Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Gains for U.S. e-mini futures and a firmer commodity complex buoyed high-beta currencies in the Asia-Pac session, with the Antipodeans pacing gains. Hawkish RBNZ repricing continued after the release of New Zealand's strong consumer inflation data on Tuesday, with little in the way of fresh headline catalysts trickling through today. Meeting-dated OIS price ~82bp worth of OCR hikes for the final meeting of 2022, with the 12bp upswing from the opening levels doubling the total post-CPI advance.

- NZGBs extended on Tuesday’s cheapening, with continued payside swap flow noted in the wake of Tuesday’s CPI reading, as hedging for a more hawkish RBNZ dragged swap spreads wider. Fresh cycle highs were registered in both swap rates and NZGB yields across the term structure as a result.

- Inflation data from the UK, Eurozone and Canada take focus from here, alongside U.S. housing starts and building permits. There is plenty of central bank speak coming up from Fed, ECB, BoE and Riksbank officials.

MNI Insight: Upside Risks To Australian Inflation, But Will It Be Enough To Shift RBA Expectations?

Executive Summary:

- Yesterday’s NZ inflation came in higher than expected across the main components driven by housing, utilities, food, and transport. Non-tradeables inflation was also its highest since the series began in 2000. Correlations between NZ and Australia CPI measures are high at the moment, across both headline and core measures. Whilst correlation doesn’t imply causation, given Australia has been experiencing similar cost pressures to NZ, the risks point to a strong Q3 Australian CPI result too, which prints next Wednesday.

- Whether or not this can shift RBA market expectations remains to be seen though. The RBA is already forecasting strong inflation outcomes into year end. Presumably next week’s result will need to be strong enough for that outlook, coupled with easing momentum forecast into the middle of next year, to be under threat.

- Current market pricing has roughly 25bps priced at each of the next three meetings, with ~145bp of cumulative tightening priced through to the end of the current cycle (based on futures). The RBNZ has been well ahead of the RBA in this tightening cycle though and current market pricing expects that to remain the case.

- For the full piece, see here:AU and NZ CPI (Oct 19) final.pdf

US TSYS: Block Sales Apply Light Pressure In Asia

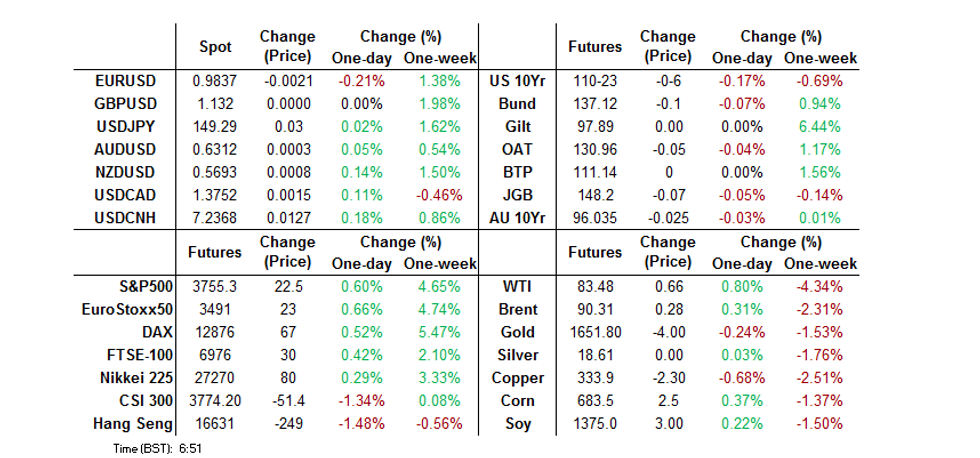

Tsys have cheapened at the margin overnight, with the now familiar TY block sales (-1.7K & -2.0K) once again evident in Asia-Pac hours, helping the space lower.

- TYZ2 deals -0-06 at 110-23, 0-01 off the base of a tight 0-07 range, on limited volume of ~54K.

