Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

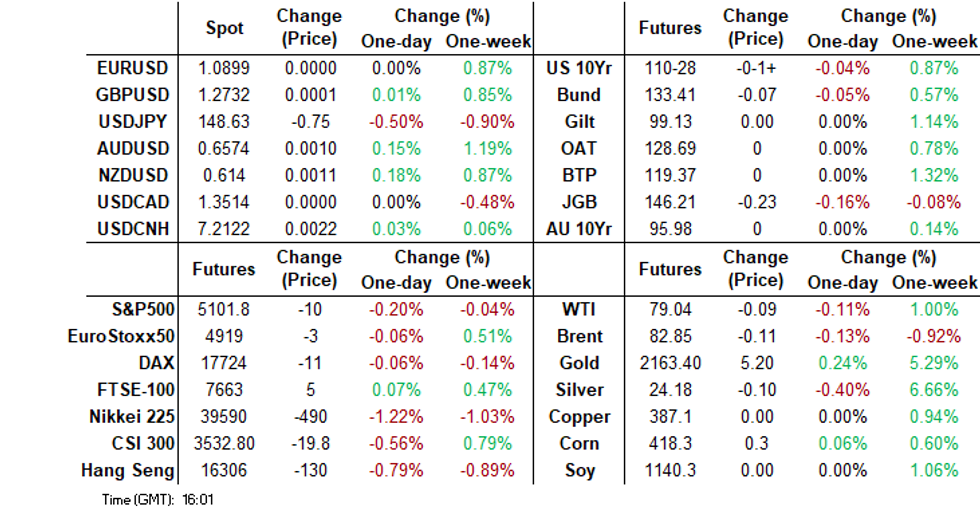

- The JPY and JGB yields are firmer today, with a number of factors lending support- stronger Jan wages data, a large union announcing larger pay increases this year versus last year, while BBG noted some Japan government officials are in favor of a near term BoJ shift (although Mar versus Apr wasn't specified). BoJ speak also noted steady progress towards the 2% inflation goal.

- USD/JPY dipped below its 50-day EMA but has since recovered some ground. JGB futures are weaker and near session lows, -25 compared to settlement levels.

- Broader USD sentiment was mostly softer. Gold prices made a fresh high above $2160 before moderating. US Treasury yields are 1-2bps higher today, but this hasn't impacted sentiment.

- Later Fed Chair Powell testifies before Congress and Mester speaks on the economic outlook. In terms of US data, there are February Challenger job cuts, jobless claims and January trade. The ECB decision is announced including updated forecasts and press conference.

MARKETS

US TSYS: Treasury Futures Edge Lower, Kashkari Sees 2 Cuts, Powell Day Two Later

- Jun'24 10Y futures are weaker and near session lows, moves lower by JGB futures could be having a part in the move, after BoJ Board Member Nakagawa indicated the timing for an interest rate increase is coming closer. Ranges remain tight and well within Wednesdays, we trade just off the daily lows of 111-11+ at 111-12 down - 03 + from NY closing levels.

- Looking at technical levels, Initial technical resistance is 111-23 (High Mar 6), a break above would open 111-27 (50% retracement of the Feb 1 - 23 bear leg). To the downside, levels to watch include 110-05+/109-25+ (Low Mar 1 / Low Feb 23 and bear trigger), below there 109-14+ (Low Nov 28)

- Treasury yields are 1-2bps higher today, with the 2Y yield up +1bps to 4.564%, 10Y yield up +1.7bps to 4.119%, while the 2y10y is +0.705 higher to -44.664.

- Post US Close, Fed's Kashkari spoke at a WSJ Event, his statements suggest a cautious approach to monetary policy, with the base case indicating no further rate hikes, while keeping with his December projections case of 2 cuts. However, he acknowledges that if inflation becomes more entrenched, the Fed may prolong its current stance, and if inflation flares again, a rate hike could be justified. See MNI piece (here)

- Thursday's data calendar includes Weekly Claims, Unit Labor Cost, and day two of Chairman Powell's testimony.

