Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

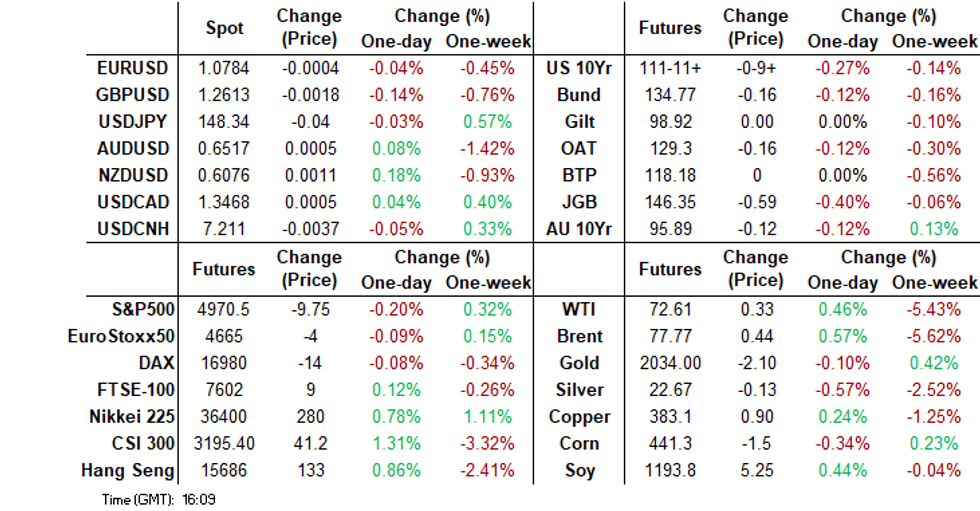

- US TSYS futures have found some support going into Asia lunch, with Mar'24 10Y futures testing new lows of 111-08 post Powell's 60 minute interview. He mentioned that there needs to be more disinflation evidence to cut rates. The CBS reporter stated that Powell suggested a mid-year cut, but this wasn't in the transcript of the interview. Cash yields curves have come off their highs of the day to trade 3.5-6.5bps higher.

- The USD was higher earlier but has lost ground as the session progressed, with NZD outperforming marginally.

- China equity volatility has been the other macro focus. Markets have recouped earlier losses, as the regulator pledged support over the weekend and take measures against risks of stock pledges. Still, sentiment appears far from buoyant at this stage.

- Later the Fed’s Goolsbee and Bostic speak. On the data front there are US/European January services ISM/PMIs.

MARKETS

US TSYS: Yield Gains Extend, But Off Post Powell Highs

TYH4 is trading at 111-10+, - 10+ from NY closing levels.Futures have found some support going into Asia lunch, with Mar'24 10Y futures testing new lows of 111-08 post Powell's 60 minute interview. He mentioned that there needs to be more disinflation evidence to cut rates. The CBS reporter stated that Powell suggested a mid-year cut, but this wasn't in the transcript of the interview.

- Mar'24 10Y futures ended the week lower to close at 111-22, with a low of 111-16. Earlier we hit news lows of 111-08, before finding some support, we have been unable to break back above the lows from Friday with the next support level at 110-26 from Jan 19, a close below here would imply a bear trigger.

- Earlier we saw buying in Mar'24 5Y futures, at 107-20.25, in 4,700 size, month lows are 107-16.75.

- Cash yields curves have come off their highs of the day to trade 3.5-6.5bps higher, with a slight flattening of the curve. Currently, the 2Y yield is 5.4bps higher at 4.416%, while the 10y is 5.1bps higher at 4.071%. The 2y10y is -2.2 lower today at -34.2, but off Friday's lows of -40.198.

- Data Tonight: ISM Non-Manufacturing, PMI while Atlanta Fed's Raphael Bostic speaks.

JGBS: Cheaper, 10Y-20Y Underperforming, Labour & Real Cash Earnings Tomorrow

JGB futures are holding sharply weaker, -65 compared to settlement levels.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Jibun Bank PMI Services & Composite. Labour and Real Cash Earnings, and Household Spending are due tomorrow.

- Cash US tsys are 2-6bps cheaper in today’s Asia-Pac session following Fed Chair Powell's appearance on 60 Minutes. This comes after Friday’s aggressive sell-off sparked by much stronger-than-expected Nonfarm Payrolls data.

- The cash JGBs are cheaper across the curve, with 10-20-year zone leading (5bps cheaper). The benchmark 10-year yield is 5.1bps higher at 0.723% versus the Nov-Dec rally low of 0.555%.

