Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- The BoJ played a straight bat and left its core monetary policy settings unchanged, matching the view of almost all sell-side economists, albeit being at odds with the recent, well-documented developments in Japanese markets. There was a tweak to the BoJ’s "Principal Terms and Conditions for Funds-Supplying Operations against Pooled Collateral," allowing it to “determine the duration of each loan taking account of conditions in financial markets and the duration shall not exceed ten years.” This was seemingly a bid to promote market functioning and further backstop its YCC settings that it seems keen to stick with, at least for now (the BoJ promptly deployed a 5-Year loan in the afternoon).

- JGBs firmed accordingly, driving a bid in core global FI, but finished off best levels, while the JPY came under notable pressure in FX trade, given the pre-BOJ speculation.

- Coming up, UK CPI for Dec prints, while the final Eurozone CPI is for Dec also slated. There is a busy data schedule in the U.S. today with the focus likely to be retail sales and PPI. Elsewhere, we will get a raft of comments from various Fed speakers, ECB's Villeroy and BoJ Governor Kuroda.

US TSYS: Richer, BoJ-Related Flows Dominate

TYH3 deals at 114-29+, +0-08, as it retreats from the top of a 0-20 range, on very strong volume of ~259K.

- Cash Tsys are running 2-6bp richer across major benchmarks, with 7s and 10s leading the bid.

- Any early round of modest cheapening was observed in Asia trade, in the absence of any headline driver there was perhaps some pre-BoJ positioning in Tsys (albeit with JGB futures bid).

- Tsys then firmed in the immediate aftermath of the BoJ decision, as the Bank left all major policy parameters unchanged. The BoJ's decision was in line with the view of most economists, although it was at odds with well-documented JGB market pricing.

- JGBs are off best levels late in Tokyo trade, facilitating a similar move in Tsys.

- In Europe today CPI data from the UK and the Eurozone (final) provide the highlights. Further out we have a slew of US data including Retail Sales, PPI and Industrial Production as well as the Fed' s Beige Book. There will be Fedspeak from Atlanta Fed President Bostic, Philadelphia Fed President Harker and St Louis Fed President Bullard. We also have the latest round of 20-Year supply and a meeting between Yellen & Liu He.

JGBS: Futures Lead Post-BoJ Bid, As The Bank Sticks With YCC Settings

The BoJ played a straight bat and left its core monetary policy settings unchanged, matching the view of almost all sell-side economists, albeit being at odds with the recent, well-documented developments in Japanese markets.

- There was a tweak to the BoJ’s "Principal Terms and Conditions for Funds-Supplying Operations against Pooled Collateral," allowing it to “determine the duration of each loan taking account of conditions in financial markets and the duration shall not exceed ten years.” This was seemingly a bid to promote market functioning and further backstop its YCC settings that it seems keen to stick with, at least for now (the BoJ promptly deployed a 5-Year loan in the afternoon).

- The decision was backed by 9-0 votes across the board, with forward guidance also unchanged.

- When it comes to the Bank's underlying CPI projection’s there was a mark higher for the current FY, along with some tweaks further out, but crucially, there was no indication that the Bank expects to achieve its inflation target over the medium term (although it may be a little more confident of doing so, based on the adjustments).

- This triggered a notable firming in JGBs, with futures +130 ticks into the bell, ~50 ticks off best levels, while cash JGBs run flat to 11bp richer on the day with 7s leading the bid owing to the move in futures. The super-long end lagged but unwound the morning cheapening (which was seemingly linked to flattener unwinds pre BoJ). 10-Year JGB yields are set to close around 0.42%, after once again printing above the BoJ’s YCC cap (0.50%) ahead of the monetary policy decision. 10-Year swap rates are 12bp lower on the day, printing at 0.78%, extending the pullback from last week’s foray above 1.00%.

- Governor Kuroda’s post-meeting press conference will start in just under 30 minutes.

