Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

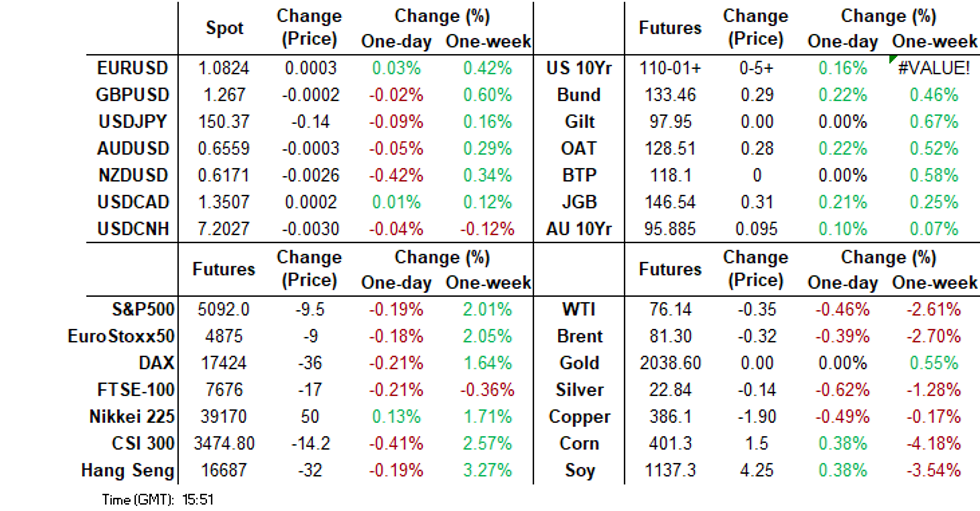

- NZD/USD weakness has been the standout as trading kicks off for the week. A pullback wasn't unexpected given the size of the move last week, and as we head into the RBNZ rate decision later this week traders are understandably cautious. Market pricing is around 30% chance of a hike on Wed. Also note, leveraged kiwi longs now sit at the highest since August 2023.

- US Tsy futures have been grinding higher throughout the day, with little in the way of market news. Lower yields haven't weighed on the USD, although yen has outperformed in the G10 space.

- After falling around 2.5% on Friday oil prices are down again during APAC trading as softer risk appetite has weighed on commodities generally. Markets remain concerned about weaker demand from the US and China while supply remains robust.

- Later there are US new home sales for January. The ECB’s Lagarde participates in a plenary debate and BoE’s Pill and Breeden also speak.

MARKETS

US TSYS: Treasuries Edge Higher, 2y10y Makes Fresh New lows

- Mar'24 10Y futures have been grinding higher throughout the day, with little in the way of market news, trading near highs of the day at 110-01+, vs highs of 110-02+. Levels to watch to the upside are initial resistance is at 110-14+ (20-day EMA) above here opens a moved to 110-17+ (high Feb 15), while on the downside initial support is at 109-10 (Low Feb 23) a break here opens the Nov 28 lows at 109-05+,

- Treasury yield curves are flatter today, with the 2Y yield -1.9bps lower at 4.671%, the 10Y yield -2.2bps lower at 4.226%, while the 2Y10Y made fresh yearly lows earlier to now trade mostly unchanged at -44.594.

- Biden to meet congress leaders on Tuesday a bid to unlock billions of dollars in emergency aid to allies including Ukraine and avert a US government shutdown.

JGBS: Bull-Flattener, National CPI & 5Y Climate Transition Bond Supply Tomorrow

JGB futures are higher and at session highs, +23 compared to settlement levels, after being closed on Friday.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined PPI Services data.

- (Dow Jones) Japan's weak growth trajectory prompts UBS to tweak its view on the central bank's policy path. UBS still expects the BoJ to end its easy policy framework--which includes negative interest rates--in April but no longer sees a July policy rate hike, chief Japan economist Masamichi Adachi says. (See link)

- The cash JGB curve has bull-flattened, with yields flat to 3bps lower. The benchmark 10-year yield is 2bps lower at 0.700% versus the Nov-Dec rally low of 0.555%.

