Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Firm pricing at the latest round of 40-Year JGB supply promoted twist flattening of the JGB curve.

- Regional Asia-Pac equity markets are mostly higher, following the positive lead from EU/U.S. markets during Monday's session.

- Comments from the Fed, ECB & BoE, as well as lower tier U.S. data headline the broader docket on Tuesday.

MACRO: World Bank Warns Growth Reforms Needed, Global IP Weakens

The World Bank continues to expect 2023 global growth to slow to 1.7% but in a new report it warns that long-term growth could fall to a 2.2% average over 2022-2030, a three-decade low, and emerging markets to 4% from 6% 2000-2010. The World Bank recommends reforms that boost investment in capital and people, working hours and technology use that increases productivity. January CPB global data show that trade and growth trends remained weak at the start of 2023.

- World Bank chief economist Gill said “A lost decade could be in the making for the global economy. The ongoing decline in potential growth has serious implications for the world’s ability to tackle the expanding array of challenges unique to our times. Co-author Ohnsorge noted “Recessions tend to lower potential growth. Systemic banking crises do greater immediate harm than recessions, but their impact tends to ease over time.”See “Falling Long-Term Growth Prospects: Trends, Expectations, and Policies here.

- CPB’s global trade fell 0.1% m/m in January but exports rose 0.8% after slumping 3.3%. But 3-month annualised export momentum deteriorated to -10.5%, which signals further softening. The weakness continues to be in emerging market exports which have negative momentum and are still down 4.1% y/y with China only stabilising at -10.9%.

- Global IP was flat on the month to be down 1.1% y/y and 3-month momentum deteriorated to -3.9%. But the global PMI rose in January and February, and the Baltic Freight index has stabilised, which suggest that output growth may be close to a trough, however LME metals prices fell in February and March.

- Global export prices fell 0.2% m/m while import prices rose 0.7% but generally pressures from traded prices have eased significantly from H1 2022, which is good news for central banks. Energy prices are now down 6% y/y and raw materials -12.6%.

Source: MNI - Market News/Refinitiv/CPB/Bloomberg

Fig. 2: Exports y/y%

Source: MNI - Market News/CPB

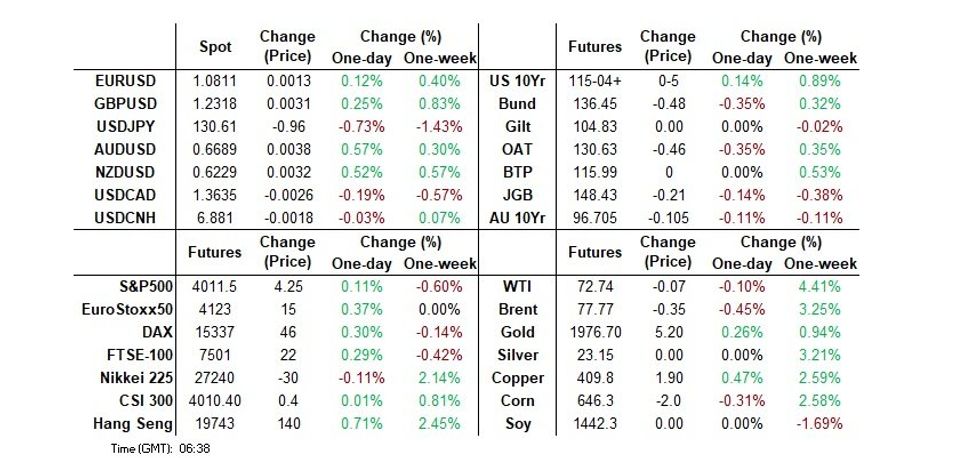

US TSYS: Richer In Asia

TYM3 deals at 115-04, +0-04+, observing a 0-10 range on volume of ~86k.

- Cash tsys sit 2-4bps richer across the major benchmarks, the curve has bull steepened.

- In early dealing tsys were marginally richer, as Asia-Pac participants used yesterday's cheapening as an opportunity to close short positions/enter fresh long positions in early dealing.

- Pressure on the USD, as an offer in USD/JPY spilled over, saw tsys continue to richen through the session.

- Despite the absence of a headline driver, gains briefly extended, 2 Year Yield showed below 3.9%. Gains moderated and tsys held richer observing narrow ranges with little follow through on moves for the remainder of the Asian session.

- Fed Governor Jefferson was on the wires early in the session, he didn't comment directly on the outlook for Fed policy, noting that the bank is still learning the full effects of tightening.

- On the docket today we have ECB speak from Lagarde, US Wholesale Inventories and Consumer Confidence. Fed VC Barr testifies before the Senate Banking Committee. We also have the latest 5-Year supply.