AUSSIE BONDS: Unchanged BoJ Triggers About Face In ACGBs, Bull Flattening On The Day

The BoJ’s choice to leave its YCC parameters unchanged, despite market speculation to the contrary (even though the majority of the sell-side economists looked for no change in monetary policy settings, with varying degrees of conviction) put a bid into ACGBs on Wednesday.

- That left YM +4.0 & XM +6.0 at the bell, with the early bear steepening impulse (derived from wider core global FI trade on Tuesday) flipping to bull flattening. The major cash ACGB benchmarks run 4-6bp richer, with the 7- to 12-Year zone outperforming on the curve.

- The early EFP narrowing reversed on the move, suggesting that bonds led the swings in both directions.

- Bills finished 1-3bp firmer through the reds, once again reversing the overnight/early Sydney cheapening. RBA dated OIS was little changed on the day, showing ~20bp of tightening for next month’s gathering and a terminal cash rate of somewhere between 3.70-3.75%.

- Looking ahead, the monthly labour market report and consumer inflation expectations print headline local matters on Thursday.

NZGBS: BoJ Sees Space Away From Session Cheaps, Swaps Flat To Lower

NZGBs richened into the close, with the lack of movement in the BoJ’s YCC settings taking the edge off the early session cheapening. The early move was seemingly linked to the weakness in U.S. Tsys observed into the NY close and perhaps an element of some last minute pre-BoJ positioning in the NZGB market.

- That left the major benchmarks running 2-3bp cheaper at the close, with some very modest bear steepening in play.

- Swap rates followed the general gyrations in NZGBs, albeit with slightly longer trading hours, which allowed a flattening bias to develop, as swap rates finished unchanged to 3bp lower across the curve.

- There could be a further adjustment to the post-BoJ decision moves in early Thursday dealing, but that will be contingent on the global reaction to the matter.

- RBNZ dated OIS is showing 62bp of tightening for next month’s meeting after nearly fully pricing in a 75bp step in recent weeks, while the terminal OCR print shows in familiar territory, between 5.40-5.45%.

- On the local data front, card spending data saw a M/M fall in Dec, while the latest REINZ house price reading pulled lower once again as the impact of the RBNZ’s expeditious tightening cycle continues to filter through.

- Looking ahead, supply in the form of NZGB-28, -32 & -41 is due tomorrow, with food prices and non-resident bond holding data also set to cross.

NEW ZEALAND: Weak Consumption Momentum Going Into 2023

December card spending was weak, likely reflecting the impact of 400bp of tightening. Electronic card transactions fell 1.2% m/m, its second consecutive monthly drop. Retail card transactions fell 2.5% m/m after rising 0.3% in November. Annual growth is now well off of its September peak but still positive. The RBNZ Governor Orr asked people to reduce their spending at his November press conference and it seems that they listened.

- There is a high correlation between retail card transactions and nominal retail sales, which is a quarterly series. Despite a weak end to the quarter, the value of retail transactions rose 1.4% q/q in Q4 2022 suggesting that Q4 retail sales could still post another strong result on February 27 (Q3 +2.5% q/q).

- But the card transactions data indicate that there was weak momentum going into the start of 2023, and that with the sharp drop in December consumer confidence suggests that retail sales could possibly be quite weak in Q1 2023.

Source: MNI - Market News/Refinitiv

NEW ZEALAND: Property Market Continues Correction In Wake Of Higher Rates

REINZ reported a 23.6% m/m drop in property sales in December which is down 39% on December 2021. The median price fell 12.2% annually to NZ$790k. The number of days to sell a property improved by one to 40 days but is still 11 days more than the same time in 2021. The REINZ house price index fell 13.7% annually. The housing market continues to correct and adjust to the 400bp of tightening so far this cycle but the pace has slowed. See report here.

