Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Risk assets extend their rout as the U.S. puts troops on high alert amid escalating tension with Russia over Ukraine. Asia-Pac equity benchmarks retreat along U.S. e-mini futures, yen leads gains in G10 FX space.

- Core FI receive a fillip from risk aversion, but ACGBs remain on the back foot after the release of strong CPI data out of Australia. Participants add hawkish RBA bets as inflation figures top forecasts.

- SGD rallies after the Monetary Authority of Singapore joins the growing pack of hawkish central banks and announces an unscheduled decision to tighten currency policy.

BOND SUMMARY: Risk Aversion Aids Core FI But ACGBs Take Hit From Strong Inflation Data

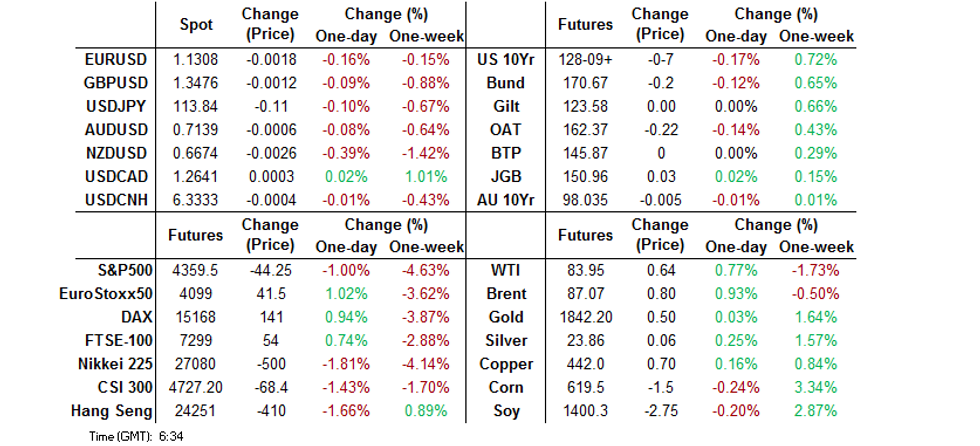

Australia's above-forecast Q4 CPI data delivered a blow to ACGBs but continued risk rout provided support to the core FI space, underpinning partial recovery in Aussie bonds. The prospect of a Russian military strike on Ukraine and uncertainty ahead of Wednesday's monetary policy announcement from the increasingly hawkish Fed cumulated into an unabating sense of anxiety.

- Consumer prices down under grew 3.5% Y/Y in the final quarter of 2021, while the RBA's preferred metric of underlying inflation printed at +2.6%, crossing above the mid-point of the +2.0%-3.0% target range for the first time since 2014. The data inspired more sell-side desks to revise their RBA rate-hike calls, with market participants adding hawkish central bank bets. ACGBs took a hit after the release of inflation figures, with 3-year yield hitting its highest point since Apr 2019 amid a growing choir of voices expecting the RBA to scrap their QE programme as soon as next week. Risk-off flows brought the space some reprieve, but bear flattening remains evident in cash Sydney trade. ACGB yields last sit 1.5-7.0bp higher across the curve. Aussie bond futures have ticked away from post-CPI lows, YM last -4.0 & XM -1.5. Bills trade 1-4 ticks lower through the reds.

- T-Notes crept higher, retracing part of their sharp pullback from Monday's NY hours. The contract last operates -0-07 at 128-09+, just shy of best levels of the session. Eurodollar futures trade 1.0-5.0 ticks lower through the reds. Tsy curve has steepened in cash Tokyo trade, with yields last seen +0.6bp to -2.0bp. Conf. Board Consumer Confidence & 5-Year Tsy auction will take focus in the U.S. today.

- JGB futures advanced after an initial spell of mild weakness, which seemed like a follow-through from the move in U.S. Tsys observed in the NY session. JBH2 printed new session highs after the Tokyo lunch break and last sits at 150.99, 6 ticks above previous settlement. The yield curve steepened in cash trade, with the super-long end slipping. Japan's MOF sold Y598.8bn of 40-Year JGBs, with high yield matching the forecast based on BBG dealer poll. Comments from BoJ Gov Kuroda and PM Kishida were shrugged off, as both officials failed to offer much in the way of fresh insights.

FOREX: Risk-Off Storm Intensifies, Forces AUD/USD To Give Away Post-CPI Gains

The Asia-Pac session witnessed a renewed flight into safe haven currencies, as regional equity benchmarks retreated alongside U.S. e-mini futures on the back of imminent policy decision from the Fed & deepening geopolitical angst.