JGBS: Strong 40-Year Auction Pricing Promotes Twist Flattening

JGB futures hold on to their post-40-Year auction bid after some light richening in U.S. Tsys allowed the contract to tick away from session lows ahead of the Tokyo lunch break. That leaves the contract -23 as we head into the final hour of Tokyo trade, albeit nowhere near fully reversing the overnight weakness generated by a reduction (not a removal) in fear surrounding the global banking sphere. The well-received auction has prompted twist flattening of the wider JGB curve, with the major benchmarks now running 1.5bp cheaper to 8.5bp richer, pivoting between 10s and 20s. The swap curve has also twist flattened, with swap spreads generally flat through 10s and wider beyond there.

- Various policymakers have stressed the relative soundness of the Japanese banking sector, while soon to be departing BoJ Governor Kuroda has gone over old ground re: inflation and the need for continued easing.

- Japanese investing giant Dai-Ichi Life flagged a shift in capital allocation to JGBs from U.S. Tsys and other foreign securities, given the well-documented, elevated currency hedging costs imposed on the Japanese investor base at present. ALM duration matching activity sees Dai-Ichi preferring 30- & 40-Year JGBs, per the BBG interview. The firm also flagged a want to deploy capital in alternative assets as it looks to boost returns (private equity, real assets and hedge funds are potential destinations for their capital).

- Looking ahead, BoJ Rinban operations (covering 3- to 25-Year JGBs) headline domestically on Wednesday.

AUSSIE BONDS: Cheaper With A Tight Range

ACGBs are weaker (YM -11.0 & XM -11.0) ahead of the bell after trading in a relatively tight range in the Asia-Pac session. Once retail sales data printed at consensus and failed to provide a local driver, the market largely tracked movements in U.S. Tsys, which recouped a portion of NY session losses in Asia-Pac trade.

- Cash ACGBs are 10-11bp cheaper with the AU-US 10-year yield differential -2bp at -21bp.

- Swaps rates are 9-10bp higher with the 3s10s curve 1bp steeper and EFPs 1bp tighter.

- Bills strip pricing is -6 to -11 with reds leading.

- RBA dated OIS is 6-11bp firmer for meetings beyond May with expected year-end easing at 25bp.

- Locally, attention now shifts to the scheduled release of CPI Monthly for February tomorrow. BBG consensus is expecting another slowing in the Y/Y rate to 7.2% from 7.4% in January and 8.4% in December. It is important to note however that the series can be volatile from month to month given not all components are updated.

- With the global calendar relatively light until Friday when Euro Area CPI (Mar) and US PCE deflator (Feb) are released, the markets will be closely watching to see if the recent improvement in risk sentiment, and upward pressure on global yields, can extend further.

AUSTRALIA: Retail Sales Data Implies Volumes Contracted Moderately

February retail sales rose 0.2% m/m after +1.8% the previous month, exactly on expectations. The series is nominal and so the moderate increase implies that sales volumes contracted moderately. Following the March RBA meeting, Governor Lowe said that the Board would be looking at the “collective” signal from inflation, employment, retail and business confidence data. The NAB business survey and the labour market data for February both point to another 25bp hike on April 4 and retail sales were probably neutral. The CPI on Wednesday will round out the 4 key pieces of data.

- Retail sales in February were 6.4% higher than a year ago (Jan 7.5%) and appear to have stabilised around the September 2022 level after year-end volatility. They are showing weak 3-month momentum though at -5.9% annualised.

- All components rose, except other retailing, with department stores posting the strongest result at +1% m/m and 7.7% y/y followed by clothing & footwear +0.6% and 6.2%, and restaurants & takeaways +0.5% and 17.1%.

- The ABS noted that consumers continue to “pull back on discretionary spending in response to high cost of living pressures”. Household goods retailing was flat.

Source: MNI - Market News/ABS

Fig. 2: Australia retail sales vs CBA spending intentions y/y%

Source: MNI - Market News/ABS/Bloomberg

NZGBS: Off Cheaps, Outperforming $-Bloc

NZGBs closed mid-range 5-8bp cheaper with the 2/10 curve 3bp flatter after U.S. Tsys recouped a portion of NY session losses in Asia-Pac trade. NZGBs nonetheless outperformed its $-Bloc peers with the NZ/US and NZ/AU 10-year yield differentials respectively -9bp and -7bp on the day.

- Swaps closed at session bests 2-4bp weaker, implying tighter swap spreads.

- RBNZ dated OIS closed 4-8bp firmer for meetings beyond April with October leading. 24bp of tightening was priced for April with terminal OCR expectations pushed out to 5.20%.

