Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Reports of a fire at a Ukrainian nuclear power plant (the largest such facility in Europe) in the wake of Russian shelling triggered sharp risk-off price action in Asia, although wider risk aversion has moderated after it became apparent that the fire was limited to an administrative building on the outskirts of the facility. The reactors suffered no meaningful damage. Note that the Russian army has seized control of the facility in the last 30 minutes.

- AUD's solid run of outperformance continued overnight

- The latest U.S. NFP report headlines the global data docket today, with Eurozone retail sales also due. The Russia Ukraine situation will continue to dominate wider headline flow.

BOND SUMMARY: Frenetic Asia Session Wire Fire At Ukrainian Nuclear Plant Controlled

Sharp risk-off flows kicked in as reports did the rounds of a fire at Ukraine’s largest nuclear power station (the largest such facility in Europe), with the Ukrainians pointing to a Russian shelling of the facility. It took some time before it became apparent that the fire was limited to an administrative building on the outskirts of the complex, with the nuclear reactors avoiding anything in the way of material damage. Caution remained apparent for the remainder of the session.

- TYM2 is +0-15 last, printing 127-31+, well shy of the peak of its 1-15 Asia range, operating on ~450K lots ahead of European hours. Cash Tsy trade sees the major benchmarks run 1.5-5.0bp richer, with 7s leading and 2s lagging. Comments from NY Fed President Williams didn’t move the market, as he looked to play down stagflationary worry and OK’d a series of rate hikes from March. Selling in the very front end of the Eurodollar strip has been apparent into European hours, perhaps as European traders look for an extension in yesterday’s EDH2/SFRH2 & FRA/OIS widening (which was primarily driven by a jump in the 3-month LIBOR fixing and 40K block sale of EDH2). Monthly NFPs headline the docket during NY hours.

- JGB futures finished 8 ticks higher, but 26 ticks off of their session peak. Cash JGBs ultimately bull flattened, with the 5- to 7-Year zone underperforming as JGB futures moved back towards neutral levels. There hasn’t been much in the way of meaningful domestic headline flow, with Japanese PM Kishida flagging the importance of FX rates moving in a stable manner. He also made a pledge that the government will do all it can to manage the economy and fiscal policy in an appropriate manner. Kishida then noted that he wants the BoJ to continue to aim for the 2% inflation level, while stressing that he will pick the “most appropriate” successor for BoJ Governor Kuroda. Finally, Kishida pointed to pressure on oil producing nations to boost supply, while Chief Cabinet Secretary Matsuno noted that the cabinet has approved a Y360bn response re: higher oil prices (with more to come next FY, if required).

- Aussie bond futures followed the broader gyrations when it came to risk appetite, with futures quickly unwinding overnight losses, before returning to near neutral levels. That left YM -2.0, while XM was +1.5 at the bell. Cash ACGB trade saw cheapening further out the strip (in the 15+-Year zone), while the 7- to 12-Year zone firmed a touch. The IR strip settled 3-9bp cheaper through the reds, after a volatile session, with the late whites and early reds leading the way lower. There wasn’t much in the way of meaningful domestic headline flow.

JGBS AUCTION: Japanese MOF sells Y4.6209tn 3-Month Bills:

The Japanese Ministry of Finance (MOF) sells Y4.6209tn 3-Month Bills:

- Average Yield -0.0934% (prev. -0.0904%)

- Average Price 100.0251 (prev. 100.0243)

- High Yield: -0.0856% (prev. -0.0837%)

- Low Price 100.0230 (prev. 100.0225)

- % Allotted At High Yield: 44.8954% (prev. 97.6211%)

- Bid/Cover: 2.490x (prev. 3.096x)

AUSSIE BONDS: The AOFM sells A$1.0bn of the 1.50% 21 Jun ‘31 Bond, issue #TB157:

The Australian Office of Financial Management (AOFM) sells A$1.0bn of the 1.50% 21 June 2031 Bond, issue #TB157:

- Average Yield: 2.1597% (prev. 1.7001%)

- High Yield: 2.1625% (prev. 1.7025%)

- Bid/Cover: 3.1650x (prev. 2.5950x)

- Amount allotted at highest accepted yield as percentage of amount bid at that yield 45.7% (prev. 44.3%)

- Bidders 38 (prev. 39), successful 16 (prev. 16), allocated in full 7 (prev. 10)

AUSSIE BONDS: AOFM Weekly Issuance Slate

The AOFM has released its weekly issuance slate:

- On Monday 7 March it plans to sell A$1.0bn of the 0.25% 21 November 2024 Bond.