STIR: Year-End Pricing Softens 30bps In Canada & NZ Over The Past Few Weeks

STIR markets within the $-bloc persist in foreseeing a notable easing cycle in 2024. In fact, over the last three weeks, the pricing for the year-end official rate in Canada and NZ has eased by approximately 30-35bps. Conversely, year-end OIS pricing in Australia has softened by around 10bps, while remaining unchanged in the US. As for overnight developments:

- There were few hawkish surprises from Fed Chair Powell’s testimony to Congress, where he reiterated the Fed’s view of cutting interest rates "at some point this year" but not until it becomes more confident that inflation will keep falling.

- The Bank of Canada kept its policy rate on hold at 5.0% for a fifth consecutive meeting. BoC Governor Macklem said, “It’s still too early to consider lowering the policy interest rate”. In the statement, the line “the council is still concerned about risks to the outlook for inflation, particularly the persistence in underlying inflation” was kept.

Figure 1: $-Bloc STIR

Source: MNI – Market News / Bloomberg

JGBS: No Recovery From BoJ Nakagawa-Induced Sell-Off

JGB futures are weaker and near session lows, -25 compared to settlement levels after BoJ Board Member Nakagawa indicated the timing for an interest rate increase is coming closer. He noted progress toward achieving the bank’s price target. “Japan’s economy and inflation are steadily making progress toward meeting the stable 2% inflation target,” Nakagawa said in a speech to local business leaders in Shimane, western Japan. (See Bloomberg link)

- Outside the above domestic driver, Japan's January wages data was stronger than expected, as previously outlined, and 30-year supply saw poor demand metrics. The low price failed to meet dealer expectations, the cover ratio declined to 2.934x from 3.181x in February and the auction tail widened.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session after yesterday’s post-Powell bull-flattening. Later today sees Weekly Claims, Unit Labor Cost, and day two of Chair Powell's testimony.

- The cash JGB curve bear-steepened, with yields flat to 3bps higher. The benchmark 10-year yield is 1.5bps higher at 0.732% versus the February high of 0.772%.

- The swaps curve has also bear-steepened, with rates 1-2bps higher. Swap spreads are wider apart from the 7-year and 20-year.

- Tomorrow, the local calendar sees Household Spending, BoP Current Account, Bank Lending and Leading & Coincident Indices data.

- Tomorrow will also see BoJ Rinban operations covering 1- to 10-year JGBs.

JAPAN DATA: Jan Wages Stronger Than Forecast

Japan Jan wages data was stronger than expected. The headline labor cash earnings rose 2.0% y/y, versus a 1.2% forecast and a prior 0.8% gain. In real terms, earnings were still in negative terms, but not as much as forecast. We were -0.6% y/y, versus -1.5% projected and -2.1% prior.

- Cash earnings on the same sample basis were +2.0%y/y, against a 1.9% forecast and 2.0% prior. Scheduled full time pay (on the same sample base) was 2.0% y/y in line with expectations but down slightly from the 2.1% prior outcome.

- Bonus payments were +16.2%y/y, versus 0.5% in Dec last year. This component tends to be volatile, so there may be some payback in Feb.

- Nevertheless, we saw broad based y/y gains across nearly all of the sub-categories (hours worked, overtime etc).

- This may aid confidence that firmer wage gains will continue in the first half, particularly during the current wage negotiation period, where there is evidence that some firms are raising wages more so than they did last year.

- Bloomberg noted that BoJ officials are getting more confidence over the strength of wage growth, see this link. Also note the latest MNI policy team insight, noting the BoJ could end NIRP in March (see this link).

AUSSIE BONDS: Cheaper, Near Session Lows, Powell Part II Later Today

ACGBs (YM -1.0 & XM flat) sit in negative territory and near session lows. There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Home Loan Values and Trade Balance data.

