Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

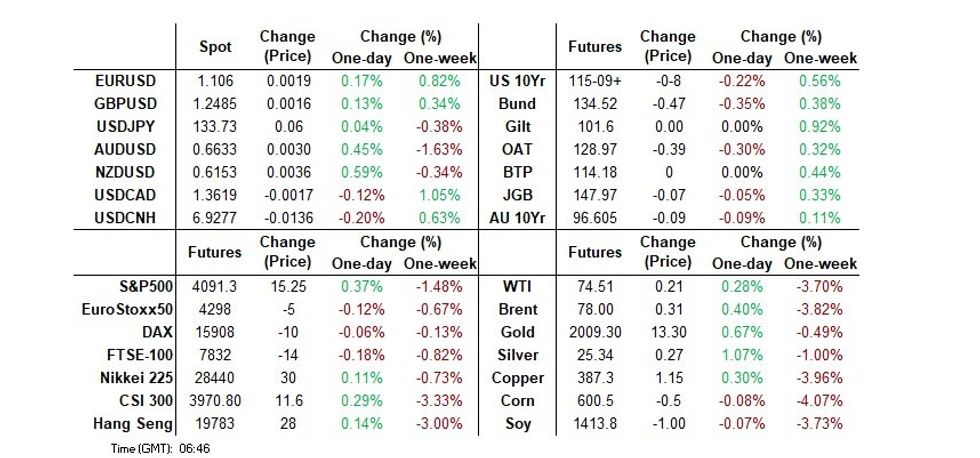

- Asia Pac equities are mixed, with the major indices not showing definitive trends through the course of the session.

- Kiwi is the best performer in the G-10 FX space.

- On the wires today we have Eurozone Consumer Confidence, Advance US GDP and Initial Jobless Claims.

MNI BoJ Preview - April 2023: No Change, But A Possible Assessment Of Longer Term Settings

EXECUTIVE SUMMARY

- We lean heavily towards the consensus no change view when it comes to the BoJ’s major policy parameters at the end of Governor Ueda’s first meeting atop the central bank. This is owing to the relatively short period of time that has elapsed since Ueda took up his new post, existing BoJ forward guidance, the underlying BoJ view on inflation and continued jitters surrounding the U.S. banking sector. There may be a tweak to the forward guidance, removing the reference to COVID-19, but that shouldn’t be viewed as substantial, if it is indeed forthcoming.

- When it comes to the next YCC tweak (we flag July’s meeting as a potential staging post for that event, given that it will coincide with the release of the next outlook report, although many on the sell-side favour June) we shouldn’t necessarily expect overt signalling ahead of time, with Ueda already revealing that he is open to the idea of deploying a surprise policy move in certain instances.

- We should probably expect Ueda to be a little more balanced than his ultra-dovish predecessor in the post-meeting press conference, although his communication to date has generally presented a more dovish outlook than most assumed would be the case when he was nominated for the role. Ueda’s oratory skills were flagged as a major positive by the government, seemingly playing a key part in his nomination.

- Click to view full preview.

US TSYS: Curve Marginally Steepens In Asia

TYM3 deals at 115-15, -0-02+, with an observed 0-05 range on volume of ~53k

- Cash tsys sit 1.5bps richer to flat across the major benchmarks, light bull steepening has been observed.

- Tsys were richer in early dealing as Asia participants faded Wednesdays moderate cheapening perhaps using the opportunity to enter fresh long positions/close out shorts.

- A block trade in FV, 2k lots, added an additional level of support and tsys marginally extended gains.

- There was little follow through on the move higher and gains were marginally pared.

- Little meaningful macro news flow crossed through the session.

- There is a thin data calendar in Europe today, with the final read of Eurozone Consumer Confidence providing the highlight. Further out we have Advance US GDP and Initial Jobless Claims. We also have the latest 7 Year Supply.

JGBS: Futures Sitting Mid-Range, Push Off Overnight High

JGB futures are currently sitting in the middle of their range, -2 compared to settlement levels. This afternoon, JGB futures experienced some cheapening, likely due to the reversal of early Asia-Pacific strength in US Tsys.

- The JBM3 is currently trading at 148.02, which is higher than the range of 147.40-147.92 that it has been trading in since early April. Attention remains on 149.53, the March 22 high, according to MNI’s technical analyst.

- With few domestic drivers today, the local market has traded in a tight range ahead of the BoJ Decision tomorrow. The consensus view is that there will be no major policy changes due to Governor Ueda's recent appointment, existing BoJ forward guidance, the BoJ's view on inflation, and concerns about the US banking sector. There may be a small change to forward guidance by removing the reference to COVID-19.

- Cash JGBs twist steepen pivoting at the 7-year zone with yields -0.7bp lower to 0.5bp higher. The benchmark 10-year yield is flat at 0.465%, below the BoJ's YCC limit of 0.50%.