- On Tuesday 8 March it plans to sell A$150mn of the 0.25% 21 November 2032 Indexed Bond.

- On Wednesday 9 March it plans to sell A$1.0bn of the 1.75% 21 November 2032 Bond.

- On Thursday 10 March it plans to sell A$1.5bn of the 24 June 2022 Note & A$1.0bn of the 22 July 2022 Note.

US DATA PREVIEW: MNI Payrolls Preview

- February nonfarm payrolls are expected to have risen by +420k according to the Bloomberg survey median with dispersion of views quite evenly spread.

- The strength is seen coming from a rebound after Omicron-related disruption in January, even though January was surprisingly strong. Distortions dropping out from annual adjustments should make the report easier to digest.

- We see potential asymmetric upside risks to March pricing of hikes but more balanced risks to the broader rate path, all ahead of CPI on Mar 10.

- See the full report below with previews from 10 sell-side analysts.

- https://roar-assets-auto.rbl.ms/documents/14079/USNFPMar2022Preview.pdf

US DATA PREVIEW: Primary Dealer NFP Estimates

| Primary Dealer | Estimate | Primary Dealer | Estimate |

|---|---|---|---|

| Morgan Stanley | +730K | Amherst Pierpoint | +700K |

| NatWest | +650K | Societe Generale | +555K |

| Jefferies | +550K | Citi | +510K |

| Goldman Sachs | +500K | J.P.Morgan | +500K |

| Nomura | +500K | Barclays | +450K |

| Daiwa | +450K | Scotiabank | +450K |

| UBS | +425K | BMO | +420K |

| BNP Paribas | +400K | HSBC | +400K |

| RBC | +380K | Bank of America | +375K |

| Wells Fargo | +375K | Mizuho | +300K |

| TD Securities | +300K | Credit Suisse | +250K |

| Deutsche Bank | +200K | -- | |

| Dealer Median | +450K | BBG Whisper | +375K |

US DATA PREVIEW: MNI BRIEF: St. Louis Fed Model Signals 450k Gain For Feb Jobs

U.S. employment likely rose by 450,000 in February as measured by the BLS's household survey, according to St. Louis Fed economist Max Dvorkin's analysis of real-time employment data from scheduling software company Homebase.

- Annual revisions to the BLS's population estimates at the start of the year complicate how to read the model's output for February. The St. Louis Fed model had undershot the better-than-expected January jobs report, but the improvement in the household survey at the start of the year largely reflected a 1 million increase in U.S. population and less so the growing share of employed people, Dvorkin said.

- Using January as a base, the model expects a seasonally adjusted increase of 1.5 million employed for February. But with December as a base, the model sees a 184,000 decline in employed. "My personal forecast is in between these two numbers," Dvorkin said.

CHINA: NPC: What To Look For

Chinese Premier Li is set to unveil the country’s official 2022 economic targets on Saturday, via the Government Work Report.

- Sell-side consensus seemingly looks for a GDP growth target of 5.0-5.5%, with potential alternatives including “around 5.5%” and “above 5.0%.” Any of these outcomes would represent a markdown vs. the “above 6%” target set in ’21 (actual GDP growth sat at 8.1% last year).

- China’s COVID zero policy continues to present headwinds to domestic economic activity, with local lockdowns, port bottlenecks and a lack of tourism providing the major points of note. Still, recent days have seen growing speculation surrounding the potential for an adjustment in China’s COVID stance. An official has noted that China is looking for ways to reduce the “social costs” of its strict COVID zero strategy, although BBG sources suggested that the existing policy will “remain throughout 2022.”

