Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- JGB futures extended on their early bid into the bell and close just shy of best levels, +26. Cash JGBs are 3bp richer to 3bp cheaper, twist steepening, with a pivot around 10s (which operate in a narrow range between 0.50-0.51%, just through the peak of the BoJ’s YCC band). Tokyo participants have looked to the latest Bloomberg sources piece and survey covering the BoJ (both of which were released between yesterday’s local close and today’s open), which played down the likelihood of a hawkish policy tweak from the BoJ next week. Local data saw downticks in the headline and core Tokyo CPI readings in the month of February (driven by government subsidies surrounding energy), with the prints near enough meeting expectations, while there was a slightly larger than expected uptick in the excluding fresh food and energy metric.

- Firmer regional equities have boosted risk sentiment weighing on the USD, however ranges do remain modest with little follow through on moves in G10 FX, with the USD nudging lower at the margins.

- In Europe today Eurozone PPI data and ECB-speak from de Guindos headline. Further out the ISM Services survey provides the highlight ahead of the weekend. We also have a number of Fed speakers scheduled to cross.

US TSYS: Marginally Richer In Asia

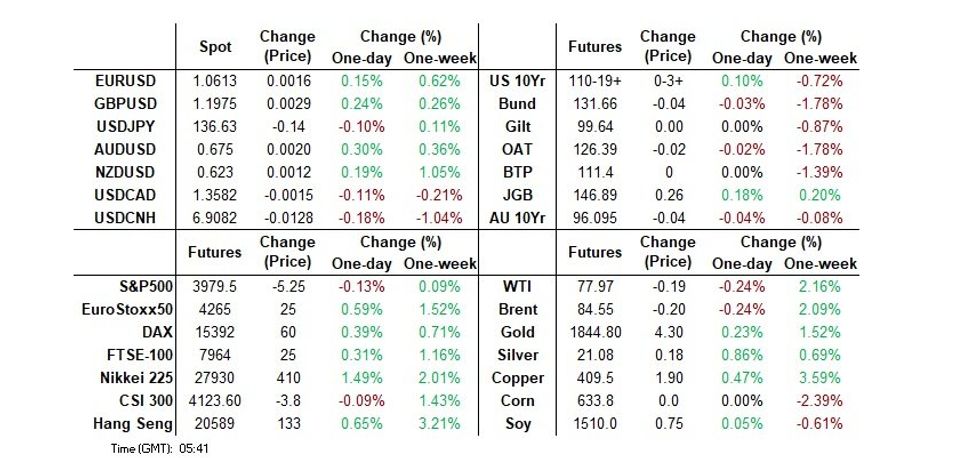

TYM3 deals at 110-19+, +0-03+, a touch off the top of the contained 0-05 range on volume of ~89k.

- Cash Tsys sit flat to 1bp richer across the major benchmarks, with some light bull flattening apparent.

- Modest pressure from February's Tokyo CPI data, the headline and core-core measures print a touch above expectations, saw Tsys weaken in early dealing.

- The pressure reversed as a bid in JGBs facilitated a recovery from early session lows.

- Tsys looked through the firmer than expected Caixin Services PMI print out of China, and the light richening held.

- Narrow ranges were observed for the remainder of the session with little follow through.

- Early in the Asian session Fed Gov Waller noted that a strong labour market could force the Fed to raise rates further than officials currently expect. Elsehwere, Minneapolis Fed President Kashkari ('23 voter) reiterated that inflation is very high, with demand exceeding supply.

- In Europe today Eurozone PPI data and ECB-speak from de Guindos headline. Further out the ISM Services survey provides the highlight ahead of the weekend.

JGBS: Curve Twist Steepens, Futures Outperform, YCC Band Breached

JGB futures extended on their early bid into the bell and close just shy of best levels, +26. Cash JGBs are 3bp richer to 3bp cheaper, twist steepening, with a pivot around 10s (which operate in a narrow range between 0.50-0.51%, just through the peak of the BoJ’s YCC band). 7s outperform on the bid in futures. Weakness in the long end was at least partially linked to payside swap flows, but the move in JGBs in now more notable, with twist steepening also observed on the swap curve.

- Tokyo participants have looked to the latest Bloomberg sources piece and survey covering the BoJ (both of which were released between yesterday’s local close and today’s open), which played down the likelihood of a hawkish policy tweak from the BoJ next week.

