Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

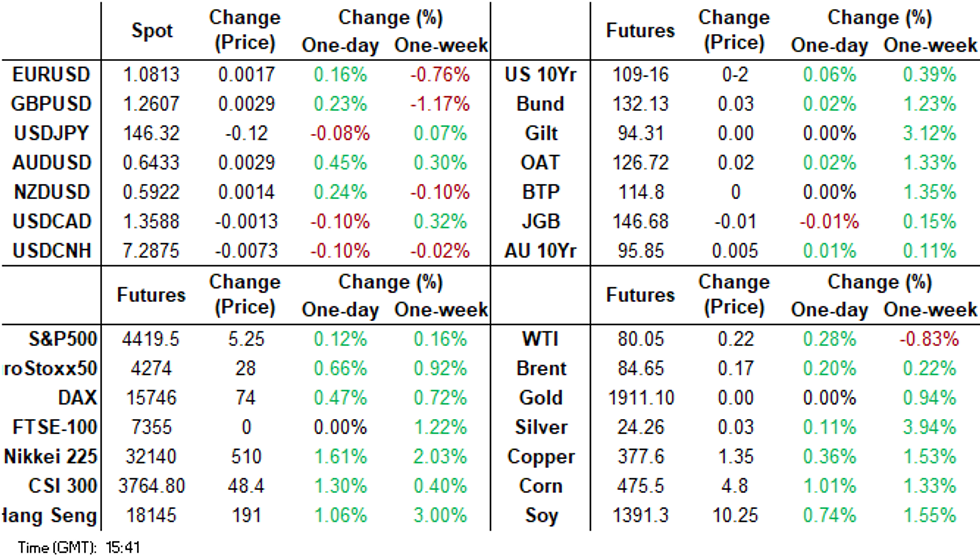

- China related assets rallied strongly in the first part of trade, as a variety of measures were announced, including cutting the stock trading levy (from 0.1% to 0.05%) for the first time since 2008. Onshore equities opened up +5%, but gains have been pared to less than 2% post the lunchtime break. USD/CNH has followed a similar trajectory, unable to sustain an early dip sub 7.2700.

- Elsewhere, US cash tsys sit little changed across the major benchmarks, as the market digests Jackson Hole from late last week. AUD/USD has outperformed in the G10 space, aided by the above China news and a retail sales beat. The cash ACGB curve has bear-flattened, with yields flat to 2bp higher.

- CPB data for June showed global trade deteriorated in the middle of the year. The trough in the Baltic Freight Index though is some sign that global trade growth may stabilise in the coming months. Global IP growth was stronger than trade in June according to CPB data, see below for more details.

- Looking ahead, there is a public holiday in the UK today and cash tsys will be closed during the European session. Further out we have Dallas Fed Mfg Activity, as well as Fedspeak from Fed VC Barr. The latest 2- and 5-Year Supply is due.

MARKETS

GLOBAL: Trade volumes & Prices Weak In Mid-2023

CPB data for June showed global trade deteriorated in the middle of the year. It fell 0.8% m/m to be down 2.5% y/y after -2.1% y/y. Growth had improved from the -2.9% y/y trough in December 2022 but is now deteriorating again. The trough in the Baltic Freight Index though is some sign that global trade growth may stabilise in the coming months.

- The Baltic Freight index fell sharply in June but has risen 10.1% m/m in August to date. While it is still 18.1% lower than a year ago, that has improved from -55.1% y/y in June. The index appears to have troughed earlier this year.

Source: MNI - Market News/Refinitiv

- Export volumes fell 0.3% m/m to be down 1.3% y/y after -1.2% in May and Q2 saw a 0.6% q/q drop. They were weak from both developed and emerging nations with negative 3-month momentum.

Source: MNI - Market News/Refinitiv

- Import volumes fell 1.1% m/m in June and -3.7% y/y after -2.9%, the weakest since August 2020.

- Trade prices remain soft falling 1.7% m/m again in June to be down 8.1% y/y with export prices down 8.9% y/y. Energy prices were weak falling 48.3% y/y, but oil prices didn’t rally until July, and raw material prices were down 18.2% y/y, off the trough of -25.6% in March.

