Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

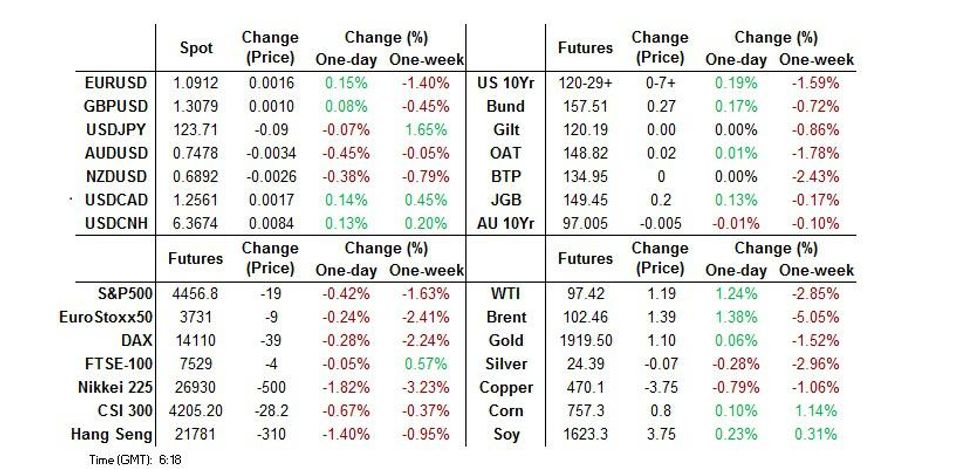

- Equity markets came under some pressure in Asia, while Tsys firmed at the margins, with most pointing to growth worries re: The Fed's B/S wind down outline as the driving force.

- There was little in the way of major headline flow to note in Asia-Pac hours, leaving Fed matters front & centre.

- On the data front, Eurozone retail sales, German industrial output & U.S. weekly jobless claims take focus from here. Comments are due from BoE's Pill as well as Fed's Bullard, Bostic & Evans. In addition, the ECB will publish the account of its March monetary policy meeting.

US TSYS: All About The Caps

Tsys operate shy of best levels as we move towards London trade, after a couple of rounds of richening were seen in Asia (with the second round failing to extend on the first round), with some of the gains then pared. It seems that growth worries stemming from the Fed’s B/S run off plans drove the bid in Asia. TYM2 +0-09 at 120-31, 0-06+ shy of the session peak, operating around the middle of its Asia range on volume of ~145K. Cash Tsys are 1.5-3.0bp richer across the curve, with 5s outperforming and bull steepening apparent. The 2- to 10-Year zone printed through Wednesday’s yield troughs, with the more pronounced breaks coming in the front end of the curve, but those benchmarks now operate back around Wednesday’s lows (in yield terms). Asia flow was headlined by block sales of FVK2 113.25 puts (-5K in total) and block FV/TY flow (2 blocks totalling 9,016 vs. 5,553, potentially steepener flow, but unsure).

- To recap, the minutes from the March FOMC meeting saw the Fed outline the parameters that it has identified when it comes to shrinking its B/S. The Fed will limit B/S runoff to $95bn/month ($60bn Tsys, $35bn MBS), phased in over 3 months/modestly longer (if market conditions continue to warrant) with all indications that the formal announcement will come at the May FOMC meeting. Interestingly, many participants would have preferred to hike rates by 50bp at the March meeting, although Ukraine proved to be the limiting factor on this front (Bullard was the only dissenter who called for a 50bp hike), with many participants noting that “one or more 50 basis point increases in the target range could be appropriate at future meetings, particularly if inflation pressures remained elevated or intensified.” Market reaction was two-way in nature, with benchmark yields across the curve finishing Wednesday around pre-minute levels after fresh YtD highs were registered across the curve. The 2-/10-Year and 5-/30-Year yield curves went out around session steeps, as the wider curve twist steepened.