- Local data saw downticks in the headline and core Tokyo CPI readings in the month of February (driven by government subsidies surrounding energy), with the prints near enough meeting expectations, while there was a slightly larger than expected uptick in the excluding fresh food and energy metric. This comes after recent rhetoric from BoJ Governor-in-waiting Ueda flagged the likelihood of a slowing inflationary impulse in the months ahead. Meanwhile, the latest labour market report saw a modest downtick in the unemployment rate.

- The offer to cover ratios covering today’s BoJ Rinban operations were subdued to average (1.95-2.25x).

- Elsewhere, PM Kishida instructed the LDP to compile a package of additional measures to further curb the burden of the recent run of inflation.

- The aforementioned BoJ monetary policy meeting headlines next week’s local docket, with confirmation votes for BoJ Governor-in-waiting Ueda also slated.

AUSSIE BONDS: A Heavy Global Calendar Next Week With RBA Decision The Local Highlight

ACGBs move away from overnight lows to close near session highs (YM -3.0 & XM -4.0) with U.S Tsys lightly richening in Asia-Pac trade. The AU/U.S. 10-Year yield differential treads water at -16bp.

- Bills strip twist steepens with the whites out to Sep-23 +2bp and up to 6bp of cheapening seen beyond there.

- Ahead of the RBA’s rates decision on Tuesday, RBA-dated OIS is pricing a 92% chance of a 25bp hike. More broadly, strip pricing was mixed with meetings through October flat to -2bp, but November and December respectively +1 and +3bp firmer, as the market prices out any chance of an easing this year.

- The RBA rates decision (Tues) and RBA Governor Lowe’s AFR Summit speech (Wed) are the local highlights next week with the market keen for an update after last month’s hawkish shift. In the February decision statement, the RBA signalled multiple hikes by removing the ‘not on a pre-set course’. With Q4 WPI and January monthly CPI both surprising on the downside since then, the market will be watching to see if the RBA stays on the pre-set course of “further increases in interest rates will be needed”.

- Elsewhere, the global calendar is busy with the highlights: Fed Chair Powell’s semi-annual Monetary Policy Reports to Congress (Tue & Wed), BoC's decision (Wed), China’s CPI (Thu) and U.S. Payrolls (Fri).

NZGBS: Weaker Ahead of Heavy Global Calendar

NZGBs close near cheaps as the market looks to U.S Tsys for guidance heading into a next week’s heavy global calendar.

- Comments from RBNZ Governor Orr before market hours saw a marginally less hawkish message of “early signs of price pressures easing”, but U.S. Tsys were the driver today.

- Cash benchmarks close 7-9bp weaker across the curve, underperforming U.S Tsys. After narrowing from +26bp last Friday to an intraday low of flat yesterday, the NZ/US cash 2-year yield differential closes the week +10bp wider on the day at +15bp. The 10-year differential mapped out a similar path, closing in the middle of the week’s +54-74bp range.

- 2s10s swap curve bear steepens with rates +5-8bp higher, implying a 1-2bp tightening in swap spreads.

- RBNZ-dated OIS was subdued with pricing flat to 2bp firmer across meetings, leaving April meeting pricing at 40bp of tightening and terminal OCR pricing at the RBNZ’s projected OCR peak of 5.50%.

- A busy calendar of Antipodean and global data and events is seen next week. In Australia, all eyes will be on the RBA decision (Tue) and Governor Lowe’s speech at the AFR Business Summit (Wed). On the global calendar, the highlights will be Fed Chair Powell’s semi-annual Monetary Policy Reports to Congress (Tue & Wed), BoC’s decision (Wed), China’s CPI (Thu) and U.S. Payrolls (Fri).

FOREX: USD Softer In Asia, Regional Equities Firm

The greenback is marginally pressured in Asia today. Firmer regional equities have boosted risk sentiment weighing on the USD, however ranges do remain modest with little follow through on moves in G10 FX.

- AUD/USD is ~0.2% firmer, last printing at $0.6740/45 the next upside target is $0.6812 the low from 17 Feb. The final read of Judo Banks Feb Composite and Services PMI was on the wires this morning, the measures are a touch above 50 in expansionary territory. Jan Home Loans fell -5.3%, the RBAs tightening continues to be felt in the housing market.

- Kiwi is also firmed, NZD/USD is up ~0.1%. The pair firmed as the Hang Seng opened up over 1% before paring gains to sit marginally higher as regional equities retreated from best levels. ANZ Consumer Confidence fell in February. The Index printed 79.8, down -4.3%, as continued RBNZ tightening and the impact of Cyclone Gabrielle are felt.

