Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

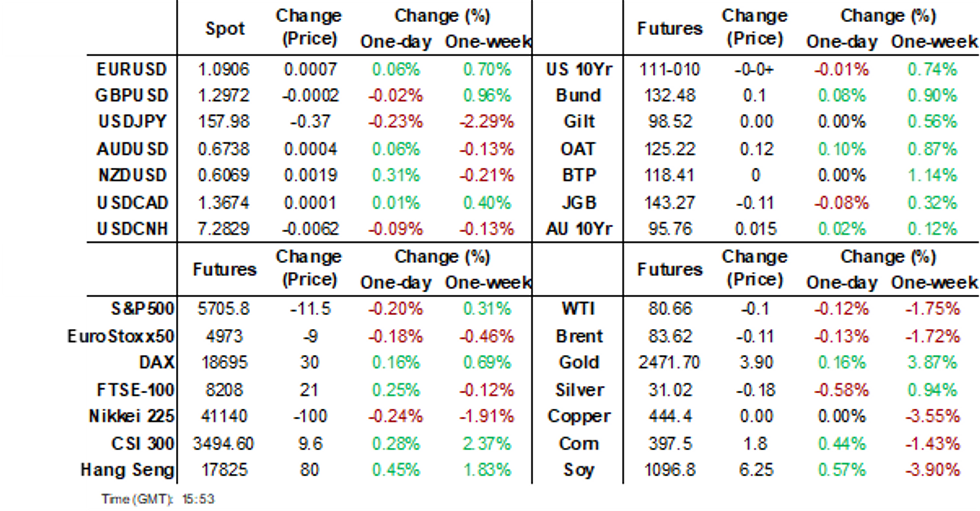

- The RBNZ’s measure of core inflation from its sectoral factor model moderated to 3.6% y/y in Q2 from 4.2%, the lowest since Q3 2021 but still above the central bank’s 1-3% band. We believe though that it will want to see Q3 CPI on October 16 before cutting rates. NZGBs closed on a weak note, with yields 2-3bps higher on the day and 3-5bps higher than pre-CPI levels. NZD recouped some of its recent losses.

- Treasury futures gave back all the post NY close moves in the first half of the session today, we have since traded sideways in tight ranges. JGB futures are weaker and at session cheaps, -7 compared to settlement levels.

- Later the Fed’s Barkin and Waller both speak on the economy and the Beige Book is published. June UK CPI and final June euro area CPI print, as well as US June housing and IP data.

MARKETS

US TSYS: Tsys Futures Little Changed, Curve Bear-Flattens

- Treasury futures gave back all the post NY close moves in the first half of the session today, we have since traded sideways in tight ranges. TUU4 is -0-0⅛ lower at 102-19⅝, while TYU4 is back to unchanged from NY closing levels but -0-03 from the morning highs at 111-10.

- Cash treasury curve has bear-flattened today, yields are 0.5-2bps cheaper.

- The 2s10s curve made new highs overnight of -20.680 on the back of stronger-than-expected retail sales, we now trade 7bps lower at -27.5bps.

- US futures are pricing a 6.5% chance of a rate cut in July and 100% chance of a cut in September for a cumulative cut of 26.6bps.

- Projected rate cut pricing into year end remains slightly cooler vs. late Monday levels (*): July'24 at -6.5% w/ cumulative at -1.6bp at 5.313%, Sep'24 cumulative -26.6bp (-27.5bp), Nov'24 cumulative -42.9bp (-44.1bp), Dec'24 -65.4bp (-65.8bp).

- Focus turns to Wednesday's Build Permits, House Starts, Beige Book, Tsy 20Y Bond auction reopen

JGBS: Cash Bonds Little Changed, 5-year Climate Transition Supply Tomorrow

JGB futures are weaker and at session cheaps, -7 compared to settlement levels.

- With the domestic calendar light today, the futures move away from session bests was assisted by a 1-2bps cheapening in cash US tsys in today’s Asia-Pac session.

- (MNI) Heightened uncertainty over the U.S. economy will make a Bank of Japan rate hike less likely and fuel Governor Kazuo Ueda’s cautious approach to monetary policy when the board meets July 30-31, MNI understands. (See link)

- Ueda will prefer to hold the policy interest rate until he receives evidence the U.S. economy will not deteriorate sharply. While the BoJ has not revealed whether Ueda will attend next month’s Jackson Hole economic meeting, the governor joined last year’s session and will likely make an appearance this year to gather insight into the U.S. economy.

