Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Subdued trading session in Asia on Friday, very few headlines with just Japanese CPI data which came in just below estimates

- Equities were weaker on the back of cheaper semiconductor prices during the US session, the Philadelphia SE Semiconductor index fell 2.69% on Thursday

- Local rates have largely tracked US tsys, and have bounced of session lows although still trade well within yesterday ranges

Source: MNI - Market News/Bloomberg

MARKETS

US TSYS: Treasury Futures Off Earlier Lows Ahead Of US PMIs

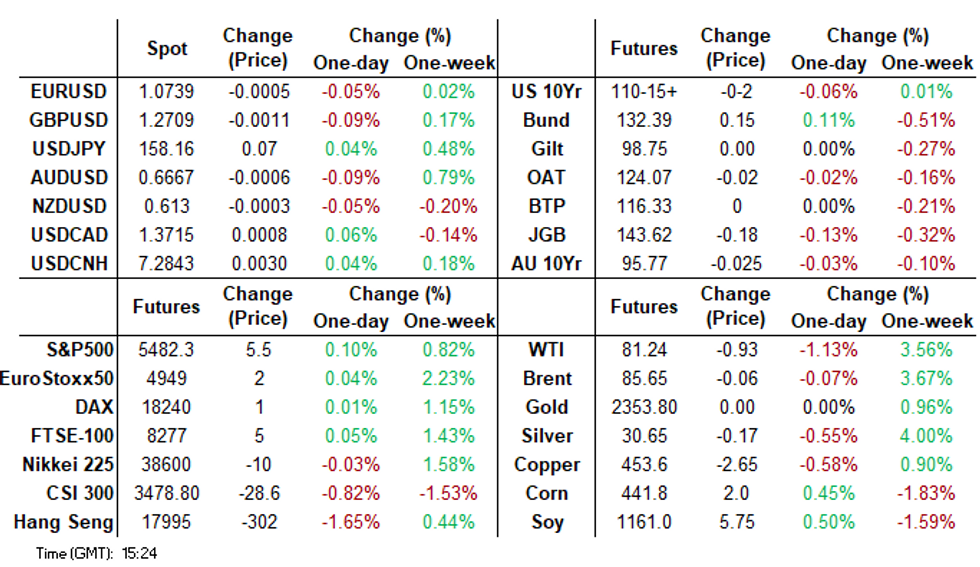

- Treasury futures have moved off session lows and trade only slightly lower on the day. TUU4 is -0-00¾ at 102-05⅝ after making a low of 102-05, while TYU4 is -0-02+ at 110-15, after earlier reaching a low of 110-12+, we trade well within yesterday's ranges.

- Volumes are on the low side today with TU 17k, FV 29k, TY 52k

- The cash treasury curve is little changed, yields are flat to 0.5bp lower, with the 2Y +0.1bp at 4.749%, 5Y unch at 4.274% while the 10Y is -0.2bp at 4.257%.

- APAC: ACGBs are 2-4bps cheaper, curve steeper. NZGBs are 2-3bps cheaper while JGBs are 1-3bps cheaper, better selling seen through the belly. The JPY continues to weaken and is now trading back around 159.00.

- Fed's Thomas Barkin stated he needs more clarity on inflation before supporting interest rate cuts, emphasizing the importance of sustained progress towards the Fed’s 2% target and suggesting that current conditions do not warrant forward guidance on future policy adjustments. He reiterated that the Fed's policy is well-positioned and that any rate cuts would be data-dependent.

- Looking ahead, S&P Flash PMIs, Leading Index, Home Sales.

NZGBS: Subdued Session, Light Local Calendar Next Week

NZGBs closed 2-3bps cheaper but off the session’s worst levels. With the domestic calendar light, the move away from the session’s yield high appeared tied to a similar move by cash US tsys. Currently, US tsys are dealing flat to 1bp cheaper in today’s Asia-Pac session after yesterday’s 2-5bp cheapening.

- Swap rates are 1-2bps higher, with the 2s01s curve steeper.

- RBNZ dated OIS pricing is slightly firmer for 2025 meetings. A cumulative 29bps of easing is priced by year-end.

- Next week, the local calendar is light, with Trade Balance data on Monday and Consumer and Business Confidence on Thursday.

- Later today, the US calendar will see S&P Flash PMIs, Leading Index and Home Sales.