Fig. 1: NZ house price measures y/y%

Source: MNI - Market News/Refinitiv

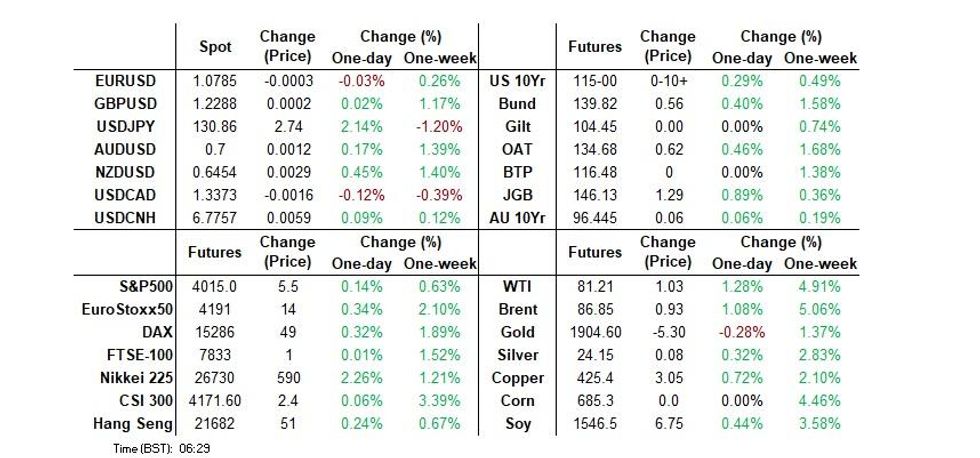

FOREX: USD/JPY Up 2.5% Post BoJ, Eyeing 20-Day EMA Test, NZD Outperforms Elsewhere

USD indices are higher in large part to the 2.5% surge in USD/JPY post today's BoJ outcome. The BBDXY is back to 1230, +0.40% for the session and highs back to Thursday last week. The DXY is up by a similar amount.

- USD/JPY was modestly higher ahead of the BoJ, but still found selling interest ahead of 129.00. Post the meeting, which left all major policy parameters unchanged, we surged higher. Yen bulls will be disappointed there was no further changes, particularly to YCC dynamics. We met some resistance ahead of 131.00, but ultimately pushed close to 131.60. The pair last tracked around 131.45/50.

- The 20-day EMA is not too far away at 131.68, a resistance level we have spent little time above since early November last year. 1 week implied vol is down off highs, last at 16.27%.

- Elsewhere, NZD/USD has outperformed, last tracking close to 0.6450, +0.40% for the session. There haven't been any headline drivers, however yesterday's NZD/USD close above $0.64, which emerged as a key level recently, may be aiding technical flows. Q4 CPI is coming into focus as well, the print is next Wednesday and looms as a key input into February's RBNZ meeting. the AUD/NZD cross has also weakened, back sub the 100 & 200 day Mas this past week.

- AUD/USD is a touch above NY closing levels, last near 0.6990, but is still facing resistance ahead of 0.7000.

- Coming up, UK CPI for Dec prints, while the final EU CPI is due for Dec. There is also a busy data schedule in the US today with the focus likely to be US December retail sales and PPI.

FX OPTIONS: Expiries for Jan18 NY cut 1000ET (Source DTCC)

EUR/USD: $1.2080(E522mln-EUR puts), $1.2100-05(E627mln-EUR puts)

USD/JPY: Y103.50-60($551mln), Y104.15-25($549mln)

EUR/GBP: Gbp0.8840-50(E780mln-EUR puts)

AUD/USD: $0.7345(A$836mln-AUD calls)

ASIA FX: USD/JPY Spike Spills Over, But USD/Asia Pairs Down From Highs

USD/Asia pairs are mostly higher, with some spill over from the spike in USD/JPY post the BoJ. However, moves haven't been uniform, with IDR a notable outperformer and bucking the recent trend of firmer correlations with yen moves. The meeting between China Vice Premier Liu He and US Treasury Secretary Janet Yellen later today will be in focus. Tomorrow both BI and BNM policy decisions are due, with +25bps expected from both central banks.

- USD/CNH continues to trade with a firmer bias, although outside of USD/JPY spill over, profit taking ahead of LNY next week could be a factor. We saw selling interest emerge ahead of the 6.7900 level, with the pair last sub 6.7800.