- The swaps curve has also bull-flattened, with rates flat to 3bps lower. Swap spreads are generally tighter.

- National CPI data for January is due tomorrow, along with the MoF sales of 5-Year Climate Transition Bonds.

AUSSIE BONDS: Richer But Off Best Levels, CPI & Retail Sales Data Later In The Week

ACGBs (YM +5.0 & XM +9.0) are higher but off Sydney session highs. ACGBs opened stronger today following on from US tsys’ bull-flattening on Friday. Without domestic catalysts, the local market has extended those gains in sympathy with US tsy dealings in today’s Asia-Pac session. Cash US tsys are ~2bps richer across benchmarks.

- Cash ACGBs are 6-9bps richer, with the AU-US 10-year yield differential at -13bps.

- Swap rates are 4-7bps lower, with the 3s10s curve flatter.

- The bills strip has bull-flattened, with pricing flat to +6.

- RBA-dated OIS pricing is flat to 4bps softer across meetings. A cumulative 37bps of easing is priced by year-end.

- The local calendar is empty tomorrow, with January CPI (Wed) and Retail Sales (Thu) as the week's highlights.

- January CPI is expected to increase moderately to 3.6% y/y from 3.4% in December with forecasts between 3.4% and 4%. As it is the first month of the quarter it will contain limited updated information on services and will mainly cover goods prices.

- Retail Sales for January is expected to rise 1.6% m/m after falling 2.7%. The series has been volatile due to changes in the timing of seasonal discounts and forecasts for January range from +0.3% to +2.5%.

NZGBS: Richer, 30% Chance Of A RBNZ Hike On Wed Is Priced

NZGBs closed 3-4bps richer and near the session’s best levels. With the domestic calendar empty today, local participants appear to have taken their directional guidance from US tsys. After closing out last week with a solid bull-flattening of the curve, US tsys have extended those gains in today’s Asia-Pac session. Cash US tsys are currently dealing 1-2bps richer across benchmarks.

- Swap rates closed 7bps lower, with the 2s10s curve little changed.

- Ahead of the RBNZ Policy Decision on Wednesday, Bloomberg consensus is nearly unanimous (19 of the 21 surveyed economists) in expecting a no-change result for the OCR. Only ANZ and TD are calling for a 25bp hike to 5.75%.

- Shadow Board members recommended the RBNZ keep the OCR at 5.5% this week, according to the NZIER.

- RBNZ dated OIS pricing is 1-3bps softer across meetings. A 32% chance of a 25bp hike is priced for this week’s meeting, with an expected terminal OCR of 5.65% (a 61% chance of a 25bp hike) for the May meeting. A cumulative 40bps of easing is priced by year-end.

- Tomorrow, the local calendar is empty.

NZ STIR: RBNZ Dated OIS Has A Hike At A 30% Chance

Ahead of the RBNZ Policy Decision on Wednesday, Bloomberg consensus is nearly unanimous (19 of the 21 surveyed economists) in expecting a no-change result for the OCR. Only ANZ and TD are calling for a 25bp hike to 5.75%.

- RBNZ dated OIS pricing is 1-3bps softer across meetings. A 32% chance of a 25bp hike is priced for this week’s meeting, with an expected terminal OCR of 5.65% (a 61% chance of a 25bp hike) for the May meeting.

- A cumulative 40bps of easing is priced by year-end.

Figure 1: RBNZ Dated OIS Pricing (%)

Source: MNI – Market News / Bloomberg

FOREX: NZD Unwinds Some Recent Outperformance, As RBNZ Comes Into View

The main theme in G10 FX markets in the first part of Monday trade has been the retracement in NZD. Trends have been relatively subdued elsewhere. The BBDXY is little changed, last near 1242.7.

- NZD/USD sits just above session lows, last near 0.6170 (earlier lows at 0.6163). This is around 0.45% weaker versus end levels from NY last Friday.

- A pullback wasn't unexpected given the size of the move last week, and as we head into the RBNZ rate decision later this week traders are understandably cautious. Also note, leveraged kiwi longs now sit at the highest since August 2023.

