Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

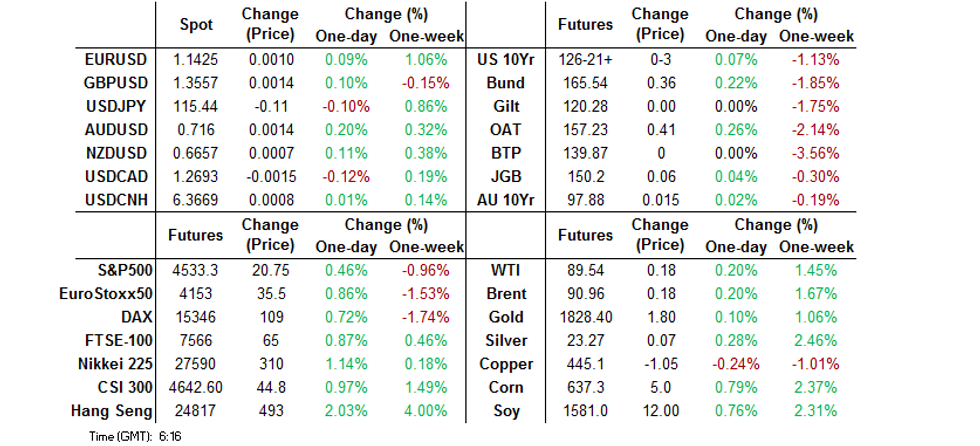

- Core fixed income markets nudged higher overnight, backing away from cycle lows, with a lack of meaningful macro headline flow apparent.

- Major regional equity indices & e-minis were higher in Asia.

- Today's data docket is fairly empty, which turns focus to central bank speak. Comments are due from Fed's Bowman & Mester, ECB's Schnabel, BoE's Pill & BoC's Macklem.

BOND SUMMARY: Better Bid Overnight

Core FI markets moved away from worst levels in Asia-Pac hours, with bears unable to force a meaningful extension of the recent weakness. There wasn’t much in the way of notable macro news flow.

- The more notable market flows tried to fade the Asia-Pac uptick in the Tsy space, with a couple of 2K+ screen sellers of TYH2 futures hitting, while 10K of block lifts in TYJ2 126.00 puts headlined broader overnight flow. TYH2 last +0-03+ at 126-22, 0-01 off session highs, while cash Tsys run 1-3bp richer across the curve, with bull flattening in play. Looking ahead, Wednesday’s NY docket is headlined by Fedspeak from Bowman & Mester, in addition to 10-Year Tsy supply.

- The super-long end led the JGB rally, with the major cash JGB benchmarks little changed to ~3.0bp richer, bull flattening in the process. Long dated swap spread tightening also pointed to receiver flows in swaps aiding the rally. JGB futures were +6 at the bell, with overnight losses more than reversed. The broader core FI bid and expectations re: the BoJ’s defence of the upper bound of its permitted 10-Year JGB yield trading band (0.25%) on any test of the level (if not pre-emptively) seemed to be the major supportive factors for the space. BoJ Rinban operations covering 1- to 10-Year JGBs saw little movement vs. prev in offer/cover terms. In local news, BoJ board member Nakamura stuck to the BoJ’s well-trodden central views in his latest address. Meanwhile, Tokyo and other prefectures requested an extension of the quasi COVID-19 state of emergency that they are currently observing, in line with press reports that have hit in recent days.

- Aussie bonds benefited from the broader uptick in core FI markets and the passage of supply-related pressure, with ACGB Nov’32 and semi-government issuance now behind us. YM +1.0 & XM +1.5 at the close, a touch shy of best levels of the day.

JGBS AUCTION: Japanese MOF sells Y2.7565tn 6-Month Bills:

The Japanese Ministry of Finance (MOF) sells Y2.7565tn 6-Month Bills:

- Average Yield -0.0907% (prev. -0.0907%)

- Average Price 100.045 (prev. 100.045)

- High Yield: -0.0866% (prev. -0.0866%)

- Low Price 100.043 (prev. 100.043)

- % Allotted At High Yield: 27.7941% (prev. 28.7513%)

- Bid/Cover: 3.547x (prev. 4.416x)

AUSSIE BONDS: The AOFM sells A$1.0bn of the 1.75% 21 Nov ‘32 Bond, issue #TB165:

The Australian Office of Financial Management (AOFM) sells A$1.0bn of the 1.75% 21 November 2032 Bond, issue #TB165:

- Average Yield: 2.1435% (prev. 1.8898%)

- High Yield: 2.1450% (prev. 1.8925%)

- Bid/Cover: 3.2250x (prev. 3.6550x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield 65.3% (prev. 4.9%)

- Bidders 45 (prev. 48), successful 20 (prev. 26), allocated in full 12 (prev. 15)

FOREX: Greenback Struggles Amid Risk-On Flows, Softer U.S. Tsy Yields

A key gauge of broader greenback strength (DXY) lost altitude in tandem with U.S. Tsy yields, with participants looking to the release of U.S. CPI data on Thursday. Dollar weakness may have been exacerbated by a pullback in USD/JPY after the pair rejected resistance from Y115.68, the high print of Jan 28. The move shielded the yen from the impact of reduced demand for safe haven currencies, with both USD and CHF faltering amid a decent showing from the equity markets.

- The Antipodean currencies benefited from greater appetite for risk proxies. Australian Westpac-Melbourne Institute Index of Consumer Sentiment fell to a near-neutral level, with breakdown data playing into the hands of RBA hawks, as consumers' expectations of an increase in mortgage rates rose markedly.

- Today's data docket is fairly empty, which turns focus to central bank speak. Comments are due from Fed's Bowman & Mester, ECB's Schnabel, BoJ's Nakamura, BoE's Pill & BoC's Macklem.

