Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- As widely expected, the RBNZ left interest rates unchanged at 5.50%. The accompanying statement suggested rates would be held in restrictive territory for the foreseeable future, although it didn't hint at any fresh need for further policy tightening. NZGBs closed sharply richer with yields 10-14bp lower on the day, while terminal OCR expectations have softened to 5.64% (Nov'23) versus 5.81% at the start of the week and 5.67% on Friday. NZD/USD is still higher against the USD but has lagged AUD and JPY.

- USD/JPY has made fresh lows, with lower yield US-JP differentials aiding the move. In the Tokyo afternoon session, JGB futures are sitting just off the Tokyo session’s worst levels at 147.27, -47 compared to the settlement levels. 10yr swap is near 0.70%, while the 10yr government bond yield is just above 0.47%.

- USD/CNH has also made fresh multi week lows, although there is less support evident from local equities so far today. Other USD/Asia pairs are lower, with the exception of USD/THB which has rebounded strongly amid fresh election uncertainty around PM candidate Pita's eligibility.

- The highlight of today's docket is the latest US CPI print, the MNI preview is here.

MARKETS

US TSYS: Marginally Richer In Asia, CPI On Tap

TYU3 deals at 111-11+, +0-03, a 0-05 range has been observed on volume of ~59k.

- Cash tsys sit 1bp richer across the major benchmarks.

- Tsys have been range bound in a muted Asian session on Wednesday, local participants are perhaps sidelined due to the proximity of today's June CPI print.

- Support was seen on spillover from NZGBs, as the RBNZ held the OCR steady at 5.50%, however the move didn't follow through and tsys ticked away from session highs.

- The highlight of today's docket is the latest US CPI print, the MNI preview is here.

- There are a number of Fed speakers scheduled to cross including Richmond Fed President Barkin, Minneapolis Fed President Kashkari and Atlanta Fed President Bostic. The latest 10-Year Supply is also due.

JGBS: Futures At Session Lows, Through Key Support, 20-Year Supply Tomorrow

In the Tokyo afternoon session, JGB futures are sitting just off the Tokyo session’s worst levels at 147.27, -47 compared to the settlement levels. The session low so far has been 147.23. This comes despite PPI and Core Machine Orders data undershooting expectations.

- According to the MNI technicals team, a breach of 147.34 signals a deeper reversal and opens 146.11, the Feb 22 low.

- As reported by Bloomberg (ICYMI), the decline in JGB futures, coupled with the absence of any official statements from Japanese authorities, is intensifying speculation about a potential policy adjustment from the BoJ this month. Although the BoJ has not provided any hints, some traders are preparing for a larger JGB short position that could gain momentum and continue to grow once policy-tightening measures are eventually implemented. (See link)

- The cash JGB curve, beyond the 1-year zone, has bear steepened in the Tokyo afternoon session with the futures linked 7-year zone underperforming (3.8bp cheaper). The benchmark 10-year yield is 1.3bp higher at 0.472%, below the BoJ's YCC limit of 0.50%.

- The 20-year benchmark is 1.9bp cheaper at 1.093%, ahead of tomorrow’s supply.

- Swap rates are higher beyond the 1-year with the curve steeper. Swap spreads are wider beyond the 2-year.

- Tomorrow the local calendar sees International Investment Flow (Jul 7) along with 20-year supply.

AUSSIE BONDS: Richer, RBA Gov. Lowe Announces Changes To RBA

ACGBs richened to Sydney session highs as RBA Governor Lowe’s commenced his speech to the Economic Society of Australia, but reversed part of the gains (YM +4.0 & XM +4.0) after the Q&A session revealed little that was new with respect to the policy outlook.

- Lowe did, however, announce changes in response to the recent review of the central bank, according to the ABC. Amongst other initiatives, from 2024, the RBA board will only meet eight times a year, rather than 11. He said the RBA governor will hold a press conference after every board meeting to explain the board's interest rate decision. (See link)

- Cash ACGBs are 4-5bp richer with the AU-US 10-year yield differential -4bp at +18bp.