- Offshore demand post last week's chunky onshore debt auction may have dissipated as well.

- AUD/USD has been dragged down a little by NZD, but is only marginally weaker, last near 0.6555. The AUD/NZD cross is back to 1.0625/30, after making fresh lows last week to 1.0570.

- Weakness in iron ore prices has impacted AUD, while HK and China equities are tracking lower at this stage.

- JPY has outperformed at the margins, but remains well within recent ranges, last near 150.50.

- US yields are slightly softer to start the week, down around 2bps across the benchmarks. This may be aiding yen performance on a cross basis.

- Looking ahead, there are US new home sales for January. The ECB’s Lagarde participates in a plenary debate and BoE’s Pill and Breeden also speak.

ASIA STOCKS HK & China Equities Mostly Lower, Focus Turns To Earnings

Hong Kong and China equities are lower today, as investors opt to take profit after equities notched up their longest winning streak since 2018. There has been little in the way of market headlines or economic data. Looking ahead this week, China PMI is due out on Friday, while Hong Kong sees Trade Balance, GDP data out.

- Hong Kong Equities are lower today after the HSI climb to a seven-week high last week. Investors are now looking forward to company earnings with little economic data due out this week. Baidu, NetEase, Li Auto & HKEX lead the way this week for earnings, with close eyes on Baidu & NetEase on the back of China announcing they will be tightening their grip on the tech sector. HSI is down 0.70%, HSTech down 0.40%, while the Mainland Property Index is well off earlier lows to trade just 0.39% at the break.

- China Equities are mixed today as financial underperform. The CSI300 is 0.71% lower, while the CSI1000 is trading 0.74% higher.

- China Northbound flows turned positive for year late last week and are tracking along steady with the 5-day average sit in line with the 20-day average at around 2.1b yuan above the longer term 200-day average of -0.633b

- The Chinese government seeks to boost the sales of traditional consumer products, as reported by state broadcaster CCTV, the CSI All Share auto Index traded 2.00% higher post the announcement.

- Companies have been withdrawing their applications for IPOs on China's domestic markets are regulators look to step up scrutiny.

ASIA PAC EQUITIES: Asian Equities Mostly Lower, Foreign Equity Inflows Lose Momentum

Regional Asian Equities have opened mostly lower to start the week, with Japan being the exception after being out on Friday.

- Japan equities are higher today, continuing their stellar run of late however they are off their highs from this morning. Trading houses are leading the gains today after Berkshire Hathaway reported an unrealized gain in Japan's five largest trading houses of $8B, while Warren Buffet mentioned Japan's Shareholder friendly policies are "superior" to those in the US. The Nikkei 225 made new all-time highs last week and is now nearing the 40,000 mark, up 0.40% today, while the Topix is up 0.65%.

- Taiwan Equities are slightly higher, with Electronic Parts sector leading the way higher, Largan Precision contributed the most to gains up 3.00%. Foreign Equity inflows are positive but momentum is starting to slow; the 5-day average is $113m, down from $620m a week earlier, while the 20-day average is $458m. The Taiex is up 0.22%

- South Korean Equities are lower today due to the "Value Up" announcement disappointing investors with a lack of details and enforcement measures released. The KOSPI was down as much as 1.4% earlier but has recovered somewhat to trade just 0.47% lower for the day. Similar to Taiwan equity flow, momentum is slowly diminishing; the 5-day average is now $148m vs $305m a week ago, while the 20-day average hovers around $300m.

- Australian equities are slightly higher today, with gains in the financial sector being offset by weakness in metal and mining names, while energy names are the worst performers for the day, the ASX closed up 0.12%

- Elsewhere in SEA, NZ equities are down 0.08%, Indonesian equity are 0.18% after two days of foreign equity outflows, while Singapore equities are down 0.80%

ASIAN EQUITY FLOWS

- China equities inflows are tracking along steady the 5-day average sit inline with the 20-day average at around 2.1b yuan above the longer term 200-day average of -0.633b. On the CSI300 climbed for 9 straight day marking the longest rally since 2018.