- (MT Newswires) "The economy remains weak but looks consistent with positive jobs growth and despite an improvement in productivity, unit labour cost growth (a proxy for services inflation) remains robust," Morgan Stanley said, adding that it still expects the RBA to hold interest rates steady through the course of this year, before cutting rates in early 2025.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session after yesterday’s post-Powell bull-flattening. News flow has so far been light today. Later today sees Weekly Claims, Unit Labor Cost, and day two of Chair Powell's testimony, ahead of Non-Farm Payrolls on Friday.

- Cash ACGBs are flat to 1bps cheaper after being flat to 2bps richer earlier in the session. The AU-US 10-year yield differential is 3bps higher at -11bps.

- Swap rates are flat to 1bp lower, with the 3s10s curve flatter.

- The bills strip is slightly cheaper, with pricing flat to -1.

- RBA-dated OIS pricing is unchanged across meetings. A cumulative 43bps of easing is priced by year-end.

- Tomorrow, the local calendar is empty.

AUSTRALIA: Housing Affordability Likely To Continue To Deteriorate

Real private residential dwelling construction fell 3.8% q/q in Q4 to be down 3.1% y/y after two quarters of only moderate growth. It fell between Q4 2021 and Q1 2023 apart from Q3 2022’s small rise. Both supply and demand issues are adding to Australia’s housing shortage as the working age population increased 327k in 2023 after +513k in 2022. This is reflected in housing inflation with both rents and prices rising strongly and currently there are no signs the situation is improving.

Australia GFCF dwellings %

Source: MNI - Market News/ABS

- CoreLogic capital city home prices rose 10.4% y/y in February, which is putting further pressure on housing affordability along with higher mortgage rates. With no signs yet of an improvement in supply and population continuing to increase, affordability is likely to continue to deteriorate over 2024 even if the RBA cuts rates.

- There was a strong rise in gross household disposable income in Q4 of 2.3% q/q and 5% y/y but this was not enough to drive an improvement in housing affordability with our HAI deteriorating another percentage point. It is now 44% below trend, a new low since our series began in 1981.

- The pickup in disposable income drove a small improvement in the house-price-to-disposable income ratio. It now stands 7.5% above trend down from 8% in Q3.

- With a shortage of properties, rental vacancy rates are very high and rents are rising strongly as a result. Q4 CPI rents rose 7.3% y/y down slightly from Q3’s 7.6% helped by government rent assistance.

- The ratio of house prices to rents gives an indication of valuation and while housing is not as overvalued as it was during the pandemic it was 11.1% overvalued in Q4 up from 10.5%.

Source: MNI - Market News/Refinitiv

AUSTRALIAN DATA: Trade Makes Good Start To 2024

Australia’s trade picture remained robust at the start of 2024 after net exports contributed 0.6pp to Q4 growth but import picture still suggests lacklustre domestic demand. The January merchandise trade surplus widened by $284mn to $11 027mn, a bit less than expected. Exports outpaced imports rising 1.6% m/m versus 1.3% m/m respectively, but both are weak on the year falling 5.2% y/y and -5.3%.

- The growth in goods exports was driven by non-monetary gold but rural goods also rose strongly due to meat and cereals. Non-rural goods fell 0.5% m/m and -9.1% y/y due to drops in coal and other mineral fuels but metal ores were stronger. Lower commodity prices are also weighing on the series.

- Goods imports were driven by an increase in non-industrial vehicles (+17.2% m/m). After a couple of weak months consumer and capex goods imports rose strongly by 5.2% m/m and 5.9% respectively, but machinery & equipment fell 2.1% with industrial transport up 13.1%. Despite the January improvement, the 7% y/y and 9.2% y/y drops in both consumer and capex goods imports signal soft domestic demand.

Source: MNI - Market News/ABS

AUSTRALIAN DATA: Commodity Volumes Down To Much Of Asia

Australia’s merchandise exports to Asia were generally weak again in January with them falling to China on the month after rising in January 2023 on the back of China’s re-opening, which resulted in shipments to Australia’s largest destination little changed on a year ago.

- Exports to Japan and Korea remained weak falling 25.5% y/y and -14.9% y/y respectively in January. They are the second and third most important destinations for Australian goods. Taiwan was also weak falling 36% y/y and India -27.6%, they are the fourth and fifth largest destinations. On a brighter note exports to the US rose 15.7% y/y.

