Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- The early focus was on the Fitch US credit rating downgrade. Regional equities and US futures have traded weaker, while in the FX space, trends have been volatile but safe havens have outperformed higher beta plays. NZD has been the weakest performer, with a tick higher in the Q2 unemployment also weighing.

- US Tsys firmed in early dealing after Fitch downgraded the US to AA+ from AAA. A retreat from session highs was observed, perhaps as the aforementioned Fitch downgrade was based on governance and medium term fiscal challenges but not new fiscal information.

- Elsewhere, BoJ Deputy Governor Shinichi Uchida said that the BoJ is far from an exit or raising its negative interest rate.

- Looking ahead, there is a thin docket in Europe today. Further out ADP Employment provides the highlight.

MARKETS

US TSYS: Curve Marginally Steeper, Pare Post-Fitch Gains

TYU3 deals at 111-01, +0-05, a touch off the base of the 0-07+ range on volume of ~109k.

- Cash tsys sit 1bp richer to 1bp cheaper across the major benchmarks, the curve has twist steepened pivoting on 5s.

- Tsys firmed in early dealing after Fitch downgraded the US to AA+ from AAA. Fitch noted that the rating change reflected an expected fiscal deterioration over the next three years, a high and growing government debt burden and repeated debt limit standoffs.

- A retreat from session highs was observed, perhaps as the aforementioned Fitch downgrade was based on governance and medium term fiscal challenges but not new fiscal information. The move came alongside pressure on regional equities and the USD ticking higher.

- FOMC dated OIS remain stable, a terminal rate of 5.40% is seen in November with ~60bps of cuts by June 2024.

- There is a thin docket in Europe today. Further out ADP Employment provides the highlight.

JGBS: Futures Extend Morning Weakness, BoJ Dep Gov Uchida Comments On YCC

In the Tokyo afternoon session, JGB futures continued to weaken, down by 33 compared to settlement levels. This trend aligns with the results of this morning's BoJ Rinban operations, which showed higher and positive spreads, and generally higher cover ratios.

- In addition to the previously outlined monetary base data and the BoJ Minutes from the June MPM, the key domestic news were comments from BoJ Deputy Governor Shinichi Uchida who said that the BoJ is far from an exit or raising its negative interest rate. “Needless to say, we do not have an exit from monetary easing in mind,” Uchida said in a speech to local business leaders. “In sum, the bank’s decision to conduct yield curve control with greater flexibility aims at patiently continuing with monetary easing.” (See link)

- The cash JGB curve has bear steepened with yield changes from +0.5bp to +2.6bp. The benchmark 10-year yield is +2.4bp at 0.631%, above BoJ's YCC old limit of 0.50% but below its new hard limit of 1.0%.

- Swap rates see an almost uniform 1-2bp shift higher across the curve. Swap spreads are wider out to the 5-year and tighter beyond.

- Tomorrow the local calendar sees International Investment Flow and Jibun Bank Services and Composite PMIs data, along with 10-year Inflation Linked supply.

AUSSIE BONDS: Weaker, XM Near Session Lows, YM Is Mid-range

ACGBs (YM -2.0 & XM -6.0) sit weaker. XMU3 is currently trading close to its Sydney session lows, while YMU3 is in the middle of the trading range. The decline in the 10-year contract from its session highs is a result of US tsys pulling back from their morning highs after Fitch's downgrade of the US to AA+.

- According to MNI’s technicals team, XMU3 backtracked slightly despite the unchanged RBA rate decision yesterday. Nonetheless, the recent recovery is yet to encounter meaningful resistance - first crossing at 96.440. Moving average studies remain in bear mode, highlighting the trend direction. First support sits at the Dec 29 low of 95.670.

- Cash ACGBs are 1-6bp cheaper with the AU-US 10-year yield differential -3bp at flat.

- Expectations of sustained strong pricing at today's auction of the May-34 bond proved accurate, as the weighted average yield printed 1.0bp through prevailing mids. However, the cover ratio moved lower.

- Swap rates are 1bp lower to 5bp higher with the 3s10s curve twist steepening.

- The bills strip is richer with pricing +1 to +2.

- RBA-dated OIS pricing is 1-3bp softer across meetings.