- Most expect the fiscal deficit ratio to be left unchanged at 3.2%, although some look for a markdown to ~3.0%, or even 2.8%. Policymakers have pointed to the deployment of an “appropriate” fiscal deficit during ’22 in recent communique. Fiscal stimulus will likely become more supportive, as China battles the headwinds from the previously outlined economic issues that it faces. Particular focus is set to fall on infrastructure, in addition to continued support for electric vehicles and rural economies.

- Sell-side consensus looks for no change in the local government special bond issuance quota, which stood at CNY3.65tn in ’21. There is clear upside risk to this (none of the estimates that we have seen look for a move onto the CNY4tn handle).

- Elsewhere, there is little in the way of real discussion when it comes to China shifting its 3% inflation target (Y/Y headline CPI is running well below target at present, +0.9% in January, while PPI runs well above that level, +9.1% in January).

- China’s credit impulse has started to turn in recent months, after a precipitous fall in ’21. The credit impulse has a strong correlation with PPI (with a lag), which has pulled back from ’21 highs given the fall in the credit impulse during ’21. The recent acceleration in the commodity price boom may challenge that trend in the coming months.

- Monetary policy is set to remain accommodative, with most of the sell-side looking for further PBoC easing in H122, which is perceived to the window for such action given the pullback in PPI and expectations for the Fed to embark on a “series” of rate hikes, starting later this month. The PBoC’s switch to a more pro-growth stance has already seen some easing in early ’22. Still, the phraseology surrounding monetary policy should not move from “prudent monetary policy will be flexible and appropriate.”

- Policy towards housing is likely to be less restrictive, given worries surrounding the property sector and GDP growth slowdown. Indeed, some of the more notable property hawks in the policymaking sphere have softened their tone in recent weeks. The authorities will likely implement a less prescribed directive, allowing some variance in housing policy on a region-by-region basis to facilitate a soft landing for the sector. Still, the authorities will continue to be of the view that "housing is for living in, not for speculation," and we shouldn’t expect the housing market to be used as a short-term booster for wider GDP growth given the extensive rhetoric pushing back against such ideas. China needs to increase the availability of affordable housing, while the direction of travel re: the property tax trials will also be eyed (this matter may not even be mentioned, given the worry and cancellation of the expansion of the scheme).

- The unemployment target will remain somewhere in the region of 5.5%, with the government needing to facilitate social stability via economic assurance on a household level.

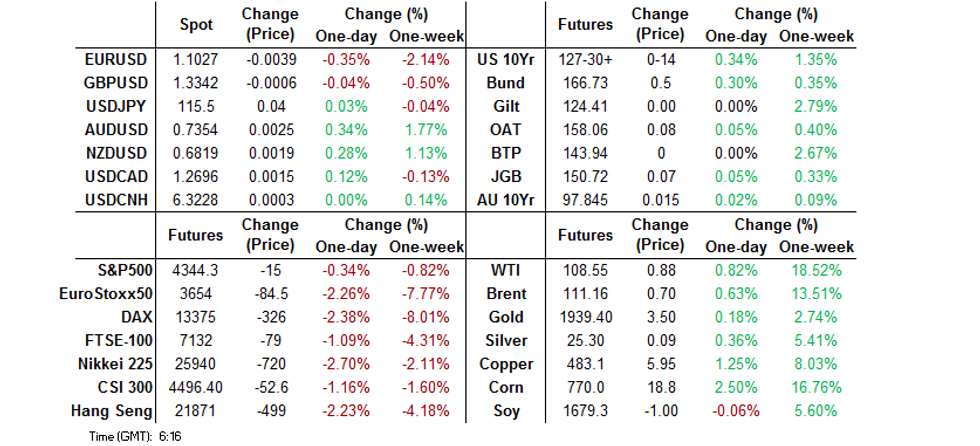

FOREX: Russian Attack On Ukraine's Key Nuclear Power Plant Spooks Europe

European currencies got battered while the risk switch flicked to off as Russian troops shelled Ukraine's (and Europe's) largest nuclear plant setting it ablaze. Initial headlines flagged the danger posed by damaged reactors and suggested that Russian shelling prevents fire brigades from entering the plant. The news rattled markets by raising the prospect of potential radioactive contamination, but subsequent headlines helped soothe the nerves. Ukrainian officials clarified that the fire broke out in a training complex outside the main perimeter of the plant, leaving essential equipment intact and causing no change in radiation levels. The emergency services managed to put out the fire but the incident fuelled fears that continued fighting may lead to dramatic unforeseen consequences. President Zelensky and his ministers contacted their Western counterparts, with UK PM Johnson pledging to call an emergency session of UNSC to discuss the situation.