- The NZ calendar remains light until later in the week with the next major release, not until ANZ Business Confidence and Building Consents on Thursday.

- Before then, Australia is scheduled to release CPI Monthly for February tomorrow. BBG consensus is expecting another slowing in the Y/Y rate to 7.2% from 7.4% in January and 8.4% in December.

- With the global calendar relatively light until Friday when Euro Area CPI (Mar) and US PCE deflator (Feb) are released, the markets will be closely watching to see if the recent improvement in risk sentiment, and upward pressure on global yields, can extend further.

FOREX: USD Pressured In Asia

The greenback is pressured in Asia today, regional equities are firmer and US Treasury Yields are lower. Yen is the strongest performer in G-10 space at the margins.

- USD/JPY prints at ¥130.50/130.60, ~0.8% softer today. Downside support comes in at ¥129.75, 76.4% retracement of the Jan 16 to Mar 8 rally.

- AUD/USD is also firmer, last printing at $0.6690/95. Australian retail sales for February printed as expected at 0.2%. Resistance is seen at 50-Day EMA ($0.6764). Firmer Iron Ore has aided AUD at the margins, futures in Singapore are up ~1.5% as we move back above $120/tonne.

- Kiwi has firmed above its 20-Day EMA ($0.6216), NZD/USD prints at $0.6230/35. Bulls first target a break of $0.6263 (200-Day EMA).

- Elsewhere in G-10 NOK is ~0.4% firmer. EUR is lagging gains seen elsewhere in G-10, EUR/USD is up ~0.1%.

- US Treasury Yields are lower, 2 year yields are down ~5bps. E-minis are ~0.2% firmer and Hang Seng is up ~0.7%. BBDXY is down ~0.3%.

- On the docket today we have ECB speak from Lagarde, US Wholesale Inventories and Consumer Confidence. Fed VC Barr testifies before the Senate Banking Committee.

FX OPTIONS: Expiries for Mar28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0875-80(E1.1bln), $1.0945-55(E1.8bln)

- USD/JPY: Y128.50-70($875mln)

- AUD/USD: $0.6500(A$575mln), $0.6750(A$652mln)

ASIA FX: Commodity Related FX Outperform

USD/Asia pairs are mostly lower, led by the commodity related currencies. In North East Asia, gains have generally lagged those seen elsewhere in the region. USD/CNH is back to unchanged, above the 6.8800 level. Tomorrow, we have South Korea consumer sentiment out, along with the BoT decision, with +25bps expected.

- USD/CNH was softer in early trade, in line with broad USD weakness, but couldn't sustain moves sub 6.8800. We sit back above this level now, unchanged for the session. This compares with a ~0.30% drop in the BBDXY index. China equities are underperforming more positive trends elsewhere in the region. Northbound stock connect flows are evident for the third straight session. They are modest overall though.

- 1 month USD/KRW hasn't been able to break back below the 1290 level, despite a firmer equity backdrop. Offshore investors have remained sellers of local equities today, with a further -$135.5mn in outflows (now -$438.8mn since the start of the week). 1 month USD/KRW was last back close to 1296.

- Spot USD/TWD sits just above session lows, last around 30.35. This is close to lows going back to late Feb, while the 200-day EMA sits slightly higher at 30.37. The simple 50-day MA is just above that at 30.38. There isn't much in the way of downside levels between here and the 30.00 handle. Today's modest TWD gains also come despite some weakness in local equities, with the Taiex off by around 0.8% at this point. This is line with weakness in the SOX through Monday's session, as core yields rebounded.

- USD/IDR is back sub the 15100 level (last 15090), around +0.45% firmer in IDR terms for the session so far. We are up slightly from session lows, but this puts the pair back to levels last seen in early Feb. The better equity tone, coupled with lower CDS levels will be driving improving risk appetite towards the IDR, particularly with light domestic news flows. 5yr CDS is back to 110, versus recent highs near 125.

- MYR is the best performer in the USD/Asia space. USD is pressured today as US Treasury Yields tick lower, firmer commodities have aided the MYR at the margins. Higher oil and palm oil prices since the start of this week have helped ringgit outperformance. Palm oil is up over 5%, although remains below the 200-day MA (MYR4114, versus current levels of MYR3974). From a technical perspective USD/MYR has ticked away from the 200-Day EMA (4.43) as it continues the recent downward momentum.

MNI Bank Of Thailand Preview - March 2023: +25bp In March, Is That The End?

EXECUTIVE SUMMARY

- The Bank of Thailand (BoT) is widely expected to hike rates 25bp to 1.75% on March 29. The statement will be monitored closely for downward revisions to forecasts, especially core inflation, and any changes to the “gradual policy normalisation” phrasing. The breakdown of the March vote is also likely to be important.