- A former BoJ economist last week gave a roughly 40% chance of a July rate hike due to favourable trends in the Tankan survey, wages and services prices.

- Cash JGBs are slightly mixed across benchmarks, with yield movements bounded by +/- 1bp. The benchmark 10-year yield is 0.1bp lower at 1.028% versus the cycle high of 1.108%.

- Swap rates are little changed across maturities, with the curve slightly flatter and swap spreads mostly tighter.

- Tomorrow, the local calendar will see Trade Balance data alongside 5-year Climate Transition supply.

AUSSIE BONDS: Slightly Richer, June’s Employment Report Tomorrow

ACGBs (YM flat & XM +1.5) are slightly richer and sit near the bottom of today’s ranges. With the domestic calendar light, the local market has drifted with cash US tsys, which are 1-2bps cheaper in today’s Asia-Pac session after yesterday’s solid gains.

- Today’s lacklustre performance may also reflect some spillover from NZGBs. NZGB benchmarks have cheapened 3-5bps following today’s release of Q2 CPI. While the headline CPI came in moderately lower than expected, the important domestically driven non-tradeables came in slightly higher than the RBNZ expected.

- June jobs data prints tomorrow and will be watched closely for signs of a pickup in the pace of labour market easing ahead of Q2 CPI due on July 31 and the next RBA meeting on August 6.

- Even if the unemployment rate prints in line with consensus at 4.1%, the Q2 average will be close to the RBA’s May forecast of 4.0%, but still above Q1.

- Bloomberg consensus is forecasting a 20k increase in new jobs.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session.

- Cash ACGBs are 1bp richer, with the AU-US 10-year yield differential at +7bps.

- Swap rates are 3bps lower.

- The bills strip has bull-flattened, with pricing flat to +5.

- RBA-dated OIS pricing is 1-4bps softer across meetings. Terminal rate expectations sit at 4.40%.

AUSTRALIAN DATA: Monthly CPIs Suggest That Australia Won’t Follow NZ’s Moderation

There is a high correlation between Australian and NZ CPI inflation over both 3- and 5-year periods. With Australia’s Q2 CPI not printing until July 31, there is some information in the NZ data – that Australia should see a moderation in quarterly non-tradeables growth. However, NZ’s Q2 headline printed lower than expected and moderated to 3.3% y/y from 4%, whereas Australia’s monthly CPI data for April/May are pointing to a pickup in annual headline and underlying inflation.

- The RBA forecast in May that Q2 CPI would pickup to 3.8% from 3.6% in Q1. While Governor Bullock has warned about extrapolating from the monthly averages, they have been within 0.1pp in both Q1 and Q4. The April/May headline average is in line with the RBA at 3.8% y/y, which would require a 1% q/q rise, the same as Q1. However, the annual correlation with NZ is 90% signaling that there may be some downside risk.

Australia vs NZ CPI y/y%

Source: MNI - Market News/Refinitiv

- The April/May average of the trimmed mean is at 4.25%, well above the RBA’s 3.8% projection. This means that Q2 could print at least at 1% q/q. The RBNZ’s measure of underlying inflation moderated to 3.6% in Q2 from 4.2% which is materially below Australia’s Q2 average.

- NZ non-tradeables inflation was slightly stronger than expected at 0.9% q/q and 5.4% y/y but still lower than Q1’s 1.6% and 5.8%. The Q2 average of Australia’s non-tradeables inflation is 5.1%, below NZ’s but the gap is narrowing. The annual rate suggests that Australia’s quarterly rise will be lower than Q1’s, a trend that was seen in NZ too. The correlation between the annual rates stands around 90%.

AUSSIE BONDS: AU-NZ 10Y Yield Differential Near Highest Since August 2022

The NZGB 10-year closed 2bps cheaper on the day and 3bps cheaper than pre-Q2 CPI levels.

- While the headline CPI came in moderately lower than expected, the important domestically driven non-tradeables came in slightly higher than the RBNZ expected.

- Despite today's cheapening, the AU-NZ 10-year yield differential closed near its highest level since August 2022, at -15bps.

