Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

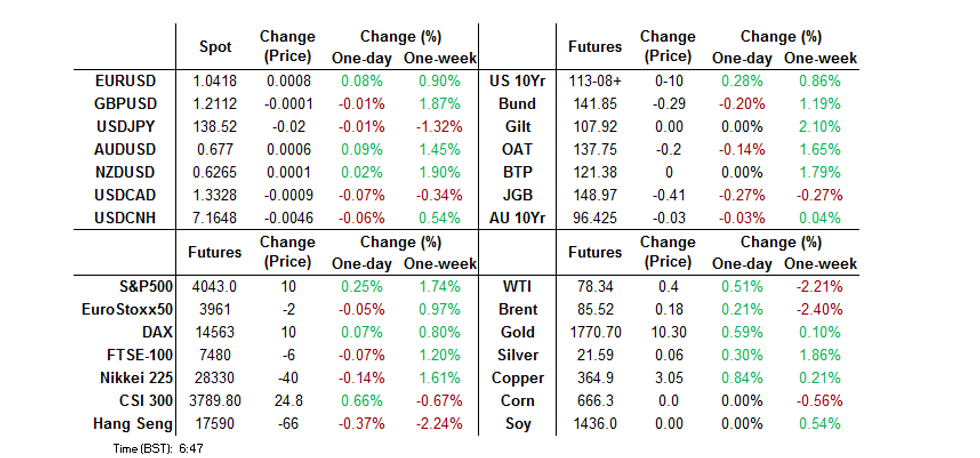

- The impact from the minutes covering the most recent FOMC meeting continued to be felt after the Thanksgiving holiday, with Tsys underpinned during Tokyo dealing.

- The post-Fed minutes downtick in the USD continued during Asia-Pac hours, with U.S. Tsys underpinned and continued focus on the seemingly impending slowing of Fed tightening evident. That left the greenback and the CHF at the bottom of the G10 FX pile in limited Asia-Pac dealing.

- ECB & Riksbank speak headline the broader macro docket on Friday, with wider market liquidity set to be thinned as many U.S. participants opt to take an elongated weekend in lieu of Thursday’s Thanksgiving holiday (note that U.S. markets will be subjected to shortened operating hours ahead of the weekend). A reminder that speculation/expectation surrounding a potential RRR cut from the PBoC is elevated after Wednesday's State Council meeting guided towards such a move. Many expect the PBoC to act after local market hours on Friday.

US TSYS: Underpinned In Asia

The impact from the minutes covering the most recent FOMC meeting continued to be felt after the Thanksgiving holiday, with Tsys underpinned during Tokyo dealing.

- That leaves the major cash Tsy benchmarks running 3-6bp richer into London hours, with bull steepening apparent. TYZ2 deals just shy of the peak of its 0-06 range, last +0-11+ (vs. Wednesday’s settlement) at 113-10.

- The impulse from a softer JGB complex in lieu of firmer than expected Tokyo CPI data provided a modest downtick for Tsys at one point, although the pressure was limited.

- Elsewhere, continued focus falls on the COVID situation in China, with localised restrictions in some of the country’s major cities tightening this week, while the new daily COVID case count metric hit a fresh record high today. Speculation/expectation surrounding a potential RRR cut from the PBoC is elevated after Wednesday's State Council meeting guided towards such a move. Many expect the PBoC to act after local market hours on Friday.

- ECB and Riksbank speak provides the highlights of the wider macro docket on Friday.

- A quick reminder that cash Tsys and Tsy futures will be subjected to holiday-shortened trading hours ahead of the weekend.

JGBS: Off Lows But Comfortably Cheaper after Firm Tokyo CPI Data

The JGB space operates off of worst levels into the bell, but is still comfortably cheaper on the day.

- Cash JGBs run little changed to ~4bp cheaper across the curve, with the early steepening giving way to 7s leading the weakness as futures remain heavy and the long end recovers from session lows, with life insurers and pension funds perhaps deploying capital after the passage of 40-Year JGB supply. Futures print ~40 ticks lower on the day ahead of the bell, operating a little off worst levels.

