Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

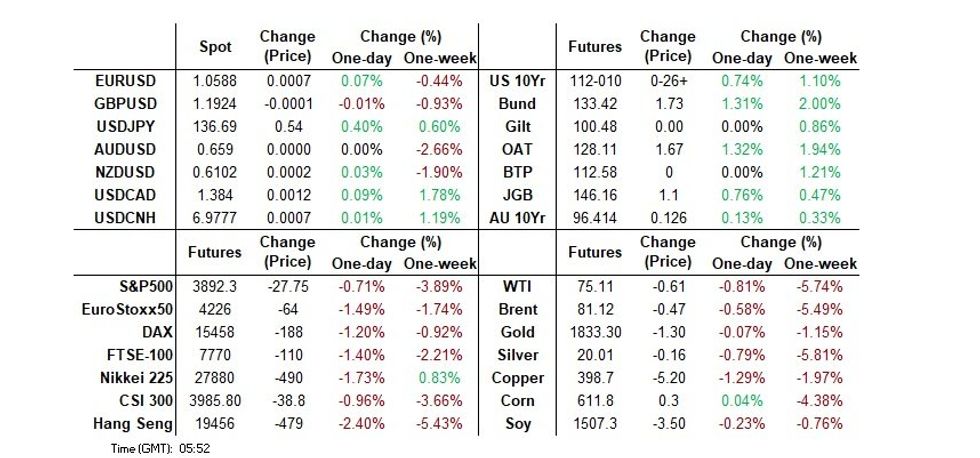

- JPY went offered and JGBs surged post-BoJ, with no surprise policy changes at Kuroda's final meeting.

- Elsewhere, worry surrounding Silicon Valley Bank applies pressure to equities, while CHF outperforms in the G10 FX sphere.

- UK GDP headlines in Europe. Further out, February's NFP print provides today's highlight (our preview of that event is here).

US TSYS: Firmer In Asia As SVB Worry Takes Hold, NFP In Focus

TYM3 deals at 112-09+, +0-26, a touch off the top of the observed 0-24+ range on very heavy volume of ~389K.

- Cash Tsys sit 6-10bps richer across the major benchmarks, the curve has bull steepened, building on Thursday's move.

- Continued weakness in U.S. equity futures, with that move centred on concerns re: the U.S. bank sector, has aided the bid in Tsys, with pre-NFP positioning also in play (given the focus on fresh short setting in the wake of Fed Chair Powell's comments earlier this week).

- The BOJ's decision to leave policy settings unchanged provided a further leg of support (this was the consensus view, but the unwind of hedging against a hawkish step added legs to a rally in JGBs that was already underway pre-decision).

- TYM3 took out resistance levels at 20 day EMA (111-31+) and 112-03 (24 Feb high). Initial resistance moves up to the Feb 17 high (112-18).

- S&P500 e-minis breached the 2 March low and bear trigger at 3,925.00 the break confirmed a resumption of the bear leg which started on Feb 2.

- UK GDP headlines in Europe. February's NFP print provides today's highlight, our preview is here.

JGBS: 10s Lead Post-BoJ Rally As Kuroda Leaves Policy Unchanged At Final Meeting

JGBs were notably richer on Friday, with the initial bid derived from the wider risk-off feel evident since NY hours developing further as the BoJ left its monetary policy settings unchanged.

- While the clear consensus looked for no change in the Bank’s monetary policy settings, the degree of conviction displayed in that view was highly variable as this was BoJ Governor Kuroda’s final monetary policy meeting, with the spectre of December’s surprise YCC tweak adding an extra layer of uncertainty.

- Post-BoJ decision moves looked very much like an unwind of hawkish plays, with futures over 100 ticks higher on the day (albeit not anywhere near meaningful resistance after the recent re-establishment of a technical downtrend).

- Cash JGBs are 1-11bp richer, with 10s now leading the move, sitting around the 0.39% mark after operating around the BoJ’s 0.50% YCC cap pre-decision. No change in tone of the BoJ’s post-meeting statement was key, with Kuroda playing a straight bat as he prepares to hand control over to Ueda (as opposed to tweaking policy to facilitate a ‘smoother’ handover and less pressure on Ueda).

- Swap spreads are now tighter out to 5s but wider beyond that, after swaps initially outperformed bonds into the BoJ decision.