- Tomorrow the local calendar sees Q2 Retail Sales Ex-Inflation and Trade Balance data. With nominal sales +0.4% q/q and prices +1.0%, the market is expecting -0.6% q/q.

RBA: MNI RBA Review - August 2023: Holding Onto Employment Gains

- The RBA left rates at 4.1% at its August meeting but retained its tightening bias, in line with our expectations. Its reasons for pausing for a second consecutive month were unchanged from July. Importantly it appears that the RBA’s forecasts are broadly unchanged from May.

- While “some further tightening of monetary policy may be required” it will now depend upon the “data and the evolving assessment of risks”, thus RBA decisions have become even more data dependent and contingent on risks to its forecasts.

- Whether rates peak at 4.1% or higher seems as though it is going to depend on whether firms still have enough pricing power to pass higher costs onto customers. Currently it is unclear whether this is the case. All meetings will be highly data dependent but November looks most likely for a hike – depending on Q3 CPI.

- See full review here.

NZGBS: Cash Curve Twist Steepens, Wages Growth Peaked But Remain Elevated

The 2-year NZGBs benchmark ended on a positive note, with its yield 1bp lower. The 10-year benchmark is however at session cheaps (3bp cheaper). Longer-dated NZGBs faced pressure due to the reversal of ACGBs' post-RBA rally and a retreat in US Tsys from the morning’s highs following Fitch's downgrade of the US to AA+.

- The 2s10s swap curve twist steepens with rates 3bp lower to 3bp higher.

- RBNZ dated OIS pricing closed 1-5bp softer across meetings, with mid’24 leading.

- The NZ Treasury in coordination with modelling from the RBNZ has decided to give the central bank more capital and an indemnity to allow it to increase its capacity for FX intervention if needed. See the report here.

- Private sector wages rose 1.1% q/q and 4.3% y/y with the public sector lower at 0.6% and 4.2%, which is driven by collective agreements. Significant moderation in wage growth is still needed before the RBNZ eases.

- Tomorrow the local calendar sees ANZ Commodity Prices. All main commodity prices remain under downward pressure.

- In Australia, Q2 Retail Sales Ex-Inflation data is due.

- Tomorrow the NZ Treasury announced that they plan to sell NZ$250mn of the 0.25% May-28 bond, NZ$175mn of the 4.25% May-34 bond and NZ$75mn of the 2.75% May-51 bond.

New Zealand: Jobs Growth Strong, RBNZ Unlikely To Ease Soon

While the Q2 unemployment rate rose more than expected to 3.6% from 3.4%, the labour market was actually stronger than expected. Employment grew 1% q/q to be up 4% y/y after 0.8% and 2.5% in Q1 with the participation rate rising 0.4pp to 72.4%, a new high since 1986. The data show that the NZ economy continues to provide jobs despite slower growth but is unlikely to be enough to prompt another RBNZ hike but also means a cut is some way off.

- Working-age population rose 0.7% q/q to be up 2.2% y/y and while many found jobs, with the strongest annual employment growth since Q3 2017, unemployment still rose. The employment rate increased to a series high of 69.8%. The number of unemployed was 5.8% q/q higher and 13.5% y/y, highest since Q4 2020. While vacancies are down the ratio with unemployment is still elevated.

- Underutilisation also rose to 9.8% from 9.1%, which is still historically low, driven by underemployed part-time workers. Part-time employment growth was stronger than full-time at 2.9% q/q and 9.9% y/y compared with 0.5% and 2.6%.

- Hours worked rose 0.3% q/q to be up 3.1% y/y after 3.8% in Q1.

- Stats NZ noted that tourism-related employment returned to its pre-Covid level and even though it is around 9.5% of total employment, it accounted for about a quarter of Q2 annual employment growth.

Source: MNI - Market News/Refinitiv

NEW ZEALAND: Wage Growth Peaked But Remains Elevated

Wage growth has peaked in NZ with the total salary & wages (labour cost index) steady at 4.3% y/y in Q2 with the main drivers inflation, market matching and retaining/attracting staff. Private sector rose 1.1% q/q and 4.3% y/y with the public sector lower at 0.6% and 4.2%, which is driven by collective agreements. Given that the minimum wage rose 7.1% on April 1, the increase in the labour cost index remained contained and well below inflation. Average hourly ordinary time earnings ex overtime remained elevated but eased to 6.9% y/y from 7.6%, which was the peak, with the private sector down to 7.7% from 8.2%. Significant moderation in wage growth still needed before the RBNZ eases.