- Firmer than expected Tokyo CPI data provided the initial catalyst for the move lower, while the soft cover ratio observed at the latest round of 40-Year JGB supply promoted an extension of the early steepening momentum during the early rounds of afternoon dealing.

- There was also the potential for some delayed reaction to comments from Japanese Finance Minister Suzuki re: a desire to move away from short-term financing to factor into the steepening.

- Weekly Japanese international security flow data from the MoF revealed that foreign investors deployed the second largest ever round of net weekly purchases of Japanese bonds last week. This was probably a mix of short covering and perhaps some deployment of capital owing to advantageous FX-hedged yield pickups on offer.

- Note that the weekend will see BoJ Deputy Governor Amamiya appear at a meeting on monetary economics, while Monday’s domestic docket will be headlined by the latest round of BoJ Rinban operations.

AUSSIE BONDS: Supply Dynamics & RBA Speak Eyed

ACGBs corrected from worst levels in the latter rounds of Sydney trade, with spill over from a bid in U.S. Tsys helping after the impulse from a heavier impending weekly AOFM issuance slate (which includes ACGB Mar-47 supply) and weakness in JGBs applied pressure during the first half of the Sydney session. That left YM -2.0 & XM -3.0 at the bell with cash ACGBS running 2.5-3.5bp cheaper across the curve.

- Bills were flat to -3 through the reds, with light bear steepening in play. RBA dated OIS continue to price just over 20bp of tightening for next month’s RBA decision, with terminal cash rate pricing hovering around the 3.90% mark, as both measures operate within their recent ranges.

- Looking ahead, RBA Governor Lowe’s latest appearance in Canberra headlines Monday’s domestic docket, with retail sales data and the aforementioned round of ACGGB Mar-47 supply also slated.

- Next week’s domestic docket also includes monthly CPI data, building approvals, private sector credit, CoreLogic house price readings, housing finance data and the first round of Q3 GDP partials, which comes in the from of the capex print. Note that we will also hear from RBA’s Kearns, Head of the Bank’s domestic markets division, during the course of the week, via an appearance in front of the Australian Securitisation Conference.

NZGBS: Twisting Flatter Into The Weekend

The cheapening witnessed in the wider core global FI space saw NZGBs soften as Friday’s session wore on, although the early twist flattening impulse held, with the major benchmarks running 6bp cheaper to 4bp richer, with a pivot observed around 7s.

- Meanwhile, the swap curve saw rates run lower to unchanged, with a light steepening impulse seen. That left swap spreads a little tighter in the front end, but marginally wider further out.

- RBNZ dated OIS continues to price just over 70bp of tightening for the RBNZ’s Feb ’23 meeting, with a terminal rate of just under 5.50% eyed. The recent repricing probably helped bias front end NZGBs lower, alongside the wider weakness in bonds.

- Local data saw the ANZ consumer confidence reading hit the lowest level observed since June. The survey collator noted that “sharp increases in the cost of living and interest rates (not to mention falling house prices) are clearly hurting confidence, but excellent job security and strong wage growth have so far seen spending hold up far better than this level of confidence would normally imply. This dynamic is likely to be on borrowed time.”

- Elsewhere, Q3 retail sales volume data was virtually in line with exp., rising by 0.4% Q/Q (the BBG survey median looked for a reading of +0.5%).

- Next week’s domestic docket includes the ANZ business survey, building permits, terms of trade and CoreLogic house price data.

FOREX: DXY Remains On The Defensive

The post-Fed minutes downtick in the USD continued during Asia-Pac hours, with U.S. Tsys underpinned and continued focus on the seemingly impending slowing of Fed tightening evident. That left the greenback and the CHF at the bottom of the G10 FX pile in limited Asia-Pac dealing.

- USD/JPY operates near unchanged levels after some potential gotobi demand and the bid in U.S. Tsys introduced two-way price action.

- The NZD was an early underperformer, with soft NZD data applying some modest pressure to the kiwi, although that has faded.

- USD/CNH briefly ticked higher, with another uptick in the new daily COVID case count in China supporting the pair, before a slightly firmer than expected CNY mid-point fixing and the downtick in the broader USD allowed the cross to move away from best levels.

- USD/KRW more than reversed an early uptick that was a result of increased focus on the BoK nearing the end of its tightening cycle.

