Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

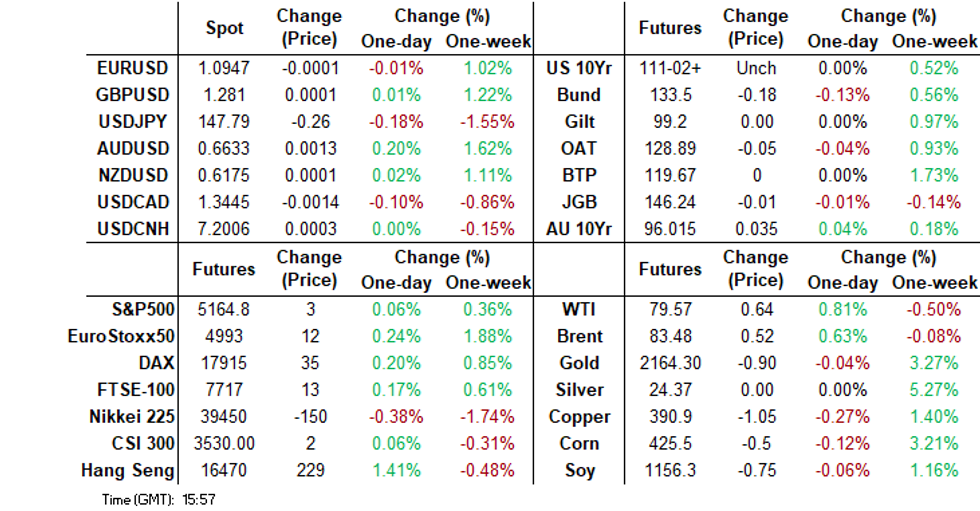

- The USD index (BBDXY) sits marginally lower in latest dealings, last near 1230.2. We are up from earlier multi week lows at 1229.45. US yields are roughly 1bp lower across the curve.

- Yen strength was again an early focus point, but we are away from best levels. USD/Asia pairs are mostly lower, except for USD/CNH. Regional Asian equities are higher today and are on track to make it seven straight weeks of gains, tech stocks have been rallying again on dovish signals from the US Fed as well as optimism around the AI space.

- Oil prices are higher, but remain within recent ranges, while Gold is slightly weaker in the Asia-Pac session, after closing 0.5% higher at $2159.98 on Thursday.

- Looking ahead, US non-farm payrolls will be the main focus point. We also hear from The Feds Williams.

MARKETS

US TSYS: Tsys Future Edge Higher, Break Initial Resistance Ahead of Employ Data

- Jun'24 10Y futures are edging higher as we come back from the break, reaching new highs of 111-24 above initial resistance, eyes will be on weather we can hold above here. Ranges have remained tight with lows of 111-19+ and highs of 111-24 where we trade now.

- Futures briefly traded above initial resistance at 111-23 (Mar 6 highs) on Thursday, a break and hold above there opens 111-27 (50% retracement of the Feb 1 - 23 bear leg) further up 112-04 (Feb 7 highs), while to the downside 110-21 (Mar 4 lows) and 110-05+/109-25+ (Low Mar 1 / Low Feb 23 and bear trigger)

- Treasury yields are roughly 1bp lower across the curve with the 2Y -0.9bp at 4.492%, 10Y is -0.6bps higher at 4.077%, while the 2y10y is +0.238 to -41.842

- Biden is spoke at the State Of Union earlier, while there was little in the way of market moving headlines he did mention he would not hesitate to order more strikes on Houthis, and that he would ban AI voice impersonation.

- Looking ahead February Employment Report.

JGBS: Off Worst Levels, Futures Back To Flat, Awaiting US Payrolls

JGB futures are little changed, +1 compared to the settlement levels, after spending most of today’s session in the red.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined household spending and current account data. Leading & Coincident Indices are due later today.