- Swap rates are 4-6bp lower.

- Bills pricing is +2 to +6 with late whites leading.

- RBA dated OIS 7-8bp softer for meetings beyond December.

- Tomorrow the local calendar sees June MI Inflation Expectations.

- Attention now turns to the release of June US CPI data later. Consensus puts core CPI at 0.3% m/m. A higher-than-expected reading, particularly with robust details in ex-shelter services, would further solidify the "higher for longer" narrative. Conversely, if there is a miss, it would have the most significant impact on pricing expectations for September.

NZGBS: Sharply Richer After RBNZ Leaves OCR At 5.50%

NZGBs closed sharply richer with yields 10-14bp lower on the day after the RBNZ decided to leave the OCR at 5.50%. The 2/10 cash curve is steeper.

- According to the RBNZ, the level of interest rates is constraining spending and inflation pressure as anticipated and required. The Committee agreed that the OCR will need to remain at a restrictive level for the foreseeable future, to ensure that consumer price inflation returns to the 1 to 3% annual target range, while supporting maximum sustainable employment. Note we get Q2 inflation data next Tuesday.

- Swap rates are 6-8bp lower after the decision, and 11-13bp lower on the day.

- RBNZ dated OIS is 2-12bp softer across meetings, Apr’24 leading. The market had given a 25bp hike today a 10% chance. Terminal OCR expectations have softened to 5.64% (Nov'23) versus 5.81% at the start of the week and 5.67% on Friday.

- Tomorrow the local calendar releases REINZ House Prices, Manufacturing PMI, Food prices and Retail Card Spending data.

- Attention now turns to the release of US CPI data later. Consensus puts core CPI inflation at 0.3% m/m in June versus 0.44% in May.

RBA: Policy Meetings Cut To 8 (From 11) In 2024

RBA Governor Lowe has announced several changes to the RBA policy setting framework. In a speech the Governor has stated the following, see this link for more details.

- "From 2024, the Board will meet eight times a year, rather than 11 times as is currently the case. Four of the meetings will be on the first Tuesday of February, May, August and November. The other four meetings will be held midway between these meetings. The exact dates for 2024 will be published soon and the dates for future years will be published well in advance."

- "The Board meetings will be longer than is currently the case. They will typically start on the Monday afternoon and then continue on the Tuesday morning. The outcome of the meeting will be announced at 2.30 pm on the second day, typically a Tuesday as is the case now."

- "The Governor will hold a media conference after each Board meeting to explain the decision. The media conference is expected to be held at 3.30 pm."

- "The quarterly Statement on Monetary Policy will be released at the same time as the outcome of the Board meeting (in February, May, August and November), rather than on the following Friday as is currently the case. Given this and other changes, we are reviewing the structure of this document."

RBNZ: Holds Steady, To Stay In Restrictive Territory

As widely expected, the RBNZ left interest rates unchanged at 5.50%, This was the sell-side consensus and our own firm bias.

- The accompanying statement indicated rates will need to stay in restrictive territory for the foreseeable future in order to ensure that inflation returns to the 1-3% target, while supporting sustainable employment. The current level of policy rates is constraining inflation and spending as anticipated.

- The global growth backdrop is weaker, which is weighing on NZ related commodity prices, while global inflation pressures have moderated.

- Local inflation pressures are easing and are expected to continue to do so. The labor market is still tight and operating beyond maximum capacity but there are signs of reduced pressure, which is expected to be aided by an on-going recovery in net migration.

- Consumer and business spending is generally softer, as is residential construction activity. House prices have returned to more sustainable levels.

- Inbound tourism activity is supporting spending, as is the flood rebuilds, although the RBNZ expects broader government spending to moderate as a share of GDP (adjusted for inflation).

- All in all, the RBNZ appears happy with its current policy stance. The restrictive stance will be maintained in the near term, with further tightening likely to be dependent on upside inflation/growth surprises. Note we get Q2 inflation data next Tuesday.

