Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- A block buy in TY futures (+1,750) and news that the latest North Korean missile test resulted in an ICBM falling into Japanese waters (with no damage to Japanese assets reported) allowed the space to unwind the modest downtick that came in early Asia-Pac trade, after regional participants initially followed Thursday’s cheapen, albeit in a limited manner.

- The yen was resilient amid risk-on flows elsewhere in the G10 FX space, with the Antipodeans leading gains, while the USD and CHF lagged behind. Spot USD/JPY rejected intraday resistance from Y140.50 and gave back initial gains. Reports of a North Korean missile test involving an ICBM capable of reaching U.S. mainland failed to provoke any broader flip in market sentiment.

- Looking ahead, focus on the data front turns to U.S. existing home sales, UK retail sales and Norwegian GDP. Comments are due from ECB's Lagarde, Nagel & Knot, Fed's Collins, as well as BoE's Mann & Haskel.

US TSYS: A Touch Firmer As North Korean Missile Test Helps Unwind Early Downtick

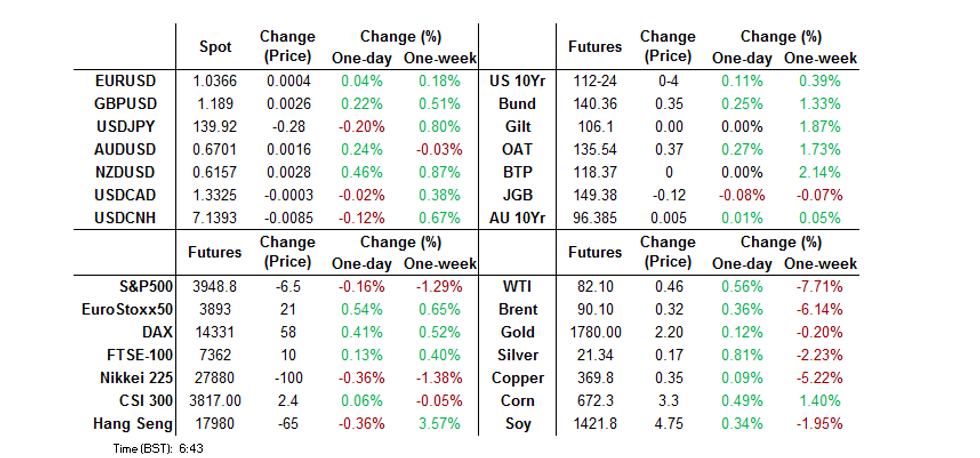

TYZ2 prints +0-02+ at 112-22+, 0-01 off the peak of its 0-08 overnight range, on volume of ~71K. Cash Tsys run flat to 1.5bp richer into London hours.

- A block buy in TY futures (+1,750) and news that the latest North Korean missile test resulted in an ICBM falling into Japanese waters (with no damage to Japanese assets reported) allowed the space to unwind the modest downtick that came in early Asia-Pac trade, after regional participants initially followed Thursday’s cheapen, albeit in a limited manner.

- The 2-/10-Year yield spread continues to hover within a couple of bp of the deepest levels of inversion witnessed during the current cycle (which printed on Thursday, in lieu of hawkish rhetoric from St. Louis Fed President Bullard).

- Outside of the aforementioned block buy of TY futures, Asia-Pac trade also saw some buying of the TYZ2 112.00/111.50 1x2 put spread on screen.

- Looking ahead, NY hours will bring existing home sales data and Fedspeak from Collins. We will also see a joint round of comments from President Biden & Tsy Sec Yellen.

JGBS: Twisting Flatter, No Lasting Reaction To North Korean Missile Launch

Cash JGBs run 2bp cheaper to 0.5bp richer across the curve, with only 40s firming on Friday. Influence from Thursday’s wider core global FI trade seemingly crept in. Meanwhile, futures print -10 ahead of the bell and have struggled to turn bid all day.

- Domestic CPI data may also have had some minor impact on price action. The 3 major CPI metrics all topped consensus estimates by 0.1ppt, as the major Y/Y inflation rates moved 0.6-0.7ppt higher vs. previous readings. The readings won’t be a gamechanger for the BoJ, with the Bank committed to maintaining its ultra-loose policy settings, as it looks to foster meaningful wage growth in a bid to develop demand-pull, not cost-push, inflation.

- The home bias of Japanese investors that we have discussed previously will likely have aided the flattening move.

- There wasn’t much in the way of tangible, lasting reaction to the latest North Korean missile test, which saw an ICBM fall in the sea which is covered by Japan’s EEZ (there was no damage reported re: Japanese assets). Language from Japanese, South Korean & U.S. leadership has condemned the action, as you would expect.

- Elsehwere, policymaker rhetoric failed to inspire anything in the way of meaningful price action, offering little new for participants to trade off.

- Looking ahead, BoJ Rinban operations covering 1- to 10-Year JGBs headlines domestic matters on Monday.