- (Bloomberg) -- Japan’s annual wage negotiations are nearing a conclusion, drawing intense scrutiny as the BoJ looks for evidence of a virtuous wage-price cycle that would allow it to exit from the world’s last negative rate regime. (See link)

- Results from today’s BoJ Rinban operations covering 1- to 10-year JGBs showed positive spreads and elevated off-cover ratios. Nevertheless, JGBS moved away from the session’s worst levels.

- Cash US tsys are dealing little changed in today’s Asia-Pac session ahead of US Non-Farm Payrolls later today.

- Cash JGBs are still cheaper, with the 20-year zone as the underperformer (+1.8bps). The benchmark 10-year yield is 0.2bps higher at 0.733% versus the February high of 0.772%.

- The 2-year JGB yield earlier rose to 0.2% for the first time since 2011. It currently sits at 0.197%.

- Swap rates are slightly lower, with swap spreads tighter.

- On Monday, the local calendar sees Q4 F GDP, February Money Stock M2 & M3 and February Machine Tool Orders data.

JAPAN DATA: Household Spending Fell in Jan, Current Account Surplus Stronger Than Expected

Earlier, household spending data for Jan was weaker than expected, printing at -6.3% y/y, versus -4.1% forecast and prior of -2.5%. This is a measure real household spending and it is now back to early 2021 lows.

- Consumption is a key focus point for the authorities and the BoJ outlook. Firmer wages growth is seen as critical to driving firmer spending trends as we progress through 2024. Given anecdotes around wage negotiations are firmer for this year compared with last year, today's weaker household spending print may not impact BoJ thinking.

- Food spending was down 2.7% y/y, while transport spending, -13.1%y/y was also a weak point. These trends do tend to be volatile though.

- Other data showed the current account stronger than expected for Jan. It printed ¥438.2bn, versus the -¥330.4bn forecast. In adjusted terms were ¥2727.5bn, against a ¥2074.4bn forecast. The adjusted trend is just sub 2023 highs. Primary income surged to nearly ¥3600bn. The trade deficit (in seasonally adjusted terms) was -¥328.7bn, slightly improved on the Dec reading.

- Exports and imports both fell in Jan versus Dec levels.

AUSSIE BONDS: Slightly Richer, Narrow Ranges Ahead Of US Payrolls

ACGBs (YM +2.0 & XM +1.0) are little changed after dealing in relatively narrow ranges in the Sydney session. With the domestic calendar empty, today’s session has been your typical pre-US payrolls session. US Non-Farm Payrolls is due later today.

- Bloomberg consensus sees payrolls growth of 200k for February, but two-month revisions will likely be closely watched. Please find the MNI's Preview here.

- (MNI) The BoC left its overnight rate at 5% and said it’s still too early to consider lowering the policy rate. (See MNI’s BoC Review here)

- Cash US tsys are dealing little changed in today’s Asia-Pac session after yesterday’s bull-steepening. News flow has been light today.

- Cash ACGBs are 1-2bps richer, with the AU-US 10-year yield differential 2bps higher at -9bps.

- Swap rates are 2bps lower.

- Bills strip pricing is flat to +2.

- RBA-dated OIS pricing is flat to 2bps softer across meetings. A cumulative 44bps of easing is priced by year-end.

- The local calendar is empty on Monday.

- TCorp has priced a new A$2.5bn 4.75% 20 Feb-37 benchmark bond via syndication. The final price for the transaction is 90.50bps over the 10-year bond futures contract, equivalent to 79.20bps over the ACGB 3.75% 21 April 2037. Joint lead managers for the transaction are BofA Securities, Deutsche Bank, NAB and Westpac.

NZGBS: Closed Slightly Richer Ahead Of US Payrolls Later Today

NZGBs closed well off session cheaps, 2-3bps richer across benchmarks. With the domestic calendar empty, local participants were content to sit on the sidelines ahead of US Non-Farm Payrolls later today.

- Bloomberg consensus sees payroll growth of 200k for February, but two-month revisions will likely be closely watched. Please find the MNI's Preview here.

- Swap rates closed 5-7bps lower, with implied swaps spreads 3-4bps tighter.

