Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

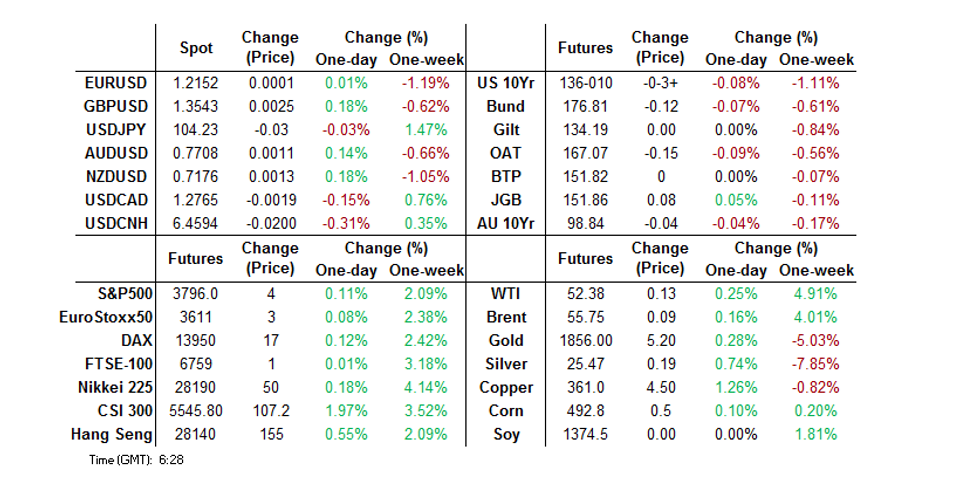

- T-Notes trade through recent lows with TY options rejig/profit taking headlining overnight.

- Familiar stories dominate the wires, namely the Fed taper debate, tension surrounding Hong Kong and the political situation in DC.

- G10 FX sticks to tight ranges.

BOND SUMMARY: Core FI Mixed After Early Pressure In Asia, TY Option Flow eyed

T-Notes recovered from worst levels of the Asia-Pac session after early trade saw Monday's low breached, with some profit taking on low vol TY downside plays (both on screen and via block), before further block flow pointed to a position rejig and further profit taking, as some suggested that the Asia-Pac participant may have left themselves short 30K of both the TYH1 136.50/136.00 and 136.50/135.50 put spreads. Macro headline flow was generally light, with Fed's Kaplan (a non-voter in '21) pointing to the potential for QE tapering later this year and a sign from Messrs Trump & Pence that the President plans to see out the short remainder of his term headlining overnight. RTRS source reports pointing to the potential for a deeper Chinese crackdown re: the HK political sphere may have provided some light support. T-Notes last -0-03+ at 136-10, while cash Tsys trade little changed across the curve. Focus today moves to Fedspeak from Brainard, George & Rosengren, 10-Year supply from the Tsy, in addition to JOLTS & NFIB small biz confidence data.

- JGB futures firmed in afternoon trading, aided by a moderation in offer to cover ratios in the BoJ's latest round of 3-25 Year Rinban ops, while FinMin Aso noted that the government will maintain its existing budget outlines for now. This came after early morning trade saw some light pressure on the back of the broader impetus seen in core global FI in recent sessions, with Tokyo returning from an elongated weekend. Futures finished +8 (at best levels). The Rinban allowed the belly of the cash curve to outperform at the margin, with some modest weakness in the wings vs. Friday's closing levels. Expectations are building for a widening of the area covered by the COVID-19 state of emergency, which is set to be announced in the coming days.

- Aussie bonds traded in a lacklustre fashion, with little in the way of notable idiosyncratic headline flow seen. YM -0.5, XM -4.0 at the close, following the broader themes seen in core FI during Asia-Pac hours after the latter printed at the lowest levels seen since the March vol in early Sydney trade, before edging away from lows alongside U.S. Tsys. Cash trade saw the 10 to 15-Year sector lag on the curve, with swaps tightening vs. ACGBs. Corporate flow saw University of Melbourne price up A$150mn of a '31 line, which may have added to the pressure seen early on. Bills were virtually unchanged through the reds. We should also flag that surplus E/S balances lodged at the RBA have topped the A$100bn mark for the first time in recent days.