- Major continental European currencies got battered on the back of contagion risk, with events at Zaporizhzhia Nuclear Power Plant drawing attention to risks surrounding the war in Ukraine. EUR/CHF printed a session low of CHF1.0117, a fresh multi-year trough, before trimming some losses. The Scandies, EUR and CHF continue to trade on a softer footing as we head for the London session.

- The main Asia-Pac risk barometer AUD/JPY fell to Y84.16 in the initial reaction to the Zaporizhzhia NPP news before bouncing to a new four-month high. The Antipodeans gained the most from the unwinding of initial risk-off moves and jumped onto the top of the G10 pile. The yen is the third best performer as the attack on Ukraine's key nuclear facility continues to spook Europe.

- U.S. NFP report headlines the global data docket today, with EZ retail sales also due.

FOREX OPTIONS: Expiries for Mar04 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1100-20(E1.4bln), $1.1300-15(E1.2bln), $1.1325-30(E681mln)

- USD/JPY: Y114.00($1.5bln), Y115.00($675mln), Y116.00($680mln)

- EUR/GBP: Gbp0.8530(E610mln)

- AUD/USD: $0.7030(A$1.2bln), $0.7300(A$841mln)

- USD/CAD: C$1.2495($520mln), C$1.2595-00($1.2bln), C$1.2700($1.4bln), C$1.2800($831mln)

- USD/CAD: C$1.2700-20($1.6bln)

ASIA FX: Won Leads Losses & Prints Cycle Low, Peso Cracks Through Key Support

Participants continued to assess the fallout from the ongoing war in Ukraine, with inflation data from several Asian emerging economies providing regional points of note.

- CNH: Spot USD/CNH unwound its initial uptick and dipped into negative territory, while holding a fairly narrow range in the process. China begins its "Two Sessions" on Saturday, with the annual National People's Congress due to kick off with a keynote speech from Premier Li, who will outline economic targets for this year.

- KRW: South Korean won went offered, with spot USD/KRW printing its best levels since Jun 23, 2020. The won retreated on risk aversion, even as South Korea's CPI beat expectations. Headline inflation accelerated to +3.7% Y/Y in February, with core prices up 3.2% Y/Y.

- IDR: The rupiah was rangebound as local markets re-opened after a public holiday.

- MYR: Spot USD/MYR ground lower. Bank Negara Malaysia kept its main policy rate unchanged Thursday, while flagging the war in Ukraine as a key risk to the global growth outlook.

- PHP: Spot USD/PHP surged above the key PHP51.500 figure, hitting fresh one-year highs, as the Philippines' CPI inflation missed expectations. That level was associated with recent interventions by the Bangko Sentral ng Pilipinas and a key technical barrier. Gov Diokno noted that the central bank "continues to have a wide arsenal of policy instruments to respond" to the war in Ukraine.

- THB: Spot USD/THB erased its initial uptick. Thailand's CPI surged 5.28% Y/Y in February, smashing expectations, amid mounting concerns about rising living costs. Core prices rose 1.80% Y/Y, also beating consensus forecast.

EQUITIES: Taking A Tumble On Geopolitical Volatility

Major regional equity indices trade sharply lower at writing, failing to recover from losses observed earlier in the Asia-Pac session. The region-wide decline was facilitated by worry over a well-documented fire at the Ukrainian Zaporizhzhia nuclear plant (with Ukraine pointing to Russian shelling of the facility), spurring risk-off moves that saw high-beta stocks across various sectors again struggle on the day. Containment of the fire to an administrative building at the Ukrainian nuclear facility failed to provide a notable boost to the space.