ACGBS: Drifted Cheaper, Post-RBA Adjustment Continued, CPI Monthly On Wednesday

ACGBs (YM -4.0 & XM -4.5) are cheaper and at/near Sydney session lows. With the domestic calendar light, the local market took its cue from cash US tsys, which are dealing flat to 1bp cheaper in today’s Asia-Pac session after yesterday’s modest sell-off.

- That said, ACGB market weakness also likely reflects an ongoing adjustment by local participants to the RBA’s hawkish hold on Tuesday.

- RBA-dated OIS pricing is 6-12bps firmer for meetings beyond August versus pre-RBA levels. 6bps of easing is priced by year-end from an expected terminal rate of 4.37%.

- Cash ACGBs are 3bps cheaper. The AU-US 10-year yield differential is at -2bps, the highest level since February. The AU-NZ 10-year differential, at -38bps, is also near the highest level for the year. The lowest level was -65bps.

- Swap rates are 2bps higher.

- The bills strip has bear-steepened, with pricing -1 to -5.

- Next week, the local calendar will see the sale of A$900mn of the 3.25% Apr-29 bond on Monday, Westpac Consumer Confidence on Tuesday and May’s CPI Monthly on Wednesday.

- RBA Christopher Kent, Assistant Governor (Financial Markets), will give a speech at the ABA Banking Conference on Wednesday.

JGBS: Futures Holding Cheaper, June’s BoJ Summary Of Opinions On Monday

JGB futures are weaker but above session cheaps, -18 compared to settlement levels.

- Outside of the previously outlined National CPI and Jibun Bank PMIs, there hasn't been much in the way of domestic drivers to flag.

- (MNI) The Bank of Japan's June Tankan survey will show little change among major business sentiment over the past three months, while small- and major firms' capital investment plans will remain solid, economists told MNI (see Main Wire).

- (MNI) BoJ officials will focus on branch-manager meetings on July 8 to gauge wage hikes at smaller firms and the impact of the weak yen on corporate price-setting behaviour. They are also focused on how inflation expectations held by businesses, which are rising, have evolved amid slowing price hikes and weak private consumption (see Main Wire).

- Cash US tsys are flat to 1bp cheaper in today’s Asia-Pac session after yesterday’s modest sell-off.

- The cash JGB curve has bear-steepened, with yields flat to 2bps higher. The benchmark 10-year yield is 1.8bps higher at 0.975% versus the cycle high of 1.101%.

- Swaps are mostly modestly cheaper across the curve, with rates flat to 1bp higher. Swap spreads are mostly tighter.

- The local calendar will see BoJ's Summary of Opinions (June MPM) and Department Store Sales on Monday.

ASIA STOCKS: Hong Kong & China Markets Head Lower, Tech Stocks Worst Performers

The Hong Kong and China markets are experiencing declines today, Hong Kong markets are performing worse than China onshore equities with markets concerned about economic recovery and geopolitical tensions persist. The Shanghai Stock Exchange Composite Index fell below the 3,000-point level for the first time since March, impacted by Beijing’s reluctance to implement further stimulus and stringent regulatory policies. Additionally, reports of Canada potentially boosting tariffs on Chinese electric vehicles added to the market headwinds.

- Hong Kong equities are lower across the board today with tech stocks the worst performing following a sell-off in US semiconductor stocks over night, the HSTECH Index is down 2.15%, property isn't trading much better with the Mainland Property Index down 1.23%, while the HS Property Index is down 1.25%, the wider HSI is off 1.71%.

- China onshore equities are also lower today with the CSI 300 Index down 0.60%. Small-cap indices also fell but holding up better than other parts of the market, with the CSI 1000 down 0.15% and the CSI 2000 down 0.26%.

- Property space, Chinese developer Road King Infrastructure is facing potential default unless investors agree to its proposed bond buyback at discounted rates and extend repayment terms for other debts. The company warned that failure to secure these measures could lead to payment defaults, highlighting ongoing liquidity challenges in China's property sector despite government support efforts. China Vanke plans to raise approximately 1 billion yuan by listing its long-term rental business, Boyu, through a real estate investment trust (REIT) in China. This move is part of Vanke's efforts to enhance liquidity amid ongoing financial challenges, including exploring asset sales and securing a large bank loan to avoid potential defaults in the property sector crisis.