GLOBAL: Sluggish Outlook For Global IP

Global IP growth was stronger than trade in June according to CPB data and rose 0.5% q/q in Q2. It increased 0.4% m/m after +0.3% the previous month but the annual rate slowed to 0.5% y/y from 1.1% and 3-month momentum, which is negative, deteriorated further. The S&P Global manufacturing PMI is signalling that output is contracting mildly but that while global IP may deteriorate further it shouldn’t collapse. In terms of other IP lead indicators, LME metal prices have been moving lower over 2023 but in August were down only 3.5% y/y and iron ore is up 0.7% y/y, both consistent with soft but not terrible IP.

Global growth %

Source: MNI - Market News/Refinitiv/Bloomberg

Global IP vs LME metal prices y/y%

Source: MNI - Market News/Refinitiv

US TSYS: Little Changed In Asia

TYU3 deals at 109-15, +0-01, a touch off the top of the 0-06 range on volume of ~109k.

- Cash tsys sit little changed across the major benchmarks.

- Tsys firmed from session lows alongside regional equities and marginally pressure on the USD after the China Securities Regulatory Commission cut the levy charged on stock trades supported risk assets.

- Earlier tsys had been marginally pressured in early dealing as local participants digested Fed Chair Powell's remarks at the Jackson Hole Symposium.

- FOMC dated OIS remains stable, a terminal rate of ~5.50% is seen in November with ~60bps of cuts by July 2024.

- There is a public holiday in the UK today and cash tsys will be closed during the European session.

- Further out we have Dallas Fed Mfg Activity, as well as Fedspeak from Fed VC Barr. The latest 2- and 5-Year Supply is due.

JGBS: Futures Pare Losses In The Afternoon Session, Jobless Rate and 2Y Supply Tomorrow

JGB futures have unwound much of the morning weakness, -2 compared to settlement levels, in the Tokyo afternoon session.

- There hasn’t been much in the way of domestic drivers to flag. June Leading and Coincident Indices, just released, printed respectively little changed at 108.9 and 115.1.

- Accordingly, local participants have spent the Tokyo session on headlines and US tsys watch. US tsys sit ~1bp richer across the major benchmarks in Asia-Pac trading.

- Cash JGBs are dealing mixed, with yields +/-0.4bp. The benchmark 10-year yield is 0.4bp higher at 0.665%.

- Bloomberg reports that Japan’s sovereign debt rating needn’t automatically change if the central bank lifts its negative interest rate policy, according to Fitch Ratings director Krisjanis Krustins. Nominal interest rates are only one factor for determining the trajectory of government debt, Krustins, who covers Asia-Pacific sovereigns for the firm, said in an interview on Aug. 25. (See link ICYMI)

- Swap rates are mixed, with pricing 0.4bp lower to 0.5bp higher. Swap spreads are mixed.

- Tomorrow the local calendar sees the Jobless Rate and the Job-To-Applicant Ratio for July, along with 2-year supply.

AUSSIE BONDS: Mixed, Near Session Cheaps, RBA Bullock Speaks Tomorrow

ACGBs (YM -3.0 & XM flat) are dealing at or near session lows. Retail sales data for July printed stronger than expected, although additional spending at catering and takeaway food outlets linked to the 2023 FIFA Women’s World Cup and school holidays boosted the overall result.

- The cash ACGB curve has bear-flattened, with yields flat to 2bp higher. The AU-US 10-year yield differential is 1bp higher at -7bp, after dealing at -10bp earlier in the local session.

- Swap rates are higher, with pricing flat to 2bp higher. EFPs are little changed, with the curve flatter.

- The bills strip has bear-steepened, with pricing -1 to -5.

- RBA-dated OIS is 2-8bp firmer for meetings beyond November, with Sep’24 leading.

- S&P Global Ratings reported that home loan arrears remained very low in Q2 rising to 0.97% for prime mortgages from 0.95% in Q1 and falling to 3.47% for non-prime from 3.7% due to the number of loans increasing. However, Roy Morgan released data showing the number of people at risk of mortgage stress rising 642k on a year ago to a record 1.5mn in the 3 months to July. (The Australian)

- Tomorrow the local calendar sees a speech from RBA Governor-Elect Bullock, titled “Climate Change and Central Banks”. On Wednesday, the CPI Monthly for July is on tap.

AUSTRALIAN DATA: Monthly Retail Sales Volatile, Momentum Positive But Soft

Retail sales rose a stronger than expected 0.5% m/m in July, which was also above most forecasts, as partial payback for the 0.8% drop in June. The monthly changes are volatile but 3-month momentum remains positive but softer than it has been and while retail sales continue to grow compared to a year ago that pace has slowed substantially from the post-Covid spending spree period. Nominal sales have been fairly steady since late 2022 up only 0.4% since October despite higher prices.