- Meanwhile, cash Tsys run 1-2bp cheaper across the curve, bear flattening.

- Minneapolis Fed President Kashkari (’23 voter) underscored the need for continued tightening during the NY-Asia crossover, as he suggested that there would be no pause in tightening until there is compelling evidence that core inflation has peaked.

- The first notable risk event of Wednesday trade comes in the form of UK CPI data.

- Further out, housing starts and building permits data headline the NY data docket, with Fedspeak from Bullard, Evans & Kashkari, as well as the release of the Fed’s Beige Book, also due. On the supply side, we will see the latest 20-Year Tsy auction.

JGBS: Bear Steepening Flips To Bear Flattening

JGBs came under some cheapening pressure as the Tokyo morning session wore on, with the curve steepening. 40-Year yields registered a fresh cycle high, with 20- & 30-Year yields printing a touch shy of their respective cycle peaks, with the recent run of pressure maintained.

- That was before a pull away from cheapest levels of the session in the super-long end, with the respective outright levels and steepness vs. 10s (which are capped by the BoJ’s YCC mechanism) perhaps luring domestic life insurers and pension funds in.

- Cash JGBs run little changed to ~1.5bp cheaper, with the front end now leading the cheapening, as the curve bear flattens.

- JGB futures last -7, sticking to a very narrow range.

- Local headline flow has been focused on FX matters, once again, with Finance Minister Suzuki highlighting the increased frequency of the monitoring of FX markets.

- BoJ board member Adachi stuck to the BoJ’s central script, playing down any suggestions that the Bank should tighten monetary policy, while providing familiar overtures re: the JPY. Elsewhere, BoJ Governor Kuroda failed to provide fresh, meaningful information.

- Looking ahead, the monthly trade balance reading and weekly international security flow data from the Japanese MoF headline the domestic docket on Thursday.

AUSSIE BONDS: Cheaper On Global Moves, Labour Market Report Eyed

Spill over from the wider core global FI space (a downtick in U.S. Tsys and a heavier move in NZGBs) applied modest pressure to the ACGB space on Wednesday, although Sydney trade was relatively narrow, with the major bond futures contracts sticking within their respective overnight ranges.

- YM prints -4.0 ahead of the bell, with XM -2.5, while wider cash ACGB trade sees 2-6bp of cheapening, as the curve bear flattens

- EFPs are a little wider on the day, with the 3-/10-Year box steepening.

- Bills sit 7-10bp cheaper through the reds, with RBA dated OIS pointing to a terminal rate of just under ~4.10%, 10bp or so higher on the day, but comfortably within the recently observed range.

- ACGB Apr-29 supply was easily digested, while SAFA conducted a A$750mn tap of its May-30 select line.

- It is worth remembering that 21 October represents the joint largest round of ACGB coupon payments of the year (A$4.87bn), with eyes on the potential for coupon cash deployments over the next few sessions of a result.

- Looking ahead, Thursday’s domestic docket is headlined by the release of the monthly labour market report.

NZGBS: Continued Hedging For A More Hawkish RBNZ Weighs

NZGBs extended on Tuesday’s cheapening, with continued payside swap flow noted in the wake of Tuesday’s CPI reading, as hedging for a more hawkish RBNZ dragged swap spreads wider. Fresh cycle highs were registered in both swap rates and NZGB yields across the term structure as a result.

- NZGBs finished the session 8-12bp cheaper, bear flattening.

- RBNZ dated OIS now prices a peak OCR of just over 5.40%, with ~78bp of tightening priced in for next month’s meeting (some are pointing to the 3-month RBNZ meeting hiatus that follows that meeting as another source of uncertainty re: monetary policy, given the firmer than expected inflation prints).

- Looking ahead, Thursday’s domestic docket is headlined by the weekly round of NZGB issuance, with May-28, Apr-33 and May-51 paper set to come to market.

