher commodity prices post the China data has helped, as has better than expected Q1 Capex figures locally. The AUD/NZD cross is trading at fresh highs for May, last near 1.0840.

- NZD/USD has lagged, last near the 0.6010/15 region, although we haven't moved back below 0.6000 so far today.

- Looking ahead, focus shifts to German retail sales on Thursday morning before the final manufacturing PMI reads for May. Attention will then be on the Eurozone Flash estimate of CPI which is expected to come in at 6.3% Y/y. This will be the final read before the June 15 ECB meeting. US ADP and the ISM Manufacturing PMI highlight the docket before Friday’s key employment report.

OIL: Crude Firmer On Debt-Deal & China Demand Optimism

Oil prices are higher during APAC trading driven by the passage of the US debt deal through the House of Reps and the Caixin PMI rising above 50. The USD index is flat.

- WTI is up 0.5% and has broken through $68 and is currently around $68.43/bbl, close to the intraday high of $68.64. Brent is 0.6% higher and is holding around $73.

- The dive in oil prices this week will not make for a happy OPEC meeting on the weekend. They will be looking at disappointing demand from China, while the group’s exports are declining and Russian output remains robust. The Saudi energy minister warned short-sellers earlier this month. It is possible that OPEC+ makes a small symbolic quota reduction to send a signal to the market. Most analysts expect no change.

- Bloomberg reported a 5.2mn crude stock build in the US according to API data. The official EIA numbers are released today.

- Later the Fed’s Harker speaks on the economic outlook. There are also US manufacturing PMI/ISM, Challenger job cuts, jobless claims and final Q1 productivity/ULC. In Europe, ECB President Lagarde speaks and PMIs, preliminary May CPI and unemployment rate are released.

GOLD: Supported By Lower Global Yields

Gold is slightly higher in the Asia-Pacific session, after closing at 1962.73 (+0.2%) on Wednesday.

- Bullion rose as bond yields declined following weaker economic data, softer equity markets, and Fedspeak (Jefferson/Harker) pushing back against a June hike.

- As far as FOMC dated OIS was concerned, Fedspeak weighed most heavily, especially for June OIS pricing with most of the day’s decline coming after Jefferson/Harker, to leave just +8bp priced, whilst it no longer fully prices a hike come July with +20bp.

- Gold experienced a decline of 1.4% in May, reversing the gains it made earlier in the month when it surged to nearly record levels due to concerns about a potential US default. However, these worries have subsided as President Joe Biden and Republican House Speaker Kevin McCarthy expressed optimism that legislation will be passed by lawmakers to prevent such a scenario.

- Fears of economic weakness have Wall Street strategists seeing a longer-term bull case for gold and the miners who dig up the precious metal even as the price of the bullion nears all-time highs. (link)

ASIA FX: Little Follow Through USD Weakness Post Caixin PMI Beat, INR Strengthens

USD/Asia pairs have traded in a mixed fashion today. USD/CNH tracked lower post the Caixin PMI beat, but dips towards 7.1000 were supported. INR has rallied, but otherwise most pairs have respected recent ranges. Tomorrow, South Korea Q1 GDP revisions and May CPI prints are due, but the data calendar is empty otherwise.

- USD/CNH highs were near 7.1270 prior to the Caixin PMI, but we sunk back to 7.1020 post the data. We have steadily recovered back above 7.1150 since, but a better tone to onshore equities post the lunch time break may aid sentiment at the margins. The CNY fixing was neutral.

- 1 month USD/KRW got to lows near 1316, but dips once again were supported, the pair last back closer to 1320. Export growth was close to expectations, remaining deeply negative in y/y terms, but the trade deficit position continues to improve.

- USD/TWD is relatively steady, spot last near 30.71. Onshore equities have faltered somewhat as the recent surge higher in tech cools. The Taiwan PMI also slipped back to 44.3 in May from 47.1 in April.

- USD/INR is tracking lower in the first part of trade, the pair off 0.40%, last in the 82.45/50 region, slightly above session lows. This is fresh lows from mid May. Note the 50-day and 100 day MAs sit in the 82.20/25 region, while below that is the 200-day MA back at 81.795. On the topside, recent highs sit close to 83.00. The May manufacturing PMI rose to 58.7 from 57.2, keeping the recent run of better data outcomes going.

- USD/THB has tracked recent ranges, last sitting near 34.75/80, while USD/PHP is currently at the 56.20 level.

CHINA DATA: Caixin PMI Rise Inconsistent With Official PMI, China Related Assets Pare Gains

The Caixin PMI print puts the index back at 50.9, comfortably above the 50 expansion/contraction point, albeit still below recent highs in Feb of 51.6. In terms of the detail, the output sub-index rose to 53.8 from 50.2 in April. This is the highest print for this sub-index since June 2022. New orders were also up from the prior month.

- The Caixin survey tends to focus more on small and medium sized enterprises and gives a somewhat inconsistent reading with yesterday's official manufacturing PMI. This survey showed conditions deteriorated in May for such enterprises (47.6 from 49.2 for medium enterprises, 47.9 from 49.0 for small enterprises).

- The survey firms also tend to more export orientated, which again is somewhat inconsistent with the trends in external seen elsewhere in the region and across the globe.