- Iron ore and coal export volumes to China fell sharply in January but the former was strong to Korea while the latter fell. Higher iron and coal prices provided some support given that total quantities were sharply lower. There appears to be some volatility as volumes rose in December.

- LNG export volumes were down 4.8% m/m but this was after a 14.7% rise in December. Prices rose 4.4% after falling 3.3%.

Source: MNI - Market News/ABS

NZGBS: Bull-Flattening After Mixed Results From Weekly Auctions

NZGB curve closed with a bull-flattening (flat to 2bps richer) after today’s weekly supply saw mixed results across the lines. The May-32 and May-41 lines saw cover ratios over 3.00x, while the Apr-27 bond saw cover at a poor 1.69x (3.80x previously).

- In addition to the previously outlined Manufacturing Volume data, the RBNZ published new credit flow figures for January. Total New Lending fell 2.1% y/y, while New Residential Lending rose 9.2%y/y.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session after yesterday’s post-Powell bull-flattening. Later today sees Weekly Claims, Unit Labor Cost, and day two of Chair Powell's testimony, ahead of Non-Farm Payrolls on Friday.

- Swap rates closed 2-3bps lower, with the 2s10s curve flatter and implied swap spreads narrower.

- RBNZ dated OIS pricing is 1-5bps softer across meetings beyond July. A cumulative 52bps of easing is priced by year-end.

- Tomorrow, the local calendar is empty.

- RBNZ Governor, Adrian Orr and Chief Economist, Paul Conway will speak about the February Monetary Policy Statement at separate events over 12-14 March 2024.

FOREX: USD Index Testing Sub Wednesday Lows, Yen The Outperformer

The BBDXY is testing below Wednesday lows in recent dealings, last under 1235. We are around 0.15% weaker for the session so far, with yen the clear outperformer, up nearly 0.65% against the USD.

- Cross asset sentiment in terms of lower US equity futures, coupled with a slight rise in US yields hasn't mattered much for the USD today. Regional equity sentiment has softened somewhat as well.

- The rise in the gold price to fresh record highs above $2160 has been a positive, although how much of this is just reflective of USD weakness is difficult to say.

- Yen strength has come down to a number of factors, stronger Jan wages data, a large union announcing larger pay increases this year versus last year, while BBG noted some Japan government officials are in favor of a near term BoJ shift (although Mar versus Apr wasn't specified). BoJ speak also noted steady progress towards the 2% inflation goal. Governor Ueda is before parliament this afternoon.

- USD/JPY tracks near session lows in recent dealings, close to 148.40. This is just under the 50-day EMA (148.51). Note as well a chunky option strike at 148.25 for notional 1.13 bn (USD call, JPY put) expires on the 12th of March. The Feb 7 low came in at 147.63, which may come into play if we can break lower.

- AUD/USD is also higher, along with NZD. The A$ last near 0.6590 around 0.35% stronger. NZD/USD up 0.30%, tracking close to 0.6150. Firmer commodity prices have likely helped both currencies, as other cross-asset drivers haven't been supportive.

- Later Fed Chair Powell testifies before Congress and Mester speaks on the economic outlook. In terms of US data, there are February Challenger job cuts, jobless claims and January trade. The ECB decision is announced including updated forecasts and press conference.

ASIA EQUITIES: China & HK Equities Lower As US Look To Block Foreign Biotech Firms

Hong Kong and China equities are lower today, with Biotech names the worst-performing sector after the US advanced a bill that would block them from accessing US Federal contracts, while property names are also lower after China Overseas Land's sales declined 69% in February.

- Hong Kong Equities are lower today with the HS Biotech Index down 4.60%, while property names are again under pressure with the Mainland Property Index down 1.10%. Tech names have been performing well in the wider APAC region today however the HSTech Index is now down 0.90%, JD.com is the outlier up 6.00% after strong earnings, while the HSI is down 0.60%. China Mainland equities are faring slightly better however still lower with the CSI300 down 0.50%, now out-performing the CSI1000 down 1.00% and the ChiNext down 1.50%

- China Northbound flows were -1.5b yuan on Wednesday, with the 5-day average to 0.85b, while the 20-day average sits at 2.6b yuan.