- Kuroda’s final post-meeting press conference will get underway shortly.

AUSSIE BONDS: Strong Rally Ahead Of U.S. Payrolls

ACGB's close at highs (YM +10.8 & XM 12.6) with the wider risk-averse tone (centred on worry in the U.S. banking sector) setting the stall out for the space. Cash ACGBs close 10-12bp richer with the 3/10 curve 2bp flatter and AU/US 10-year yield differential +4bp at -24bp versus its cyclical low of -32bp intraday yesterday.

- Swap rates fell 12-17bp, although the move faded from extremes, particularly at the short-end.

- Similarly, Bills were stronger but off session bests with closes +4-10bp.

- RBA dated OIS softens 6-13bp for meetings beyond June with terminal rate expectations holding below 4.0% level at 3.98%. Notably, pricing for April declined to less than a 50% chance of a 25bp hike.

- With February Non-Farm Payrolls due in the overnight session, the market will stay tuned to developments in U.S. Tsys through the release. With data dependency the flavour of the week for the Fed, the market-moving potential of the data should not be underestimated.

- Beyond that, next week delivers February U.S. CPI (Tue), and February NAB Business Confidence (Tue) and Employment (Thu) in Australia. Attention to these releases will be amped up given the RBA's explicit focus on these data prints.

NZGBS: Rally But Lag Tsys

NZGBs close at best levels with yields 9bp lower across the curve in line with a strong extension rally in U.S. Tsys in Asia-Pac trade as the market eyes softer equities (on the back of worries surrounding the U.S. banking sector) ahead of U.S. Non-Farm Payrolls tonight. On a relative basis, NZGBs underperform U.S. Tsys but tread water against ACGBs with the NZ/US 10-year yield differential +5bp and the NZ/AU at +84bp versus its 8-year high (+90bp) struck yesterday intraday.

- Swaps close at the richest levels with rates 11-12bp lower, implying tighter swap spreads, with the 2s10s curve unchanged.

- RBNZ dated OIS soften 5-6bp for meetings beyond July. Terminal OCR expectations pull back to 5.58% but remain above RBNZ’s projected OCR peak of 5.50%.

- On the local data front, expansion in the February Business NZ Manufacturing PMI quickened, as the headline index its highest reading in 5 months, but Q4 Manufacturing Volumes declined 4.7% Q/Q after a revised +2.6% in Q3.

- Next week sees a raft of releases locally with Q4 Current Account (Wed) and Q4 GDP (Thu) the highlights. BBG consensus for Q4 GDP is currently -0.2% Q/Q and +3.3% Y/Y.

- In the interim, the market will surely stay focused on U.S. Tsys through Non-Farm Payrolls tonight while eyeing global equity moves.

FOREX: Yen Pressured In Asia, CHF Outperforming

JPY is the weakest performer in the G-10 space at the margins. The Yen was pressured as the BOJ held policy unchanged today.

- USD/JPY prints at ¥136.60/70, ~0.3% firmer today. The pair rose from a touch below ¥136 handle, meeting resistance ahead of ¥137.00 before paring gains in the aftermath of the BOJ decision. The spike higher may have been facilitated by downside protection that was in play. In the lead up to the decision the 1-week risk reversal was at the lowest level since the depth of the initial COVID outbreak.

- Kiwi is ~0.2% firmer, NZD/USD prints at $0.6105/10. Early in the Asian session Feb Business NZ Mfg PMI printed 52.0 with the prior revised higher to 51.2. Q4 Manufacturing Activity fell -0.4% with the prior read revised lower to 5.0%.

- AUD/USD is a touch firmer at $0.6595/0.6600. The pair was pressured in early trade, printing a fresh 2023 low, as the fall in US and regional equities and an offer in AUD/NZD are weighed. However support was seen at $0.6565 and the pair pared losses.

- CHF is the standout in the G-10 space, USD/CHF is down ~0.4%. The pair broke its 20-Day EMA (0.9328), and broke through $0.93 to last print 0.9290/95.

- EUR and GBP are both a touch firmer as softer US Treasury Yields marginally weigh on the USD.

- US Treasury Yields have ticked lower in Asia, 10 Year Yields is down ~9bps. S&P500 E-minis sit ~0.8% lower today, and the Hang Seng is ~2.5% lower.