- South Korean equities saw positive inflows again post Nvidia earnings, but well off the level Taiwan saw. The 5-day average is now $148m vs $305m a week ago, while the 20-day average hovers around $300, signally investors may be looking to take profit after such strong recent performance. SK Finance minister is speaking this morning about the "Value Up" program.

- Taiwan equities saw a large inflow on Friday, largely due to flows into the semiconductor space.

- Indonesian equities saw their 2nd day in a row of outflows, and the largest day since 26 Jan. There has been little in the way of catalyst, although the JCI for the third time this month fail above the 7350, and now trade back toward the lower ranges for the past two weeks. Goldman has upgraded Indonesian equities due to reduced political uncertainty.

- Indian equities saw an outflow on Friday, this could just be profit taking as equities hit new all time highs. Momentum is still strong as the 5-day average still sits well above the 20-day at $108m vs -$41.

- Thailand equities saw -$54 in outflows on Friday as trade balance data missed, while a delay in cut rate expectations from the Fed have seen to be weighing on stocks. Thai equities still have positive equity flow momentum with the 5-day average hovering around $50m vs the 20-day at $9m

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| China (Yuan bn)* | -0.1 | 10.7 | 17.4 |

| South Korea (USDmn) | 44 | 741 | 7617 |

| Taiwan (USDmn) | 998 | 567 | 5082 |

| India (USDmn)** | -23 | 542 | -3401 |

| Indonesia (USDmn) | -67 | 65 | 1349 |

| Thailand (USDmn) | -54 | 249 | -624 |

| Malaysia (USDmn) ** | 14 | 147 | 450 |

| Philippines (USDmn) | 1 | 30.1 | 198 |

| Total (Ex China USDmn) | 913 | 2341 | 10670 |

| * Northbound Stock Connect Flows | |||

| ** Data Up To Feb 22 |

OIL: Crude Continues Sell Off As Weaker Risk Appetite Weighs On Commodities

After falling around 2.5% on Friday oil prices are down again during APAC trading as softer risk appetite has weighed on commodities generally. Markets remain concerned about weaker demand from the US and China while supply remains robust. Brent is 0.4% lower at $81.27/bbl, close to the intraday low of $81.19. WTI is down 0.5% to $76.13, finding support around $76. The USD index is little changed.

- The market will be monitoring comments from International Energy Week in London for signals of what is expected going forward. OPEC will announce in early March if it will extend production cuts into Q2, which is looking likely. Goldman Sachs doesn’t expect the reductions to be eased until Q3.

- January US PCE inflation data due on Thursday will also be watched closely. If it prints high, then expectations of further delays to Fed cuts are likely to increase – a development that has been worrying oil markets.

- Bloomberg is reporting that strong travel in China over the Lunar New Year holiday has meant an increase in demand since then by local refiners.

- On Saturday a US tanker was targeted but not struck by Houthi rebels in the Gulf of Aden. The US and UK hit 18 Houthi sites in Yemen the same day.

- Later there are US new home sales for January. The ECB’s Lagarde participates in a plenary debate and BoE’s Pill and Breeden also speak.

IRON ORE: Fresh Lows Back Early Nov 2023, As China Property Headwinds Persist

Iron ore has started off the week on a soft note. The active Singapore contract back close to $116/ton, off a further 3.2%. This comes after last week's 8.55% drop, although we did see some stability through Thurs/Fri trade.

- The active contract is now back to levels last seen in early Nov last year. Sentiment around China housing still looks quite uncertain in terms of any significant rebound, while China real estate equities have lagged the broader market gains in recent weeks.

- Iron ore inventories at China ports are climbing, recording a +5.43% gain last week. We are now up +26.9% from late Oct lows last year, which also points to less robust demand onshore, all else equal.

- We get the official PMI readings this Friday for China, which will be an important update for the mnauftacuring sector.

GOLD: Slightly Lower After The Largest Weekly Gain In Two Months

Gold is slightly lower in the Asia-Pac session after its largest weekly gain in two months. Bullion closed 0.5% higher at $2035.40 on Friday.