- Weekly jobless claims data and Fedspeak from Bullard (’22 voter), Bostic (’24 voter) & Evans (’23 voter) will cross during NY hours.

JGBS: 7s Lead The Bid On Futures Uptick, 30-Year JGB Supply Sees Soft Cover

JGB futures generally followed the broader ebb and flow of wider core global FI markets during the Tokyo morning, although the bid has been a little stickier during the afternoon. Still, JGB futures have failed to test early Tokyo highs, last +19 vs. Wednesday’s settlement. Cash JGBs are little changed to ~2bp richer, with 7s maintaining their early outperformance, aided by the bid in futures, while 20s provided the weakest point on the curve.

- BoJ board member Noguchi stuck to the wider dovish script provided by the central bank, underlining the need for continued easing, while BoJ Exec. Dir. Uchida flagged the positives surrounding the BoJ’s ultra-loose policy settings.

- The latest round of 30-Year JGB supply saw firm enough pricing, with the low price providing a modest beat vs. wider expectations, although the cover ratio softened at the margin, holding comfortably below the 6-auction average (3.29x). It would seem that the previously flagged worry re: continued market vol. and spill over from offshore bond market gyrations stood in the way of wider interest at today’s auction.

AUSSIE BONDS: Curve Steepens, YM Unwinds Some Of Early Squeeze Higher

YMM2 has erased some of the early squeeze higher, but hasn’t gotten anywhere near neutral levels, last +4.5, while XM has generally marched to the beat of U.S. TY futures, with a lack of meaningful idiosyncratic drivers evident, to last deal unch. The YM/XM curve has bull steepened, although it sits off the early session wides, while 10+-Year cash ACGBS are marginally cheaper on the day, resulting in twist steepening of the broader ACGB curve. EFPs are mixed, with some notable twist flattening of the 3-/10-Year box apparent. Meanwhile, Bills run 1-8 ticks higher through the reds, with the post-FOMC minutes move higher in U.S. Eurodollar futures providing at least some of the impetus there, n addition to the squeeze in YM.

- Elsewhere, the latest round of ABS payrolls data revealed that “payroll jobs fell 0.6% in the month to 12 March 2022. There were differences across the fortnights, with payroll jobs falling by 0.8% in the second half of February and then rising slightly, by 0.2%, in the first half of March. These changes in payroll jobs coincided with adverse weather conditions and flooding in New South Wales and Queensland (in late February), the continuing influence of the COVID-19 Omicron variant and easing of pandemic restrictions across the country. Given the disruption to business operations from the weather and Omicron infections, the increase in payroll jobs in early 2022 continued to be weaker than in both 2020 and 2021, particularly over the last month.”

JAPAN: Plenty To Note In Weekly International Security Flow Data

Bonds dominated the latest round of Japanese weekly international security flows data, with Japanese investors shedding foreign bonds for a sixth straight week (the Japanese FY end and recent run of JPY weakness potentially explains that dynamic). Meanwhile, foreign investors were net sellers of Japanese bonds for a third consecutive week, even after the BoJ reinforced its YCC settings.

- When it comes to equities, Japanese investors recorded the largest weekly amount of net selling of foreign equities since early January, while foreign investors broke a streak of nine consecutive weeks of net sales of Japanese equities.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

|---|---|---|---|

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | -1673.7 | -703.3 | -2650.9 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | -781.3 | 24.6 | -827.8 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | -1336.6 | -2396.3 | -3359.6 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | 543.2 | -250.7 | -1389.6 |

FOREX: Caution Takes Hold, Circling Fed Hawks Cast Shadow Over Asia

Initial defensive feel deepened as the Asia-Pac session progressed, with G10 FX trading in a typical risk-off fashion. Regional players assessed the minutes from the FOMC's March monetary policy meeting, which reaffirmed intensifying hawkish leanings among Fed policymakers. The prospect of rapid balance-sheet reduction and the Fed's apparent sense of comfort with a potential 50bp rate hike undermined risk appetite, albeit the greenback struggled for meaningful topside impetus.