NZ Wages y/y%

Source: MNI - Market News/Refinitiv

FOREX: Kiwi Pressured In Asia, Fitch Downgrades US

The NZD is the weakest performer in the G-10 space at the margins on Wednesday, New Zealand's Unemployment Rate ticked higher in Q2 and wages growth slowed. Early in the session Fitch downgraded the US from AAA to AA+, the downgrade echoes a similar move made by S&P in 2011.

- NZD/USD has been pressured through today's Asian session. The pair sits at $0.6105/10, down ~0.7% today. Bears now target low from Jun 28 ($0.6051) and year to date lows ($0.5985).

- AUD/USD sits at key support of $0.6596, the low from Jun 29. Weaker regional equities weighed on risk sentiment through the session seeing AUD print its lowest level since early June before marginally paring losses.

- Yen unwound early gains, USD/JPY was ~0.3% lower after the Fitch downgrade was announced before paring losses to sit at ¥143.10/20. Support comes in at ¥140.89 (50-Day EMA), resistance is at yesterday's high ¥143.47.

- Elsewhere in G-10 EUR and CHF have ticked away from session highs and both now sit little changed from opening levels.

- Cross asset wise; Hang Seng is down ~2%, e-minis are ~0.5% softer and BBDXY sits up ~0.1% having been down ~0.2% early in the session post the Fitch downgrade news.

- There is a thin docket today, ADP Employment highlights an otherwise light data calendar.

EQUITIES: Weakness Across The Board, US Futures Weaker Post Fitch Downgrade

Regional equities are down across the board today. We had the weaker lead from EU/US markets on Tuesday, followed by the earlier news today of the Fitch downgrade for the US credit rating. US equity futures gapped lower when they re-opened and while we are away from worst levels, we remain comfortably in the red. Eminis were last around 4580, -0.47% lower, while Nasdaq futures were off by -0.58%.

- The reaction in US government bond markets has been fairly muted, with yields higher versus earlier lows, suggesting little safe haven bid in this part of the market post the ratings news. Hence weaker equity sentiment may reflect other factors, such as the continued climb higher in real yields (10yr now up to 1.68% in Tuesday trade).

- China related markets are lower. The HSI off by 2% at the break, with tech weaker. The Golden Dragon index did fall by 2% in US trade on Tuesday. The HSTECH index is off by 2.56%.

- Further talk of property stimulus, with the PBoC reportedly set guide mortgage rates lower for existing loans not enough to drive better sentiment. On the mainland, the CSI 300 is off -0.70% at the break, while the Shanghai Composite is down by 0.84%. The CSI 300 real estate sub index is down from early session highs.

- The Kospi and Taiex are both down by around 1.70% at this stage. The Kosdaq falling 2.8%. The Nikkei 225 is down around 2%.

- In SEA, the Philippines bourse is the worst performer, down over 1.5%. Other indices are tracking lower, but losses are less than 1% at this stage.

OIL: Crude Rises Further As US Sees Large Stock Draw, EIA Data Later

Oil is higher again during the APAC session rising around 0.9% supported by the large drawdown in US inventories. The market rallied over July on signs that supply is tightening. WTI is holding above $82 at $82.14/bbl after a high of $82.40. Brent is $85.67, around its intraday low of $85.61. It reached a high of $85.99 earlier facing resistance at $86. $86.18 is the level to watch. The USD started the day lower following Fitch’s US downgrade but the index is now slightly higher.

- Bloomberg reported that API US crude inventories fell 15.4mn barrels with the key storage hub Cushing down 1.76mn, gasoline -1.68mn and distillate -512k, according to sources familiar with the data. The official EIA data print later today and if the crude draw is confirmed, it would be the largest stock decline since 1982.

- WTI futures contracts are in the widest backwardation since November, adding to sentiment that supply is tightening.

- There is only July ADP employment later in the US and Spanish unemployment in the euro area. The focus for crude is Friday’s US July payrolls.