- Looking ahead to next week and it is a light calendar for China, while Hong Kong has trade balance data on Tuesday

ASIA STOCKS: Asian Equities Mixed As Tech Stocks Weigh On Market

Asian stock markets experienced mixed performances, with the MSCI Asia Pacific Index dropping 0.4% in early trading, weighed down by losses in South Korean and Chinese shares, while Japanese stocks rose. The decline was influenced by a sell-off in US tech stocks and a stronger US dollar. Japanese inflation data showing acceleration due to rising energy costs bolstered the case for potential interest rate hikes, while yen weakness heightened the risk of market intervention by Japanese officials.

- Japanese equities opened higher this morning, driven primarily by financial stocks amid speculation that the Bank of Japan might tighten its policy due to yen weakness and rising inflation. Exporters also benefited from a weaker yen, with Keyence Corp., which earns a significant portion of its revenue overseas, contributing significantly with a 2.2% gain. The Nikkei advanced slightly by 0.1% to 38,669.57, although chip-related shares like Advantest led losses, reflecting trends from US markets, while the Topix is 0.30% higher.

- South Korean equities are lower today with the Kospi falling by as much as 1.1%, marking its first loss in four sessions, as chip stocks like Samsung and SK Hynix dropped following declines in US tech stocks. SK bid for a market upgrade from MSCI was hindered by the reimposition of a short-selling ban, maintaining its emerging market status. Despite reforms aimed at improving market accessibility. Local funds were net sellers of Kospi equities, while retail investors were net buyers. Despite this decline, the Kospi remained on track for its third consecutive weekly gain. The small-cap Kosdaq Index is down 0.40%

- Taiwan equities have opened lower today with the Taiex opening 0.5% lower at 23 with semiconductor stocks leading the decline. Taiwan Semiconductor Manufacturing Co. (TSMC) was the biggest contributor to the index's drop, decreasing by 0.8%.

- Australia equities are little changed today, earlier we had Judo Bank PMI data with the composite showing a drop from 52.1 to 50.6. Gains in Consumer Staples/Discretionary, Health Care & Real Estate have been offset with declines in Financials and Materials.

- Elsewhere, New Zealand equities are unchanged for the day, Indonesian equities are 0.75% higher, Singapore equities are 0.30% higher, Malaysian equities are 0.15% higher while Philippines equities are down 0.60%.

ASIA STOCKS: Asian Equity Flows Continue Trend

- South Korean equities were higher on Thursday (Kospi up 0.37%, Kosdaq up 0.43%). Flows were slightly above short term averages with the past 5 sessions have netting a total inflow of $1.36b. The Kospi hit new cycle highs on Thursday before selling off Friday morning. The 5-day average is $272m, above both the 20 day average of $82m and the longer-term 100-day average at $154m.

- Taiwan equities were higher on Thursday with another strong inflow of $1.07b. The Taiex continues to make new all time highs and is now up 4.20% for the week, with the majority of gains coming from TSMC. The past 5 session's have seen a total inflow of $3.77b with the 5-day average now $755m, above both the 20-day average at $92m, while the 100-day average is $85m.

- Thailand equities were lower on Thursday, largely erasing the gains made on Wednesday. Foreign investors have sold equities for 21 straight sessions, for a total outflow of $1.12b, the past 5 days seeing $267m in outflows. The 5-day average is now -$53.5m, below both the 20-day average at -$52m and the 100-day average at -$24.5m.

- Philippines equities were slightly lower on Thursday making new ytd lows. Foreign investors have been better sellers of equities recently with seven straight days of selling, with the past 5 sessions have seen a net outflow of $30.5m. The 5-day average is now -$6.1m, slightly above the 20-day average at -$11m, but inline with the long term average at -$5.70m

- Indonesian equities rallied 1.36% on Thursday, although the JCI is still down 2.18% for the past 5 trading sessions. Foreign investors have been better sellers of stocks recently apart from a decent inflow on the 13th, otherwise it has been 18 of the past 19 days of selling. The 5-day average is $8.5m, above the 20-day average at -$28m and the 100-day average at -$7m

- Indian equities were slightly higher on Thursday, and now trade 1% higher for the week. Foreign investors have been better buyers post the election the other week, with 8 straight days of inflows for $1.1b. The 5-day average is $417m, above the 20-day average at $69m, and the 100-day average at $21m

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | 314 | 1362 | 16951 |

| Taiwan (USDmn) | 1071 | 3777 | 7061 |

| India (USDmn)** | 1100 | 2089 | -1710 |

| Indonesia (USDmn) | -6 | 43 | -527 |

| Thailand (USDmn) | -53 | -267 | -2949 |

| Malaysia (USDmn) ** | -26 | -31 | -46 |

| Philippines (USDmn) | -9 | -30.5 | -505 |

| Total | 2390 | 6943 | 18276 |

| ** Up to 19th June |

GOLD: Buoyed By Weaker Than Expected US Economic Data

Gold is little changed in the Asia-Pac session, after closing 1.4% higher at $2360.09 on Thursday.