- RBNZ dated OIS pricing closed flat to 4bps softer across meetings, with Feb-25 leading. A cumulative 55bps of easing is priced by year-end.

- Recently released quarterly indicators that feed into Q4 GDP have resulted in BNZ Economics nudging up its estimate to +0.1%. Against strong population growth of 0.6% for the quarter, this would represent another significant contraction in GDP per capita, with the economy experiencing conditions similar to the depths of the GFC on this basis.

- Next week, the local calendar sees Card Spending on Tuesday, Food Prices on Wednesday, Net Migration on Thursday and BusinessNZ Manufacturing PMI on Friday.

- Also, RBNZ Governor, Adrian Orr and Chief Economist, Paul Conway will speak about the February Monetary Policy Statement at separate events over 12-14 March 2024.

FOREX: Strong Regional Equities Keep USD Upside Limited, As NFP Comes Into Focus

The USD index (BBDXY) sits marginally lower in latest dealings, last near 1230.2. We are up from earlier multi week lows at 1229.45.

- Early sentiment appeared as a carry over from US trade on Thursday, with yen strength in focus. USD/JPY got to fresh lows of 147.53, but we sit back near 147.85 now. Moves above 148.00 have drawn selling interest from the market.

- Data was mixed with real household spending comfortably below estimates (-6.3% versus -4.1% forecast and -2.5% prior). The market and BoJ may look through the print to a degree given positive wage growth signals for this year. Current account figures were stronger though.

- AUD/USD tried to break higher in early trade, but ran out of steam above 0.6630. Dips have been supported though and we were last a touch lower at 0.6625. A better regional equity tone in Asia Pac, amid broad based gains, except for onshore China markets, has aided sentiment this afternoon.

- NZD/USD has trailed somewhat, the pair last unchanged near 0.6175. The AUD/NZD cross is challenging the 100-day EMA at 1.0734.

- Recent sharp USD losses may be giving rise to some caution in the market around extending these moves further, particularly with the US NFP print coming up later. Canadian employment data will also cross later.

ASIA EQUITIES: HK Equities Out-Perform, Biotech Recovers After Thursday's Sell Off

Hong Kong and China equities are mixed today with HK markets out-performing. Comments from Powell on Thursday regarding potential rate cuts this year, though not new or unexpected, have contributed to the market's upward momentum.

- Hong Kong equity markets show positive gains today, with biotech names reversing some losses from Thursday, marking a 1.94% increase and emerging as the top-performing sector. The Mainland Property Index is up by 0.50%, the HSTech Index records a 1.00% gain, and the HSI experiences a 1.10% increase. China equities are underperforming the moves higher by HK markets and now trade mixed with the CSI300 down 0.15% while the CSI1000 is up 0.35%

- China Northbound flows were -2.1b yuan on Thursday, with the 5-day average to -2.88b, while the 20-day average sits at 2.31b yuan. While investors pulled $109m from the 2nd largest Chinese focused ETF (iShares MSCI China ETF) on Thursday, the most since Dec 22nd.

- In the property space, China Vanke continues to face pressure as several major insurers seek to protect their privately issues debt over concerns of potential liquidity stress. Chinese property developer Kaisa Group will be in court this morning over a wind-up petition. While Hong Kong's recently scrapping of property curbs have caused a spike in property sales with Henderson Land Development selling 190 of 208 apartments with the units receiving over 7,300 applications meaning they were oversubscribed by 34 times.

- Looking ahead China has CPI & PPI due out on Saturday, while the NPC meeting continues

ASIA PAC EQUITIES: Asian Equities Higher Led by Tech and Financials

Regional Asian equities are higher today and are on track to make it seven straight weeks of gains, tech stocks have been rallying again on dovish signals from the US Fed as well as optimism around the AI space.

- Japan equities are higher today with banking names leading the way, the Topix Bank Index is up 2.60% as strong Japan trade data makes the chances for a rate hike grow. The Topix is up 0.83%, while the Nikkei is trading just below the 40,000 level up 0.88% today. The Yen has surged 1.5% over the past week

- South Korean equities are 0.90% higher today as tech stocks rally following dovish remarks from Powell on Thursday with SK Hynix, Samsung Electronics and Samsung Biologics the top performers, while the Kospi is on track to finish the week up 1.70%.