- UK GDP headlines in Europe. Further out February's NFP print provides today's highlight, our preview is here

FX OPTIONS: Expiries for Mar10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0500(E1.5bln), $1.0525-30(E1.4bln), $1.0550-65(E1.5bln), $1.0600-20(E1.2bln), $1.0660-65(E1.1bln), $1.0695-00(E616mln)

- USD/JPY: Y135.00($606mln), Y136.00($2.6bln)

- AUD/USD: $0.6750(A$746mln), $0.6800-20($1.0bln)

- AUD/NZD: N$1.0750(A$914mln)

- USD/CAD: C$1.3710($618mln)

- USD/CNY: Cny6.9500($573mln)

EQUITIES: A Sea Of Red

Thursday’s risk negative-tone surrounding the troubles of Silcon Valley Bank reverberated through the Asia-Pac session, weighing on equities.

- E-minis extended on Thursday’s declines, with the S&P 500 contract below the 3,900 level after it breached a technical bear trigger. The contract operates a touch above its Asia-Pac base, last -0.7%, with any fresh extension lower set to turn focus towards the early January lows.

- The major Asia-Pac equity indices are comfortably in the red.

- The Hang Seng is the weakest, running 2.5% softer ahead of the weekend, while the Nikkei 225 (on the BoJ’s decision to stand pat) and CSI 300 were quick to unwind some relief rallies, before pushing onto fresh session lows thereafter.

- Japanese financials were particularly pressured in lieu of the BoJ decision, after the recent run of outperformance surrounding monetary normalisation hopes.

- Macro headline flow has been limited across Friday’s Asia-Pac decision, excluding the BoJ, leaving focus on Thursday’s headwinds for risk appetite.

GOLD: Thursday’s Rally Consolidated In Asia

Gold has benefited from the pullback in Fed terminal rate pricing, which sits nearly 25bp off of the peak pricing witnessed on the OIS strip just over 24 hours ago, operating just below 5.50%. This came in lieu of softer than expected U.S. labour market data and worry surrounding the U.S. banking sector given the troubles of Silicon Valley Bank.

- Spot gold has largely consolidated the gains registered on Thursday, last dealing little changed around the $1,830/oz mark.

- Technically, trend conditions in gold remain bearish after Tuesday’s strong sell-off reinforced this theme. The yellow metal needs to breach $1,858.3/oz, the Mar 6 high, to signal scope for a stronger bullish reversal.

- Known ETF holdings of gold have registered a fresh cycle low.

- Friday’s NFP report and any developments in the banking sector will set the tone ahead of the weekend.

OIL: Broader Risk-Negative Impulse Continues To Weigh In Asia

The risk-negative tone surrounding the U.S. banking sector applied further pressure to crude oil futures in Asia-Pac dealing, with Brent & WTI trading ~$0.50 softer apiece as a result. This builds on the weakness that was inspired by signs of more meaningful Fed tightening earlier in the week.

- Elsewhere, Russian oil export matters continue to catch the eye, with the FT reporting that “the US has privately urged some of the world’s largest commodity traders to shed concerns over shipping price-capped Russian oil, in a bid to keep supplies stable and regain some oversight of Moscow’s exports.”

- Friday’s NFP report and any developments in the banking sector will set the broader risk tone ahead of the weekend.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 10/03/2023 | 0700/0700 | ** |  | UK | UK Monthly GDP |

| 10/03/2023 | 0700/0700 | ** | | UK | Index of Services |

| 10/03/2023 | 0700/0700 | *** | | UK | Index of Production |

| 10/03/2023 | 0700/0700 | ** | | UK | Output in the Construction Industry |

| 10/03/2023 | 0700/0700 | ** | | UK | Trade Balance |

| 10/03/2023 | 0700/0800 | * |  | NO | CPI Norway |

| 10/03/2023 | 0700/0800 | *** |  | DE | HICP (f) |

| 10/03/2023 | 0745/0845 | * |  | FR | Foreign Trade |

| 10/03/2023 | 0900/1000 | ** |  | IT | PPI |

| 10/03/2023 | 0900/1000 |  | EU | ECB Panetta Presentation on Digital Euro | |

| 10/03/2023 | 1330/0830 | *** |  | CA | Labour Force Survey |

| 10/03/2023 | 1330/0830 | *** |  | US | Employment Report |

| 10/03/2023 | 1900/1400 | ** | | US | Treasury Budget |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.