- 1 month USD/KRW got to a high of 1245.40 post the BoJ, before selling interest emerged. This still leaves us within recent ranges though. The pair is back to the low 1240 region now. Weaker onshore equities have likely weighed at the margins today as well.

- USD/IDR edged up post BoJ, but found selling interest not long after. Spot got close to 15200 but we are now back close to 15100, around 0.50% firmer in IDR terms for the session. We highlighted earlier the stronger correlation between USD/IDR and USD/JPY over the past month, but this trend clearly hasn't been evident post the BoJ outcome today. Lows m the start of the week in USD/IDR come in just under 15000. BI is forecast to hike by another 25bps tomorrow.

- USD/MYR spiked towards 4.3400 in early trade but is now back to 4.3330. Trade figures for Dec, showed export and import growth slowing more than expected, export growth back to 6.0% y/y, from 15.1%, while imports were +12.0% y/y, from 15.6%. The trade surplus remained healthy though at MYR27.76bn and above expectations. BNM is expected to hike by 25bps tomorrow.

- Elsewhere, THB and PHP have outperformed against the SGD. USD/SGD is back towards 1.3240, seeing some spill over from higher USD/JPY levels. USD/THB is near 33.12, only slightly up for the session, while USD/PHP is down sub 54.80.

MNI Bank Indonesia Preview - January 2023: Inflation Means Another 25bp

EXECUTIVE SUMMARY

- Bank Indonesia is likely to hike rates another 25bp to 5.75% at its January 19 meeting due to continued price pressures and need to defend the currency. If the Fed hikes by 25bp, as expected, at its February meeting, then this would keep the rate differential unchanged and aid FX stabilisation.

- Some analysts are expecting BI to pause in January but with both headline and underlying inflation edging up in December and BI reiterating that it will respond to ensure that core remains under the upper end of its target band, another rate increase is likely this month. FX stability and ensuring continued foreign inflows are also a BI priority and while the IDR has appreciated somewhat since the last meeting, further support is likely from the central bank.

- Another 25bp is certainly possible in February given BI expectations that inflation pressures will remain elevated in H1 2023 and the need to attract foreign inflows. But given more dovish Fed expectations and lower commodity prices, BI is likely close to its terminal rate.

- For the full piece, see here.BI Preview - January 2023.pdf

MNI BNM Preview - January 2023: +25bps Likely, But Getting Closer To A Pause

EXECUTIVE SUMMARY

- The consensus looks for a 25bps hike from BNM tomorrow. Our base case also sits in the +25bps camp. Like elsewhere in the region, headline inflation pressures have cooled. The latest CPI y/y coming in at 4.0%, compared with 2022 highs at 4.70%. Still, this is only a modest move lower, while core inflation pressures continued to trend higher, the last print at 4.2% y/y, which was a fresh cyclical high.

- Growth rates remain elevated, but are expected to cool as we progress through 2023. The continued trend move down in the unemployment rate (latest at 3.6%), coupled with still elevated wages growth, +4.7% y/y for the manufacturing sector, should help keep domestic activity supported in the near term though.

- For this meeting, with inflation pressures still persisting, the path of least resistance is expected to be a further 25bps hike. The statement is likely to be monitored for signs around future monetary policy shifts, particularly scope for a pause in the tightening cycle. We are likely getting closer to this point.

- See the full preview here:BNM Preview - January 2023.pdf

EQUITIES: Little Spill Over From Japan Equity Surge Post BoJ

Outside of Japan equities, regional moves have been fairly modest. US futures currently sit close to flat, up from earlier lows, with eminis last near 4011 in index terms. Futures spiked post the BOJ decision, which left major policy parameters unchanged, but we are away from highs for the major indices.

- Post the lunch time break, Japan equities have surged as markets digest the BoJ outcome. The Nikkei 225 is up around 2.25% stage, as Japan bonds surge and the FX has fallen sharply. We still remain sub levels that prevailed prior to the last BoJ meeting (around 27250, versus 26725 current).