- Many no longer expect a further hike at the May 31 meeting given the lower-than-expected February inflation data and recent global events. There is significant uncertainty surrounding that meeting with CPIs on April 5 and May 5, BoT forecasts, the outcome of the Fed's May 3 meeting, any further banking troubles and May 14 elections all likely to influence the outcome.

- For the full piece, see here: BoT Preview - March 2023.pdf

EQUITIES: Most Regional Indices Higher, China Lags

Regional equity markets are mostly higher, following the positive lead from EU/US markets during Monday's session. US futures are also tracking higher, with 0.15/0.20% gains across eminis and Nasdaq futures. China shares are lagging, while gains elsewhere are under the 1% mark at this stage.

- The CSI 300 is off modestly, down 0.16%, while the Shanghai Composite Index is close to flat. This comes despite better trends from energy related names, which follows higher oil prices. Saudi Aramco has also taken a 10% stake in Rongsheng Petrochemical, which has likely helped at the margins as well.

- Northbound stock connect flows have been modestly negative again today (1.67bn yuan so far in the session).

- The HSI has been volatile, up 1.2% earlier in the session, before getting back close too flat. We now sit around ~0.70% higher.

- Elsewhere, the Topix is close to flat, while the Kospi is +0.60%, outperforming the Taiex, which is down -0.70%. This follows weakness in the semiconductor space during Monday's session (the SOX off more than 1%).

- The ASX 200 is up close to 1%, aided by broad based commodity price gains. Most SEA bourses are higher but gains are mostly under 0.50%.

GOLD: Bullion Stabilising After Safe Haven Flows Pulled Back

Gold fell 1% on Monday reaching a low of $1944.07/oz as banking fears eased, equities rallied and safe haven flows moved out of the precious metal. It has been range trading during APAC trading today and is up 0.1% to $1959.00, between the intraday high and low, even though the USD index is down 0.3% and US yields are lower.

- Trend conditions for bullion remain in place and recent downward moves are seen as corrective. The break above $1959.70, the February 2 high, confirmed the resumption of the bull trend that started in late September 2022. Prices continue to hold above this level and are only down 2.2% from their March 23 high.

- The Fed’s Barr appears before the Senate banking panel later and there is also US trade and house price data released. The focus of the week though is Friday’s US core PCE price index, the Fed’s preferred measure. It is expected to remain stable at 4.7% y/y in February.

OIL: Crude Eases Today But Brent Over 10% Above March Low

Oil prices are moderately lower during the APAC session with Brent down 0.4% to $77.78/bbl but WTI is only down 0.1% to around $72.75. The USD index is down 0.3%. Crude rose sharply on Monday as risk appetite improved on hopes that a broader banking crisis would be avoided, supply disruptions and a weaker dollar.

- WTI reached a high today of $73.05 and a low or $72.64, while Brent hit $78.27 followed by a low of $77.70.

- Bloomberg reported, that crude consumers, especially airlines, used the sharp drop in prices seen in March as an opportunity to boost protection against a rally expected later in 2023. Swap dealers reported the second-largest increase in long Brent positions on record for last week. As an example Lufthansa increased its hedging of planned consumption to 85%. Brent reached a monthly low of $70.12 on March 20 but is now 10.9% above that level.

- The Fed’s Barr appears before the Senate banking panel later and there is also US trade and house price data released. API inventory data also prints. The focus of the week though is Friday’s US core PCE price index, the Fed’s preferred measure. It is expected to remain stable at 4.7% y/y in February.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/03/2023 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 28/03/2023 | 0800/1000 | ** |  | IT | ISTAT Business Confidence |

| 28/03/2023 | 0800/1000 | ** | | IT | ISTAT Consumer Confidence |

| 28/03/2023 | 1230/0830 | ** |  | US | Advance Trade, Advance Business Inventories |

| 28/03/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 28/03/2023 | 1300/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 28/03/2023 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 28/03/2023 | 1315/1515 |  | EU | ECB Lagarde Speech at BIS Innovation Hub Opening | |

| 28/03/2023 | 1400/1000 | *** | | US | Conference Board Consumer Confidence |

| 28/03/2023 | 1400/1000 | ** | | US | Richmond Fed Survey |

| 28/03/2023 | 1400/1000 | | US | Senate Banking Committee Hearing | |

| 28/03/2023 | 1430/1030 | ** | | US | Dallas Fed Services Survey |

| 28/03/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 28/03/2023 | 1700/1300 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 28/03/2023 | 1700/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

| 28/03/2023 | 2000/1600 |  | CA | Federal budget (Release around 4pm, as finance minister delivers it to Parliament) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.