- Taiwan equities are higher today although well of earlier highs made on the open, the Taiex at one point was 1.83% higher now trading just 0.40% better for the day the top contributor to the move has been TSMC who will be releasing February sales figures shortly.

- Australian equities are higher today following one from US moves on Thursday, the dovish tone for Powell has helped push the market higher. Financials are the top performing sector, with just Commercial & Professional Services stocks in the red, the ASX200 has closed 1% higher.

- Elsewhere in SEA, NZ closed 1% higher, Thailand equities continue to see foreign investors selling with Thursday marking 8 out of 10 days of net outflows although equities are 1% higher today,

ASIA EQUITY FLOWS: Asia Equity Flows Positive As Semiconductor Names Lead The Way

- China equities were lower on Thursday despite strong data equity flows have now seen two days of outflows taking the past 5 days to -14.4b yuan. China CPI & PPI is due out on Saturday expected to be 0.3%, while PPI is expected to remain unchanged at -2.5%. The 5-day average continues to trend lower, now at -2.88b vs the 20-day average at +2.31 billion yuan.

- South Korean equities have now notched up two days in a row of outflows the first in over a month and worst day since Jan 17th. Most the the outflows came from the tech sector with -$171m in net flow. The 5-day average continues to trend lower, now at $52m vs the 20-day average at +$188m.

- Taiwan equities were again higher with global semiconductor names leading the way. TSMC will release Feb sales figures later today which will set the trend for future flows. The 5-day average continues to trend lower, now at $446m vs the 20-day average at +$265m.

- Thailand equities were higher on Thursday after consumer confidence data rose to 4 year highs on higher tourism levels and government's economic stimulus. Equity flows have been negative for the past two weeks, with the 5-day average now -$28m vs the 20-day average at -$11m

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| China (Yuan bn)* | -2.1 | -14.4 | 31.8 |

| South Korea (USDmn) | -394 | 260 | 8449 |

| Taiwan (USDmn) | 588 | 2231 | 7036 |

| India (USDmn)** | 686 | 1426 | -1738 |

| Indonesia (USDmn)** | 5 | -132 | 1089 |

| Thailand (USDmn) | -72 | -141 | -929 |

| Malaysia (USDmn) ** | -95 | -342 | 114 |

| Philippines (USDmn) | 0 | 32.9 | 241 |

| Total (Ex China USDmn) | 717 | 3335 | 14262 |

| * Northbound Stock Connect Flows | |||

| ** Data Up To March 6 |

OIL: Higher, But Modestly Lower For The Week Amid Mixed Supply/Demand Signals

The active Brent futures (K4) is marginally higher in the first part of Friday dealing. Last near $83.45/bbl, this is 0.55% firmer on end Thursday levels, but little changed versus end levels from last week. We have had a little over 20cent range since the open, as markets await the US NFP print later. For WTI (J4) we were last near $79.50/bbl, up nearly 0.80% for the session so far, but slightly lower for the week.

- To a large extent oil is being buffeted by the weaker USD trend, which has emerged this week and is supportive, against signs of higher non-OPEC supply. The China demand outlook remains uncertain as well.

- The head of China's CNPC stated that the country has entered a period of lower growth for oil. That is, demand will still rise, but at a reduced pace compared to prior (see this BBG link).

- Disruptions from the Keystone pipeline (service the US from Canada) raised supply concerns on Thursday, but the operator said it was only temporarily paused and there was no crude released (BBG).

- Elsewhere, Kuwait Petroleum Corp is swapping cargoes with suppliers in order to avoid sailing via the Red Sea, KPC’s CEO Sheikh Nawaf Al-Sabah said, cited by Bloomberg. Industry consultant FGE stated that Brent can rise to $90/bbl by Q3 (see this BBG link).