FOREX OPTIONS: Expiries for Feb09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1300-20(E1.0bln)

- USD/JPY: Y113.80-00($964mln), Y114.50-55($840mln), Y115.00($725mln), Y115.50-60($822mln), Y115.70-90($1.1bln)

- AUD/USD: $0.7150-70(A$1.0bln)

- USD/CAD: C$1.2720-30($740mln)

ASIA FX: Asia EM FX Awaken As U.S. Tsy Yields Slip

Most currencies from the Asia EM basket garnered some strength amid a downtick in the broader USD strength/U.S. Tsy yields. Better risk appetite lent support to regional FX.

- CNH: Spot USD/CNH slipped into a loss as the greenback faltered along U.S. Tsy yields. The PBOC fix was only marginally firmer than forecast, providing no market impulse on its own.

- KRW: The South Korean won printed its best levels in two weeks, drawing support from better appetite for risk.

- IDR: The rupiah advanced with participants on the lookout for comments from top Indonesian officials, including BI Gov Warjiyo & FinMin Indrawati.

- MYR: The ringgit failed to register gains in sync with its regional peers. Participants assessed Malaysia's Covid-19 situation, as officials expressed willingness to ease restrictions despite rising daily cases.

- PHP: Spot USD/PHP retreated after rejecting key resistance from PHP51.500 on Tuesday. The level has withheld a number of attacks at the start to 2022, becoming a key near-term bullish target.

- THB: The baht caught a bid even as daily Covid-19 caseload hit the highest level since Sep 23. The Bank of Thailand will deliver their monetary policy decision today, but the consensus view is that they will keep the policy rate unchanged.

EQUITIES: Asia-Pac Higher On Wall St. Lead, Chinese Mega Cap Rally

The major Asia-Pac equity indices trade 0.3% to 2.0% higher, on the back of a positive lead from U.S. equities.

- The Hang Seng leads the gains, driven by a rally in Chinese mega cap tech names such as Alibaba, following a rise in their U.S. ADRs on Tuesday. The Hang Seng Tech index gained 3.1%, after a 3.9% rise in the Nasdaq Golden Dragon China index during the U.S. session.

- The CSI300 brings up the rear amongst regional peers, adding 0.3%. A broad rally in Chinese property developer shares (on the back of the latest unwind of tightening measures hampering the sector) was countered by weakness in high-beta equities, with the tech-heavy ChiNext and STAR50 unchanged to a touch lower at typing. Note that offshore investors haven’t showed much in the way of interest when it comes to following Tuesday’s reported “National Team” buying of mainland Chinese equities, at least when it comes to observable Northbound Hong Kong-China Stock Connect flows. This morning’s cumulative net northbound flows via the Stock Connect channels sit at a relatively paltry ~CNY2bn of purchases.

- The ASX 200 closed 1.1% higher, shrugging off a decline in the Australian Westpac-Melbourne Institute Index of Consumer Sentiment, with the latter pulling back to near-neutral levels.

- E-mini futures trade at the top of their Asia range at typing, 0.4% to 0.5% above their respective settlement levels.

GOLD: Range Trading

Spot remains hemmed in its recently observed range, leaving well-defined technical parameters intact, as participants zero in on Thursday’s U.S. CPI release (with the well-documented global fears re: inflation and recent hawkish turns from the likes of the ECB & BoE front & centre). Tuesday’s pullback from best levels for both our U.S. real yield monitor and the DXY allowed gold to register fresh session highs into Tuesday’s NY close, with bullion finishing just below best levels. Tuesday’s peak has held in narrow Asia-Pac dealing, with spot little changed, just shy of $1,830/oz.

OIL: A Marginal Uptick In Asia

WTI and Brent futures are ~$0.40 better off at typing, consolidating above Tuesday's worst levels aided by an uptick in U.S. e-mini equity futures. Crude specific news has also been supportive, with the latest round of weekly U.S. API crude inventory figures reportedly revealing drawdowns in crude, gasoline, and distillate inventories.

- A reminder that hope surrounding the Iranian nuclear talks in Vienna pressured crude prices on Tuesday, leaving WTI & Brent futures ~$2.00 lower on the day come settlement. EU foreign policy chief Josep Borrell noted that parties to the talks were “reaching the last steps” of negotiations, although the discussions still rely on intermediaries from third party nations when it comes to facilitating U.S.-Iran communique.

- Tuesday also saw the EIA revise its 2022 U.S. shale production forecasts into positive territory i.e. projecting growth vs. ’21 levels, but this is unlikely to assuage broader fears re: tight oil markets, at least in isolation.

- WTI & Brent have breached technical support (which came in the form of their respective 4 Feb lows), with bears now switching focus to the Jan 31 low in WTI ($86.34) and the Jan 24 low in Brent ($87.05).

- U.S. EIA oil inventory data is due later Wednesday, with the median estimate of those surveyed by Platts looking for a 100K build in headline crude stocks.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 09/02/2022 | 0700/0800 | ** |  | DE | Trade Balance |

| 09/02/2022 | 0900/1000 | * |  | IT | Industrial Production |

| 09/02/2022 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 09/02/2022 | 1310/1310 |  | UK | BOE Pill at UK Monetary Policy outlook conference | |

| 09/02/2022 | 1500/1000 | ** | | US | Wholesale Trade |

| 09/02/2022 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 09/02/2022 | 1530/1030 | | US | Fed Governor Michelle Bowman | |

| 09/02/2022 | 1630/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 09/02/2022 | 1700/1200 |  | CA | BOC Governor Macklem speaks to Chamber of Commerce | |

| 09/02/2022 | 1700/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 09/02/2022 | 1700/1200 | | US | Cleveland Fed's Loretta Mester | |

| 09/02/2022 | 1800/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.