AUSSIE BONDS: Firmer In The Second Half, Lowe’s Speech Now Eyed

There was little in the way of idiosyncracies to drive the Aussie bond space ahead of the weekend, leaving futures to meander through the final Sydney session of the week, with YM closing -2.0, in line with late overnight levels, while XM was +0.5, as the flattening impetus from wider core FI trade on Thursday was maintained. Wider cash ACGBs run 2bp cheaper to 5.5bp richer, pivoting around 10s.

- EFPs were essentially unchanged on the day.

- Early rounds of trade were driven by reaction to Thursday’s cheapening in wider core global FI markets, before the latest North Korean missile test (which saw the ICBM fall into the sea covered by Japan’s EEZ) provided a bid.

- The latest round of ACGB Nov-29 supply went well.

- Next week’s AOFM issuance slate is pretty vanilla, with ACGB Apr-25 & ACGB May-32 set to come to market.

- Bills finished +1 to -2 through the reds, with some light twist steepening seen.

- Looking ahead, next week’s local docket is lacking when it comes to major economic releases, with the flash S&P Global PMI prints providing the only real point of note. That means that it will be Governor Lowe’s Tuesday dinner address (on “Price Stability, the Supply Side and Prosperity”) that headlines the domestic docket.

NZGBS: Cheaper Ahead Of Weekend, Pre-RBNZ Hedging May Have Weighed

Cash NZGBs were cheaper ahead of the weekend, with the early uptick in yields seeing a modest extension through the day, as the major benchmarks finished the final session of the week 3.5-5.0bp cheaper. The curve came under some light bear flattening pressure.

- This came even as U.S. Tsys richened incrementally during Asia-Pac hours, with payside swap flow in the front end of the NZ curve seemingly aiding the cheapening, as both 2- & 5-Year swap spreads widened, while swap spreads further out the curve were little changed to a touch tighter.

- This payside flow may have been a case of participants putting some pre-RBNZ hedges into place, with RBNZ dated OIS now pricing 65bp of tightening for next week’s meeting, alongside a terminal cash rate of just below 5.10%, with both moving incrementally higher on the day.

- The aforementioned RBNZ decision headlines next week’s domestic docket, with 10 of the 14 surveyed by BBG looking for a super-sized 75bp step from the Bank, after a run of consecutive 50bp moves.

- Elsewhere, the monthly credit card spending, trade balance and ANZ consumer confidence data is slated, with Q3 retail sales volume also due.

FOREX: Yen Outperforms Safe Haven Peers, Yuan Stages Firm Rebound

The yen was resilient amid risk-on flows elsewhere in the G10 FX space, with the Antipodeans leading gains, while the USD and CHF lagged behind. Spot USD/JPY rejected intraday resistance from Y140.50 and gave back initial gains. Reports of a North Korean missile test involving an ICBM capable of reaching U.S. mainland failed to provoke any broader flip in market sentiment.

- The yen initially found Japan's CPI report uninspiring, albeit garnered some strength as the session progressed. Core consumer inflation picked up to +3.6% Y/Y in October from +3.0% prior, beating the median estimate of +3.5%, which is unlikely to persuade the BoJ to change tack. After the release, central bank Governor Kuroda said that the current inflation situation isn't sustainable.

- USD/CNH snapped a three-day winning streak, potentially on the back of headlines that Hong Kong has approved emergency use of the BioNTech Bivalent vaccine. Bloomberg cited trader sources flagged dollar sales by Chinese state-owned banks as a factor behind yuan rebound.

- Gains for offshore yuan spilled over into the outperforming Antipodeans, prompting them to refresh session highs. AUD/NZD extended its losing streak to five consecutive days.

- Looking ahead, focus on the data front turns to U.S. existing home sales, UK retail sales and Norwegian GDP. Comments are due from ECB's Lagarde, Nagel & Knot, Fed's Collins, as well as BoE's Mann & Haskel.

FX OPTIONS: Expiries for Nov18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0200(E739mln), $1.0225-50(E1.3bln), $1.0300(E836mln), $1.0450(E2.6bln)

- USD/JPY: Y138.00($770mln), Y138.90-00($615mln), Y139.45($567mln), Y140.50($1.3bln)GBP/USD: $1.1700(Gbp560mln)

- AUD/USD: $0.6650-60(A$1.1bln)

- USD/CAD: C$1.3325($1.2bln)

- USD/CNY: Cny7.0500($3.3bln), Cny7.1500($3.0bln), Cny7.2000($2.2bln)

ASIA FX: Mixed End To The Week, Despite Softer USD Against The Majors

USD/Asia pairs have been mixed, this comes despite a generally softer USD tone against the majors. USD/CNH moved lower but there wasn't much follow through, likewise for USD/KRW. THB and PHP have held onto gains, while IDR remains a laggard. Next Monday, the focus will be on China's LPR announcements, although no change is expected. South Korea's first 20-days of trade data for November also prints.

- USD/CNH slipped to the low 7.1200 region, but has since recovered towards 7.1400. Positive covid vaccine headlines for HK looked like a catalyst but there was much follow through. Bloomberg also notes reports of USD selling in the morning session from state banks, which may have been a catalyst as well.

- USD/KRW was softer at the open, as positive equity sentiment spilled over into the FX space. We couldn't get below 1336 though, and we now sit back above 1340. North Korea's ICMB test has taken the shine off South Korean assets today.