- Annual growth in retail sales moderated further in July to 2.1% y/y from 2.3%, the lowest since August 2021. 2019 averaged 2.7% growth. July CPI is published on Wednesday and is expected to rise 5.2% y/y.

- There was a July bounce in non-food retailing after the weak June readings. Department store sales rose 3.6% m/m to be flat on the year and clothing & footwear +2% m/m -0.4% y/y but household goods fell 0.2% m/m to be down 4.1% y/y. Restaurant sales remain robust rising 1.3% m/m to be up 9% y/y boosted by school holidays and the Women’s World Cup.

Source: MNI - Market News/ABS

NZGBS: Closed At Cheaps, AU-NZ 10Y Differential Too Negative

NZGBs closed at local session cheaps, with benchmarks flat to 1bp cheaper. Without domestic catalysts, the local market has largely tracked US tsys in the Asia-Pac session.

- A simple regression of the AU/NZ 10-year yield differential versus the AU-NZ 1Y3M swap differential suggests fair value is around -65bp versus the 10-year differential’s current level of around -85bp. The current negative regression error could be in part due to speculation that the September 12 release of the NZ Pre-Election Economic and Fiscal Update (PREFU) may highlight a material fiscal deterioration. (See link)

- The swap curve has twist flattened, with rates 2bp higher to 1bp lower. The implied 2s10s swap spread box is flatter.

- RBNZ dated OIS pricing is 1-2bp softer for meetings beyond Feb’24. Terminal OCR expectations sit at 5.65%.

- The local calendar is empty until Building Permits on Wednesday. On Thursday, ANZ Business Confidence is on tap, ahead of ANZ Consumer Confidence on Friday.

AU-NZ RATES: AU-NZ 10Y Yield Differential Lower Than It Should Be

Further to our previous discussion of the drivers of the AU-NZ 10-year yield differential, a simple regression of the AU/NZ 10-year yield differential versus the AU-NZ 1Y3M swap differential suggests fair value is around -65bp versus the 10-year differential’s current level of around -85bp.

- The last time the divergence from fair value was this large was in mid-March. At that time, the AU-NZ 10-year yield differential reached a concerning -100bp, marking its lowest level since the late 1990s. This sharp decline was triggered by a disappointing deterioration in NZ's current account deficit, which caught the attention of S&P bond ratings, leading to consequential comments from them.

- The current negative regression error could be in part due to speculation that the September 12 release of the NZ Pre-Election Economic and Fiscal Update (PREFU) may highlight a material fiscal deterioration.

Figure 1: AU/NZ Regression Error - 10-Year Yield Differential Vs. 1Y3M Swap Differential

Source: MNI – Market News / Bloomberg

FOREX: AUD Outperforming In Asia

The AUD is the strongest performer in the G-10 space at the margins on Monday, benefitting from the improving risk sentiment in Chinese and Hong Kong equities after China Securities Regulatory Commission cut the levy charged on stock trades from 0.1% to 0.05%. It is the first time the levy has been cut since April 2008.

- AUD/USD is up ~0.4%, marginally paring gains of as much as 0.6% as the Hang Seng retreated from session highs. Despite today's price action technically the outlook for Aussie is bearish, support comes in at $0.6535 (low from Aug 17) and resistance is at $0.6488 (high from 24 Aug).

- Kiwi is a touch firmer, NZD/USD has dealt in a narrow range consolidating above the $0.59 handle.

- Yen was marginally pressured as US Tsy Yields firmed in early trade before paring losses to sit little changed from opening levels. USD/JPY remains in an uptrend, resistance is at ¥146.63 (high from Aug 25 and bull trigger) and ¥146.93 (8 Nov 22 high). Support comes in at ¥144.39 (20-Day EMA).

- Elsewhere in G-10 GBP and EUR are both ~0.1% firmer reflecting the broader USD move.

- Cross asset wise; the Hang Seng is up ~2% having been up as much as ~3% in early trade. US Tsy Yields are little changed across the curve. BBDXY is down ~0.1%.

- There is a thin docket on Monday, UK markets are closed due to the observance of a national holiday and wider liquidity will be affected.