- JD.com soared 8% after beating estimates, while also approving a $3B buyback program and hiking it's annual dividend payout by 23%

- The CSRC has pledged to "act decisively" in extreme cases to address market failures and contain turmoil in the stock market at the NPC on Wednesday. They outlined scenarios prompting intervention, including severe deviations from fundamentals, irrational fluctuations, liquidity drying up, and indications of market panic. This move comes as Beijing seeks to restore confidence in the $9 trillion stock market after three years of losses, with the regulator focusing on improving regulations, preventing systemic risks, cracking down on market manipulation, and enhancing fairness in trading.

- The US Senate Homeland Security Committee advances a bill that would block certain foreign biotech companies from accessing US federal contracts. While the US government is also pressing allies including the Netherlands, Germany, South Korea, and Japan to further tighten restrictions on China’s access to semiconductor technology, the move is drawing resistance in some countries.

ASIA PAC EQUITIES: Asia Equities Mostly Higher, Stronger Yen Weighs On Japan Equities

Regional Asian equities are mixed today with Japan being the under-performer in the region, the stronger yen has offset moves higher in technology names. Markets have been higher after Powell's testimony they rate cuts are expected to be seen later in the year.

- Japan equities are mostly lower today, as the stronger yen offset moves in tech names, while banking names opening up 2% after increasing expectations that the BoJ will scrap it's negative interest rate policy in the coming months, the Topic Bank Index is up 1.25%. The stronger yen isn't helping the wider market as it rallied to its highest level in a month, the Topix is down 0.26%, while the Nikkei 225 with a higher exposure to tech names is down 0.85%n

- South Korean equities are slightly higher today, tech names have led the way higher with Samsung SDI is the top performer after it was reported the EV battery maker will start mass producing an all solid state battery in 2027. While foreign investors have been better sellers with paper and paper products and non metallic mineral names seeing the most of the outflows The Kospi is up 0.15%

- Taiwan equities are the top performing region today, semiconductor names again are leading the way higher after the Philadelphia semiconductor Index closed up 2.42% on Wednesday. The Taiex is currently 1.20% higher.

- Australian equities are slightly higher today, as Banking and Industrial names edge higher, Metals & Mining names are lower. The ASX has closed up 0.37%

- Elsewhere in SEA, NZ closed up 0.07%, Indonesia is up 0.62%, India up 0.06%, while Singapore down 0.20% and Philippines down 0.80% being the worst performer.

ASIA EQUITY FLOWS: Asian Equity Flows Negative As SK Sees Outflows From Tech Names

- China equities were lower on Wednesday while also seeing -1.5 billion yuan in outflows via northbound connect. The market will again be focused on the NPC; on Wednesday afternoon, the CSRC said it will move to fix “market failures” in extreme cases, giving its most detailed pledge yet on when it acts to contain turmoil in the world’s second-largest stock market. China's chip-related stocks may trade weaker today as the US urges allies to squeeze China on chip technology. The 5-day average continues to trend lower, now at 0.85 billion vs the 20-day average at 2.6 billion yuan.

- South Korean equities were lower on Wednesday while foreign equity flows saw the worst outflow since Jan 17th at -$285m. This could be linked to the doubt being cast around the breakthrough made by researchers behind LK-99 who have claimed to have synthesized a new material showing superconducting behaviour at room temperature. The 5-day average is $225m, while the 20-day average sits at $210m.

- Taiwan equities were higher on Wednesday up 0.60% led higher by semiconductor names, while flows turned negative with $13.1m leaving the market. The 5-day average is $329m, while the 20-day average sits at $260m.