- Still, an upside surprise runs the recent run of downside surprises and may halt any further downgrades of the growth outlook, at least in the near term. Note we get the Caixin services and composite PMI readings next Mon, followed by trade data on Wed.

- China related assets have responded positively to the print, although there hasn't been much follow through. HK equities are back close +0.50%, against earlier gains of +1%. USD/CNH is back above 7.1100, against post data lows close to 7.1020. AUD and NZD gains have also slipped.

ASIA DATA: Manufacturing Contraction Continues Across Northern Asia

The S&P manufacturing PMIs in north Asia are signalling contracting activity with China and Taiwan seeing the situation deteriorate further but South Korea improving slightly. With the global growth outlook highly uncertain, this lacklustre industrial picture is unlikely to change soon.

- The manufacturing PMI in South Korea rose to 48.4 from 48.1, but is still signalling contracting industrial activity. But new orders fell at a sharper rate than in April driven by weak demand. Foreign orders were not as soft as the prior month. Despite the weakness, employment rose at its strongest pace in over a year. The 1-year outlook was its most optimistic for 10-months, as global headwinds are expected to ease.

- Cost pressures in Korea rose at their slowest since September 2020 and as a result output inflation fell for the first time in 32 months, as firms used price to attract sales. This is good news for the Bank of Korea.

- Taiwan saw the decline in manufacturing deteriorate sharply in May. The PMI fell to 44.3 from 47.1, as output and new orders fell sharply. Businesses are reporting softer demand both domestically and from overseas (especially China, Europe & US), and so also reduced jobs at the fastest pace in more than 3 years. Despite this bleak picture, the 12-month outlook was mildly optimistic for the 2nd consecutive month.

- Input prices in Taiwan fell for the first time in 6 months due to weak demand and these savings were often passed on to customers to boost demand.

ASIA DATA: Manufacturing PMIs Mixed Across ASEAN, Price Pressures Muted

Global S&P manufacturing PMIs across ASEAN were mixed in May with some showing activity continues to grow while in other countries it is contracting. The ASEAN aggregate and Indonesia’s PMI are published on June 5.

- Thailand’s PMI eased from its April record of 60.4 to 58.2 in May, which is still very strong and has been above 50 for 17 months. Demand is rising strongly, even foreign orders improved, and so employment picked up slightly. It is signalling that manufacturing output should begin to recover soon, as April fell 8.1% y/y with capacity utilisation falling to 53.8% from 66.5%. Business confidence remained positive but was negatively impacted by the macro uncertainty. Input costs increased further but output inflation rose at its slowest in 19 months and is below average.

- Manufacturing growth rose further in the Philippines with the PMI rising to 52.2 from 51.4 driven by stronger production and new orders (domestically & from overseas). This was the 16th consecutive month of growth. As a result, employment picked up. Producers were generally optimistic about the outlook. Unfortunately, price pressures intensified in May; given the Philippines has one of the highest inflation rates in Asia. Higher cost inflation was passed onto customers but input and output measures were below series averages.

- Malaysia saw the pace of manufacturing contraction deteriorate with the PMI falling to 47.8 from 48.8 due to weak demand, output and employment. Businesses were generally positive on the outlook as they expect demand to improve. While input costs and output prices rose, the move was muted.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 01/06/2023 | 0600/0800 | ** |  | DE | Retail Sales |

| 01/06/2023 | 0715/0915 | ** |  | ES | IHS Markit Manufacturing PMI (f) |

| 01/06/2023 | 0745/0945 | ** |  | IT | S&P Global Manufacturing PMI (f) |

| 01/06/2023 | 0750/0950 | ** |  | FR | IHS Markit Manufacturing PMI (f) |

| 01/06/2023 | 0755/0955 | ** | | DE | IHS Markit Manufacturing PMI (f) |

| 01/06/2023 | 0800/1000 | ** |  | EU | IHS Markit Manufacturing PMI (f) |

| 01/06/2023 | 0830/0930 | ** |  | UK | S&P Global Manufacturing PMI (Final) |

| 01/06/2023 | 0830/0930 | ** | | UK | BOE M4 |

| 01/06/2023 | 0830/0930 | ** | | UK | BOE Lending to Individuals |

| 01/06/2023 | 0900/1100 | *** | | EU | HICP (p) |

| 01/06/2023 | 0900/1100 | ** | | EU | Unemployment |

| 01/06/2023 | 0930/1130 | | EU | ECB Lagarde Speech at German Savings Banks Conference | |

| 01/06/2023 | - | *** |  | US | Domestic-Made Vehicle Sales |

| 01/06/2023 | 1215/0815 | *** | | US | ADP Employment Report |

| 01/06/2023 | 1230/0830 | ** | | US | Jobless Claims |

| 01/06/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 01/06/2023 | 1230/0830 | ** | | US | Non-Farm Productivity (f) |

| 01/06/2023 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (final) |

| 01/06/2023 | 1400/1000 | *** | | US | ISM Manufacturing Index |

| 01/06/2023 | 1400/1000 | * | | US | Construction Spending |

| 01/06/2023 | 1400/1000 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 01/06/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 01/06/2023 | 1500/1100 | ** | | US | DOE Weekly Crude Oil Stocks |

| 01/06/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 01/06/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 01/06/2023 | 1700/1300 | | US | Philadelphia Fed's Pat Harker |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.