- A simple regression of the AU-NZ 10-year yield differential versus the AU-NZ 3-month swap rate 1-year forward (1y3m) differential over the current tightening cycle suggests the differential is still 6bps too low versus fair value (i.e., -15bps versus -9bps).

- The 1y3m differential is a proxy for the expected relative policy path over the next 12 months.

Figure 1: AU-NZ Regression: 10-Year Yield Differential Vs. 1Y3M Swap Differential

Source: MNI – Market News / Bloomberg

NZGBS: Cheaper Despite Moderating Core Inflation

NZGBs closed on a weak note, with yields 2-3bps higher on the day and 3-5bps higher than pre-CPI levels.

- Q2 headline CPI came in moderately lower than expected at 0.4% q/q with the annual rate easing to 3.3% from 4%. It is now approaching the top of the 1-3% RBNZ target. The RBNZ had forecast 0.6% q/q and 3.6% in May.

- The important domestically-driven non-tradeables are moderating but came in slightly higher than the RBNZ expected and is unlikely to be enough for them to ease at the August 14 meeting, which is likely to be when it chooses to communicate rather than move.

- The RBNZ’s measure of core inflation from its sectoral factor model moderated to 3.6% y/y in Q2 from 4.2%, the lowest since Q3 2021 but still above the central bank’s 1-3% band.

- Swap rates closed 2-3bps higher, with the 2s10s curve flatter.

- RBNZ dated OIS pricing is little changed across meetings. Nevertheless, OIS pricing sits 18-44bps softer for meetings beyond August versus pre-RBNZ Decision levels. By year-end, a cumulative 65bps of easing is factored into the pricing.

- The local calendar is empty tomorrow.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$225mn of the 4.25% May-34 bond and NZ$50mn of the 2.75% Apr-37 bond.

NEW ZEALAND DATA: Core Inflation Moderating, Non-Tradeables Stubbornly High

The RBNZ’s measure of core inflation from its sectoral factor model moderated to 3.6% y/y in Q2 from 4.2%, the lowest since Q3 2021 but still above the central bank’s 1-3% band. It has moderated more than 2pp over the last year but remains above the pre-Covid series average of 2.1% (to 1993). The RBNZ will be reassured that underlying price pressures are easing and more confident that inflation will sustainably return to target. We believe though that it will want to see Q3 CPI on October 16 before cutting rates.

- Both core tradeables and non-tradeables moderated but as with headline inflation, the bulk of the work was done by the former rising only 0.8% y/y.

- Underlying non-tradeables inflation moderated to a still high 4.8% y/y in Q2 from 5.1% in Q1 and its peak of 5.5% a year ago. It remains uncomfortably above the pre-Covid series average of 3.1% and the RBNZ is likely to want to see it a lot closer to that mark.

Source: MNI - Market News/RBNZ

NZ STIR: - RBNZ Dated OIS Prices 65bps Of Cuts By Year-End

RBNZ dated OIS pricing is little changed across meetings, after today’s Q2 CPI data.

- Nevertheless, OIS pricing sits 18-44bps softer for meetings beyond August versus pre-RBNZ Decision levels.

- By year-end, a cumulative 65bps of easing is factored into the pricing.

Figure 1: RBNZ Dated OIS Post-RBNZ Versus Pre-RBNZ Levels (%)

Source: MNI – Market News / Bloomberg

FOREX: NZD Bounces On Sticky Domestic Inflation, But AUD/NZD Supported On Dips

An NZD bounce has been the main focus in Asia Pac markets today, which came post firmer than expected domestic inflation pressures. The BBDXY sits little changed, last near 1251.5, as the major haven't shifted greatly against the USD.

- NZD/USD last tracked near 0.6070, slightly off session highs (0.6082), but around 0.35% higher. Recent lows are marked just under 0.6040. The Q2 inflation report was a mixed bag, with weaker headline relative to expectations, while non-tradables eased but not as much as the market and the RBNZ projected (0.9% versus 0.8% forecast).

- The RBNZ’s measure of core inflation from its sectoral factor model moderated to 3.6% y/y in Q2 from 4.2%, the lowest since Q3 2021 but still above the central bank’s 1-3% band.

- The AUD/NZD cross fell to lows of 1.1073, but sits back at 1.1100 in recent dealings. As we noted in this piece here, there is risks of divergence between Aust and NZ CPI reads. Recent highs in the cross rest at 1.1152. AUD/USD has risen a touch, last near 0.6740.