- Thailand equities were higher on Wednesday after weaker CPI reading on Tuesday build a case to lower rates with Wednesday breaking the run of outflows that have been seen over the past week or so, $52m of foreign equity inflows hit the market, taking the 5-day to -$38m, while the 20-day still sits at -$10m

- Philippines equities were slightly higher on Wednesday and continues its run of inflow days now marking the 25th day in the row. The Philippine Central Bank Governor signalled policy makers would likely not cut rates for a while. The 5-day average is now $8.1m, while the 20-day average is -$7.5m

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| China (Yuan bn)* | -1.5 | 4.3 | 33.9 |

| South Korea (USDmn) | -285 | 1128 | 8843 |

| Taiwan (USDmn) | -13 | 1646 | 6448 |

| India (USDmn)** | -27 | 573 | -2424 |

| Indonesia (USDmn)** | 0 | -138 | 1083 |

| Thailand (USDmn) | 52 | -190 | -857 |

| Malaysia (USDmn) ** | -103 | -302 | 210 |

| Philippines (USDmn) | 1 | 40.5 | 241 |

| Total (Ex China USDmn) | -375 | 2757 | 13545 |

| * Northbound Stock Connect Flows | |||

| ** Data Up To March 5 |

JAPAN DATA: Offshore Investors Return To Local Equities, Japan Investors Resume Offshore Bond Purchases

Offshore investors returned to Japan stocks last week. We saw ¥283.9bn in net inflows, more than offsetting the prior week's outflows (which were the first recorded outflows for the year). Offshore investors also stepped up bond buying, with ¥572.5bn in inflows. The net flow backdrop for this segment is around flat though for the past 3 weeks.

- Local investors stepped up purchases of offshore bonds, with ¥484.6bn in outflows. This ended a run of two consecutive weeks of net selling for this segment. The generally trend since the start of the year has been for Japan investors to be net purchases of offshore bonds.

- The reverse transpired in the equity space, with -¥517.2 in net outflows. The trend there though has also been close to flat for the past month.

Table 1: Japan Weekly Investment Flows

| Billion Yen | Week ending Mar 1 | Prior Week |

| Foreign Buying Japan Stocks | 283.9 | -206.3 |

| Foreign Buying Japan Bonds | 572.5 | -46.3 |

| Japan Buying Foreign Bonds | 484.6 | -250.1 |

| Japan Buying Foreign Stocks | -517.2 | 225.9 |

Source: MNI - Market News/Bloomberg

OIL: Crude Holds Onto Gains On US Demand Hopes

Oil prices have held onto most of Wednesday’s gains due to further greenback weakness and continued US gasoline stock drawdown, but gave up increases from early in the APAC session. WTI is flat at $79.12/bbl after reaching an intraday high of $79.36, and Brent is at $82.92 after a high of $83.17. The USD index is down another 0.1%, which should help to put a floor under crude. Markets will be looking to Friday’s US payrolls now for direction.

- Better-than-expected January-February China trade data failed to boost oil prices. Its crude import volumes rose 5.1% y/y YTD and refined oil +35.6% y/y YTD.

- Oil has continued to find support during today’s session from the EIA reported 4.46mn gasoline inventory drawdown last week. This fifth decline is signalling robust demand ahead of the driving season.

- A Barbados-flagged bulk carrier was hit by Houthi rebels in the Gulf of Aden on Wednesday killing two crew members for the first time. The US and UK reiterated that it will act to protect shipping in the area.

- Later Fed Chair Powell testifies before Congress and Mester speaks on the economic outlook. In terms of US data, there are February Challenger job cuts, jobless claims and January trade. The ECB decision is announced including updated forecasts and press conference.

GOLD: Slightly Higher After A New Record High On Wednesday

Gold is slightly higher in the Asia-Pac session, after closing 0.9% higher at $2148.18 on Wednesday. Earlier in yesterday's session bullion achieved a new record high of $2152.25.

- The precious metal was buoyed by continued Houthi attacks plus the sizeable depreciation of the USD after there were no hawkish surprises in ADP employment, the JOLTS report or Fed Chair Powell’s testimony.