NZ RATES: RBNZ Dated OIS Softer After RBNZ Holds Policy Steady

RBNZ dated OIS is 1-7bp softer across meetings, May’24 leading, after the RBNZ decides to leave the cash rate unchanged at 5.50%. The market had given a 25bp hike today a 10% chance.

- Terminal OCR expectations have softened to 5.65% versus 5.81% at the start of the week and 5.67% on Friday.

Figure 1: RBNZ Dated OIS Terminal Rate Pricing (%)

Source: MNI – Market News / Bloomberg

FOREX: Greenback Pressured In Asia

The Greenback has been pressured through the Asian session, a continuation of the recent move lower in USD/JPY which printed its lowest level since mid-June has spilled over into broader USD weakness ahead of today's CPI print.

- USD/JPY prints at ¥139.50/60, the pair is ~0.6% lower. There was no obvious headline driver with pre-US CPI positioning and technical flows weighing on the pair. The next support level is ¥139.18, 38.2% retracement of Mar-Jun bull leg.

- AUD is the strongest performer in the G-10 space at the margins. AUD/USD is up ~0.6% last printing at $0.6720/25. The next upside target is $0.6806 the high from June 22. Firmer commodities have aided the bid in AUD with Iron Ore futures up ~2.4% and Copper up ~0.7%.

- Kiwi is ~0.5% firmer despite the RBNZ's decision to hold the OCR steady at 5.50%. NZD/USD sits a touch above the 200-Day EMA, a level which bulls have not been able to sustain a break of.

- Elsewhere in G-10 EUR and GBP are both ~0.2% firmer. The Scandies are up, NOK and SEK are both ~0.4% higher, however liquidity is generally poor in Asia.

- Cross asset wise; BBDXY is down ~0.3% and US Tsy Yields are a touch lower. E-minis are ~0.1% higher and Hang Seng is up ~1%.

- The highlight of today's docket is the latest US CPI print, the MNI preview is here.

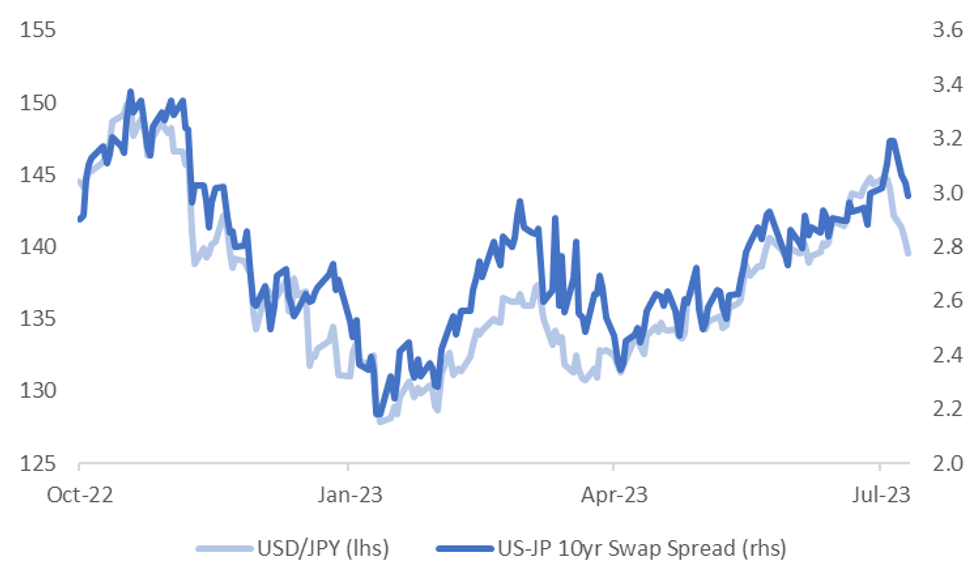

JPY: Yen Rebound Continues, Relative Yield Momentum Helping

USD/JPY continues to track lower, the pair last in the 139.50/55 region, down a further 0.60% in Asia Pac trade so far. Session lows were marked just under 139.40. We aren't too far off 139.18, a 38.2% retracement of Mar-Jun bull leg. Further south is the 100-day EMA around the 138.30 region.