- USD/JPY prints at ¥136.65/75, marginally below yesterday's closing level. The pair initially softened post Tokyo CPI prints, headline and core-core measure were a touch firmer than expectations. Support was seen ahead of ¥136.50 with the level tested several times through the session.

- EUR and GBP are both marginally firmer, benefiting from the pressure on the USD.

- Cross asset flows are mixed; Hang Seng is up ~0.8% and e-minis are ~0.2% lower. BBDXY sits ~0.1% lower, 10 Year US Treasury Yields are ~1bp softer.

- In Europe today Eurozone PPI data and ECB-speak from de Guindos headline. Further out the ISM Services survey provides the highlight ahead of the weekend. We also have a number of Fed speakers scheduled to cross.

FX OPTIONS: Expiries for Mar03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0500(E1.8bln), $1.0550(E577mln), $1.0595-00(E2.2bln), $1.0625-35(E893mln), $1.0675(E969mln), $1.0700-05(E1.8bln)

- USD/JPY: Y135.00($795mln), Y136.00($718mln)

- GBP/USD: $1.2060(Gbp645mln)

- AUD/USD: $0.6800(A$951mln)

- NZD/USD: $0.6100(N$1.0bln)

- USD/CAD: C$1.3500-15($591mln), C$1.3600($702mln)

- USD/CNY: Cny6.9000($1.3bln), Cny7.0000($800mln)

ASIA FX: KRW & INR Outperform, IDR & THB Lag

USD/Asia pairs are mostly lower, with the won and the Indian rupee the best performers at this stage. USD/CNH is lower but found support sub the 6.9000 level. Equities have been firmer around the region, albeit to varying degrees, while a softer USD against the majors has also helped. The weekend focus will be firmly on China's NPC, while on Monday we get South Korea CPI data.

- USD/CNH tried to break back below 6.9000 on a number of occasions but found USD support each time. Commentary from the PBoC, which pushed back against any imminent shift in monetary policy, appeared to weigh on local equities, which may have impacted CNH negatively. USD/CNH last stood at 6.9070.

- 1 month USD/KRW has traded with a firmer downside bias. The pair was last around the 1300 level, -0.70% sub NY closing levels. This comes despite only a modestly positive onshore equity lead. The market may be mindful of a positive growth surprise from this weekend's NPC (i.e. something closer to 6%), with the won seen as a good proxy for China-related sentiment.

- USD/SGD is slightly lower, last near 1.3475/80, but underperforming trends elsewhere in the region. The SGD NEER is down slightly, with weaker than expected retail figures (-0.8% y/y, +4.9% expected) and the PMI slipping back into contraction (49.6 from 51.2) likely weighing at the margins on NEER performance.

- USD/INR is down -0.40% in the first part of trade, last near 82.25. Rupee is firming in early trade on reports that offshore investor GQG Partners bought shares in four Adani group firms. Note also the services PMI rose further to 59.4 from 57.2 last month. USD/INR bears look to target 2023 lows at 80.89. Bulls still look to target a break of 83.00.

- Spot USD/IDR is through the 15300 level, last tracking around the 15310/15 region, slightly down from session highs. This puts us back to mid Jan levels. The pair is above all key EMAs, while the simple 100-day MA sits higher at 15432. IDR is the second worst performer within the region this past week, down 0.60%, with only MYR, off by nearly 1%, a worst performer. The rupiah is tracking lower for the fourth straight week. The continued push higher in core yields remains a headwind.

- THB has underperformed, with USD/THB around +0.15% higher for the session, last in the 34.80/85 region. Onshore equities remain under pressure, while yesterday's weaker trade figures may also still be weighing.

EQUITIES: Positive Ending To The Week, Japan & India The Standouts

Regional markets are tracking higher, following the positive lead from Wall St on Thursday, but gains haven't been uniform. China markets have struggled to maintain a positive bias, while in SEA a number of markets are weaker. US futures are softer as well, albeit away from session lows. Eminis last near 3980 (-0.11%), while Nasdaq futures are off slightly more -0.18% (near 12040).

- The HSI opened higher, but couldn't hold firm gains. Last we sat still +0.70% higher for the session. The PBoC held a press conference, which appeared to push back against any imminent easing signals in monetary policy. This weighed at the margins.

- The CSI 300 is close to flat, while the Shanghai composite is +0.25%. The focus on the weekend if the NPC. Market expectations for this year's growth target are in the 5-5.5% range. Anything higher (say closer to 6%) could support risk appetite in the early part of next week.