- Fed Chair Powell reiterated in front of Congress the Fed’s view of cutting interest rates "at some point this year" but not until it becomes more confident that inflation will keep falling.

- US Treasuries finished with yields flat to 5bps lower.

- The next resistance is $2177.6 (Fibonacci projection of Oct 6 – 27 – Nov 13 price swing), according to MNI's technicals team.

- (Bloomberg) Citigroup Inc. raised its gold forecast for the next three months to $2,200 an ounce, and upgraded the projection to $2,300 for the next six to 12 months. It cited recession risks in the second quarter, which can favour gold, “especially given the recent equity and credit market rallies.”

CHINA DATA: Jan-Feb Trade Figures Better Than Forecast, But No Follow Through Support For the Yuan

China trade figures were better than forecast for the Jan-Feb period. The Feb data gets reported this way due to LNY timing, which would obviously impact the headline Feb result. Exports were +7.1% ytd y/y versus 1.9% forecast. Imports rose 6.7% ytd y/y. The trade surplus is $125.16bn ytd, versus a $106.8bn forecast.

- In terms of the detail, exports processed with import materials were -12.2% ytd y/y. Note this item was -14.6% y/y in Dec. Other parts of exports generally recorded healthy ytd y/y rises.

- By country exports were stronger to India and the US along with parts of the EU. Asean exports also rose, but softer trends were seen to Japan and South Korea.

- On the import side, crude oil imports were higher compared to a year ago (88.31mln tonnes versus 84.05 a yr ago). Iron ore imports were 209.45mln tonnes, versus 193.8 a year earlier. Coal imports and natural gas imports were also up on levels versus a year ago.

- Better export growth and the healthy trade surplus is being offset by capital outflows from a yuan standpoint. Reuters noted yesterday that domestic investors are butting up against outbound investment limits. General confidence around the economic outlook also remains a headwind, while China's low rates compared to other major economies, particularly the US, is likely driving preferences towards foreign currency holdings rather than the yuan. USD/CNH sits little changed post the data, last near 7.2100.

- Note we get Feb inflation data out on Saturday, which is likely to carry more weight in terms of the monetary policy outlook.

THAILAND DATA: Consumer Confidence Rises To Pre-Covid Level

Thai growth has been underperforming most of the region but there was some good news today from the University of Thai Chamber of Commerce consumer sentiment report. Consumer confidence rose almost one point to 63.8 in February from 62.9 to be its highest since February 2020, pre-Covid. The Q1 average is pointing to another robust quarter for real consumer spending after Q4 rose 7.4% y/y.

- The economy is heavily dependent on international tourists and while numbers rose 41.5% y/y in January, they are still below pre-pandemic levels. Consumer sentiment is probably being boosted by the recovery in the sector and the expected digital wallet payment.

- The concern though is that tourists are staying in Thailand for shorter periods than previously and spending less per person. This is reflected in flat January private consumption volumes.

Source: MNI - Market News/Refinitiv

ASIA FX: South East Asia FX Again Outperforms The North, BNM Decision Still To Come Today

USD/Asia pairs are mostly lower, although SEA FX is once again outperforming NEA FX. In SEA, MYR has surged, while THB has risen. IDR spot is higher but the 1 month NDF is little changed. CNH has been steady, despite positive trade data. The KRW NDF is closed to unchanged. Still to come today is Taiwan inflation figures, along with the BNM decision, no change is expected. Tomorrow, we have South Korea current account data, while Philippines bank lending figures are due. Later on, Taiwan trade figures are out.

- USD/CNH volatility remains remain low, the pair not far from 7.2090 in recent dealings. A weaker equity tone is not helping sentiment (although CNH didn't rally earlier when equities were firmer), while USD/CNY onshore spot remains close to 7.2000, with this pair largely ignoring broader USD trends in recent weeks. We had better trade figures earlier, but there was little positive follow through for the yuan.

- Better export growth and the healthy trade surplus is being offset by capital outflows from a yuan standpoint. Reuters noted yesterday that domestic investors are butting up against outbound investment limits. General confidence around the economic outlook also remains a headwind, while China's low rates compared to other major economies, particularly the US, is likely driving preferences towards foreign currency holdings rather than the yuan.