- Bullion received a boost from weaker-than-expected US data that potentially strengthened the case for the Federal Reserve to pivot to monetary easing later this year.

- Housing Starts (1.277M vs. 1.37M est), MoM (-5.5% vs. 0.7% est), Building Permits (1.386M vs. 1.45M est), MoM (-3.8% vs. 0.7% est). Weekly Claims a little higher than expected at 238k vs. 235k est, continuing claims 1.828M vs. 1.810M est.

- Nevertheless, gold is in consolidation mode, with initial firm resistance at $2387.8, the Jun 7 high, according to MNI’s technicals team. Support is at $2,277.4, the May 3 low.

- Silver also rallied yesterday, achieving its highest level since June 7. For silver, key resistance is at $32.518, the May 20 high, while support to watch lies at the 50-day EMA, at $28.979.

FOREX: USD Down Against G10 Currencies, Ranges Tight On Light Data

The USD has slipped today, down again all G10 currencies with the BBDXY down 0.07% at 1,266.82. Focus in the APAC region has been on whether or not the BoJ will intervene in the currency, earlier we had Japanese CPI which came in below expectations, the currency initially traded above 159.00, before paring gains to trade unch for the day.

- NZDUSD is a touch higher today, up 0.10% at 0.6125. The pair is trading at the bottom end of the monthly ranges, with 0.6100 acting as support.

- AUDUSD is 0.18% higher at 0.6667 and currently at sessions best levels, although well within yesterday's ranges. AUDNZD is little changed today at 1.0884 near monthly highs.

- USDJPY is little changed at around 158.87 after earlier breaching 159.00, the pair has slid about 1% this week. Concerns remain around another intervention.

- EURUSD has edged higher since the open up 0.14% at 1.0717 at sessions best, although we still trade towards the bottom of the weeks ranges.

- The USDCNY fix today was 107pips wider than yesterday making new cycle wides. USDCNH sold off on the back of the fixing to 7.2840, we have recovered some of those moves but the pair is trading heavy at 7.2858 currently.

- The USDKRW gapped higher this morning and has been slowly giving up those gains, we now trade 0.22% at 1,387.15 vs 1,392.95 highs.

- Later we have UK retail sales, EU PMIs & US PMIs and Existing Home

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 21/06/2024 | 0600/0700 | *** |  | UK | Retail Sales |

| 21/06/2024 | 0600/0700 | *** | | UK | Public Sector Finances |

| 21/06/2024 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 21/06/2024 | 0700/0900 |  | EU | ECB's De Guindos participates in ECONFIN meeting | |

| 21/06/2024 | 0715/0915 | ** | | FR | S&P Global Services PMI (p) |

| 21/06/2024 | 0715/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 21/06/2024 | 0730/0930 | ** |  | DE | S&P Global Services PMI (p) |

| 21/06/2024 | 0730/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 21/06/2024 | 0800/1000 | ** | | EU | S&P Global Services PMI (p) |

| 21/06/2024 | 0800/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 21/06/2024 | 0800/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 21/06/2024 | 0830/0930 | *** | | UK | S&P Global Manufacturing PMI flash |

| 21/06/2024 | 0830/0930 | *** | | UK | S&P Global Services PMI flash |

| 21/06/2024 | 0830/0930 | *** | | UK | S&P Global Composite PMI flash |

| 21/06/2024 | 1230/0830 | * |  | CA | Industrial Product and Raw Material Price Index |

| 21/06/2024 | 1230/0830 | ** | | CA | Retail Trade |

| 21/06/2024 | 1230/0830 | ** |  | US | WASDE Weekly Import/Export |

| 21/06/2024 | 1345/0945 | *** | | US | S&P Global Manufacturing Index (Flash) |

| 21/06/2024 | 1345/0945 | *** | | US | S&P Global Services Index (flash) |

| 21/06/2024 | 1400/1000 | *** | | US | NAR existing home sales |

| 21/06/2024 | 1530/1630 | | UK | BoE APF Sales Schedule for Q3 | |

| 21/06/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.