- The auction of 10-year inflation-indexed bonds drew a lower-than-expected cut-off price (104.50 vs 105.00 estimated by traders in the Bloomberg survey). However, the bid-to-cover ratio did increase to 3 from 2.73 at the previous sale on Nov. 7.

- (MNI) The BoJ on Monday offered to buy a total of JPY9 trillion of Japanese government bonds under repurchase agreements to cope with the rise of tomorrow's next repo rates caused by temporary strong fund demand. (See linkICYMI)

- The swaps curve has bull-steepened, with rates flat to 5bps higher. Swap spreads are tighter out to the 30-year.

RBA: MNI RBA Preview - February 2024: Prolonged Hold From Cautious RBA

- The RBA is unanimously expected (Bloomberg consensus) to leave rates unchanged at 4.35% at its February 6 meeting given lower-than-projected Q4 CPI and activity data have been soft since the last meeting. But it is likely to be too soon to remove the tightening bias given still elevated domestic price pressures and tight labour market.

- Talk of rate cuts is probably too soon and the Board may want more time to assess activity and price developments. Thus, a prolonged hold is certainly possible. Given heightened data dependency, the first rate cut is likely to coincide with a meeting that includes new quarterly CPI data and updated forecasts, thus making August more likely than June.

- This will be the first meeting that includes recommendations from the RBA review and there will be significantly more communication.

- See full preview here.

AU STIR: RBA Dated OIS Pricing 50bps Of Easing By Year End Ahead Of RBA Decision Tomorrow

RBA-dated OIS pricing is 6-15bps firmer for meetings beyond March ahead of tomorrow’s RBA Policy Decision. Nevertheless, a cumulative 48bps of easing remains priced by year-end.

- Aligned with the unanimous Bloomberg consensus anticipating a status quo decision, the market currently indicates a 0% likelihood of a 25bp hike or cut transpiring tomorrow.

- Concurrently, terminal rate expectations persist at the prevailing effective cash rate of 4.32%, having eliminated any prospect of further tightening since early December. To provide context, the market had factored in nearly 20bps of additional tightening leading up to the October CPI Monthly release in late November.

Figure 1: RBA-Dated OIS Terminal Rate Expectations Versus Cash Rate

Source: MNI – Market News / Bloomberg

AUSSIE BONDS: Holding Sharply Cheaper, RBA Policy Decision Tomorrow

ACGBs (YM -15.0 & XM -12.0) are holding sharply lower after dealing in relatively narrow ranges in today’s Sydney session. While the local market saw a raft of data releases (PMIs, Inflation Gauge, Trade Balance and Job Ads), US tsys were the key driver for ACGBs today.

- Cash US tsys are 2-6bps cheaper in today’s Asia-Pac session following Fed Chair Powell's appearance on 60 Minutes. This comes after Friday’s aggressive sell-off sparked by much stronger-than-expected Nonfarm Payrolls data.

- Cash ACGBs are 12-14bps cheaper, with the AU-US 10-year yield differential 6bps tighter at +4bps.

- Swap rates are 12-14bps higher.

- The bills strip has sharply bear-steepened, with pricing -4 to -16.

- RBA-dated OIS pricing is 6-15bps firmer for meetings beyond March ahead of tomorrow’s RBA Policy Decision. A cumulative 48bps of easing is priced by year-end.

- Tomorrow, the local calendar sees 4Q Retail Sales Ex Inflation, ahead of the RBA Policy Decision. Bloomberg consensus is unanimous in expecting a no-change decision.

- Bloomberg reported that Sally Auld, chief investment officer at JBWere, believes the RBA may seek to push back against market bets on any sort of rapid pivot toward interest-rate cuts at Tuesday’s policy meeting. (See link)

AUSTRALIAN DATA: Trade Data Show Softening Capex Imports & Strong Commodity Volumes

The merchandise trade surplus narrowed slightly in December as export growth underperformed import growth. It came in at $10.96bn after $11.76bn with imports rising 4.8% m/m and exports 1.8%. The data doesn’t change the view of the economy with signs that the domestic economy is softening and export growth solid to Australia’s largest trading partner.

- Goods exports rose for the third consecutive month in December but were still down 5% y/y but this improved from -8.5%. The December rise was driven by non-monetary gold +20.2% m/m. Key metal ores and coal export values fell on the month but metals rose strongly.

- Merchandise imports rose for the first time since September driven by transport equipment parts and are down 1.8% y/y. Consumer goods rose 9.8% m/m but are down 2.6% y/y, in line with weak household demand. Capex imports are signalling softer investment growth as they fell 1% m/m in December, third straight drop, and are now down 5.1% y/y.