- Swap spreads are wider across the curve with the swaps curve bear steepening.

- The local data calendar sees the release of Tokyo CPI, Retail Sales and Industrial Production tomorrow, ahead of the BoJ Policy Decision.

JAPAN: Biggest Week Of Net Selling Of International Bonds Since October Lodged Last Week

Weekly international security flow data from the Japanese MoF reveals the most sizable round of net selling recorded since October re: international bonds on the part of Japanese investors. This isn’t a surprise, given the investment outlines provided by the major Japanese life insurers and pension companies in recent days.

- The 3 remaining major metrics in the dataset revealed marginal net buying, with the recent runs of net purchases of Japanese equities on the part of international investors and net purchases of international equities on the part of Japanese investors extending to 4 consecutive weeks, respectively.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | -1059.5 | 502.5 | -1829.1 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | 173.1 | -65.3 | 527.4 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | 41.6 | 9.2 | 2305.5 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | 342.9 | 1876.1 | 4650.1 |

AUSSIE BONDS: Weaker, At Cheaps, Tracking US Tsys

ACGBs sit weaker (YM -4.0 & XM -5.0) at or near session cheaps as US Tsys pare early Asia-Pac strength. Without any tier-one economic data or meaningful headlines, the local market appeared happy to track US Tsys.

- Cash ACGBs are 4-5bp cheaper with the AU-US 10-year yield differential unchanged at -10bp.

- Swap rates are 3bp higher with EFPs 1bp tighter.

- Bills pricing is -4 to -5 across the strip.

- RBA dated OIS pricing is flat to 3bp firmer across meetings with November leading.

- Trade data surprised on the upside with Export Prices +1.6% Q/Q and Import Prices -4.2% Q/Q versus expectations of -2.6% and +0.5% respectively.

- NSWTC priced today A$2.5bn of the new 4.25% 20 February 2036 benchmark bond via syndication after yesterday's launch. Joint lead managers for the transaction were Commonwealth Bank of Australia, UBS and Westpac.

- The local calendar is relatively light ahead of the RBA Decision Meetings on Tuesday with the release of Private Sector Credit and PPI data tomorrow as the highlights.

- Accordingly, the local market will likely seek guidance from US Tsys through the release of Q1 GDP later today and the March PCE Deflator tomorrow.

NZGBS: Weaker, Off Cheaps, Outperforms $-Bloc

NZGB benchmarks closed 2-3bp higher, off session cheaps, after weekly supply showed decent demand (cover ratios of 3.34-3.74). Yields were as much as 1.5bp lower post-auction. NZ/US and NZ/AU 10-year yield differentials both closed 2bp tighter.

- Swap rates closed 5-6bp higher with implied swap spreads wider.

- RBNZ dated OIS closed flat to 3bp firmer across meetings.

- Prime Minister Chris Hipkins, in a pre-Budget speech, has announced that the government will not impose a levy to pay for the recovery from recent natural disasters. The estimated costs of these disasters are between NZ$9-14.5bn, and the government will fund the recovery through a combination of operating and capital allowances, savings, reprioritizations, and some debt. The upcoming budget (May 18) will not introduce any major new taxes, such as a wealth tax or capital gains tax.

- ANZ business activity indicators remained stable in April while inflation signals decreased, indicating progress for the RBNZ. However, a significant percentage of firms continue to experience high costs and intend to raise prices, suggesting that the RBNZ has more work to do.

- With the Antipodean calendar light for the remainder of the week, the local market will likely be guided by US Tsys as they navigate Q1 GDP later today and the March PCE Deflator tomorrow.

NEW ZEALAND: ANZ Business Survey Shows Elevated But Moderating Inflation Pressures

ANZ business confidence in April was down only slightly from March at -43.8 from -43.4, but remains more optimistic than the trough in December. The activity outlook however rose to -7.6 from -8.5, the best result since October but still lacklustre. The April results were fairly stable despite the unexpected 50bp RBNZ rate hike at the start of April. ANZ interprets the price data as moving as the RBNZ would have expected, moderating but still elevated. Thus another hike on May 24, in line with RBNZ forecasts, is possible.

- ANZ points out that cost expectations remain very high at 84.2, which could limit the downside to inflation going forward. Neither of these indicators is moving as the RBNZ would hope at this stage of the tightening cycle. On the other hand, pricing intentions moderated to 53.7 from 56.8, which are still high but the lowest since early 2021, and inflation expectations eased to 5.7% from 5.8%.

- Employment intentions rose to -2.4 from -4.6, the highest since October but the sixth consecutive negative. Wage rise expectations were already elevated and rose further in April to 87.2%, but down from 94% in mid-2022. Past wage settlements were almost unchanged at 6% and expectations for the next year moderated slightly to 4.7% from 4.8%, which is well off the peak in 2022.