EQUITIES: China Shares Surge On Policy Support, But We Sit Away From Best Levels

Regional equities are higher, with much of the focus on China and associated markets, following weekend announcements designed to support equity market sentiment. US equity futures opened higher, but there was little follow to earlier positive moves. Eminis sit back at 4417, still reasonably close to Friday highs, while Nasdaq futures were last near 14984, also just in positive territory.

- To recap, China announced yesterday it would cut the stock trading levy to 0.05% from 0.1%. The first such cut since 2008. Not surprisingly, onshore brokerages have done well. Other market supports were announced in the form of limiting IPOs, while 17 new ETF products were approved at the end of last week, which is reportedly a rare move in terms of so many being approved at once.

- The CSI 300 opened more than 5% higher, but sits back at +2.3% at the break. In index terms we got above 3900 in the first part of trade but sit back under 3800 now.

- The HSI is +1.7% higher at the break, but like mainland shares,are comfortably away from opening highs.

- Elsewhere, Japan shares are higher, with gains of 1.3% for the Topix and 1.6% for the Nikkei 225 at this stage. For the Kospi and Taiex, gains are well under 1% at this stage. Offshore inflows into local shares have been fairly modest for South Korea at this stage, +$26.3mn.

- In SEA, gains are also more modest, while Malaysia shares are down slightly. Singapore's Strait Times outperforming, with a 1% rally.

OIL: WTI Trading Below $80 But Holding Onto Friday’s Gains

Oil prices are down slightly today during APAC trading and have been moving sideways since the trough earlier. They have been range trading as supply and demand issues balance out. The USD index is down 0.1%.

- WTI is around $79.78/bbl after the intraday low of $79.70. It traded above $80 earlier in the session reaching a high of $80.42. Brent is trading around $84.39 after a low of $84.30. It made a high of $84.98 earlier.

- Crude hasn’t been boosted by measures in China to support its property sector and equities. China is the world’s largest oil importer.

- A tightening market due to OPEC output cuts is likely to provide support to prices through H2 2023 but there could be increased supply from Iran, Venezuela and Iraqi Kurdistan as talks in all three continue. The market remains worried about demand from China and further rate hikes in the US.

- Later the Fed’s Barr speaks and the Dallas Fed index is released. Also Bundesbank President Nagel is due to speak.

GOLD: Steady After Jackson Hole

Gold is unchanged in the Asia-Pac session, after closing 0.1% lower on Friday. Friday’s steady performance, following a weekly advance, comes after global central bankers updated policy guidance at the Jackson Hole Symposium. Fed Chair Powell's speech was deemed balanced with few surprises. “We are prepared to raise rates further if appropriate and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective,” Powell said.

- Meanwhile, ECB President Christine Lagarde vowed to set borrowing costs as high as needed and leave them there until inflation is back to its goal.

- In contrast, BoJ Governor Ueda said price growth remained slower than the central bank’s goal, explaining why officials are continuing with their current monetary policy strategy. “We think underlying inflation is still a bit below our target of 2%,” Ueda said. “This is why we are sticking with our current monetary easing framework.”

- Notwithstanding last week’s gain, the trend outlook remains bearish with support at $1897.7 (Aug 23 low), according to MNI's technicals team. With the breach of resistance at the 20-day EMA last week, resistance is raised to $1931.4 (50-day EMA).

GLOBAL: Asia & Euro Area See Weak Export Volumes

CPB data showed global export volume growth remained weak in June in both developed and emerging nations, especially in Asia. Advanced economies’ export growth rose 0.2% m/m to be down 0.6% y/y an improvement from -1.6% and outpacing EM which fell 1% m/m to be down 2.6% y/y after -0.5% y/y. Annual export growth contracted across Asia, except Japan which returned to positive territory, but generally saw some improvement.

- Export volumes from Japan grew 1.1% y/y in June after falling 3.5%, whereas advanced Asia ex Japan fell 3.8% y/y but improved from May’s -6.4%.

- China’s exports fell 1.3% y/y after falling 5.1%, while emerging Asia ex China saw shipments worsen to -8.4% y/y from +0.2% in May.

- The euro area was another weak spot in June with volumes falling 1.7% y/y after -1.8%. The UK on the other hand saw growth of 4.9% y/y. The US continued its run of positive outcomes since April 2022 with exports growing 2.9% y/y in June.

