Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Core FI markets extend recent sell off in Asia.

- HEadline flow was relatively light in Asia, although expectations re: RBA tightening continue to garner attention, as did an FT report poitning to the potential for a de-escalation in geopolitical tensions surrounding Russia.

- ECB Speak from Villeroy & de Cos will headline the remainder of Tuesday's docket.

BOND SUMMARY: No Let Up For Core FI In Asia

Core FI markets continued to leak lower during Asia-Pac hours, with FT reports pointing to the potential for de-escalation when it comes Russia-related geopolitical tensions potentially aiding the cheapening.

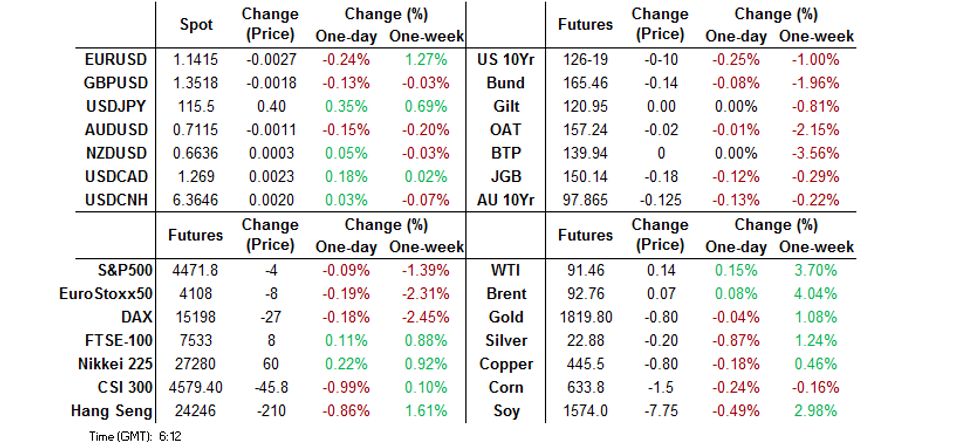

- TYH2 took out Monday’s Asia lows, with focus now switching to nearby Fibonacci support (126-16), as the contract trades -0-09+ at 126-19+, just off worst levels of the day. Cash Tsy trade saw 10-Year yields register fresh multi-year highs (with the same holding true for 2s & 5s), with the major benchmarks cheapening by 2-4bp, as the front end led the way lower. A 2.5K block sale FVH2 118.50 puts headlined on the flow side in Asia. NFIB small business optimism data and the latest round of 3-Year Tsy supply headline the NY docket on Tuesday.

- JGB trade saw the curve bear steepen, with the major benchmarks cheapening by 0.5-3.0bp on the day. Participants remain wary of the potential for BoJ enforcement when it comes to the top end of the Bank’s permitted trading band (0.25%), with that particular benchmark operating around the 0.21% level. JGB futures respected post-NFP lows, closing -18 on the day.

- Broader core FI weakness, trans-Tasman impetus from NZ bonds (although part of that reflected a degree of catchup after the long weekend in NZ), a couple of major sell-side institutions pointing to hawkish risks re: their RBA calls and an ex-RBA board member pointing to cash rate lift off by August and the likelihood of a 1.00% cash rate target at year end (which is a little less hawkish than market pricing at present) all applied pressure to the ACGB space, after futures steepened in overnight dealing. That left YM -8.5 & XM -12.5 at the close (as steepening came back to the fore as we moved through Sydney trade). Meanwhile, the IR strip bear steepened, finishing unchanged to 10 ticks cheaper on the day.

JGBS AUCTION: Japanese MOF sells Y199.9bn 10-Year JGBis:

The Japanese Ministry of Finance (MOF) sells Y199.9bn 10-Year JGBis:

- High Yield: -0.388% (prev. -0.357%)

- Low Price 103.70 (prev. 103.50)

- % Allotted At High Yield: 48.3443% (prev. 23.9819%)

- Bid/Cover: 4.198x (prev. 3.314x)

AUSSIE BONDS: The AOFM sells A$150mn of the 1.25% 21 Aug ‘40 I/L Bond, issue #CAIN413:

The Australian Office of Financial Management (AOFM) sells A$150mn of the 1.25% 21 August 2040 I/L Bond, issue #CAIN413:

- Average Yield: 0.2498% (prev. 0.1663%)

- High Yield: 0.2550% (prev. 0.1700%)

- Bid/Cover: 5.0867x (prev. 5.5333x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield 81.2% (prev. 50.0%)

- Bidders 50 (prev. 47), successful 9 (prev. 12), allocated in full 7 (prev. 7)

FOREX: Antipodeans Lead Gains, Yen Falters

The Antipodean currencies caught a bid, as the choir of RBA hawks grew further, while NZGB yields rallied on re-open after a local holiday. Ex-RBA board member Edwards told the WSJ that the Reserve Bank could raise the cash rate four times this year, while CBA & ANZ flagged hawkish risks to their central RBA scenarios.