- Position adjustment, paring of carry trade positions, appears one explanation for JPY strength. Since the start of the month yen is up 3.45%, only bettered by NOK in the G10 space. The yen has been outperforming other higher beta plays though, with AUD/JPY tracking lower for the past 5 sessions.

- Market expectations for the upcoming BoJ meeting at end July remain fairly modest in terms not expecting any meaningful shifts. Still, in recent sessions we have seen Japan yields outperform their US counterparts. Japan's 10yr swap is 0.69%, up nearly 15bps since the start of the month, while the 10-yr US swap is off 12bps since the end of last week.

- The chart below overlays the US-JP 10yr swap spread against USD/JPY. The move lower in the pair looks too large for the relative yield movements, but the spread is trending yen's favour.

- The 10yr government bond yield remains below the BoJ's 0.50% ceiling though, last near 0.47%, which is below earlier YTD highs when the market arguably saw larger risks of a BoJ shift.

Fig 1: USD/JPY Versus US-JP 10yr Swap Spread

Source: MNI - Market News/Bloomberg

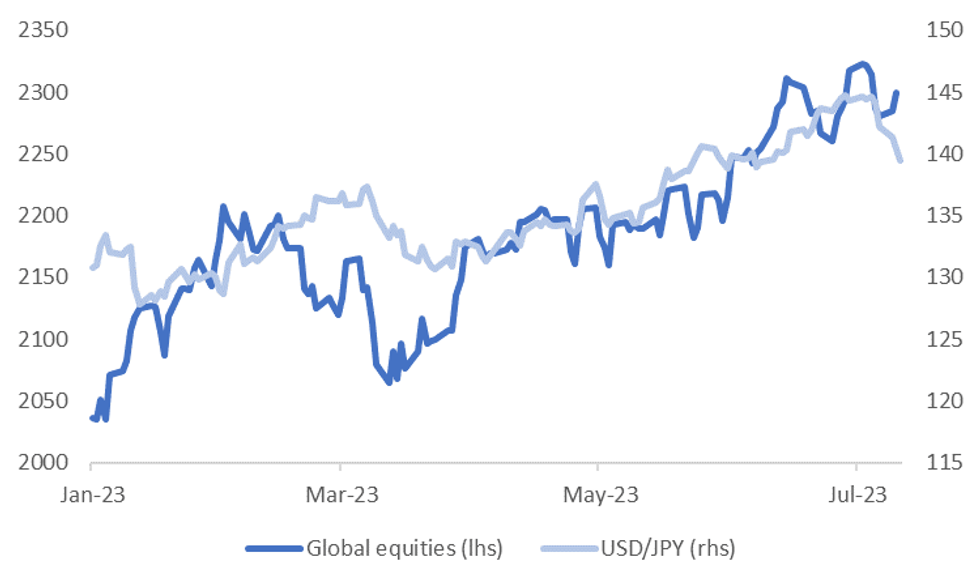

- Recent yen strength doesn't appear to reflect renewed risk aversion, see the second chart below of USD/JPY versus global equities.

Fig 2: USD/JPY Versus Global Equities

Source: MNI - Market News/Bloomberg

EQUITIES: Mixed Trends Ahead Of US CPI Print

Regional equity sentiment has been mixed today. China and Japan markets have struggled for positive traction, but we have mostly seen positive gains elsewhere. US futures are ticking higher, but only modestly. Eminis were last near 4476, +0.05% firmer for the session.

- China mainland stocks are a touch lower at the break. The CSI 300 close to flat at this stage, while the Shanghai Composite is down 0.13%. Onshore media has highlighted local analysts calling for fresh fiscal stimulus in H2.

- The HSI is faring better, up 1.15% at this stage. The Golden Dragon Index continued to recover in US Trade on Tuesday, up a further 1.61%, so we may be seeing some positive carry over from this.