FOREX: Further Hawkish RBNZ Repricing Aids Kiwi, Japanese FinMin Vows To Boost Market Monitoring

Gains for U.S. e-mini futures and a firmer commodity complex buoyed high-beta currencies in the Asia-Pac session, with the Antipodeans pacing gains. Hawkish RBNZ repricing continued after the release of New Zealand's strong consumer inflation data on Tuesday, with little in the way of fresh headline catalysts trickling through today. Meeting-dated OIS price ~82bp worth of OCR hikes for the final meeting of 2022, with the 12bp upswing from the opening levels doubling the total post-CPI advance.

- AUD/NZD traded on a heavier footing but struggled to test yesterday's lows, as a move higher in the BBG Commodity Index lent support to the Aussie dollar. Relative interest rate dynamics remained skewed in favour of the kiwi, as Australia/New Zealand 2-year swap spread refreshed multi-month lows.

- Yen watchers were on alert for signs of an FX intervention by Japanese officials, after a sudden bout of purchases resulted in a sudden 110-pips downswing in USD/JPY on Tuesday, inspiring speculation on potential stealth action. Officials resumed jawboning, with FinMin Suzuki pledging to increase the frequency of detailed checks on market moves.

- The Asia-Pac section of G10 FX basket generally outperformed European peers, albeit sterling traded on a firmer footing. The BBDXY index ground higher alongside cash U.S. Tsy yields.

- Inflation data from the UK, Eurozone and Canada take focus from here, alongside U.S. housing starts and building permits. There is plenty of central bank speak coming up from Fed, ECB, BoE and Riksbank officials.

FX OPTIONS: Expiries for Oct19 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9750(E1.3bln), $0.9785-00(E549mln), $0.9940-50(E518mln)

- USD/JPY: Y148.00($1.0bln), Y149.25-40($876mln)

- EUR/GBP: Gbp0.8645-50(E520mln)

- USD/CAD: C$1.3800($696mln)

ASIA FX: USD/Asia Dips Supported

USD/Asia pairs have been mixed for the most part, failing to benefit a great deal from the positive equity lead seen. Dips in USD/CNH remain firmly supported, the pair last above 7.2300. The won has outperformed but is away from earlier highs. Other moves have been more modest, although the dollar has been supported against INR and IDR. Tomorrow the focus will be on China LPR outcomes (if they print), with no change expected, along with the BI decision.

- USD/CNH dips sub 7.2200 were supported, and the pair is now testing overnight highs around 7.2330/40. No change is expected in the LPR rates tomorrow, although they may not print. China equities continue to lag, although some property names have performed better today on planned state backed bond issuance. CNH has underperformed some majors, but is moving in line with the EUR.

- USD/KRW got to a low sub 1415 in the 1 month NDF, but we are now back to above 1420. Equity sentiment has been volatile today, with the Kospi last sitting flat. Still the won is around 0.30% stronger since the NY close, outperforming others in the region.

- USD/INR is just above 82.35, seeing USD demand yesterday ahead of the 82.00 level. Watch for intervention above 82.40, although such flows are reportedly taking place more in the forward area, as the authorities are mindful of running down spot FX reserves.

- Spot USD/IDR trades +16 figs at 15,483, with bulls looking for gains past the 61.8% retracement of the 2020 sell-off/Apr 23, 2020 high of 15,574/15,598. Bank Indonesia will announce its monetary policy decision tomorrow (our usual preview is forthcoming). Bank Indonesia Gov Warjiyo this morning reaffirmed the target for inflation to return to the target range in 3Q2023, while noting that the central bank will continue to intervene in the market to stabilise the rupiah.

- Spot USD/PHP operates within touching distance from the 59.00 all-time high, even as President Marcos and his administration stepped up their verbal interventions surrounding peso depreciation. We were last at 58.915. We may have to defend the peso in the coming months," Marcos tweeted on Tuesday. He added that "number one priority is still inflation" and officials "will continue to use interest rates to mitigate the effects."