- The yellow metal was supported by lower US Treasury yields on Friday. There was no obvious driver for the move. Short covering, bargain hunting, and technical buying supported US tsys, with the 10-year yield declining 7bps to 4.25%. The front end underperformed ahead of 2- and 5-year auctions later today.

- Gold traded lower into mid-month but is building well off lows and extended further above the 50-dma on Friday, according to MNI’s technicals team.

- A sustained clearance above this point and above the Feb 1 high of $2065.50 would be required to reinstate a bullish theme, with the mid-month weakness proving corrective in nature.

ASIA FX: NEA FX Steady, Some Softness in SEA Amidst Equity Weakness

For the most part it has been a quiet start to the week for Asia FX. USD/CNH has drawn selling interest above 7.2100, even with onshore equities generally under pressure. KRW and TWD have both been steady. In SEA we are seeing some USD strength, but it fairly modest at this stage. Tomorrow the data calendar is fairly quiet with South Korean retail sales and Q4 external debt on tap. Later on, Taiwan Jan export orders will print.

- USD/CNH has tracked ranges from late last week. We couldn't sustain moves above 7.2100, last near 7.2040, little changed for the session. Equity sentiment has mostly weakened as markets digest recent regulatory moves, while efforts to boost auto and other consumer durable consumption has only benefited some sectors today. Later in the week we get the official PMIs for Feb.

- 1 month USD/KRW was firmer in the first part of trade, but now sits back at 1328, unchanged from end NY levels on Friday. Local equities are weaker, as the government announced measures to reduce the valuation gap. Still, we are away from lows, the Kospi last down -0.45%, (we were off around 1.4% earlier).

- Spot USD/TWD and the 1 month NDF are very steady. Both pairs last near 31.55, not too far off YTD highs. TWD weakness comes despite generally strong tech equity sentiment. Also note last week saw positive equity inflow momentum, albeit fairly modest at $567.2mn. Feb to date has seen +$3.67bn in net inflows though. An offset is clearly coming from the push out in Fed rate cut timing. Given low levels of yields onshore, sensitivity is likely to US yield developments. The US -TW 2yr swap rate differential is +362bps, not too far off recent highs. J.P. Morgan also note that poor FX conversion (from overseas) earnings is another meaningful TWD headwind.

- Spot USD/IDR is back close to 15630, while the 1 month NDF is near 15640, bother around 0.2% weaker in IDR terms versus prior closing levels. Dips once against the pair sub 15600 have been supported. Local equities have struggled in recent session while equity inflow momentum cooled at the end of last week. We also had outflows from local bonds last week.

- Spot USD/SGD is slightly higher, last near 1.3445. Recent lows come in at 1.3394. The SGD NEER (per Goldman Sachs estimates) has drifted a little wider relative to the top end of the band (last -0.42%). We did get to -0.29% last week. Last Friday, CPI data was weaker than expected, while today Jan IP figures also feel more than forecast (-5.7% m/m, versus +3.1% expected). The fall was driven by weakness in the volatile Pharma sub sector but still recent data outcomes have weighed on SGD outperformance at the margins.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 26/02/2024 | 0800/0900 | ** |  | ES | PPI |

| 26/02/2024 | 0900/0900 |  | UK | BOE's Breeden at BOE agenda for Research Conference | |

| 26/02/2024 | 1100/1100 | ** | | UK | CBI Distributive Trades |

| 26/02/2024 | 1100/1100 | | UK | BOE's Pill at BOE Agenda for Research conference | |

| 26/02/2024 | 1500/1000 | *** |  | US | New Home Sales |

| 26/02/2024 | 1530/1030 | ** | | US | Dallas Fed manufacturing survey |

| 26/02/2024 | 1600/1700 |  | EU | ECB's Lagarde participates in debate on ECB 2022 Report | |

| 26/02/2024 | 1630/1130 | * | | US | US Treasury Auction Result for 2 Year Note |

| 26/02/2024 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 26/02/2024 | 1800/1300 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 26/02/2024 | 1800/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

| 27/02/2024 | 2330/0830 | *** |  | JP | CPI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.