- Spot USD/KRW is back to 1330, but the 1 month NDF couldn't build on early downside momentum sub 1326. We are back to 1328 only marginally firmer in won terms for the session. Spillover from yen gains is fairly limited at this stage. Local equities are back to slightly positive for the session, but haven't been impact KRW so far today.

- USD/INR is extending its break sub the simple 200-day MA, last near 82.77 (earlier lows were at 82.725). This is the lowest levels in the pair since early September last year. Whilst percentage change moves are modest ( the rupee is up only 0.55% so far this year), its outperformance against the rest of EM Asia FX remains evident. On top of the news from earlier in the week around India bond inclusion into Bloomberg's EM bond index, growth expectations remain elevated as well. RBI Governor Das stated growth may be closer to 8% for the fiscal year (ending this March), which would be above the government's target (BBG). Survey business sentiment measures remain very elevated, particularly compared to the rest of the world.

- MYR is the best performing currency in EM Asia so far today, up around 0.50%. USD/MYR was last near 4.7090. This is close to 4.7065, which is the 100-day EMA. Yesterday's intra-day high ran out of steam around the 20-day EMA (currently near 4.7485). We saw fresh rhetoric from BNM late yesterday, with the central bank stating it is committed to ensuring ringgit stability, while also increasing monitoring of export proceeds into the local currency (BBG). Later on today, the BNM policy decision is seen on hold, but financial stability issues, particularly FX are likely to be a focus point (see our full preview here).

- The baht has strengthened 0.3% against the US dollar today to around 35.58, close to the intraday low of 35.55. USD/THB is down 1.7% since its recent peak on February 15. For USD/THB we are close to the 100-day EMA near 35.52, below that is the 200-day. We haven't been below that support point since Jan of this year. The University of Thai Chamber of Commerce reported consumer confidence rose almost one point to 63.8 in February to be its highest since February 2020, pre-Covid. Gold prices reached a new high today of $2161.48/oz. Correlations with USDTHB remain skewed inversely with gold, so this along with a firmer yen, have likely seen positive spill over effects for the baht today.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/03/2024 | 0645/0745 | ** |  | CH | Unemployment |

| 07/03/2024 | 0700/0800 | ** |  | DE | Manufacturing Orders |

| 07/03/2024 | 0930/0930 |  | UK | BOE's Monthly Decision Maker Panel Data | |

| 07/03/2024 | - | *** |  | CN | Trade |

| 07/03/2024 | 1315/1415 | *** |  | EU | ECB Deposit Rate |

| 07/03/2024 | 1315/1415 | *** | | EU | ECB Main Refi Rate |

| 07/03/2024 | 1315/1415 | *** | | EU | ECB Marginal Lending Rate |

| 07/03/2024 | 1330/0830 | *** |  | US | Jobless Claims |

| 07/03/2024 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 07/03/2024 | 1330/0830 | * |  | CA | Building Permits |

| 07/03/2024 | 1330/0830 | ** | | US | Trade Balance |

| 07/03/2024 | 1330/0830 | ** | | US | Non-Farm Productivity (f) |

| 07/03/2024 | 1330/0830 | ** | | CA | International Merchandise Trade (Trade Balance) |

| 07/03/2024 | 1345/1445 | | EU | ECB Monetary Policy Press Conference | |

| 07/03/2024 | 1500/1000 | | US | Fed Chair Jay Powell | |

| 07/03/2024 | 1500/1600 | | EU | ECB Podcast - Lagarde presents latest monpol | |

| 07/03/2024 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 07/03/2024 | 1630/1130 | | US | Cleveland Fed's Loretta Mester | |

| 07/03/2024 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 07/03/2024 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 07/03/2024 | 1700/1200 | | US | BLS webinar on CPI rent and OER | |

| 07/03/2024 | 2000/1500 | * | | US | Consumer Credit |

| 08/03/2024 | 2350/0850 | ** |  | JP | Trade |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.