- As one might expect, high-beta currencies went offered and safe havens caught a bid. This brought some reprieve to the embattled yen, even as BoJ's Noguchi reaffirmed the Bank's commitment to its ultra-loose policy stance. USD/JPY shed a handful of pips but its RSI remained in overbought territory.

- Risk aversion translated into AUD/USD sales, preventing a golden cross formation from materialising on the daily chart. The pair's ascending 50-DMA now intersects just a few pips shy of the 200-DMA.

- Offshore yuan lost ground after China's State Council signalled intention to loosen monetary policy "at appropriate time" in a bid to stimulate the real economy amid heightened domestic and global economic risks.

- On the data front, EZ retail sales, German industrial output & U.S. weekly jobless claims take focus from here. Comments are due from BoE's Pill as well as Fed's Bullard, Bostic & Evans. In addition, the ECB will publish the account of its March monetary policy meeting.

FOREX OPTIONS: Expiries for Apr07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0800(E1.5bln), $1.0875(E828mln), $1.0900-15(E3.1bln), $1.0920-36(E3.1bln), $1.0965-70(E556mln), $1.1000-10(E2.2bln), $1.1025(E2.0bln), $1.1100-10(E1.1bln)

- GBP/USD: $1.3200-15(Gbp544mln)

- EUR/GBP: Gbp0.8375-90(E519mln)

- EUR/JPY: Y134.50(E677mln), Y136.00(E521mln)

- AUD/USD: $0.7575-85(A$624mln)

- USD/CAD: C$1.2500($635mln), C$1.2535-45($540mln), C$1.2575-90($1.3bln)

ASIA FX: Yuan Drops On Prospect Of Policy Easing, Most Asia EM FX Stay Rangebound

USD/Asia crosses were happy to hug tight ranges as participants assessed hawkish FOMC minutes published Wednesday and the prospect of more policy easing from China.

- CNH: Spot USD/CNH crept higher as the region played catch up with FOMC minutes, while China's State Council signalled that officials will use monetary tools and other measures "at appropriate time" to boost consumption.

- KRW: The won remained stable after the release of better than expected Q1 earnings report from Samsung.

- IDR: Spot USD/IDR oscillated around neutral levels as participants awaited Bank Indonesia Dep Gov Waluyo's speech on policy exit/support for economic recovery.

- MYR: Spot USD/MYR pushed higher, some saw it as a function of Wednesday's slide in oil prices, albeit crude regained poise in Asia.

- PHP: Spot USD/PHP traded comfortably within yesterday's range, ignoring domestic data signals. The unemployment rate stayed at 6.4% in February, while the local statistics agency revised higher its GDP growth estimate for 4Q2021 & full 2021.

- THB: Spot USD/THB printed a one-week high before trimming some gains as onshore markets re-opened after a holiday. Note that recent days saw the 50-DMA cross below the 200-DMA.

EQUITIES: Lower As Fed Worry Spills Into Asia

Virtually all Asia-Pac equity indices are in the red for a second day, following another negative lead from Wall St. Tech-related names across the region struggled in the wake of the tech-heavy Nasdaq’s underperformance, while Chinese and Hong Kong markets received some support from the Chinese authorities again voicing their intention to increase monetary stimulus “at an appropriate time”.

- The CSI300 fell to a lesser extent than most major regional peers, dealing 0.9% softer at typing. The move lower comes despite Chinese officials from a State Council meeting late on Wednesday declaring their intention to support the economy amidst intensifying “complexity and uncertainty of domestic and foreign environments” that have “exceeded expectations”. A note that there was a lack of details re: specific easing measures (e.g. reserve ratio cuts), likely limiting optimism for now, with the CSI300 seen operating around session lows below Wednesday troughs at typing.

