Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Early focus was on EU parliamentary election results from Sunday, which showed a swing to right leaning parties. French President Macron has called snapped legislative elections in the aftermath of the result.

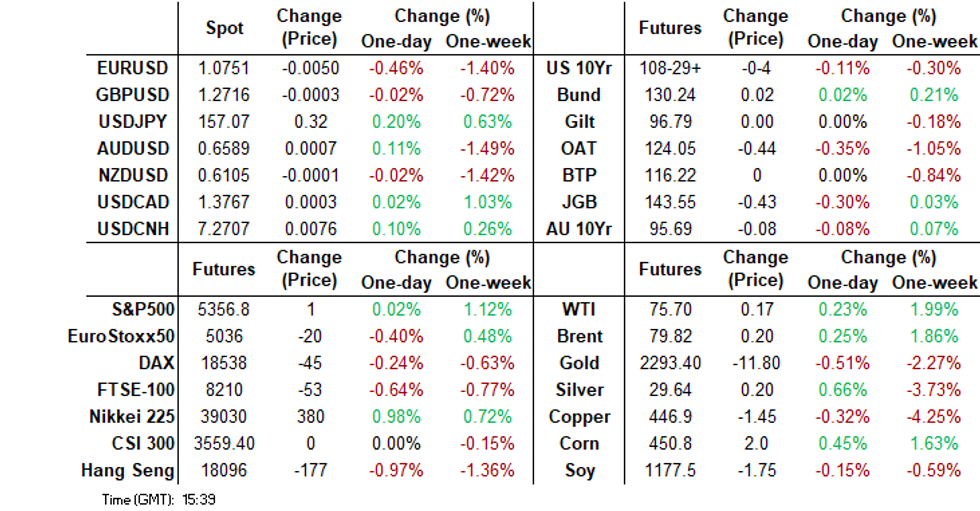

- EU related assets have been under pressure, EUR/USD comfortably sub key short term support and EU equity and bond futures lower. The USD is mostly higher against other currencies as well, building on gains from Friday post the NFP print. US Treasury futures opened a touch lower and have since managed to trade sideways and in very tight ranges.

- The only data of note has been Japan Q1 GDP revisions, which were broadly unchanged at a headline level. Elsewhere it has been a quieter session with China, Hong Kong and Australia all out today.

- Looking ahead it is a fairly quiet start to the week data wise. We do have NY Fed 1-Yr Inflation Expectations printing later.

MARKETS

US TSYS: Treasury Futures Steady, Ranges Very Tight

- Treasury futures opened a touch lower and have since managed to trade sideways and in very tight ranges. TU is -0-01⅜ lower at 101-27¾, while TY is -04 at 109-06

- Volumes: TU 45k, FV 73k TY 90k

- Tsys Flows: FV Block Seller & Buyer, TU/UXY Block Steepener

- Looking at TYU4 technical levels, initial support is at 108-27 (Jun 3 lows), with 108-04+ (Trendline drawn from the Apr low) the next target. While to the upside initial resistance is at 110-21 (June 7 highs), a break here would see a test of 110-27+ (1.00 proj of the Apr 25 - May 16 - 29 price swing)

- Cash treasury curve is slightly steeper today, with the 2Y +0.2bp to 4.891%, the 10Y +1.2bps at 4.447% while the 2y10y was +0.770 at -44.117.

- French President Emmanuel Macron and German Chancellor Olaf Scholz suffered defeats in the European Parliament elections.

- Late year rate cut projections have receded vs. late Thursday levels (*): June 2024 at -1.3% w/ cumulative rate cut -.3bp at 5.328%, July'24 at -8% w/ cumulative at -2.3bp (-5.9bp) at 5.307%, Sep'24 cumulative -13.7bp (-21.3bp), Nov'24 cumulative -20.3bp (-30.7bp), Dec'24 -37.4bp (-49.7bp).

- Looking ahead: NY Fed 1-Yr Inflation Expectations

EU: Elections Show Swing To The Right, Macron Calls Snap French Legislative Elections

Sunday's European parliamentary elections showed a swing to the far right. Leaders of both France and Germany saw their respective parties poll poorly. German Chancellor Olaf Scholz's SPD suffered their worst result. In France, President Macron has called a snap legislative election after his Renaissance party performed quite poorly relative to Marine Le Pen's National Rally party.