- ECB & Riksbank speak headline the broader macro docket on Friday, with wider market liquidity set to be thinned as many U.S. participants opt to take an elongated weekend in lieu of Thursday’s Thanksgiving holiday (note that U.S. markets will be subjected to shortened operating hours ahead of the weekend).

- A reminder that speculation/expectation surrounding a potential RRR cut from the PBoC is elevated after Wednesday's State Council meeting guided towards such a move. Many expect the PBoC to act after local market hours on Friday.

FX OPTIONS: Expiries for Nov25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0190-00(E527mln), $1.0250(E740mln), $1.0380-00(E774mln)

- USD/JPY: Y137.10($960mln) Y143.50-70($1.0bln)

- GBP/USD: $1.1858(Gbp624mln)

- EUR/GBP: Gbp0.8655(E878mln)

- AUD/USD: $0.6700(A$655mln)

- USD/CAD: C$1.3605-20($595mln)

- USD/CNY: Cny7.1500($661mln)

EQUITIES: Marginally Mixed In Asia

The major Asia-Pac equity indices recorded mixed performance on Friday, with Chinese property names continuing to benefit from sector-specific support and heightened expectations of imminent easing from the PBoC. That allowed the CSI 300 to register modest gains.

- Elsewhere, HK tech names struggled in the wake of the recent impressive rally, with worry surrounding production for key Apple supplier Foxconn applying pressure. That left the Hang Seng in the red.

- Still the major regional indices are set to finish somewhere between -/+1.0% on the day.

- Elsewhere, e-minis looked to softer Tsy yields and a downtick in the USD for support, holding onto Thursday’s modest gains.

GOLD: Fed Minutes Fallout Continues To Support

A tick lower in the broader USD and some richening in the U.S. Tsy space has supported gold in the final Asia-Pac session of the week, putting bullion on track for a modest weekly gain. The yellow metal last prints a handful of dollars higher, just shy of $1,760/oz.

- The post-FOMC minutes fallout continued to feed its way into price action after the U.S. Thanksgiving holiday.

- Technically, short-term trend conditions in Gold remain bullish, however for now, the yellow metal remains in a corrective cycle. Recent gains resulted in the break of $1,729.5/oz, the Oct 4 high. This has strengthened a bullish theme and signals scope for a test of $1,800.0/oz, which protects key resistance at $1,807.9/oz, the Aug 10 high. Ahead of that zone, the bull trigger is located at $1,786.5/oz, the Nov 15 high. Initial firm support is seen at $1,702.3/oz, the Nov 9 low.

OIL: Drawing Support From USD Downtick, Still On Track For Third Weekly Loss

A softer USD has provided some support for crude oil in the final session of the week, although continued demand worry leaves the major oil benchmarks on track for a third consecutive weekly decline.

- WTI and Brent futures sit $0.50 & $0.30 higher on the session, respectively.

- Heightened worry re: the COVID situation has been a major headwind for crude bulls during the current week.

- In the background, European officials remain locked in discussion re: the technicalities surrounding the proposed Russian oil price cap, with the relevant parties not appearing close to forming a consensus agreement.

- Note that late on Thursday we saw the Iraqi and Saudi Arabian oil ministers stress commitment to continued collective action within the OPEC+ framework via a joint statement. The statement highlighted the potential for the group to take further action re: crude output levels, if required.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 25/11/2022 | 0700/0800 | * |  | DE | GFK Consumer Climate |

| 25/11/2022 | 0700/0800 | *** | | DE | GDP (f) |

| 25/11/2022 | 0700/0800 | ** |  | SE | PPI |

| 25/11/2022 | 0745/0845 | ** |  | FR | Consumer Sentiment |

| 25/11/2022 | 0800/0900 |  | ES | PPI | |

| 25/11/2022 | 0900/1000 | ** |  | IT | ISTAT Consumer Confidence |

| 25/11/2022 | 0900/1000 | ** | | IT | ISTAT Business Confidence |

| 25/11/2022 | 1330/0830 | ** |  | US | WASDE Weekly Import/Export |

| 25/11/2022 | 1600/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) | |

| 27/11/2022 | - |  | AU | Victoria State Election |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.