GOLD: Firmer After Fitch Downgrades US Sovereign Credit Rating

Gold is up by 0.2% in the Asia-Pac session following Fitch Ratings' decision to downgrade the US sovereign credit rating. This move comes after the precious metal experienced a 1% decline on Tuesday due to the strength of the USD and higher US Treasury yields. The USD Index rose above the 100-day moving average for the first time since late June.

- The USD and US tsys looked through weaker than forecast US data; JOLTS Job Openings, ISM Mfg and Prices Paid all printing below expectations. There were no substantive headline drivers for the post-data reversal in rates, however. It appeared algos reacted too strongly to the data with prop and fast money selling into the move.

- Focus turns to ADP private employment data today (+188k est vs. 497k prior), and Non-Farm Payrolls on Friday (+200k job gains vs. +209k prior).

- Bullion briefly crossed support at $1942.7, last Thursday’s low. According to MNI’s technicals team, a sustained break opens the lowest levels in close to a month as well as the 50% retracement of the up leg off the June low at $1940.3.

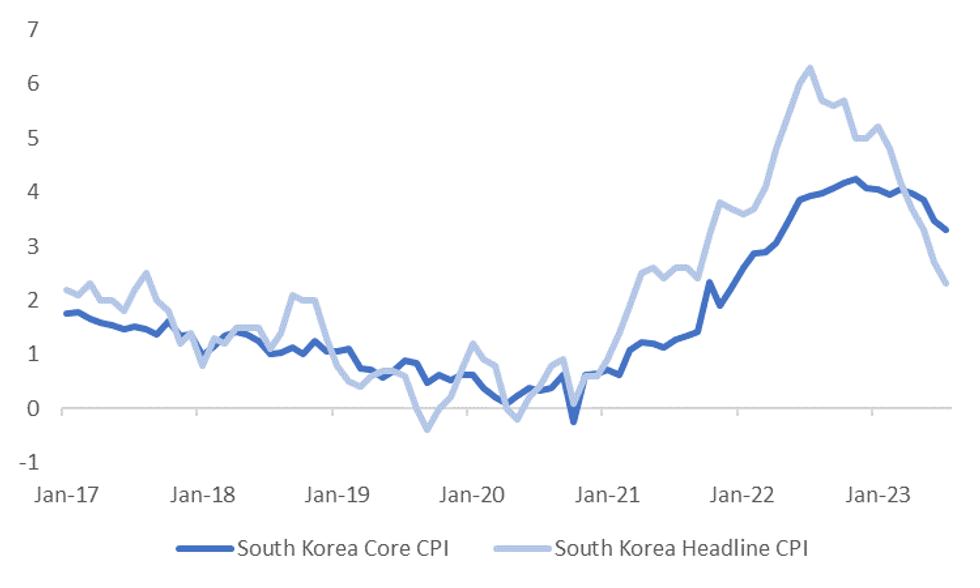

SOUTH KOREA: July CPI Weaker Than Forecast, But Base Effects Less Favorable For Headline In H2 2023

South Korea July CPI was weaker than expected, albeit at the margins. The headline was +0.1% m/m, versus +0.2% forecast, the prior outcome was flat. in y/y terms, we came in at 2.3%, against a 2.4% forecast and 2.7% prior. The core came in at 3.3% y/y, versus 3.5% prior. There is no consensus for this outcome.

- Headline CPI y/y momentum continues to retreat, we are now back to levels that prevailed in the first half of 2021. The authorities are also likely to be pleased with the continued move down in core CPI y/y momentum, see the chart below.

- Still, base effects become less favorable as we progress forward, with the y/y headline pace peaking in July last year. The BoK has stated headline inflation momentum may pick up in August. So, today's result may not shift their thinking around the policy outlook. The core measure didn't peak until November last year though.

- Looking at the detail, weaker housing/utilities (-1.3% m/m) offset a rebound in food prices (+0.8% m/m). Transport prices also edged higher (+0.4% m/m), as did restaurants/hotels (+0.5% m/m). 7 out of the 12 sub-indices for inflation recorded higher m/m outcomes relative to June.

Fig 1: South Korea Inflation - Headline & Core Y/Y

Source: MNI - Market News/Bloomberg

ASIA: ASEAN PMI Points To Slowing Industrial Growth

Manufacturing output in the ASEAN region continued to grow in July but at a slightly slower rate with the S&P Global manufacturing PMI easing to 50.8 from 51, stronger than globally at 48.7. It has been above 50 for almost two years. Most countries in the region are seeing industrial output expand with Indonesia leading. Production and orders growth slowed, with exports shrinking at their fastest in 4 months, driving a slight reduction in employment. With higher costs and lower orders, business confidence deteriorated to its lowest in three years.