- The first round of legislative elections take place on June 30, the second round on July 7. If Macron losses the legislative election it will limit his power domestically for the remaining term of his Presidency.

- Italy PM Giorgia Meloni's right wing Brothers of Italy party performed well, strengthening her local position.

- More broadly, the center-right European People's Party (EPP) won the most number of seats, which should support Ursula von der Leyen, who seeks a second term as commission President.

- The balance of power is still likely to rest with the socialists and democrats, although Reuters notes that the EPP may still need the support from some parts of the right (see this link).

- Fresh political uncertainty has weighed EUR/USD in early Asia Pac dealings. We got to lows of 1.0765, but sit back near 1.0775 in recent dealings. We are off close to 0.30%.

- This puts us sub the May 30 low of 1.0788, which is a key short term support point.

JGBS: Futures Biased Lower, Cash Yield Curve Steeper

JGB futures currently sit close to session lows, JBM4 last at 143.51, -.47 versus settlement levels. Upticks above 143.60 have sold by the market so far today.

- Spillover from a softer US Tsy and EU bond futures backdrop have arguably been key drivers for JGB markets today. For US moves, this looks to be carry over from Friday's sharp selloff post the NFP/wages data beat.

- For EU bond futures sentiment has been rattled by the Sunday EU parliamentary election results, which showed a swing to right-wing parties, while French President Macron has called a snap legislative election.

- For JGB futures, downside focus will rest on whether we can re-test late May lows sub 143.00.

- On the data front, we had Q1 GDP revisions earlier. Q/Q growth remained at -0.5%. Business spending remained negative but not to the degree as initially reported.

- For cash JGB yields, the curve has steepened. 10yr yields sit near 1.03% up around 5bps. The 20-40yr tenors are 6-7bps higher. The 10yr swap rate is up a further 2bps to 1.055%.

- Looking ahead, it is largely second tier data head of Friday's BoJ decision.

NZGBs: Curve Steady, Yields Rise 9-10bps

NZGBs closed cheaper, with yields 9-10bps higher following large moves in the US on Friday on the back of stronger Non farm payrolls. There has been little else in the way of market moving headlines, with the market now adjusting to the rate hike percentage.

- NZGBs opened trading for the week just 5-6bps higher, although continued to sell off throughout the session and closed near session highs

- The 2yr is +9.5bps at 4.891%, 10yr +9.6bps at 4.710%

- Swaps are 2-10bps higher, curve steepened

- Headlines: Chinese Premier Li Qiang to visits NZ this week. Luxon to explore AUKUS opportunities

- RBNZ dated OIS pricing is little changed. A cumulative 24bps of easing is priced by year-end.

- looking Ahead, REINZ House Sales, BusinessNZ Manufacturing PMI & Food Prices on Friday

ASIA PAC STOCKS: Asian Equities Mixed As Many Markets Shut for Public Holidays

Asian equities traded in a narrow range today with mixed performances across the region. The MSCI Asia Pacific Index fell by up to 0.2%, with declines in South Korea, where the Kospi dropped due to reduced bets on US interest rate cuts, and in Thailand, where the SET Index hit a 3.5-year low due to a stronger dollar. Meanwhile, Japanese stocks gained as higher bond yields lifted financials and a weaker yen boosted exporters. Indian stocks swing between gains and losses as traders awaited new government announcements. Trading volumes were lower than usual with markets in China, Hong Kong, Taiwan, and Australia closed for holidays.

- Japanese stocks have rebounded due to rising bond yields, benefiting financial firms. This movement comes amid speculation that the Federal Reserve will maintain its current policy stance and that the Bank of Japan may tighten its policies. Exporters, particularly automakers and machinery firms, gained from a weaker yen against the dollar. The Topix is up 0.90%, the Topix Bank Index is up 1.39% while the Nikkei 225 is up 0.83%

- South Korea’s Kospi index dropped by up to 1.2%, following its best weekly performance in four months, due to rising Treasury yields and diminishing rate cut expectations after strong US nonfarm payroll growth. Samsung, LG Energy Solution, and Celltrion were the main contributors to the decline. Nearly all sectors saw losses, except for machinery and food. Last week, the Kospi gained 3.3%, marking its best weekly advance since early February. The small-cap Kosdaq Index fell by as much as 0.6%.