- The Hang Seng sits 1.2% worse off after reversing gains made earlier in the session, with nearly all constituents trading flat to lower at writing. The real estate sub-index brings up the rear, pulling back from six-week highs made on Wednesday amidst evident pressure from an ongoing COVID outbreak in Hong Kong and China. China-based tech sold off as well, with the Hang Seng Tech Index trading 2.0% lower at typing.

- U.S. e-mini equity index futures sit 0.4% weaker apiece at typing.

GOLD: Slightly Lower In Asia

Gold sits ~$3/oz lower to print $1,922/oz at writing, operating just above session lows as an initial downtick in nominal U.S. Tsy yields has eased, giving way to lingering impetus from the relatively hawkish Mar FOMC minutes release on Wednesday.

- To elaborate, aforementioned FOMC minutes saw Fed officials propose potentially phased caps of $95bn per month in balance sheet reductions (largely in line with expectations from some quarters), while many attendees favoured “one or more” 50bp hikes going forward, flagging dependence on inflation data.

- Looking at Wednesday's price action, the precious metal closed little changed, struggling to make headway above the $1,930/oz price level as the USD (DXY) and U.S. real yields made fresh cycle highs.

- Elsewhere, OIS markets are pricing a cumulative ~215bp of Fed tightening for the rest of calendar ‘22, pointing to the potential for multiple 50bp rate hikes in the remaining six meetings for the year.

- From a technical perspective, bullion remains range bound. Key support is located around ~$1,908./oz (50-Day EMA), with further support at $1,890.2/oz (Mar 29 low and bear trigger). On the other hand, resistance is unchanged at $1,966.1/oz (Mar 24 high).

OIL: A Touch Above Three-Week Lows As IEA Release, COVID Outbreak In China Eyed

WTI is ~+$1.60 and Brent is ~+$1.80, printing $97.80 and $102.90 respectively at writing and operating a little above three-week lows recorded on Wednesday.

- To recap, both benchmarks closed ~$6 softer apiece on Wednesday, with non-U.S. International Energy Agency (IEA) member countries announcing plans to release 60mn bbls of crude from strategic reserves, alleviating some worry driving crude prices re: supply tightness. A note that the planned commitment comes on top of U.S. announcements last week to release 180mn bbls from the U.S. SPR.

- Looking to China, Shanghai has notched its sixth record-high daily COVID case count, with the tally for Apr 6 coming in just shy of 20K. Well-documented concern re: weaker Chinese energy demand has persisted as the city’s lockdown has been extended indefinitely, with most businesses and factories remaining shut for now.

- Elsewhere, EIA data released on Wednesday saw a surprise build in U.S. crude and distillate stockpiles, but a larger than expected drawdown in gasoline inventories and a decline in Cushing hub stocks as well. This comes after figures observed in reports of Tuesday’s weekly API estimates, which had pointed to increases in crude, distillate, and hub stocks, but a drawdown in gasoline stockpiles.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/04/2022 | 0545/0745 | ** |  | CH | unemployment |

| 07/04/2022 | 0600/0800 | ** |  | DE | Industrial Production |

| 07/04/2022 | 0600/0700 | * |  | UK | Halifax House Price Index |

| 07/04/2022 | 0900/1100 | ** |  | EU | retail sales |

| 07/04/2022 | 1130/1330 | | EU | ECB March meet Accts published | |

| 07/04/2022 | 1215/1315 | | UK | BOE Pill Opening at BOE Sovereign Bond Market Conference | |

| 07/04/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 07/04/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 07/04/2022 | 1300/0900 | | US | St. Louis Fed's James Bullard | |

| 07/04/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 07/04/2022 | 1530/1130 | ** | | US | NY Fed Weekly Economic Index |

| 07/04/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 07/04/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 07/04/2022 | 1800/1400 | | US | Atlanta Fed's Raphael Bostic, Chicago Fed's Charles Evans | |

| 07/04/2022 | 1900/1500 | * | | US | Consumer Credit |

| 07/04/2022 | 2005/1605 | | US | New York Fed's John Williams |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.