- All sectors were pessimistic but retail and agriculture less so and construction and services more so.

Source: MNI - Market News/Refinitiv

FOREX: NZD Firmer In Asia, Moves Limited Elsewhere

Kiwi is the best performer in the G-10 space at the margins on Thursday. NZD/USD is ~0.3% firmer. Elsewhere in G-10 moves have been limited with little follow through.

- NZD/USD prints at $0.6130/35, the pair has firmed through today's Asian session after printing a 6 week low yesterday. NZ Treasury noted that recent floods and cyclone events will add 0.4% to Q1 and Q2 inflation.

- AUD/USD is ~0.1% firmer, the pair has consolidated in a narrow above $0.66 handle on Thursday. Q1 Export prices rose 1.6%, fall of 2.6% Q/Q had been expected and Import prices fell -1.2% Q/Q a rise of 0.3% had been expected.

- Yen is little changed from yesterday's closing levels. USD/JPY has dealt in a narrow 30 pip range for the most part, last printing at ¥133.65/75. Support comes in at ¥133.09 low from Apr 26, Resistance is at ¥134.47 high from Apr 25.

- Elsewhere in G-10 the greenback is a touch pressured, BBDXY is down ~0.1% however there has been little follow through on moves thus far.

- Cross asset wise; E-minis are ~0.2% firmer and US Treasury Yields are little changed across the curve.

- On the wires today we have Eurozone Consumer Confidence, Advance US GDP and Initial Jobless Claims.

AUD: A$ Correlations - Commodities Back In The Drivers Seat

AUD/USD correlations have swung back in favor of traditional drivers over the past week. The table below shows AUD/USD levels correlations with a number of key macro drivers for the past week and month. Note yield spreads are based off government bond yield spreads.

- Correlations are sharply lower with yield differentials over the past week. This fits with A$ performance, as the currency has weakened, even as yield differentials have improved (the AU-US 2yr back to -92/-93bps, versus recent lows around -117bps).

- Note though with next week's RBA decision on Tuesday, rate differentials could re-assert themselves as an AUD driver, as has historically been the case.

- Correlations with global commodity prices have rebounded sharply. The headline Bloomberg commodity index is back to late March lows and has weighed on the AUD. Base metals are at even weaker levels.

- The correlation with iron ore is also higher, albeit still sub 50% for the past week.

- Correlations are also firmer with global equities and the VIX over the past week, but remain below longer term averages for the past month.

Table 1: AUD/USD Correlations - Levels

| 1wk | 1mth | |

| AU-US 2yr Spread | -0.38 | 0.01 |

| AU-US 5yr Spread | -0.05 | 0.03 |

| AU-US 10yr Spread | 0.10 | 0.08 |

| Global Commodities | 0.96 | 0.43 |

| Global Base Metals | 0.97 | 0.59 |

| Iron ore | 0.31 | 0.52 |

| Global equities | 0.91 | 0.36 |

| US VIX index | -0.87 | -0.25 |

Source: MNI - Market News/Bloomberg

FX OPTIONS: Expiries for Apr27 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0750(E1.1bln), $1.0830(E635mln), $1.0900(E723mln), $1.0975(E585mln), $1.1000(E779mln), $1.1040(E1.1bln), $1.1125-26(E650mln)

- USD/JPY: Y135.00($1.2bln)

- GBP/USD: $1.2390-10(Gbp743mln), $1.2425-39(Gbp633mln)

- USD/CAD: C$1.3565-80($1.0bln)

- USD/CNY: Cny6.9500-20($770mln)

SOUTH KOREA: Further Improvement In Business Sentiment, But Detail Less Upbeat

Earlier today South Korean manufacturing and non-manufacturing sentiment improved further in terms of May readings. Manufacturing edged up to 72 in terms of the headline (from 69). Non-manufacturing is at 76 versus 75 prior.

- For manufacturing, this is only back to levels from late 2022, but is trending in the right direction. The first chart below overlays this headline index against y/y GDP growth. Much like yesterday's improved consumer sentiment result, today's reading is suggesting better y/y GDP momentum in the quarters ahead.

- The seasonally adjusted series for manufacturing showed less improvement though, albeit ticking higher to 68.

Fig 1: Manufacturing Sentiment Versus Y/Y GDP

Source: MNI - Market News/Bloomberg/BoK

- The non-manufacturing reading is also back to late 2022 levels, but in an absolute sense remains at higher levels relative to manufacturing. The seasonally adjusted reading nudged down though, printing at 73.

- In terms of the detail, on the manufacturing side, there was a decent pick up in sales expectations and new orders, although this looked more orientated towards the domestic side of the economy.