- Broader recovery in risk appetite lent additional support to the Antipodeans, with an FT source report helping calm the nerves frayed by the Russia geopolitical tension. French officials told the newspaper that Russian President Putin appeared to be moving towards de-escalating the Ukraine crisis during his talks with President Macron.

- Oil-tied CAD and NOK failed to benefit from risk-on flows as crude oil futures slipped. They still outperformed the yen, which landed at the bottom of the G10 pile amid reduced demand for Asia's main safe haven currency.

- The PBOC fixed its central USD/CNY reference level just 14 pips above broader expectations, offering some stabilisation after showing a considerable upside bias yesterday. Offshore yuan was rangebound.

- U.S. trade balance headlines today's light data docket, while comments are due from ECB's Villeroy & de Cos.

FOREX OPTIONS: Expiries for Feb08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1150-65(E528mln), $1.1200(E1.2bln), $1.1250-60(E889mln), $1.1300-20(E2.3bln), $1.1380-00(E1.6bln)

- USD/JPY: Y115.50-65($636mln)

- GBP/USD: $1.3495-10(Gbp1.0bln), $1.3560(Gbp1.1bln)

- AUD/USD: $0.7100(A$732mln), $0.7125-35(A$645mln), $0.7150-55(A$521mln), $0.7165-75(A$893mln)

EQUITIES: Asia-Pac Mixed As Chinese & Hong Kong Equities Struggle

Australian equities led gains in Asia-Pac dealing, adding 1.1%, while the KOSPI and Nikkei 225sit flat & 0.2% higher, respectively, near the end of Tuesday trade.

- Mainland Chinese benchmarks and the Hang Seng diverged from their major regional counterparts, with the CSI 300 and Hang Seng both printing 1.6% worse off on the day at typing. The CSI 300 now sits at levels not witnessed since Sep 2020, as continued headwinds for the Chinese economy weigh on sentiment. Chinese-linked high beta tech struggled on the day. The Hang Seng Tech Index sits 2.2% worse off, while the ChiNext is ~4% lower on the session. This comes on the back of a negative lead from the U.S. tech space (although Monday’s NASDAQ losses weren’t as severe)

- E-minis are virtually unchanged at typing, paring early gains.

GOLD: Gains Remain Corrective, Key Resistance Still Some Way Off

Spot gold has stuck to a narrow range during Asia-Pac hours, last dealing essentially flat at $1,822/oz. This comes after U.S. real yields and the DXY moved away from best levels on Monday, adding some support to the space. Worries re: Russia-centric geopolitical risks also helped support bullion. Note that meaningful technical resistance is not seen until the Jan 25 high/bull trigger ($1,853.9/oz), with any gains considered corrective if that level is not breached.

OIL: Marginally Lower Overnight

WTI & Brent crude futures are ~$0.20 and ~$0.30 below their respective settlement levels at typing, ~$0.25 off worst levels of the day.

- There hasn’t been much in the way of major news catalysts during Asia-Pac hours, although FT reports pointing to the potential for a moderation in Russia-related geopolitical tensions may be weighing on crude. Still, losses have seemingly been limited by the fact that global crude and distillate inventories continue to show signs of tightness.

- From a technical perspective, WTI and Brent trade below their recent multi-year highs, but remain above their respective 4 Feb lows ($90.07 for WTI & $91.20 for Brent).

- Looking ahead, the latest round of Vienna talks re: the revival of the 2015 nuclear deal that Iran was party to will take place on Tuesday. In terms of the bigger picture surrounding these talks, while U.S.-Iranian tensions have cooled incrementally from extremes, Iran still refuses to meet directly with the U.S. As a result, other world powers continue to act as the middlemen in the indirect discussions.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 08/02/2022 | 0700/0800 | ** |  | SE | Private Sector Production |

| 08/02/2022 | 0745/0845 | * |  | FR | current account |

| 08/02/2022 | 0745/0845 | * | | FR | foreign trade |

| 08/02/2022 | 0800/0900 | ** |  | ES | industrial production |

| 08/02/2022 | 0900/1000 | * |  | IT | retail sales |

| 08/02/2022 | 1100/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 08/02/2022 | 1330/0830 | ** | | US | trade balance |

| 08/02/2022 | 1330/0830 | ** |  | CA | International Merchandise Trade (Trade Balance) |

| 08/02/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 08/02/2022 | 1500/1000 | ** | | US | IBD/TIPP Optimism Index |

| 08/02/2022 | 1630/1130 | ** | | US | NY Fed Weekly Economic Index |

| 08/02/2022 | 1800/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.