- Japan stocks are softer, with a firmer yen likely weighing at the margins (up 3.43% month to date). The Topix is off by around 0.50% at this stage, Nikkei 225 -0.60%.

- Other markets are doing better, albeit modestly. The Taiex and Kospi up by around 0.25%.

- In SEA gains are slightly higher, with the Philippine index up nearly 0.70% at this stage.

- Thai stocks may be impacted by PM candidate Pita's case being referred to the Thai constitutional court. Tomorrow the Thai parliament is scheduled to vote on a new PM.

OIL: Holding Near Recent Highs, Brent Eyeing $80/bbl Handle

Brent crude sits close to unchanged for the session, last tracking around $79.50/bbl. Earlier highs came in at $79.75/bbl, while a low of $79.31/bbl was seen. We did see a +2.2% gain for Brent on Tuesday, so by and large we are holding onto those gains for far in Wednesday trade. WTI was last near $74.95/bbl, a touch above NY closing levels from Tuesday.

- Broader macro themes have unfolded in a similar fashion to yesterday, with USD sentiment under pressure, the BBDXY off a further 0.30%. On-going China stimulus hopes has been another focus point, with onshore media in China highlighting local analysts calling for more fiscal stimulus in H2.

- Bloomberg also notes reduced Russian supply (based of vessel tracking) to July 9, which suggests OPEC+ supply cuts may be biting further.

- For oil bulls the $80/bbl handle is not too far away, while the 200-day EMA is higher at $82.32/bbl.

- Coming up later is the EIA release of its weekly report on US crude stockpiles.

GOLD: Hits Highest Level In Three Weeks

Gold is 0.4% higher in the Asia-Pac session, after touching the highest level in almost three weeks on Tuesday, supported by falling US tsy yields and a weaker dollar ahead of US CPI data today.

- During a generally quiet New York session, the 10-year tsy yield continued its recent downward trend, while the value of the US dollar dropped to its lowest point since mid-June. These developments typically favour non-interest-bearing metals, such as gold.

- Consensus puts core CPI inflation at 0.3% m/m in June as it slowed from a modest beat of 0.44% in May. There is no evidence that the downside miss in nonfarm payroll gains last Friday has deterred FOMC participants from signalling their preference to raise rates twice more this year. An above-expected print and/or a report with strong details in ex-shelter services would reinforce the "higher for longer" theme; a miss most impactful for September pricing. See the MNI CPI preview here.

BOK: MNI BoK Preview - July 2023: Holding Steady At 3.50%

- All of the 14 economists surveyed by Bloomberg expect rates to remain on hold at 3.50% at tomorrow’s policy meeting. This is also our firm bias.

- The on-hold outcome looks to be a fairly straight forward one at this policy meeting, given the evolution of headline inflation pressures, which continue to moderate.

- The central bank has left the door ajar for tighter policy, with 6 out of 7 board members seeing a peak rate of 3.75% as possible at the last board meeting. This is likely to be a major focus point of tomorrow’s meeting, in terms of whether we see a tone down in the hawkishness rhetoric. We suspect some members will still advocate risks that the policy rate can tighten further.

- See the full preview here:

ASIA FX: USD/Asia Pairs Lower Again, Although USD/THB Rebounds On Fresh Election Uncertainty

USD/Asia pairs are uniformly lower, with USD/CNH tracking to fresh multi week lows, aided by softer dollar trends against the majors. The strong exception is USD/THB, which rallied over 1% from intra-day lows, amid fresh election uncertainty around PM candidate Pita. Tomorrow the focus is on China trade figures for June, with export growth expected to cool further, and the BoK decision, with no change expected.

- USD/CNH hit fresh multi-week lows of 7.1857, but sits slightly higher now, last just above 7.1930. Weaker USD trends, with the BBDXY sub 1217, led by USD/JPY has helped CNH sentiment. Stimulus talks continue, with onshore media highlighting onshore analysts calling for fiscal stimulus in H2. At this stage, onshore equities are struggling to gain much traction.