- Thailand’s manufacturing PMI eased to 50.7 from 53.2, lowest since June 2022, driven by shrinking new orders leading to job losses and inventory drawdown. Output growth moderated to its slowest since December 2021. Foreign orders rose but at a slower rate while lacklustre economic conditions saw a decline in domestic demand. Input cost pressures fell for the first time since September 2020 with output prices rising at the slowest rate in almost two years. Businesses were less optimistic regarding the outlook with it falling to an 18 month low due to political and economic uncertainty.

Source: MNI - Market News/Bloomberg

ASIA FX: USD/Asia Pairs Higher On Equity Weakness

USD/Asia pairs are higher today, albeit to varying degrees. Plays sensitive to broader equity trends like KRW and IDR have underperformed. SGD has outperformed though, while USD/CNH has seen resistance ahead of 7.2000. Still to come today is the BoT decision, with +25bps expected. Tomorrow the China Caixin services PMI is on tap. The services PMI is also out for India.

- USD/CNH sits slightly below session highs, last near 7.1900. Earlier highs were just above 7.1980. The weaker tone to equities has weighed, with HK shares off over 2%, the CSI 300 down 0.80%. These moves come despite further stimulus measures, with PBoC reportedly set to guide existing mortgage rates lower. There may be some resistance to a fresh break above 7.2000. Note earlier lows came in at 7.1735.

- 1 month USD/KRW is touch below session highs, the pair last in the 1292/93 region. Earlier highs were near 1294.50. Local equities have sunk, with broad base losses in the region today and US futures lower. Earlier July CPI data came in weaker than expected, but may not shift the BoK narrative as base effects are less favorable as we progress through H2.

- After making fresh lows around 7.7925 yesterday, USD/HKD has drifted a little higher in dealings today. The pair last near 7.7980, a little under +0.10% firmer for the session to date. This is in line with broader USD gains, with both USD/CNH and USD/CNY climbing today. The pair remains below all key EMAs at this stage. The nearest being the 20-day, which comes in just above the 7.8100 level. The 200-day sits above 7.8300. In the past month though spot has generally tracked sub all key EMAs.

- Spot USD/IDR is up a further 0.40% so far today, last at 15180. We aren't too far away from July highs near 15220, which also coincides with the simple 200-day MA. Broader USD gains, coupled with fresh risk aversion in the equity space is likely weighing on the rupiah. The near term focus will be on whether the authorities intervene if we breach the 15200 handle or the 200-day MA region. Note the 1 month NDF has already above the 15200 level.

- The Ringgit sits ~0.5% softer in early dealing on Wednesday, broader USD trends are dominating with the greenback reversing early losses after Fitch downgraded the US to AA+. USD/MYR sits at 4.5400/30, the pair remains well within recent ranges after finding support at the 200-Day EMA (4.5021) on Friday. Looking ahead the domestic data docket is empty for the remainder of the week.

- The SGD NEER (per Goldman Sachs estimates) is a touch firmer in early dealing, the measure is holding near cycle highs and sits ~0.4% below the top of the band. USD/SGD firmed above its 20-Day EMA ($1.3335) on Tuesday as broader greenback trends saw the pair rise ~0.5%. The pair printed its highest level since 12 July before marginally paring gains. The pair is dealing in a narrow range on Wednesday morning and last prints at $1.3360/70. Singapore's rental price growth slowed in the second quarter, a gauge of private residential prices rose 2.8% Q/Q the smallest gain since 2021. On the wires today we have the July Purchasing Managers Index and Electronics Sector Index. There is no estimate for either print.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 02/08/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 02/08/2023 | 1215/0815 | *** | | US | ADP Employment Report |

| 02/08/2023 | 1230/0830 | ** | | US | Treasury Quarterly Refunding |

| 02/08/2023 | 1400/1000 | ** | | US | housing vacancies |

| 02/08/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 03/08/2023 | 2300/0900 | * |  | AU | IHS Markit Final Australia Services PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.