Source: MNI - Market News/ABS

- Furniture retailers have said that the industrial disputes in Australian ports and rerouting of ships away from the Red Sea are now resulting in delays of imports. This may be seen in the Q1 import data.

- Exports to China remain robust rising 14.7% y/y, the 16th straight positive. But shipments to the rest of Asia are weak with Japan down 33.5% y/y and Korea -21.2% y/y and Indonesia -21.9% y/y. Iron ore volumes to China and coal to Japan and Taiwan were robust. While there was a 2.8% drop in LNG unit values, export volumes rose strongly by 16.8% despite the mild winter in north Asia.

Source: MNI - Market News/ABS

NZGBS: Closed On A Weak Note, Pressured By US Tsys

NZGBs closed on a weak note, with benchmark yields 11-12bps higher. With the domestic data calendar light (ANZ Commodity Prices as the sole release), the local participants have likely monitored today's extension of Friday’s post-payrolls sell-off in US tsys. Cash US tsys are trading 2-5bps cheaper in today’s Asia-Pac session, with a flattening bias, after an airing of a pre-recorded interview with Fed Chair Powell on 60 Minutes.

- The NZ-US 10-year yield differential ended the session 6bps narrower, settling at +56bps. This places it near the midpoint of the range observed over the last 12 months, which has fluctuated between +40 and +85bps.

- In contrast, the NZ-AU 10-year yield differential is currently positioned towards the upper end of its recent trading range, registering at +54bps. Over the past three months, this differential has hovered within a range of +30 to +60bps. However, it's worth noting that the 12-month high for this differential stands at approximately +100bps.

- Swap rates are 10-14bps higher, with the 2s10s curve flatter.

- RBNZ dated OIS pricing is 1-10bps firmer across meetings. A cumulative 86bps of easing is priced by year-end.

- Tomorrow, the local calendar is empty, ahead of 4Q Employment and Wages data on Wednesday.

FOREX: Dollar Up, But Away From Post Powell Highs

USD indices are holding higher, albeit way from best levels at this stage. The BBDXY was last near 1242 (+0.15%). Earlier highs in the index were at 1243.45 as headlines from Fed Chair Powell's interview on 60 Minutes crossed.

- The tone from interview appeared similar to last week's FOMC press conference, around a March rate cut as being unlikely and caution around easing policy too soon. Still the transcript points to plenty of discussion around easing. BBG headlines crossed that the CBS reporter stated that mid year was the most likely window for a cut, although this didn't appear in the transcript.

- US TSY futures broke lower on the headlines but have stabilized as the afternoon session progressed. US yields were last 2-5.5bps higher, led by the front end.

- USD/JPY got to 148.82 earlier, fresh highs for the year, but we now sit back at 148.35/10 little changed for the session.

- NZD/USD is marginally higher, off intraday and new yearly lows of 0.6050. The pair last at 0.6070. Data releases in NZ and Australia haven't impacted sentiment today.

- AUD/USD is marginally underperforming, last near 0.6505/10, with earlier lows at 0.6486.

- EUR/USD sits down slightly, last near 1.0780 (earlier lows were at 1.0767).

- Looking ahead, we have the US non-manufacturing ISM index along with speak from the Fed's Bostic. The BoE's Pill is also scheduled to speak.

CHINA EQUITIES: Equity Volatility Continues, Albeit Around A Weaker Trend, But Limited Spillover

Weakness/volatility in China equities remains the main focus point from a macro standpoint, although there isn't much in the way of spill over to other asset classes at this stage.

- Today's moves follows sharp volatility from Friday's session. The weekend also saw regulators vowing to stabilize sentiment, but it still seems we are searching for a circuit breaker at this stage.

- The CSI 300 was down by around 2% earlier, which put the index very close to intra-day lows from Friday. We have since rebounded back to around flat. A break sub 3000 would be fresh lows in the index back to 2019.

- Small cap indices were seeing the heaviest losses earlier. The CSI 1000 off over 8%, but we are now back to down around 6.3%.

- In HK, the HSI is only marginally lower at the time of writing, while the HS China Enterprise Index is also back to around flat.

- The spill over to USD/CNH is only very mild, with USD/CNH sitting slightly lower at this stage, last near 7.2130. It also hasn't impacted G10 FX in a major way. Other regional equity markets are mixed.

- Earlier we had the Caixin services PMI for Jan. It printed at 52.7, versus 53.0 forecast and 52.9 prior. The market didn't react though.