- The Nikkei 225 is outperforming, up +1.66% at this stage. Better services PMI numbers helped at the margin, while prospects of a weaker yen may also aid the export sector. Today's Tokyo CPI data was a touch firmer than expected, but the economic consensus has pushed out its expectation around the timing of further BoJ action (to June).

- The Kospi and Taiex have lagged, up only modestly. Cautious guidance from Micron (around margins and pricing) may have weighed at the margins.

- Indian shares are up firmly, over 1.2%. Reports that offshore investor GQG Partners bought shares in four Adani group firms, is aiding sentiment. GQG is reported to have bought ~$1.9bn worth of shares in four of the Adani companies.

- SEA markets are a touch weaker, with Malaysia, Thia and Indonesia shares down at this stage.

GOLD: Set To Post A Weekly Gain

Gold tracks just below the $1840 level, which is just shy of highs for the week. We are up 0.15% for the session so far, and tracking +1.5% higher for the week, the first since the second week of Feb. This looks outsized relative to the ~0.3% pullback int he DXY this week, although gold sold off more than implied by USD trends in Feb, so this may reflect some pay back.

- In terms of levels, the 20 and 50-day EMAs sit around the $1845/46 level, while the 100-day EMA sits on the downside around $1821.

- Gold ETF holdings have drifted lower, after blipping higher at the end of Feb. Note China's FX reserves data prints next Tuesday, which will give an update on the country's gold holdings from an official standpoint.

OIL: Maintaining Positive Bias Ahead Of China's NPC

Brent crude has been range bound so far today, currently sitting close to the $84.50/bbl level. WTI has traced a similar trajectory last just shy of the $78/bbl handle. Both benchmarks are tracing higher for the week. For Brent, we sit just north of the 20 and 50-day EMAs but the 100-day remains higher, closer to $86.50/bbl. We tested above this resistance point in Jan, but couldn't sustain the break.

- Prompt spreads also continue to track higher, back to 0.65 for Brent. This is highs back to Nov last year.

- The weekend focus will rest on China's NPC and growth targets for 2023. A rebound in China oil demand is seen as a key input underpinning higher oil forecasts for this year. It also comes after Saudi Aramco comments from earlier in the week that described China consumption as 'very strong'.

- Looking into next week, on Tuesday we get China trade figures, which will include oil import trends. Also out on that day will be the US EIA short term monthly outlook. Note Fed Chair Powell also testifies to the US Senate on Tuesday as well.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 03/03/2023 | 0700/0800 | ** |  | DE | Trade Balance |

| 03/03/2023 | 0700/0800 | * |  | NO | Norway Unemployment Rate |

| 03/03/2023 | 0700/0200 | * |  | TR | Turkey CPI |

| 03/03/2023 | 0745/0845 | * |  | FR | Industrial Production |

| 03/03/2023 | 0815/0915 | ** |  | ES | S&P Global Services PMI (f) |

| 03/03/2023 | 0830/0930 |  | EU | ECB de Guindos Q&A at CUNEF University | |

| 03/03/2023 | 0845/0945 | ** |  | IT | S&P Global Services PMI (f) |

| 03/03/2023 | 0850/0950 | ** | | FR | IHS Markit Services PMI (f) |

| 03/03/2023 | 0855/0955 | ** | | DE | IHS Markit Services PMI (f) |

| 03/03/2023 | 0900/1000 | ** | | EU | IHS Markit Services PMI (f) |

| 03/03/2023 | 0900/1000 | *** | | IT | GDP (f) |

| 03/03/2023 | 0930/0930 | ** |  | UK | S&P Global Services PMI (Final) |

| 03/03/2023 | 1000/1100 | ** | | EU | PPI |

| 03/03/2023 | 1330/0830 | * |  | CA | Building Permits |

| 03/03/2023 | 1445/0945 | *** |  | US | IHS Markit Services Index (final) |

| 03/03/2023 | 1500/1000 | *** | | US | ISM Non-Manufacturing Index |

| 03/03/2023 | 1600/1100 | | US | Dallas Fed's Lorie Logan | |

| 03/03/2023 | 1700/1200 | | US | Atlanta Fed's Raphael Bostic | |

| 03/03/2023 | 2000/1500 | | US | Fed Governor Michelle Bowman | |

| 03/03/2023 | 2115/1615 | | US | Richmond Fed Tom Barkin |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.