- USD/JPY has been steady for much of the session, last near 158.35, close to end levels from NY trade Wednesday.

- In the cross asset space, US equity futures are lower, off 0.15-0.30%, with Nasdaq futures underperforming. US yields sit a touch higher, led by the front end, but this is only recouping modest losses from Tuesday trade in the US.

- A wide ranging interview by US Presidential Candidate Trump (given to BBG) stated Fed Chair Powell would serve his full term, although Trump warned against cutting cuts ahead of the US election in November.

- Looking ahead, we have UK inflation and a speech from the new UK PM. US data and more Fed speak is also out.

ASIA STOCKS: HK & China Equities Head Lower As Market Await Third Plenum Update

China & Hong Kong's equity markets are off earlier highs, after reports that Biden was looking into trade restrictions on companies that provide advanced semiconductors technology to China, growing odds that Trump will win the upcoming election and finally the market is also awaiting policy announcements from the China's Third Plenum.

- Hong Kong equities are mixed today, the HSTech Index is 0.90% higher and now 1.50% higher over the past week. Meanwhile, property stocks are performing well with the Mainland Property Index 2.86% and the HS Property Index is 1.30%, the wider HSI is little changed.

- China equity markets are lower today with the CSI 300 is 0.20% lower, small-cap indices are lower today with the CSI 1000 down 0.50% and the CSI 2000 down 1%, the growth focused ChiNext is 0.44% higher, while a less closely followed index the Beijing SE 50 Index has surged 5.90%, this Index tracks small to medium high growth tech stocks.

- JD Vance, named as Donald Trump’s running mate and Vice President has emphasized China as America's biggest threat in a recent Fox News interview. Vance stated that a Trump administration would focus on China rather than the war in Ukraine, proposing negotiations to end the conflict in Ukraine to concentrate on the Chinese threat. This underscores the likely hawkish stance of their administration towards Beijing if elected.

- Looking ahead, focus will again be on any headlines from the Third Plenum policy meetings.

ASIA PAC STOCKS: Asia Stocks Mixed, Semiconductors Hit On Biden's Trade Restrictions

Asian equities are mixed today, the moves have been driven by optimism that the Federal Reserve will soon cut interest rates with the markets now pricing a 100% chance of a cut in September, leading to a surge in riskier market segments. The MSCI Asia Pacific Index rebounded from a three-day decline, buoyed by fresh highs in U.S. shares, although gains were moderated by sell off this afternoon in Japanese stocks following U.S. warnings of stricter trade rules with China. Despite geopolitical concerns over a potential Trump presidency, the overall sentiment was positive, with rising expectations for rate cuts and supportive economic data boosting confidence.

- Japanese equities are off earlier highs after reports that the Biden administration is considering stringent trade restrictions on companies like Tokyo Electron if they continue providing advanced semiconductor technology to China. Tokyo Electron which makes up about 2.80% of the Nikkei 225 dropped as much as 7.6%, with the weakness confined to the chip sector. However, the broader market remained focused on the positive prospects of U.S. interest rate cuts and a potential economic soft landing. The Nikkei 225 is 0.25% lower, while the wider Topix is 0.38% higher.

- South Korean stocks are lower today as investors have looked to take profits after two days of gains. Major tech and automotive stocks like Samsung Electronics and Hyundai Motor saw declines. Conversely, SK Innovation surged 7.15% on merger news, while Korean shipbuilder stocks have surged to multi-year highs driven by expectations of strong second-quarter earnings and US industrial gains amid rate-cut bets. The Kospi is 0.60% lower, while the Kosdaq trades 0.50% lower.

- Taiwan equities are lower this morning, recently foreign investors have been heavy sellers of Taiwan equities with an outflow of $2.2b over the past week, the TWD is weaker on the back of this selling and currently sits back near two week lows. TSMC is also lower after Biden announced potential tariffs on semiconductors names and Trump questioning if it's the US duty to protect Taiwan. The Taiex is 1.23% lower.

- Australian equities are higher today, and mirror the rally in US equities overnight. The ASX200 is up 1% and is back above 8,000. Miners led the gains, supported by gold reaching its highest price ever and details from BHP’s quarterly production report.