FOREX: Tight Ranges All Round

A quiet session, US dollar strength has taken a breather in Asia on Tuesday while risk sentiment in the region is mixed. DXY last at 90.576 after closing yesterday at 90.465, the index tread water throughout the session.

- AUD & NZD are flat. Both initially moved higher alongside equity indices in the region, before gradually giving back. AUD/USD hovers around the key 0.77 level, while NZD/USD has receded from 0.72. Headline flow from the region has been thin, New Zealand did announce plans to tighten coronavirus detection measures for travellers. Both head into the European time zone near session lows.

- JPY is broadly flat at 104.30. Trade data today from Japan showed November's surplus rose to JPY 616bn against JPY 474bn expected, but lower than the JPY 971 in October. Bank lending data was also released which showed bank lending excluding trusts rose 5.9% in December, in line with October.

- The PBOC drained a net CNY 5bn from the system today, and fixed USD/CNY at 6.4823 around 59 pips higher than yesterday. The PBOC has weakened the yuan 115 pips so far this week, but USD/CNY bucked the trend and rose against the greenback. President Xi reaffirmed the nation's support for the policy of dual-circulation, as he noted that policymakers want to build a "super-sized" domestic market to ensure a high level of self-sufficiency, which in term supported risk sentiment.

- EUR slightly lower from the NY close, some chatter of bids surrounding 1.2125 coming from leveraged names. Some sizable put option strikes due today are EUR 1.4bn at 1.2250; EUR 1.4bn at 1.2200 and EUR 1.1bn at 1.2150.

FOREX OPTIONS: Expiries for Jan12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2150(E1.1bln-EUR puts), $1.2200(E1.4bln-EUR puts), $1.2230(E632mln), $1.2250(E1.4bln-EUR puts), $1.2275(E618mln), $1.2300(E2.1bln-mainly EUR puts), $1.2370-75(E826mln-EUR puts), $1.2400(E865mln-EUR puts)

- USD/JPY: Y102.90-00($984mln), Y103.10-25($1.4bln), Y103.35-43($616mln),

Y103.85-00($1.7bln-USD puts), Y104.10-30($1.1bln) - GBP/USD: $1.3995-1.4000(Gbp986mln-GBP puts)

- EUR/GBP: Gbp0.9300(E766mln)

- AUD/USD: $0.7500(A$516mln), $0.7650(A$508mln), $0.7750(A$828mln)

- USD/CAD: C$1.2750($615mln)

EQUITIES: China Outperforms As E-Minis Fade Back From Overnight Highs

E-minis traded either side of unchanged in Asia-Pac hours, while the major regional equity markets were flat to higher, with little in the way of tier 1 macro headline flow noted in the timezone. This allowed participants to step back and assess multiple, well discussed risk matters in the wake of a modest dip on Wall St.

- Chinese equities were the largest mover, with President Xi re-affirming the nation's support for the policy of dual-circulation, as he noted that policymakers want to build a "super-sized" domestic market to ensure a high level of self-sufficiency, which in turn supported Chinese equities.

- Nikkei 225 +0.1%, Hang Seng +0.9%, CSI 300 +1.9%, ASX 200 -0.3%.

- S&P 500 futures +4, DJIA futures +32, NASDAQ 100 futures +28.

GOLD: Not Threatening Recent Lows

Yesterday's low of $1,817.5/oz now represents the initial area of support which bears will look to force a break of to extend the recent sell off. Spot last dealing ~$10/oz higher on the day around the $1,855/oz mark, even with the DXY and U.S. real yields moving higher over the last 24 hours or so.

- Elsewhere, ETF holdings of gold have flatlined over the last few days.

OIL: A Quiet Start To The Week

WTI and Brent sit a handful of cents above their respective settlement levels, with the benchmarks unchanged to a touch lower vs. Friday's closing levels after a limited round of early trade this week, with crude hovering just shy of recent cycle highs. API crude inventory data will hit later on Tuesday.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.