Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

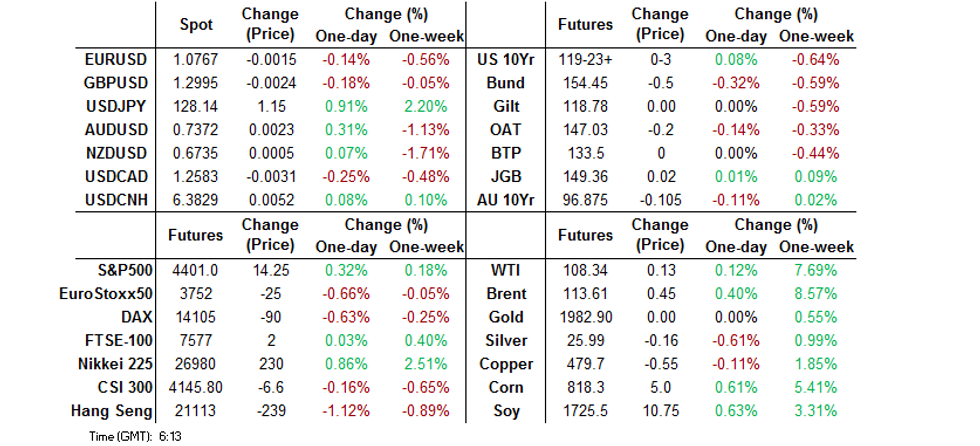

- The yen extends sharp losses despite intensified warnings from Japanese officials. USD/JPY rips through the Y128.00 mark, while its implied volatilities creep higher across the curve.

- Hawkish comments from Fed's Bullard do the rounds, with Antipodean policymakers also in the mood for tightening. By contrast, the BoJ and Asia EM central banks show more caution.

- Activity picks up as markets re-open after Easter holidays.

BOND SUMMARY: Core FI Regain Poise, ACGBs Pare Opening Post-Holiday Losses

Core bond markets found poise despite Fed hawk Bullard noting that he sees a 75bp rate hike as an option (although not his "base case"). Growing hawkish appetites among Fed members contrasted with the PBOC's intention to play a supportive role as China battles the outbreak of Covid-19.

- T-Notes edged higher and last change hands +0-05+ at 119-26, near session highs. Eurodollar futures run up to 3.0 ticks higher through the reds. Cash Tsy yields sit 1.1bp to 2.2bp lower at typing, the curve steepened a tad. The local data docket is limited to housing starts/building permits, with remarks from Chicago Fed Pres Evans also coming up. Worth noting that his colleague Bullard signalled that he sees a 75bp rate hike as an option.

- Aussie bond futures advanced, shrugging off hawkish rhetoric from Antipodean central bankers. YM last deals -2.5 & XM -2.5. Bills trade +2 to - 3 ticks through the reds. Cash ACGB curve bear steepened as trading restarted in Sydney after Easter holidays, but yields then pulled back from best levels. They last sit 6.5-8.7bp higher, off initial highs. The minutes from the RBA's April monetary policy meeting said that economic data warrants a quicker anticipated start to the rate-hike cycle.

- JGB futures climbed after a slightly softer re-open, extending gains after the lunch break. JBM2 trades at 149.42 at typing, 8 ticks above last settlement. Cash JGB yield curve flattened a tad, with 30s leading gains. Japan held a liquidity enhancement auction for off-the-run JGBs with 5-15.5 years until maturity.

FOREX: Yen Keeps Sliding Even As Warnings From Japanese Officials Grow Louder

Japanese authorities further ramped up their warnings on yen weakening, but to no avail. The currency tumbled, even as FinMin Suzuki said that officials were monitoring FX moves with a "strong sense of vigilance," as rapid depreciation has "strong negative aspects" given the current economic climate. His insistence that the exchange rate is decided by the market signalled apparent reluctance to intervene, possibly adding fuel to the selling pressure.

- Spot USD/JPY was in demand into the Tokyo fix and extended gains on the back of Suzuki's comments. The rate soared towards the Y128.00 mark, albeit this round figure remains intact when this is being typed. Implied USD/JPY volatilities surged across the curve, with 1-year tenor printing two-year highs.

- Monday's comments from Fed & BoJ policymakers served as a reminder of growing policy divergence, the main driver of USD/JPY rally over the recent weeks. BoJ Gov Kuroda reaffirmed his commitment to powerful easing, while Fed's Bullard said that a 75bp rate hike was an option.

- Bullard's remarks helped push the dollar index (DXY) to a fresh cycle high as expectations of aggressive tightening by the Fed continued to build. While St. Louis Fed Pres "wouldn't rule it out" that the FOMC could raise interest rates by 75bp, it was not "his base case."

- High-beta currencies were better bid on firmer crude oil prices & upticks in U.S. e-mini futures. Antipodean central bankers showed hawkish inclinations, as RBNZ Gov Orr reaffirmed his team's strong tightening bias, while RBA minutes said that faster inflation/wage growth "have brought forward the likely timing of the first increase in interest rates."

- U.S. housing starts/building permits take focus on the data front, while the central bank speaker slate features Riksbank's Floden & Fed's Evans.

ASIA FX: Asia EM FX Slip, Central Bankers Show Caution

Overnight demand for the U.S. dollar lent support to USD/Asia crosses, with regional central bankers offering generally cautious rhetoric.

- CNH: Offshore yuan lost some altitude as China's Covid-19 situation remained worrying, with the PBOC expected to loosen policy in attempt to soften the blow to the economy.

- KRW: The won wobbled around neutral levels, with all eyes on the confirmation hearing of BoK Governor-nominee Rhee, who vowed to be careful not to damage the economy while adjusting monetary policy.