- Elsewhere, Hong Kong and China markets appear to be winding down ahead of next week's LNY break. The CSI 300 is down slightly at this stage, off 0.22%, while the HSI has trimmed 0.13% in the first part of the session.

- South Korean shares are seeing some underperformance, off 0.80%, amidst modest offshore outflows. Losses for Samsung have been a key driver of weakness.

- The ASX is close to flat, while SEA bourses - Malaysia and Indonesia are nursing modest losses.

GOLD: Bullion Falls Again As USD Rallies

Gold prices are down again during the APAC session by 0.4% to around $1900.40/oz, close to the intraday low of $1899.33. Earlier in the session bullion reached a high of $1910.38. The pullback has been driven by a stronger USD (DXY +0.4%) in response to unchanged core BoJ monetary policy settings.

- Gold is off 1.4% from Monday’s high of $1929.03/oz but still well above support at $1874.40, the January 12 low. It remains in a bullish trend and higher highs and higher lows are expected.

- There is a busy data schedule in the US today with the focus likely to be US December retail sales and PPI. Retail sales are expected to post another monthly decline, while the core PPI is also projected to decline on the month. December IP is forecast to fall again while inventories are should rise. The NAHB housing market index and the Fed’s Beige Book are also scheduled to be released.

OIL: Crude Continues To Rally On Demand Optimism

MNI (Australia) - Oil prices are higher today but have been trading in a narrow range of less than a dollar. Optimism regarding the outlook for the Chinese economy drove the market and prices reached their highest since the start of January, despite a stronger USD (DXY +0.5%). WTI is currently around $80.75/bbl and Brent $86.45.

- The January rally means that crude is now around its 100-day simple moving average. A short-term bullish trend continues with key resistance and bull trigger for WTI at $81.50.

- OPEC released its monthly outlook on Tuesday and expects the market to be balanced in Q1 2023. The Secretary General also said that he’s “cautiously optimistic” about the global growth outlook. The IEA will issue its monthly report later today, which should contain information on the impact of sanctions on Russian supply and the demand outlook. A Bloomberg survey showed that analysts expect Chinese oil demand to reach a record high this year.

- There is a busy data schedule in the US today with the focus likely to be US December retail sales and PPI. Retail sales are expected to post another monthly decline, while the core PPI is also projected to decline on the month. IP, API fuel inventory data and the Fed’s Beige Book are also scheduled to be released.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/01/2023 | 0700/0700 | *** |  | UK | Consumer inflation report |

| 18/01/2023 | 0930/0930 | * | | UK | ONS House Price Index |

| 18/01/2023 | 1000/1100 | *** |  | EU | HICP (f) |

| 18/01/2023 | 1000/1100 | ** | | EU | Construction Production |

| 18/01/2023 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 18/01/2023 | - |  | JP | Bank of Japan policy decision | |

| 18/01/2023 | 1330/0830 | * |  | CA | Industrial Product and Raw Material Price Index |

| 18/01/2023 | 1330/0830 | *** | | US | PPI |

| 18/01/2023 | 1330/0830 | *** | | US | Retail Sales |

| 18/01/2023 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 18/01/2023 | 1400/0900 | | US | Atlanta Fed's Raphael Bostic | |

| 18/01/2023 | 1415/0915 | *** | | US | Industrial Production |

| 18/01/2023 | 1500/1000 | * | | US | Business Inventories |

| 18/01/2023 | 1500/1000 | ** | | US | NAHB Home Builder Index |

| 18/01/2023 | 1800/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 18/01/2023 | 1800/1300 | | US | Kansas City Fed's Esther George | |

| 18/01/2023 | 1900/1400 | | US | Fed Beige Book | |

| 18/01/2023 | 2015/1515 | | US | Philadelphia Fed's Pat Harker | |

| 18/01/2023 | 2100/1600 | ** | | US | TICS |

| 18/01/2023 | 2200/1700 | | US | Dallas Fed's Lorie Logan |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.