- The yen comfortably outperformed its G10 peers, with Tokyo traders digesting Monday headlines surrounding the Russo-Ukrainian stand-off. Demand for safer assets provided a tailwind for the greenback, but the DXY failed to re-test yesterday's peak.

- Sydney morning saw AUD catch a bid after Australian inflation data topped expectations, with the RBA's preferred measure of core inflation printing above the mid-point of the target range for the first time since 2014. The release boosted hawkish RBA bets, with market pricing pointing to potential for a rate hike as soon as in May.

- There was talk of cross flows applying pressure to the kiwi after Australian data hit the wires, albeit AUD/NZD struggled to take out the NZ$1.0700 figure. New Zealand's own Q4 CPI data on Thursday will provide an input into the comparative assessment of policy outlooks of Antipodean central banks.

- Post-CPI bid in AUD evaporated later in the Asia-Pac session, as risk-off flows intensified. AUD/USD erased its initial gains, but the Aussie remained the best performing high-beta currency. NOK was the main laggard, as the Ukraine tension outweighed an uptick in crude oil prices.

- German Ifo Survey & U.S. Conf. Board Consumer Confidence take focus on the data front today. Central bank speaker slate features ECB's Holzmann & Riksbank's Skingsley.

FOREX OPTIONS: Expiries for Jan25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1300-10(E1.6bln), $1.1330-40(E703mln), $1.1450(E1.1bln)

- USDJPY: Y115.25-40($663mln)

ASIA FX: Risk-Off Tone Weighs; Surprise MAS Action Bolsters SGD

Continued risk-off flows fuelled by the familiar combination of geopolitical risks & imminent Fed tightening sapped strength from Asia EM currencies, with a handful of exceptions. CNH grew stronger ahead of the LNY holidays, while SGD received a boost from unexpected monetary policy action.

- SGD: The Singapore dollar caught a bid and printed its best levels since Oct 21, after the MAS announced a surprise decision to tighten policy, joining the growing pack of monetary authorities scrambling to tame inflation. The MAS said they will "slightly raise" the appreciation rate of their S$NEER policy band, while keeping its width and centre level unchanged. It was the first unscheduled policy action from the MAS since 2015 and came on the heels of above-forecast CPI data released on Monday.

- CNH: Spot USD/CNH held a tight range. The yuan fix fell in close proximity to sell-side expectations, even as a BBG real-time tracker of redback strength against a basket of currencies surged to an all-time highs.

- KRW: The won went offered on the back of risk broader aversion. The news that South Korea's daily Covid-19 cases hit an all-time high while North Korea may have test-launched two cruise missiles added pressure to the KRW, with South Korea's growth data provoking a muted reaction. Meanwhile, South Korea said it is looking to ease rules on foreign investors' access to local FX markets.

- MYR: The ringgit traded sideways, holding a narrow range. PM Ismail Sabri noted that Malaysia considers relaxing Covid-19 rules for international travellers.

- PHP: The peso trimmed its initial losses. Philippine officials are set to discuss tweaks to Covid-19 Alert Level settings on Thursday, amid suggestions that Metro Manila could be moved down by one notch to Level 2.

- The likes of IDR and THB extended losses on the back of broader market impetus, as domestic headline flow failed to provide much in the way of notable catalysts.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 25/01/2022 | 0700/0700 | *** |  | UK | Public Sector Finances |

| 25/01/2022 | 0800/0900 | ** |  | ES | PPI |

| 25/01/2022 | 0900/1000 | *** |  | DE | IFO Business Climate Index |

| 25/01/2022 | 1100/1100 | ** | | UK | CBI Industrial Trends |

| 25/01/2022 | 1330/0830 | ** |  | US | Philadelphia Fed Nonmanufacturing Index |

| 25/01/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 25/01/2022 | 1400/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 25/01/2022 | 1400/0900 | ** | | US | FHFA Home Price Index |

| 25/01/2022 | 1400/1500 | ** |  | BE | BNB Business Sentiment |

| 25/01/2022 | 1500/1000 | *** | | US | Conference Board Consumer Confidence |

| 25/01/2022 | 1500/1000 | ** | | US | Richmond Fed Survey |

| 25/01/2022 | 1630/1130 | ** | | US | NY Fed Weekly Economic Index |

| 25/01/2022 | 1630/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 25/01/2022 | 1800/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.