- IDR: The rupiah held a very tight range ahead of Bank Indonesia monetary policy decision. There was some confusion around the time of the announcement, but it was eventually reverted to the original schedule. Policymakers are widely expected to stand pat on rates.

- PHP: The peso was the worst performer in the Asia EM basket, following the release of underwhelming overseas remittances data on Monday.

- THB: The baht fell to a three-week low after the BoT pledged to maintain an accommodative policy and stay prudent while making further decisions.

- MYR: Malaysian markets were shut in observance of a public holiday.

EQUITIES: Mixed As Chinese Regulatory Worry Takes Centre Stage

Major Asia-Pac equity indices are mixed at writing, following a mildly negative lead from Wall St. The dynamic of industry-specific crackdowns by the Chinese authorities continues to be assessed against the ongoing drumbeat of positive messaging pledging support for the Chinese economy being made in recent days, ultimately seeing Chinese and Hong Kong-based stocks underperform their regional peers.

- The Nikkei 225 is 0.6% better off at typing, backing away from session highs as losses in large-caps Softbank Group and Fast Retailing dragged the index lower, reflecting broader weakness in retail-related names. On the other hand, Tokyo Electron Ltd and Nintendo Co contributed the most to gains, adding to outperformance in energy and materials equities.

- The Hang Seng leads losses after returning from the Easter Monday holiday, rising off one-month lows made earlier in the session to trade 1.9% weaker at typing. China-based tech struggled as investors continue to balance concerns re: regulatory crackdowns against announcements of supportive measures from the Chinese authorities, seeing the Hang Seng Tech Index sit 2.8% softer. A sell-off in financials-related stocks was also observed, with China Merchants Bank Co (-11.5%) bearing the brunt of the selling after its top exec was removed by the board without a reason being given.

- A note that optimism earlier in the month re: the Chinese internet gaming sector (specifically the approval of 45 video games after a nine-month moratorium) has been largely unwound, following a ban on live streaming of “unauthorised” video games announced last Friday, adding to the sector-specific gloom after gaming giant Tencent Holdings’ move to shut down access to unapproved foreign video games on Thursday as well.

- Looking ahead, focus will likely turn to the PBoC’s LPR decision on Wednesday.

- U.S. e-mini equity index futures are 0.3% to 0.6% better off at typing, led by gains in NASDAQ contracts.

GOLD: Flat In Asia; May FOMC Eyed

Gold deals ~$1/oz softer, printing $1,977/oz at writing. The precious metal operates near the bottom of Monday’s range as the USD (DXY) has hit another fresh two-year high, keeping within a tight ~$4 band in fairly limited Asia-Pac dealing.

- To recap Monday’s price action, bullion surrendered gains after hitting fresh five-week highs at $1,998.4/oz, backing away from best levels as nominal U.S. 10-Year Tsy yields and the USD (DXY) pushed higher in the NY session, with the latter hitting two-year highs in the process. Gold ultimately closed a shade above neutral levels for the day, bucking support from a broad downtick in U.S. real yields.

- Up next, Chicago Fed President Evans (‘23 voter) is due to speak at 1605 GMT. Looking further out, focus will shift to Fed Chair Powell at an IMF event on Thursday (1700 GMT), in what will be his final public remarks before the pre-FOMC blackout period.

- A note that May FOMC dated OIS now price in a little under 50bp of tightening for that meeting, largely in line with previous comments from Powell expressing support for such a move.

- Looking to technical levels, the short-term outlook remains bullish. Resistance is situated at $1,998.4/oz (Apr 18 high) and $2,001.6/oz (61.8% retracement of Mar8-29 downleg), while immediate support is seen around ~$1,942.6/oz, near the 20-Day EMA.

OIL: A Little Higher As Libyan Disruption Assessed Against Restart Of Chinese Factories

WTI is ~+$0.20 and Brent is ~+$0.50 at typing, operating a little below three-week highs made on Monday.

- Previously flagged disruptions to Libyan crude facilities due to anti-govt protests have expanded, exacerbating worry re: tightness in global supply. BBG source reports are pointing to >500K bpd in crude output being taken offline for now, a little under half of Libya’s current output.

- Looking to China, authorities in Shanghai have begun a conditional re-opening of some factories in the city (specifically a “whitelist” of 666 companies across a few industries), although reports continue to point to the potential for supply chain disruptions and restricted market access for goods produced amidst continued lockdowns elsewhere.

- Keeping within the country, five of seven districts in China’s largest steel production hub of Tangshan re-entered lockdown conditions after 29 COVID cases were reported for Monday, with a mass testing regime due to be implemented. This comes after the previous lockdown was recently ended (lasted between Mar 22 to Apr 11), raising expectations for national crude steel output to remain under pressure for now.

- Elsewhere, the U.S. EIA’s crude drilling report crossed on Monday, highlighting continued growth in U.S. shale production, with the forecast for May predicting the largest monthly production increase since Mar ‘20. A note that the report also flagged that inventories of low-cost, ready-made wells (DUCs) are hitting multi-year lows, pointing to potential difficulties in increasing crude production in the future.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 19/04/2022 | - |  | EU | ECB Lagarde & Panetta in IMF/World Bank Meetings | |

| 19/04/2022 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 19/04/2022 | 1230/0830 | *** |  | US | Housing Starts |

| 19/04/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 19/04/2022 | 1300/0900 | * | | CA | CREA Existing Home Sales |

| 19/04/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 19/04/2022 | 1605/1205 | | US | Chicago Fed's Charles Evans |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.