ASIA EQUITIES: Regional Equities Mixed After US Jobs & Powell Interview

Regional Asia equities are mixed today, with Japan the outperformer. Higher than expected US Jobs data on Friday has been weighing on markets, while Fed President Powell's comments on 60 minutes this morning implied a rate cut won’t be coming until later in the year.- Japan equities are higher this morning outside of any real catalyst, the USDJPY is making new yearly highs, which could be helping exporters. BoJ has also offered to buy bonds in two fund-supplying operations to contain an increase in a key short-term interest rate (BBG). After Falling 35% in two days, on the back of losses sustained in their US commercial real estate portfolio, Aozoro Bank has found support, trading higher by 5.30% Currently the Nikkei is higher by 0.50% while the Topix is 0.55%

- Australia equities are lower this morning after the strong US Jobs data Friday and Powell's interview on 60 minutes earlier this morning implying a rate cut won’t be coming until later in the year, while Australia also saw raft of data releases (PMIs, Inflation Gauge, Trade Balance, and Job Ads). The RBA is out tomorrow with their interest rate announcement, expected to be left unchanged at 4.35%. Currently the ASX200 is lower by 1%.

- South Korea equities are lower to start the week, after a great start to the month last week. Government initiatives to close the "Korea Discount" were announced, with the KOSPI seeing $2.2b of inflows this month, we are giving some of those gains this morning with the KOSPI lower by 0.80% largely on the back of real money accounts taking profits.

- Taiwan, has so far escaped the sell off in Asia and is trading higher by 0.21%. CPI out tomorrow estimated to come in at 2.10%

- Elsewhere in SEA, Higher US yields are weighing on performance with markets largely down.

OIL: Crude Off Lows As US Downs Houthi Missiles

Oil prices trended lower through most of today’s APAC session, but have begun to recover following news that the US hit Houthi missiles on Sunday after strikes on Houthi positions in Yemen the day before. WTI is up 0.2% to $72.40/bbl after a low of $72.16 and Brent is 0.3% higher at $77.58/bbl after falling to $77.31. The stronger USD and signs of robust supply have put a lid on crude with the USD index up 0.2% today to be up 0.8% since Thursday.

- The US hit targets in Iraq and Syria on Friday used by Iran’s Islamic Revolutionary Guard Corps and the associated militants. US President Biden said that this may not be the end of the response to the attack on a US base and that the US could strike targets in Iran if needed, but the US won’t be dragged into a long engagement in the region.

- Attacks by the Iran-backed Houthis on Red Sea shipping have resulted in French shipping giant CMA CGM deciding to reroute its vessels away from the Bab al-Mandab Strait after one of its ships was targeted last week by Houthis. Also, the Chairman of the Suez Canal Authority said that revenue had almost halved in January and flows have fallen 36%.

- News talks were taking place to achieve a ceasefire deal between Israel and Hamas resulted in crude falling sharply last week, but on Sunday US National Security Advisor Sullivan said that an agreement wasn’t to be expected soon.

- The Lukoil refining facility in Volgograd has closed after a fire, which the Russians blame on a Ukrainian drone, pushing diesel prices higher.

- Later the Fed’s Goolsbee and Bostic speak. On the data front there are US/European January services ISM/PMIs.

MIDEAST: US Responds To Attacks From Iranian-Backed Militants

The US continued its strikes against positions of Iranian-backed insurgents in response to a drone attack which killed 3 US troops and assaults on Red Sea shipping. President Biden has said that there could be further US strikes if deemed “appropriate” and wouldn’t rule out strikes on Iranian territory. Iran has denied involvement and warned the US.

- In Biden’s letter to Congress, he said that facilities in Iraq and Syria used by Iran’s Islamic Revolutionary Guard Corps and the associated militants were targeted. The aim was to deter them from attacking US troops but the Iraqi and Omani governments have voiced concern that the US is risking stability in the region.

- The Iranian-supported Islamic Resistance in Iraq has claimed responsibility for the drone attack on the US base and the US has said the drone was Iranian made, but Iran denied any connection.

- The West’s response continued on Saturday with the US and UK striking Houthi positions in 13 places in Yemen, as they try to weaken the Iran-backed group to stop its attacks on Red Sea shipping. But the Houthis have said that they will continue to attack as the US strikes “will not deter” them from their “moral, religious, and humanitarian stance in support of the resilient Palestinian people in the Gaza Strip.

- French shipping company CMA CGM, the third largest container shipper globally, has decided to reroute its vessels away from the Bab al-Mandab Strait after one of its ships was targeted last week by Houthis. It had continued to use the Suez Canal with French naval escorts but has decided that the area is now too risky. The Chairman of the canal said that revenue had almost halved in January and flows have fallen 36%.