- The Hang Seng leads losses, printing 2.7% worse off, on track for a third straight week of declines. China-based tech stocks bore the brunt of the selling, with steep declines witnessed in large caps Alibaba (-4.9%), Meituan (-7.1%), and Tencent (-3.8%). The Hang Seng Tech index correspondingly deals 4.1% weaker at typing, notching a fresh all-time low (its inception came in Jul ’20).

- The CSI300 is on track to close lower for a third consecutive day, sitting 0.9% weaker at typing. Losses in the richly valued consumer discretionary and consumer staples sub-indices continue to weigh on the index, with steep declines again seen in large Chinese liquor stocks such as Kweichow Moutai (-2.4%) and Wuliangye Yibin Co (-2.5%).

- The ASX200 fell to a lesser extent than the remainder of the major regional indices, closing 0.8% lower. The index snapped a five-day streak of gains, with major crude benchmarks operating a little shy of their cycle highs

- U.S. e-mini equity index futures sit 0.7% to 0.9% lower into European hours.

GOLD: Slightly Higher As Knee-Jerk Reaction To Nuclear Plant Fire Moderates

Gold trades ~$4/oz firmer to print $1,940/oz at writing, back from best levels of the session ($1,950.88/oz) as the risk-off impulse from reports of Ukraine’s Zaporizhzhia nuclear plant being set ablaze by a Russian attack eased (the main nuclear facilities seemingly avoided meaningful damage, with a training facility providing the scene of the fire). The precious metal continues to operate around the top of Thursday’s range, as worry surrounding the Russia-Ukraine conflict continues to drive price action.

- On the wider Russia-Ukraine conflict, negotiators from both sides made some progress after meeting on Thursday, agreeing on the possibility of localised, temporary ceasefires for the establishment of “humanitarian corridors”. Both parties are due to meet for a third round “early next week”. Still, the conflict continues in full swing.

- Looking ahead, focus will turn to U.S. NFPs due later (1330 GMT), with March FOMC dated OIS now pricing in a little under 25bp of tightening (Fed Chair Powell’s recently voiced support for a 25bp hike at that meeting).

- From a technical perspective, gold remains in an uptrend and trades within a bull channel drawn from the Aug 9 low. Resistance is currently situated at $1,974.3/oz (Feb 24 high), while support is located some distance away at $1,878.4/oz (Feb 24 low and key short-term support).

OIL: Slightly Higher After Early Moves

WTI is +$2.40 and Brent is +$1.90 at typing, printing ~$110.10 and ~$112.40respectively.

- Both benchmarks have pulled back from the session's best levels, with the earlier move higher driven by reports of Ukraine's Zaporizhzhia nuclear plant being hit by fire. Worry re: the situation has since eased, with the plant director stating to Ukrainian media that radiation security had been secured, while later reports pointed to damage being limited to a training building and an offline nuclear reactor (albeit containing nuclear fuel).

- To recap Thursday's movements, WTI and Brent hit fresh multi-year highs (highest since '08 and '12 respectively) on well-documented supply concerns re: Russian crude exports before closing lower, as elevated hope surrounding a possible Iranian nuclear deal applied some pressure to the space. To elaborate, the Russian envoy at the Iranian talks noted that a ministerial meeting to formalise the deal was now likely (although no timeline was provided), while the head of the International Atomic Energy Agency has announced a visit to Tehran on Saturday, with the aim of potentially addressing one of the final issues that have hindered talks (specifically on "outstanding safeguards").

- On the technical front, WTI and Brent see resistance at $120.00 (psychological round number), while support is located at the Mar 2 lows of $105.18 and $106.83 respectively.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 04/03/2022 | 0700/0800 | ** |  | DE | trade balance |

| 04/03/2022 | 0745/0845 | * |  | FR | industrial production |

| 04/03/2022 | 0830/0930 | ** |  | EU | IHS Markit Final Eurozone Construction PMI |

| 04/03/2022 | 0900/1000 | *** |  | IT | GDP (f) |

| 04/03/2022 | 0930/0930 | ** |  | UK | IHS Markit/CIPS Construction PMI |

| 04/03/2022 | 1000/1100 | ** | | EU | retail sales |

| 04/03/2022 | 1330/0830 | *** |  | US | Employment Report |

| 04/03/2022 | 1500/1000 | * |  | CA | Ivey PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.