- Spot USD/IDR has added 30 figs and changes hands at 15,693, with bulls looking to force their way through Nov 4 high of 15,750. Bears take aim at Nov 11 low/50-DMA at 15,393/15,372. Bank Indonesia raised the 7-Day Reverse Repo Rate by 50bp Thursday, which was the base-case scenario of most analysts. The decision was described as a "front-loaded, preemptive and forward looking step," signalling the central bank's resolve in containing inflation as quickly as possible.

- Spot USD/PHP trades -0.07 at 57.305. Bangko Sentral ng Pilipinas delivered the expected 75bp rate hike Thursday, which was preannounced well ahead of the meeting. The 2022 inflation projection was raised to +5.8% Y/Y from +5.6% at the September monetary policy review, with the 2023 forecast raised to +4.3% from +4.1%.

- BoT Asst Gov Piti hinted that the central bank will stick to its "measured and gradual" approach to monetary tightening. Outflows of foreign capital from Thailand's equity market continued Thursday, with offshore investors shedding a net $92.57mn in Thai stocks, the largest net drain since Sep 15. Still, USD/THB is slightly lower for the session, last -0.04 figs at 35.85.

EQUITIES: Early Optimism Doesn't Have Much Follow Through

Early positive impetus in the equity space has given way to a more cautious tone in regional equities as the session has progressed. Most markets are away from best levels, with some markets slipping into negative territory. US equity futures have struggled to stay in positive territory as well.

- HSI opened up firmer, buoyed by China tech stock gains in the US overnight. The market was pleased with Alibaba's buyback plan, while China gaming stocks rallied on fresh approvals from regulators on new games.

- The HSI tech sub-index is up around 3.40% currently, although down from session highs. The broader HSI index is up a more modest 0.56%. There hasn't been much positive impetus from headlines that the Biontech Bivalent covide vaccine has approved for emergency use.

- China stocks are around flat, with the CSI 300 +0.07%, but Shanghai Composite slightly down. A PBoC advisor stated China's growth target should be at least 5% next year, with higher levels possible if Covid restrictions are lifted in the first half.

- The Kospi opened up firmer, buoyed by a Goldman Sach's upgrade, but has trimmed gains as the session progressed. We currently sit +0.20%, just under 2448, we were above 2470 in the first part of the session. North Korea's reported ICBM test has likely taken the shine of South Korean assets, although the impact doesn't look large.

- Moves elsewhere have been mixed, the Nikkei 225 couldn't hold early gains (last at -0.10%), while the Taiex is down -0.25% at this stage. The ASX 200 is up modestly, last +0.20%.

GOLD: On Track For First Weekly Loss Since End October

Gold is tracking higher for the first time since Tuesday, after dropping over 1% through the middle part of this week. The precious metal was last close to $1764, still on track for a modest weekly loss, which would be the first since late October.

- We are currently +0.20% higher from NY closing levels, which is in line with pull back in USD sentiment, the BBDXY is down 0.2% so far for the session.

- Note the 200-day EMA comes in at $1760.4 level, which could act as a support point. We broke through this level overnight but managed to close higher (lows were just under $1755).

- US yields are holding close to overnight highs, which may limit gold's upside in the near term. Highs for the week sit around the $1785 region.

OIL: Back-To-Back Weekly Losses

Brent crude is back above $90/bbl, +0.90% on NY closing levels. Still, at this stage we are -5.65% lower for the week, which follows last week's -2.62% decline. Brent is below all key MAs and is not too far away from mid-October lows (just under $89/bbl). WTI sits close to $82.50/bbl currently, but traded below mid-October lows overnight.

- Forward curves are generally indicating reduced supply pressure rather than tighter markets. Supply pressures were generally seen as getter tighter in the lead up to the northern hemisphere winter, but that hasn't materialized yet. The Brent prompt spread is back to early September lows.

- The other factor is that optimism around China shifting away from its CZS may take time to generate stronger physical oil demand.

- Looking ahead the oil calendar is fairly light for the week ahead, outside of the weekly inventory reports. Focus is likely to rest on Wednesday round of preliminary PMI prints for the EU area and the US, as an update on the global demand picture.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/11/2022 | 0700/0700 | *** |  | UK | Retail Sales |

| 18/11/2022 | 0700/0800 | ** |  | SE | Unemployment |

| 18/11/2022 | 0700/0800 | ** |  | NO | Norway GDP |

| 18/11/2022 | 0830/0930 |  | EU | ECB Lagarde Speech at European Banking Congress | |

| 18/11/2022 | - | | EU | COP 27 Ends | |

| 18/11/2022 | - |  | TH | APEC Leaders’ Summit | |

| 18/11/2022 | 1330/0830 | * |  | CA | Industrial Product and Raw Material Price Index |

| 18/11/2022 | 1500/1000 | *** |  | US | NAR existing home sales |

| 18/11/2022 | 1500/1000 | * | | US | Services Revenues |

| 18/11/2022 | 1715/1715 | | UK | BOE Haskel Panels Ditchley Economics Conference |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.