- New Zealand equities are higher today, after Q2 headline CPI came in moderately lower than expected at 0.4% q/q with the annual rate easing to 3.3% from 4%. Overnight GDT price index rose 0.40%, with strong performance in "fats" which offset a fall in "powders". The NZX 50 is up 0.76%

- Elsewhere, Singapore equities are 0.10% higher, Malaysian equities are 0.65% higher, Indonesian equities are are little changed while Philippines equities are 0.50% lower.

ASIA EQUITY FLOWS: Foreign Investors Continue Selling Taiwan Equities

- South Korea: South Korean equities saw inflows of $72m yesterday, contributing to a net inflow of $541m over the past five trading days. The 5-day average inflow is $108m, slightly lower than the 20-day average of $162m but higher than the 100-day average of $122m. Year-to-date, South Korea has experienced substantial inflows totaling $19.61b.

- Taiwan: Taiwanese equities had significant outflows of $267m yesterday, resulting in a net outflow of $2.22b over the past five trading days. Recent trend in Taiwan equities is negative and is the worst market in the region, flows could be linked to profit taking in TSMC after the stock has rally 80% this year, and concerns around what a Trump Presidency will have on the local market. The 5-day average flow is -$444m, considerably lower than the 20-day average of -$147m and the 100-day average -$25m. Year-to-date, Taiwan has accumulated inflows of $1.65b.

- India: Indian equities experienced inflows of $399m Monday, contributing to a net inflow of $1.52b over the past five trading days. The 5-day average is $306m, similar to the 20-day average of $302m and significantly higher than the 100-day average of -$41m. Year-to-date, India has seen net inflows of $3.04b.

- Indonesia: Indonesian equities recorded outflows of $33m yesterday, resulting in a net inflow of $79m over the past five trading days. The 5-day average is -$16m, below the 20-day average inflow of $14m and the 100-day average -$7m. Year-to-date, Indonesia has experienced outflows totaling $194m.

- Thailand: Thai equities saw outflows of $2m yesterday, contributing to an outflow of $86m over the past five trading days. The 5-day average is -$17m, slightly better than the 20-day average -$27m and the 100-day average of -$25m. Year-to-date, Thailand has seen significant outflows amounting to $3.35b.

- Malaysia: Malaysian equities experienced inflows of $14m yesterday, contributing to a 5-day net inflow of $176m. The 5-day average inflow is $35m, higher than the 20-day average inflow of $5m and the 100-day average outflow of -$2m. Year-to-date, Malaysia has experienced minor inflows totaling $97m.

- Philippines: Philippine equities saw inflows of $5m yesterday, with a 5-day net inflow of $6.5m. The 5-day average inflow is $1m, better than the 20-day average outflow of -$1m and the 100-day average outflow of -$7m. Year-to-date, the Philippines has seen outflows totaling $514m.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | 72 | 541 | 19606 |

| Taiwan (USDmn) | -267 | -2222 | 1651 |

| India (USDmn)* | 399 | 399 | 3044 |

| Indonesia (USDmn) | -33 | 79 | -194 |

| Thailand (USDmn) | -2 | -86 | -3354 |

| Malaysia (USDmn) | 14 | 176 | 97 |

| Philippines (USDmn) | 5 | 6.5 | -514 |

| Total | 189 | -1107 | 20335 |

| * Up to 15th July |

OIL: Crude Little Changed, EIA US Inventory Data Out Later

Oil prices are little changed after falling over a percent on Tuesday. Data showing another US crude inventory drawdown has been unable to lift markets. WTI is down 0.1% to $80.69/bbl after falling to $80.45 and Brent is -0.1% to $83.66 after $83.43. The stronger US dollar weighed on crude yesterday but today the USD index is flat.

- Bloomberg reported that US crude inventories fell 4.44mn after a 1.9mn barrel drawdown the previous week, according to people familiar with the API data. Gasoline rose 365k and distillate 4.92mn. The official EIA data is released later today and another decline would be the third in a row.

- After OPEC reported in its July report that the group had produced above its quota in June, Russia has said that it will reduce output further during the summer given it hasn’t met its commitment.

- Later the Fed’s Barkin and Waller both speak on the economy and the Beige Book is published. June UK CPI and final June euro area CPI print, as well as US June housing and IP data.