GOLD: Stronger Than Expected US Payrolls Pressure On Friday

Gold is 0.4% lower in the Asia-Pac session, after closing 0.7% lower at $2039.76 on Friday.

- Bullion came under firm pressure as the USD soared after a strong US Payrolls Report. The employment report showed a broadly higher-than-expected Change in Nonfarm Payrolls: Total +353k vs +185k est. (prior up-revised to +333k from 216k) and Private +317k vs +170k est. The Unemployment Rate was 3.7% vs 3.8% est., while the Labour Force Participation Rate was near steady at 62.5% vs 62.6% est.

- The 2-year US Treasury yield shunted 16bps higher to 4.36%, the largest daily move since March 2023. 10-year yield increased 14bps to 4.02%, marking a sharp reversal from the 2024 low of 3.81%, seen in the lead-up to the FOMC. The sell-off has continued in today's Asia-Pac session.

- The large upside surprise to US payrolls pushed back the prospect of rate cuts by the Federal Reserve until later in the year—March's chance of a 25bp cut declined to 20% from 38% pre-data. May has a cumulative 23bps of easing, while June has a cumulative 45bps.

- Nevertheless, the precious metal held onto gains for the week, with a high of $2065.48, buoyed by US retaliatory Middle East strikes. Support is seen at $2033.0 (20-day EMA), according to MNI’s technicals team.

ASIA FX: Most USD/Asia Pairs Higher, CNH Ignores Local Equity Volatility

Most USD/Asia pairs are higher in line with firmer USD index levels post the Fed Chair Powell interview earlier. Carry over from Friday's USD gains has also been evident. China equity volatility continues, but isn't spilling over into wider sentiment at this stage. Tomorrow, we have Philippines CPI as the main focus point.

- USD/CNH has drifted a little lower in the first part of Monday trade. The pair last near 7.2100. Earlier highs above 7.2200 drew selling interest. Equities sentiment has been very volatile in small cap stocks particularly, but the post lunch break has seen some firmness return, with the CSI 300 back in positive territory as the regulatory warned it would take measures against risks of stock pledges (BBG). The USD/CNY fixing error re-widened, consistent with USD strength.

- 1 month USD/KRW is comfortably off Friday highs, the pair around 0.50% stronger in won terms, last near 1330. This keeps us within recent ranges though and avoids a fresh 1340 test. Onshore equities have recouped earlier losses, the Kospi last near -0.70% after being down by 2% at one stage.

- USD/IDR pushed above 15700 in early trade today, but sits slightly lower in latest dealings. Friday lows in the pair were close to 15645, which recent weakness above 15800 saw intervention rhetorci rise. Weekend comments from BI Governor Perry Warjiyo reiterated that the rupiah is central to the outlook for easier policy settings. The Governor stated that it will look to rupiah stability in the second half to gauge the CB's ability to cut rates.

- USD/THB is around session highs, last in the 35.70/75 region, around 1.35% weaker in baht terms for the session. We are sub late Jan highs at 35.88, but back above all key EMAs. The 200-day coincides with recent lows in the 35.20/25 region. Jan CPI data was a touch weaker than expected and the government has been on the wires this afternoon talking about the potential need for near term stimulus.

- USD/PHP sits back at 56.25 in recent dealings, around 0.60% weaker in spot PHP terms. The 1 month NDF is slightly higher and also weaker in PHP terms versus end Friday levels in NY on Friday (last at 56.28).Broader USD gains and a firmer US yield backdrop have continued today. These moves keep us within recent ranges though. Spot lows around 55.92 last week, were just under the simple 200-day MA. Topside resistance could be expected just above 56.50, which has marked recent highs. Domestic political developments will remain a focus point, although broader concern in asset markets is not evident. Local shares sit just off recent highs. The National Security Advisor to President Marcos Jr stated the country will use force to quell secession moves.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 05/02/2024 | 0700/0800 | ** |  | DE | Trade Balance |

| 05/02/2024 | 0700/0200 | * |  | TR | Turkey CPI |

| 05/02/2024 | 1000/1100 | ** |  | EU | PPI |

| 05/02/2024 | 1500/1000 | *** |  | US | ISM Non-Manufacturing Index |

| 05/02/2024 | 1530/1030 |  | CA | BOC quarterly Market Participants Survey | |

| 05/02/2024 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 05/02/2024 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 05/02/2024 | 1730/1730 |  | UK | BOE's Pill MPR Virtual Q&A | |

| 05/02/2024 | 1900/1400 | | US | Atlanta Fed's Raphael Bostic |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.