- Elsewhere in SEA, New Zealand Equities closed down 0.65%, Singapore equities are 0.29% lower, Malaysian equities are down 0.17%, Philippines Equities are 0.90% lower, while Indonesian & Indian equities are up about 0.20%.

Asian Equity Flows Remain Negative, India Sees Majority of Selling

- South Korean equities edged higher on Friday, flows remain mixed with a $127m outflow on Friday, ending two days of inflows. The 5-day average is $188m, now above the 20day average of -$32m and the longer-term trend at $140m.

- Taiwan equities hit new all time highs of Thursday before a small sell off on Friday as investors looked to take profits. We saw an outflow of $175m, and a net outflow of $65m over the past 5 sessions. The 5-day average is now -$13m, below the 20-day average of $88m and the 100-day average at $25m.

- Thailand equities were higher on Friday, although returns were mixed over the past week, while Foreign investors continued to sell equities with Friday marking the 12th straight day of selling for a total outflow of $276m. The 5-day average is now -$55m, below both the 20-day average at -$26m and the 100-day average at -$24m.

- Indonesian equities have now marked 12 straight sessions of selling from foreign investors, with the past 5 session seeing a net outflow of $143m. The JCI made new ytd lows and closed the week below 7,000. The 5-day average is now -$29m, the 20-day average at -$36m and the 100-day average at -$3m.

- Philippines equities were little changed on Friday, with a small inflow as well, marking the first time in two weeks we had two days of inflows. The past 5 sessions have seen an outflow of $35m. The 5-day average is -$7m, below the 20-day average at -$7m and the 100-day average at -$5.4m.

- Indian equities have been very volatile over the past few days due to the presidential elections, after an initial 5% sell off during the votes being counted we have since pared those losses, outflows however still remain negative with a total outflow $1.76b . The 5-day average is now -$353m, 20-day average is -$211m, both below the 100-day average at $6.6m

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | -128 | 944 | 14251 |

| Taiwan (USDmn) | -175 | -65 | 2545 |

| India (USDmn)* | -811 | -1768 | -4791 |

| Indonesia (USDmn) | -55 | -55 | -479 |

| Thailand (USDmn) | -13 | -277 | -2446 |

| Malaysia (USDmn) * | 35 | -48 | -86 |

| Philippines (USDmn) | 7 | -35.6 | -459 |

| Total | -1141 | -1304 | 8534 |

| * Data Up To Jun 6 |

FOREX: EUR Weakness Follows EU Elections, USD Supported Elsewhere

USD strength has carried over from Friday's session into the first part of Monday trade. The BBDXY index is up a further 0.20%, last tracking around 1265.3. This puts the index back close to early May levels.

- EUR/USD weakness was evident from early trading, as weekend parliamentary elections showed firm support for right-wing parties and placed fresh clouds over the French near term outlook. Legislative elections were called for the end of this month by President Macron following his party's poor results from the Sunday elections.

- The currency is tracking to fresh lows near 1.0750 in recent dealings, off a further 0.4% so far today. We are below key short term support (1.0788, May 30 low), with 1.0724 (the May 9 low) a potential downside target.

- Yen initially outperformed EUR, but is also tracing weaker. USD/JPY is back to 157.10/15, firmer by 0.25%. May 29 highs at 157.71 is a key upside focus point. We had Q1 GDP revisions data out earlier, but there weren't any major shifts relative to the initial print (q/q growth remained at -0.5%).

- US yields have ticked higher, lending some further support to USD/JPY. Regional equity sentiment is mixed. Japan stocks are the main positive.

- AUD/USD is a little higher, but still sub 0.6590. Australian markets have been closed today, while China and Hong Kong markets are also out. NZD/USD is close to 0.6100, little changed for the session.

- Looking ahead, it is a relatively quiet start to the week data wise.

OIL: Modestly Higher Ahead Of Key Event Risks This Week

Oil benchmarks are marginally higher in the first part of Monday dealings. Brent has been unable to recapture the $80/bbl handle but still sits +0.355 higher, unwinding Friday's modest loss. WTI front month is around $75.80/bbl, showering a similar trajectory.