- Export expectations only improved a touch, and isn't suggesting a sharp rebound in export growth, see the second chart below.

Fig 2: Manufacturers Export Expectations Versus Exports Y/Y

Source: MNI - Market News/Bloomberg/BoK

EQUITIES: Mixed Trends In Asia Pac, Higher Nasdaq Futures Aid Tech Sensitive Plays

Asia Pac equities are mixed, with the major indices not showing definitive trends through the course of the session. HK/China shares are modestly higher. US futures are once again firmer, led once again by the tech side, with Nasdaq futures around +0.60% higher at this stage, buoyed by better earnings guidance from Meta late on Wednesday in the US.

- The CSI 300 is +0.11% at this stage, still comfortably below the 200-day MA, but showing some signs of stability. The index was weaker in earlier trading. Strength has been evident in the insurance sector on better earnings.

- The HSI is a touch higher, despite negative headwinds from the tech sub-index (last -0.84%).

- Singapore stocks are down 0.50%, weighed by the property sector, as the government announced it was increasing stamp duty for second home buyers and foreigners purchasing local property.

- The Kospi and Taiex are firmer by 0.25-0.35% respectively. Positive Nasdaq futures are helping, with Korean markets recovering from earlier losses after Samsung's Q1 earnings disappointed.

- The ASX 200 is down 0.50%, an underperformer as local banks struggled. The Topix is up 0.25% at this stage.

- In SEA Thai stocks are down over 1%, while Indonesia stocks are +0.80%, continuing yesterday's solid rebound. Hopes of positive earnings momentum the driver of the JCI.

GOLD: Bullion Higher As Fed Pause Expectations Grow Given Latest Banking Woes

Gold has continued to struggle to hold onto gains above $2000/oz. Today during APAC trading it has risen through that level but is currently trading just below. Gold is up 0.5% to $1999.182, close to the intraday high of $2000.96, after falling 0.4% on Wednesday despite the USD index also dropping 0.4%.

- Gold has benefited from flight to quality flows today as speculation grew that the Fed will have to pause given the most recent US banking troubles. Today and tomorrow’s data should be key in shaping the Fed outlook.

- First Republic’s earnings were significantly worse than expected and US regulators are now considering whether to impose borrowing restrictions on the troubled bank, according to Bloomberg.

- Later there is important US Q1 GDP data which is expected to rise 1.9% q/q saar. The price components are also likely to be watched closely and the core PCE price index is forecast to rise 4.7% q/q saar – more than Q4’s 4.4%. There are also jobless claims and pending home sales for March.

OIL: Crude Stabilises But Struggling With Global Uncertainties

Oil prices have stabilised during APAC trading today after slumping around 3.5% on Wednesday, supported by more positive equity sentiment as S&P e-minis increase 0.3%. WTI is flat at $74.40/bbl while Brent is 0.3% higher to $77.90. The USD index is down slightly.

- Prices are about 4.5% lower this week, as crude has struggled given renewed concerns around the US banking system and the possible impact it will have on US and global growth. The market has also become less worried about supply following shipping indicators pointing to robust Russian exports. Today and tomorrow’s US data are likely to influence oil prices given that they should be key in shaping the Fed outlook.

- Declining refining margins and uncertainty regarding the economic situation in China, the Fed outlook and output from Russia continue to dampen oil prices.

- Later there is important US Q1 GDP data which according to Bloomberg is expected to rise 1.9% q/q saar. The price components are also likely to be watched closely and the core PCE price index is forecast to rise 4.7% q/q saar – more than Q4’s 4.4%. There are also jobless claims and pending home sales for March and the European Commission survey for April.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 27/04/2023 | 0700/0900 | ** |  | SE | Economic Tendency Indicator |

| 27/04/2023 | 0800/1000 | ** |  | IT | ISTAT Business Confidence |

| 27/04/2023 | 0800/1000 | ** | | IT | ISTAT Consumer Confidence |

| 27/04/2023 | 0900/1100 | ** |  | EU | EZ Economic Sentiment Indicator |

| 27/04/2023 | 1100/0700 | * |  | TR | Turkey Benchmark Rate |

| 27/04/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 27/04/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 27/04/2023 | 1230/0830 | * |  | CA | Payroll employment |

| 27/04/2023 | 1230/0830 | *** | | US | GDP |

| 27/04/2023 | 1400/1000 | ** | | US | NAR Pending Home Sales |

| 27/04/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 27/04/2023 | 1500/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 27/04/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 27/04/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 27/04/2023 | 1615/1815 | | EU | ECB Panetta at EACB Board Meeting | |

| 27/04/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

| 27/04/2023 | 1700/1300 | * | | US | US Treasury Auction Result for Cash Management Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.