- 1 month USD/KRW has tracked to fresh lows back to mid June. We got to a low under 1286, but now sit slightly higher at 1288. Lower USD/JPY levels is helping, while the equity backdrop has remained positive, although offshore investors have sold $102.4mn of local equities so far today. Tomorrow, the BOK is widely expected to leave rates on hold at 3.50%.

- USD/THB has firmed on headlines that the Thai poll body will refer PM candidate Pita's election eligibility to the constitutional court, according to local media reports. This follows earlier reports of Pita owning media shares, which may have breached election rules. USD/THB was at 34.65 earlier in the session but spiked to 35.075, before settling back now at 34.91/92 (a +1% trough to peak move). This comes ahead of tomorrow's gathering of parliament to vote for a new Prime Minister. These latest headlines clearly cast doubt on how tomorrow's vote will unfold and Pita's candidacy more broadly. Note that even if Pita fails to secure enough votes to become PM, he can still stand again at the next parliament sitting, which is expected on July 19.

- Broader USD/Asia flows are dominating in early dealing for the Rupee, USD/INR is ~0.1% lower as the greenback is pressured in Asia. The pair deals at 82.25/30, and sits a touch above the 20-Day EMA (82.2771). We sit ~0.6% below the high from July 7 (82.7562). Equity inflows from Foreign investors have continued in July, a total of $1.46bn in Indian equities have been purchased in the month till Monday. On tap today we have the June CPI print, which is expected to tick higher to 4.60% Y/Y from 4.25% in May. Also due is May Industrial Production, a print of 5.0% Y/Y is forecast and the prior read was 4.2%.

- The SGD NEER (per Goldman Sachs estimates) has retreated from its highest level since 13 June, printed in early dealing however the measure is holding marginally firmer. We now sit ~0.5% below the upper end of the band. Broader USD trends are dominating flows for USD/SGD, the pair is down ~0.3% today and sits at its lowest level since mid-June. USD/SGD is ~1.5% below month to date highs and last prints at $1.3370/80. A reminder that the only local data of note this week is Friday's Advance Q2 GDP print, a fall of 0.2% Q/Q is expected.

- The Ringgit is holding early gains against the USD, broader greenback trends are dominating flows with this evenings US CPI print in view. USD/MYR prints at 4.6480/4.6520, the pair is ~0.2% lower today and sits ~1% below year to date highs seen in late June. May Industrial Production was stronger than forecast, printing at 4.7% Y/Y vs 0.0% exp. Manufacturing Sales Value rose 3.3% in May.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/07/2023 | 0600/0700 |  | UK | BOE FPC Summary and Record | |

| 12/07/2023 | 0700/0900 | *** |  | ES | HICP (f) |

| 12/07/2023 | 0800/0900 | | UK | Financial Stability Report press conference | |

| 12/07/2023 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 12/07/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 12/07/2023 | 1230/0830 | *** | | US | CPI |

| 12/07/2023 | 1230/0830 | | US | Richmond Fed's Tom Barkin | |

| 12/07/2023 | 1345/0945 | | US | Minneapolis Fed's Neel Kashkari | |

| 12/07/2023 | 1345/1545 |  | EU | ECB Lane panels at NBER conference. | |

| 12/07/2023 | 1400/1000 | *** |  | CA | Bank of Canada Policy Decision |

| 12/07/2023 | 1400/1000 | | CA | Bank of Canada Monetary Policy Report | |

| 12/07/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 12/07/2023 | 1500/1100 | | CA | Bank of Canada Governor press conference | |

| 12/07/2023 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 12/07/2023 | 1700/1300 | | US | Atlanta Fed's Raphael Bostic | |

| 12/07/2023 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

| 12/07/2023 | 1800/1400 | | US | Fed Beige Book | |

| 12/07/2023 | 2000/1600 | | US | Cleveland Fed's Loretta Mester |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.