- Broadly oil benchmarks maintain ranges from the latter stages of last week. For Brent, we are sub all key EMAs, with the 20-day at $81.57/bbl the nearest on the topside. Earlier June lows rest at $76.76/bbl.

- Goldman Sachs expected Brent to recover to $86/bbl in Q3, as the market gets pushed into deficit (see this link for more details).

- Outside of this week's Fed meeting, note we also have monthly reports from OPEC and the International Energy Agency due on Tuesday and Wednesday respectively.

GOLD: Largely Holding Friday Losses

Gold has largely tracked sideways in the first part of Monday Asia Pac trade, we remain sub $2300. This leaves us holding the bulk of Friday's near 3.5% fall. We ended last Friday losing close to 1.5% for the week.

- The USD is mostly firmer today, as EUR weakness and yen losses have pushed the BBDXY index up a further 0.20% to 1264.80. EUR weakness is reflected of renewed political concerns following the weekend parliamentary elections. This may be driving some risk aversion in markets, a likely gold support at the margins.

- From Friday we also had China FX reserves which showed a further reduction in gold buying.

- Levels wise for gold, a further correction lower could see early May lows near $2277 targeted. Further south is the 100-day EMA close to $2240. Friday highs from last week were near $2387.75. The 50-day EMA rests close to $2313.

ASIA FX: Weaker EUR, JPY Weigh On Regional FX Sentiment

USD/Asia pairs are mostly higher, albeit to varying degrees. Cross asset headwinds are evident with a weaker EUR evident in the G10 space, with EU weekend results weighing. US yields are also a touch higher, building on Friday's strong gains. Regional equities are mixed, although China/HK markets are closed today.

- USD/CNH is higher firming above 7.2700, but found selling interest near 7.2730. CNH weakness is in line with EUR and JPY weakness, although the beta with respect to such moves remains low. China markets return tomorrow. This week we get new loans/credit figures for May, along with Inflation data for May as well.

- Spot USD/KRW got above 1380 in early trade, but found some selling interest above that level, we lats track near 1377/78, still around 0.90% weaker in KRW terms. Local equities are down by around 0.30% at this stage, but still above the 2700 level in index terms.

- Spot USD/IDR has gapped higher back to 16290, which is around recent highs. The 1 month NDF is slightly higher, last near 16300/05. Consumer sentiment eased to 125.2 from 127.7 in April.

- USD/THB spot has risen by over 1% to 36.90/95. Recent highs in the pair rest above 37.00 from late April.

- USD/MYR has gaped higher, last near 4.7200 and back above the simple 200-day MA. IP for April was close to forecast, printing at 6.1%y/y.

- Spot USD/PHP is back up to 58.75/80, also close to earlier June highs, near 58.83.

- Spot USD/INR is around 83.50, with Reuters reporting central bank USD sales are likely going through at this level.

Indonesia: INDON Sov Spreads Tighten, Consumer Confidence Falls

Indonesian sov yields pushed higher following moves made in the US on Friday after a surprise NFP beat.

- The INDON curve has widen today, yields are 5 10bps higher. The 2Y yield is +9.5bps at 5.335%, 5Y yield is +8bps at 5.08%, the 10Y yield is 8bp at 5.147%, while the 5-year CDS is 0.5bp lower at 71.5bps.

- The INDON to UST spread diff the 2Y is now 44.5bps (-5bps), 5yr is 60bps (-10bps), while the 10yr is 70bps (-8bps).

- In cross-asset moves, USD/IDR is 0.61% lower today at 16,292. The JCI is 0.35% higher . While tsys futures have edged lower throughout the day, with yields about 1bps higher.

- Earlier Indonesian consumer confidence for May fell to 125.2 from 127.7 in April.

- Looking ahead, there is little on the data calendar, with a bond auction on Tuesday the major focus.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 10/06/2024 | 0600/0800 | ** |  | SE | Private Sector Production m/m |

| 10/06/2024 | 0600/0800 | *** |  | NO | CPI Norway |

| 10/06/2024 | 0800/1000 | * |  | IT | Industrial Production |

| 10/06/2024 | - |  | JP | Economy Watchers Survey | |

| 10/06/2024 | 1530/1130 | * |  | US | US Treasury Auction Result for 13 Week Bill |

| 10/06/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 10/06/2024 | 1700/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.