GOLD: Fresh All-Time High

Gold is steady in the Asia-Pac session, after hitting a fresh all-time high of $2482.42.

- Bullion closed 1.9% higher at $2469.08 on Tuesday, as traders placed stronger bets on Federal Reserve rate cuts this year and weighed an uncertain outlook for US politics.

- Lower rates are typically positive for gold, which doesn’t pay interest.

- US Treasuries finished near session bests on Tuesday with the long-end out-performing. The US 10-year yield finished 7bps lower at 4.16% versus a 4bp drop for the US 2-year to 4.42%. The early session sell-off following stronger-than-expected US Retail Sales data was completely reversed.

- Retail sales printed flat (-0.02% unrounded) growth m/m, slower than the +0.3% registered in May (upward rev from 0.1%), but above the -0.3% expected. Sales ex-autos (+0.4% vs 0.1% expected) and ex-auto/gas (+0.8% vs +0.2% expected) beat and with higher revisions.

- Gold has rallied by over 50% since late 2022, underpinned by demand from central banks, to diversify reserves and reduce their reliance on the US dollar.

- According to MNI’s technicals team, the breach of the bull trigger suggests technical conditions remain firmly in bullish territory.

CHINA RATES: OMO Injections Continue, PBoC Reportedly Monitoring Bank Bond Positions

The PBOC injected CNY270bn via reverse repo today, which follows yesterday's ample injection, as tax payment season drains liquidity.

• The 7 day weighted average interbank repo rate for depository institutions fell to 1.81% this morning

• The PBOC continues to maintain a cautious stance on bond markets following the ongoing move lower in yields recently. BBG noted earlier that the central bank is questioning banks on their bond holdings, as it continues to monitor developments in this space (see this link).

• Overnight moves across shorter to intermediate maturities moved lower in line with global trends.

• The move lower was not as rapid as other developed markets, most likely reflecting the ongoing impact of government policies

• 2 year yield decline 1.4bps to 1.59%

• 10 year yield declined 1.7bps to 2.253%

• 30 year yield declined 2.3bps to 2.461%

• With limited key data releases this week, the bond market will likely ebb and flow on global market movements and policy impacts (as per above), while we also await Third Plenum details.

ASIA RATES: Asia Sovs Little Changed, BI Rate Decision Shortly

Asian EM sovs are mostly steady today, INDON is outperforming PHILIP curve as we await the BI rate decision due out a bit later today.

- Bank Indonesia meet for the July rate decision and will likely keep the key rate at 6.25% as inflation remains well within the 1.5-3.5% band and the rupiah has strengthened since the last meeting. However, FX stability will remain the central bank's focus and rates are likely to be unchanged until the Fed eases and the IDR has strengthened further and consistently.

- See MNI's BI Preview here

- The INDON curve has bull-steepened since the last BI rate decision on June 20, with yields -20bps to +2bps , while the IDR is 1.90% higher over the same period.

- The PHILIP curves has underperformed the INDON over the past month, with yields 5-15bps lower, there has been better buying through the 5-7yr part of the curve. We are little changed today.

- The PH-US 5yr spread is trading towards the widest levels since early 2023, while the ID-US 5yr spread is trading back at June levels.

- Cross-asset: Ahead of BI today the USD/IDR is 0.33% lower at 16,127, while the USD/PHP is little changed at 58.364. In equities the JCI is unchanged, while the PSEi is down 0.50%.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/07/2024 | 0600/0700 | *** |  | UK | Consumer inflation report |

| 17/07/2024 | 0600/0700 | *** | | UK | Producer Prices |

| 17/07/2024 | 0900/1100 | *** |  | EU | HICP (f) |

| 17/07/2024 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 17/07/2024 | 1030/1130 | | UK | King's Speech | |

| 17/07/2024 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 17/07/2024 | 1230/0830 | * |  | CA | International Canadian Transaction in Securities |

| 17/07/2024 | 1230/0830 | *** | | US | Housing Starts |

| 17/07/2024 | 1300/0900 | | US | Richmond Fed's Tom Barkin | |

| 17/07/2024 | 1315/0915 | *** | | US | Industrial Production |

| 17/07/2024 | 1335/0935 | | US | Fed Governor Christopher Waller | |

| 17/07/2024 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 17/07/2024 | 1700/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 17/07/2024 | 1800/1400 | | US | Fed Beige Book |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.