EQUITIES: Positive Property News Can't Curb Broader Losses For HK/China Shares

China and Hong Kong stock indices are lower, bucking the positive trend seen for most other Asia Pac equities. US futures are higher, buoyed by late earnings new from the US session, notably from Netflix. We are away from best levels though, Eminis peaked close to 3775, but we are now back under 3765. Nasdaq futures have outperformed.

- The HSI is still around 1% lower, as HK Chief Executive Lee speaks during the policy address. Stamp duty for foreigners will be refunded after they stay for 7-yrs. It will also start a scheme to attract high salary earners and top graduates, with visas of 2yrs. The HKEX will also revise listing rules next year to help fund raising for advanced tech companies and SMEs.

- The HSI tech index is still down around 2.5%, but the property sub-index is up nearly 0.9%.

- China stocks are lower, with the CSI 300 off by close to 0.90%, the Shanghai composite is -0.50%, although the property sub-index is close to flat. A number of China property developers are planning to raise funds through state back bond sales, which has helped sentiment at the margin.

- The Nikkei 225 is up around 0.60% at this stage, in in with US tech futures' gains. The Taeix has struggled, down by close to -0.50%, as TSMC has dipped around 2%., The Kospi is in positive territory but only just (last at +0.1%).

- The rest region is positive, although gains are generally below 0.50%.

GOLD: Range Bound, Awaiting Fresh Catalysts

Gold is down from earlier session highs, although ranges remain tight overall. The precious metal last sat just above $1650, versus earlier highs close to $1655.

- We are still respecting ranges from the overnight session, with gold waiting for a fresh catalyst to dictate new direction.

- As we noted yesterday, the technical set up still looks to be a bearish one, but we haven't made fresh lows this week, with moves towards $1645 still supported at this stage.

- Cross asset signals are mixed today. Higher beta FX is a touch stronger, but not breaking out of recent ranges. The majors though have been very quiet.

- US yields are slightly higher across the curve, 1-2bps. However, US real yields remained quite steady in the 10yr overnight (closing at 1.60%).

OIL: Supply Worries Put A Floor Under Prices

Oil markets were up moderately today after falling overnight. WTI rose around 1% to $83.74 but remains below its key moving averages. Brent has stayed above $90 and is up 0.6%.

- Global growth concerns continue to weigh on oil prices but markets were also focused on supply issues, which have currently put a floor in the market.

- There was concern that the European Union’s latest sanctions against Russia would tighten the market despite the US’ expected release of up to $15mn barrels from the Strategic Petroleum Reserve (SPR). An announcement on this is expected in the US today. There could be further supplies from the SPR going forward for the winter.

- There has also been a delay to the full reopening of the Kashagan oil field in Kazakhstan. They are one of the largest alternatives to Russia for Europeans.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 19/10/2022 | 0600/0700 | *** |  | UK | Consumer inflation report |

| 19/10/2022 | 0600/0700 | *** | | UK | Producer Prices |

| 19/10/2022 | 0830/0930 | * | | UK | ONS House Price Index |

| 19/10/2022 | 0900/1100 | *** |  | EU | HICP (f) |

| 19/10/2022 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 19/10/2022 | 0900/1100 | ** | | EU | Construction Production |

| 19/10/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 19/10/2022 | 1230/0830 | *** |  | CA | CPI |

| 19/10/2022 | 1230/0830 | * | | CA | Industrial Product and Raw Material Price Index |

| 19/10/2022 | 1230/0830 | *** | | US | Housing Starts |

| 19/10/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 19/10/2022 | 1500/1600 | | UK | BOE Mann Panels Webinar on ERM Crisis | |

| 19/10/2022 | 1700/1300 | | US | Minneapolis Fed's Neel Kashkari | |

| 19/10/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 19/10/2022 | 1800/1400 | | US | Fed Beige Book | |

| 19/10/2022 | 2230/1830 | | US | St. Louis Fed's James Bullard | |

| 19/10/2022 | 2230/1830 | | US | Chicago Fed's Charles Evans |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.