- The technical backdrop for Brent looks supportive, with focus on March 1 highs at $84.34/bbl.

GOLD: Slightly Weaker After Another Record High On Thursday

Gold is slightly weaker in the Asia-Pac session, after closing 0.5% higher at $2159.98 on Thursday after pushing to a fresh record high of $2164.78.

- The precious metal was supported by lower US Treasury yields and further weakness for the USD index.

- US tsys rallied through technical resistance early in the NY session after lower-than-expected Unit Labor Costs (0.4% vs. 0.7% est). Weekly jobless claims were largely in line: (216k vs. 217k est) while Continuing Claims rose (1.906M vs. 1.880M est; prior down-revised to 1.898M from 1.905M)). Additional data: Nonfarm Productivity (3.2% vs. 3.1% est); Trade Balance (-$67.4B vs. -$63.5B est).

- No new insight from Fed Chairman Powell on Thursday as he repeated yesterday's policy testimony to Congress.

- Bullion has added more than 6% over the last seven sessions.

- (Bloomberg) The precious metal’s sharp jump “has surprised us in its intensity, and outpaced cues” from foreign exchange and rates markets, said JPMorgan Chase & Co. analysts including Gregory Shearer in a note.

- The next resistance is $2177.6 (Fibonacci projection), according to MNI's technicals team.

ASIA FX: USD/Asia Pairs Lower On Better Equity Sentiment, CNH Lagging Still

USD/Asia pairs are lower across the board, except for a steady CNH trend. The won has been the strongest performer in spot terms, while MYR and IDR have also posted solid gains. NDF markets have also shown USD losses, albeit to a reduced degree compared to spot markets. A positive regional equity backdrop has weighed on the USD, while a slightly weaker dollar against the Yen and AUD has also helped. We have Taiwan trade figures later, while tomorrow delivers China inflation data for Feb.

- USD/CNH sits near 7.2000 in latest dealings, little changed for the session. We did dip to 7.1946 in early trade, as the USD index sank to fresh multi week lows. However, there was no follow through. Onshore China equities are lagging the better regional trend for other Asia Pac markets, which may be weighing on the yuan at the margins.

- Looking ahead, Saturday delivers Feb inflation data. The CPI is expected to rise to 0.3%y/y from -0.8% in Jan. The PPI is expected to be unchanged in y/y terms at -2.5%. The headline CPI may be aided by higher food/restaurant services prices in the month, given the timing of LNY. Similar trends have been evident in South Korea and Taiwan Feb CPI prints. Next Friday we have the 1yr MLF decision. No change is expected in terms of the rate, currently, 2.5%. Expectations are for easier policy settings, but it may too soon for an adjustment in this rate. Also due on the same day is Feb house price data, which will be in focus given tentative signs in Jan of slightly better price trends. Next week should also deliver Feb new loans and aggregate finance data. This is expected to slow noticeably from Jan levels, but this is the typical seasonal norm.

- 1 month USD/KRW has broken lower, the pair last near 1318.5, which is very close to the 200-day EMA. In recent sessions the pair has broken down through the 50 and 100-day EMAs. A generally positive global equity backdrop, coupled with lower US yields, have been key won supports in recent sessions, along with the break lower in USD/JPY. We had earlier data on the Jan current account and goods balance, which showed reduced surpluses compared to Dec last year.

- USD/IDR spot is down around 0.30% in the first part of dealing on Friday, last at 15605. This is just up from session lows near 15590. IDRs pot gains largely reflect IDR NDF gains through US trade on Thursday. The 1 month USD/IDR NDF is only slightly stronger in rupiah terms, last near 15620. Broadly, IDR gains in recent sessions appears to reflect some catch up with a softer US yield backdrop. The real yield peaked back in late Feb, but month end USD demand may have delayed IDR reaction.