Source: MNI - Market News/Refinitiv/CPB

ASIA FX: USD/CNH Can't Sustain Downside Break Of 7.2700

Much of today's focus has been on China-related asset sentiment, with USD/CNH lower in early trade, but unable to sustain a break sub 7.2700, as equity momentum cooled. Most other pairs have seen relatively tight ranges and sit above session lows, in line with the USD/CNH rebound. THB and MYR have underperformed at the margins. Still to come is the Taiwan monitoring indicator, while tomorrow the regional data calendar is quiet.

- From earlier lows, USD/CNH has recovered back towards opening levels, last tracking close to 7.2890. This puts us only ~0.10% sub NY closing levels from Friday. Earlier lows were just under 7.2700, with the pair unable to break to fresh downside levels (as this level coincides with lows from last week). Equity sentiment looks more positive, albeit comfortably off earlier highs. The CSI 300 tracking around +1.75% firmer (we were above 5% not long after the open). To recap, China announced yesterday it would cut the stock trading levy to 0.05% from 0.1%. The first such cut since 2008. Not surprisingly, onshore brokerages have done well. Other market supports were announced in the form of limiting IPOs, while 17 new ETF products were approved at the end of last week.

- USD/TWD has tracked within recent ranges during today's session, the pair last around 31.835. Recent lows rest at ~31.74, while highs from mid August near 32.00 haven't been threatened. It's a similar backdrop for the 1 month NDF, which last sits close to 31.74.• Local equities are doing better today, but only at the margin (+0.25%), after last Friday's -1.72% correction, which also coincided with more than $1bn in offshore outflows. Coming up we have the July monitoring indicator, which is a composite measure of important variables for the economy, the index has been on the improve but from a low base.

- USD/IDR is relatively steady in early trade today, last at 15290, which is down slightly from Friday closing levels. Lows from last Thursday rest near 15240, while recent highs are around the 15360 level. The simple 200-day MA is back closer to 15207. BI plans to offer its new rupiah securities twice per week, Wednesday and Friday. These sales will start on September 15.

- The Ringgit is marginally pressured in early dealing, USD/MYR is up ~0.2% and remains well within recent ranges. Last week the pair consolidated recent gains in a narrow 4.64/66 range, there was little follow through on moves as broader USD trends dominated flows. August S&P Global Mfg PMI on Friday is the only data due this week as the data calendar is light.

- The Rupee is a touch firmer in early dealing this morning, broader USD trends are dominating flows however ranges remain narrow. USD/INR sits at 82.57/58 ~0.1% lower this morning. The pair fell ~0.5% last week, the largest weekly fall since early July. India, the world’s biggest exporter of rice, imposed more curbs on shipments of the grain in a move that’s likely to further squeeze global supplies. On Thursday Q2 GDP crosses an uptick to 7.8% Y/Y from 6.1% is expected. S&P Global Mfg PMI for August rounds off the docket on Friday.

- The SGD NEER (per Goldman Sachs estimates) is marginally softer in early dealing and has ticked away from its highest level since 3 Aug in recent dealing. The measure is ~0.5% below the top of the band. USD/SGD is a touch lower in early dealing, the pair is ~0.1% and last prints at $1.3550/55. The pair continues to consolidate in narrow ranges above the 20-Day EMA ($1.3511). There is a thin data calendar this week with just July M1 and M2 Money Supply due on Thursday.

- USD/THB is tracking higher in the first part of trade, last at ~35.24, down 0.40% in baht terms versus closing levels from the end of last week. Some of this reflects a resilient USD backdrop since Friday's onshore spot close. All of the key EMAs sit below current USD/THB spot levels, the nearest being the 20-day EMA at 35.01. Near term focus remains on political developments, with new PM Srettha stating the new cabinet is expected to be submitted today. Earlier reports suggested Pheu Thai would keep the key economic ministries, with Srettha potentially the Finance Minister.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/08/2023 | 0800/1000 | ** |  | EU | M3 |

| 28/08/2023 | 1430/1030 | ** |  | US | Dallas Fed manufacturing survey |

| 28/08/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 2 Year Note |

| 28/08/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 28/08/2023 | 1630/1230 | | US | Fed Vice Chair Michael Barr | |

| 28/08/2023 | 1700/1300 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 28/08/2023 | 1700/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

| 29/08/2023 | 2301/0001 | * |  | UK | BRC Monthly Shop Price Index |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.