- As was the case at yesterday's open, USD/MYR was sharply weaker in the first part of trade. The pair touched 4.6768, fresh lows back to mid-Jan. We have stabilized somewhat since then, last just above 4.69. We are still +0.30% firmer in ringgit terms. The currency is still the top performer in the EM Asia space over the past week, up nearly 1.2%. The central bank characterized MYR as undervalued and that it continues to encourage government linked corporations to repatriate offshore earnings. The latter has been a key turnaround in MYR's fortunes since it became a focus point for the authorities and the Prime Minister.

- Elsewhere, THB is around 0.20% firmer, last near 35.50 for USD/THB, fresh lows back to the first half of Feb. USD/PHP is down by the same amount, the pair last near 55.73. Earlier data showed a tick up in the unemployment rate, back above 4%, but we are only back to end Sep levels from last year.

INDONESIA: Indonesia Sov Curve Flatter, Front-End Underperforms Tsys

Indonesian USD sovereign debt curve has flattened today with yields 1-4bps lower lagging the move lower in the front end made by US Treasuries on Thursday

- The 2Y yield is 1bps lower at 4.88%, 5Y yield is 3bps lower at 4.85%, the 10Y yield is 2bps lower at 4.94%, while the 5-year CDS is down 1bp to 60.5bps.

- The Indon to US Treasury spread difference widen over the past few days with the front end under-performing. The spread difference for the 2yr is 38bps, 5yr is 36bps, while the 10yr is 86bps. Looking back over the week the 2yr is 10bps tighter, 5yr 1bp tighter while the 10yr is 8bps wider

- In cross-market moves, the USD/IDR is 0.32% lower, the JCI is 0.37% higher, while US Tsys yields are unchanged

- Foreign investors sold Indonesian debt again on Wednesday at a net flow of -$132m. Short-term, investors have largely been sellers, with a 20-day average daily flow currently at -$36m, while longer-term trends still remain positive with the 100-day average at +$4.8m.

PHILIPPINES: Philippines Sov Curve Flatter, Unemployment Rises

The Philippines USD sovereign debt curve has flattened today with yields 1-4bps lower lagging the move lower in the front end made by US Treasuries on Thursday

- The 2Y yield is 1bp lower at 4.78%, 5Y yield is 4bps lower at 4.84% the 10Y yield is 3bp higher at 4.94%, while 5yr CDS is down -1bps to 60.50bps

- The Philip to US Treasury spread difference widen over the past day with the front end under-performing. The spread difference for the 2y is 28bps, the 5yr is 34bps, while the 10yr is 86bps. Looking back over the month the front end has outperformed with the 2y spread closing 15bps, the 5yr is just 1bp tighter, while the 10yr is 8bps wider

- Cross-asset moves: the USD/PHP is down 0.13%, PSEi Index is 0.73% higher, Corporate Credit curve is 2-8bps tighter over the week with better buying at the 4-5yr maturity, while US Tsys unchanged

- Earlier Philippines Unemployment rate came in at 4.5% vs 3.2% expected and up from 3.1% in Dec, while Money supply rose 6% YoY in Jan vs a revised 6.2% in December

- Looking Ahead, Trade Balance data is due on Tuesday.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 08/03/2024 | 0700/0800 | ** |  | DE | Industrial Production |

| 08/03/2024 | 0700/0800 | ** | | DE | PPI |

| 08/03/2024 | 0700/0800 | ** |  | SE | Private Sector Production m/m |

| 08/03/2024 | 0745/0845 | * |  | FR | Foreign Trade |

| 08/03/2024 | 0800/0900 | ** |  | ES | Industrial Production |

| 08/03/2024 | 0900/1000 | ** |  | IT | PPI |

| 08/03/2024 | 1000/1100 | *** |  | EU | GDP (final) |

| 08/03/2024 | 1000/1100 | * | | EU | Employment |

| 08/03/2024 | 1200/0700 |  | US | New York Fed's John Williams | |

| 08/03/2024 | 1330/0830 | *** |  | CA | Labour Force Survey |

| 08/03/2024 | 1330/0830 | *** | | US | Employment Report |

| 08/03/2024 | 1700/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 08/03/2024 | 1800/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.