- PolicyPolicy

Exclusive interviews with leading policymakers that convey the true policy message that impacts markets.

LATEST FROM POLICY: - MarketsMarkets

Real-time insight on key fixed income and fx markets.

Launch MNI Podcasts - Emerging MarketsEmerging Markets

Real-time insight of emerging markets in CEMEA, Asia and LatAm region

- CommoditiesCommodities

Real-time insight of oil & gas markets

- Data

- MNI ResearchMNI Research

Actionable insight on monetary policy, balance sheet and inflation with focus on global issuance. Analysis on key political risk impacting the global markets.

- About Us

Real-time Actionable Insight

Get the latest on Central Bank Policy and FX & FI Markets to help inform both your strategic and tactical decision-making.

Free Access- Renewed talk of potential FX intervention rendered JPY the best G10 performed for the second consecutive day, allowing USD/JPY to move further away from its recently recorded 24-year highs.

- The long end of the JGB curve outperformed after the latest round of 20-YEar supply avoided the worst case scenario, allowing the curve to bear flatten.

- Today's data highlights include a suite of PMI readings from across the world as well as U.S. jobless claims. Fed Chair Powell will testify on the Hill, while ECB's Nagel & Villeroy are set to deliver speeches. Elsewhere, Norges Bank will announce its rate decision.

US TSYS: Block Sales Cap Early Overnight Uptick

An early downtick in e-minis and weakness in crude futures provided support for the Tsy space in early Asia-Pac dealing, although notable block sales in the futures space knocked the space away from best levels. Note that e-minis hover around neutral levels into London hours, while WTI & Brent crude futures sit ~$2 below settlement levels, nearly $2 off their respective session lows. This leaves TYU2 operating a touch below the middle of its 0-12 overnight range, last +0-01 at 116-31+, on volume of ~120K. Cash Tsys run 0.5bp cheaper to 1.5bp richer across the curve, pivoting around 3s.

- In terms of flow specifics, block sales in TU (2x -2.4K) & TY (-9.0K) futures provided the highlights, with a block buyer of FV futures (+3.0k) and block seller of FVQ2 110.00 puts (-2.5K) also observed.

- The Eurodollar dollar strip has seen some light twist flattening overnight. A quick reminder that yesterday saw recession worries at the fore, which pulled some rate hike premium out of the STIR space. This meant that the EDZ2/H3 spread moved into inverted territory for the first time in this cycle, while the EDZ2/Z3 spread registered fresh cycle lows.

- Looking ahead, European flash PMI data will be observed ahead of NY dealing. Thursday’s NY session will bring the release of weekly jobless claims data, flash U.S. PMI readings and the Kansas City Fed manufacturing print. We will also get day 2 of Fed Chair Powell’s testimony on the Hill and 5-Year TIPS supply.

JGBS: Post-Auction Long End Bid Results In Flattening

Lower crude prices and Wednesday’s rally in core global FI markets provided a bid for JGBs during early Tokyo hours.

- The latest round of 20-Year JGB supply saw the low price print a little below wider expectations, while the cover ratio softened to sit roughly in line with the 6-auction average, as the price tail widened. Note that factors centred on the well-documented impaired JGB market functioning made a strong auction very unlikely, although short cover and potential lifer demand likely provided at least some offset to these headwinds. This meant that the auction avoided the worst case scenario and allowed the long end to lead the rally during the afternoon, after it lagged the futures driven bid in the belly during the Tokyo morning, likely on pre-auction worry.

- This leaves futures 39 ticks above yesterday’s settlement levels ahead of the Tokyo bell, a touch shy of best levels after the contract moved through its overnight session peak. Cash JGB trade sees the major benchmarks running 1-5bp richer across the curve, bull flattening.

- The latest round of weekly Japanese international security flow data revealed the largest ever round of net sales of Japanese bonds by foreign investors (based on records going back to 2001) as the market tested the BoJ’s resolve when it comes to the upper boundary of its permitted 10-Year JGB yield trading band. Foreign investors shed a net Y4.8tn of Japanese paper during the week.

- Local headline flow was dominated by comments from ex-FX policy chief Nakao, as he suggested that intervention to stem the recent run of JPY weakness cannot be ruled out.

- Looking ahead, national CPI data and the latest address from BoJ Deputy Governor Amamiya headline local matters on Friday.

AUSSIE BONDS: Holding Off Best Levels

Aussie bonds and the IR strip continue to hold a little below best levels amidst relatively light macro headline flow, with lingering weakness in crude providing some support to core FI markets.

- The ACGB cash curve has bull flattened, seeing yields run 12-16bp lower at typing. YM and XM are +12.5 and +15.0 respectively, while bills run +5 to +14bp through the reds.

- Note that a previously-flagged revision in Westpac chief economist Bill Evans’ RBA view helped the space back from best levels. Evans now looks for back-to-back 50bp hikes over the next couple of RBA meetings, adjusting his terminal rate view to 2.60% (from 2.35%) accordingly. Evans expect that level to be reached in February, with his view still less aggressive than that held by market participants.

- STIR markets have seen little movement re: expectations for tightening in July, with the IB strip pricing in ~45bp of tightening for that meeting, with a cumulative ~250bp of tightening priced in for the remaining six meetings of calendar ’22 (comparing to the ~275bp priced early on Wednesday.

- The release of the weekly AOFM issuance slate headlines domestic matters on Friday, which means that wider macro matters should remain at the fore.

JAPAN: Foreign Investors Lodged Record Net Sales Of Japanese Bonds Last Week

The latest round of weekly Japanese international security flow data revealed the largest ever round of net sales of Japanese bonds by foreign investors (based on records going back to 2001) as the market tested the BoJ’s resolve when it comes to the upper boundary of its permitted 10-Year JGB yield trading band. Foreign investors shed a net Y4.8tn of Japanese paper during the week. Foreign investors were also net sellers of Japanese equities, running up the largest round of weekly net selling observed since March. Elsewhere, Japanese investors registered a fourth consecutive week of net sales of foreign bonds and marginal net purchases of foreign equities.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

|---|---|---|---|

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | -496.7 | -862.7 | -3327.8 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | 9.7 | -137.1 | 341.1 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | -4804.6 | -1103.0 | -5876.2 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | -942.5 | 205.2 | -872.6 |

Source: MNI - Market News/Bloomberg/Japanese Ministry Of Finance

FOREX: Yen Outperforms On Continued Risk Aversion & Intervention Chatter

Demand for safe-haven assets coupled with renewed talk of potential FX intervention rendered JPY the best G10 performed for the second consecutive day, allowing USD/JPY to move further away from its recent 24-year highs.

- The region played catch up with comments from Fed Chair Powell, who told lawmakers Wednesday that engineering a soft landing for the economy would be "very challenging," adding that a recession is "certainly a possibility."

- Risk backdrop remained questionable in Asia, with U.S. e-mini futures staying in the red for the better part of the session (their brief recovery attempt failed) and crude oil trading on a heavier footing. This dynamic continued to support safer currencies, such as JPY, CHF and USD.

- Japan's former currency policy chief Nakao raised the prospect of an FX intervention, which prompted the yen to turn bid afresh. Bear in mind that Nakao's comments came with some caveats, as he called coordinated interventions "very difficult" and said he was not discussing these matters with current officials.

- The overnight drop in U.S. Tsy yields likely facilitated another downswing in USD/JPY, as relative yield dynamics remain a key focal point for the pair. Meanwhile, options traders added bearish USD/JPY bets, with 1-month risk reversal slipping to a fresh weekly low.

- Commodity-tied FX came under pressure, with the Aussie dollar pacing losses. AUD/USD fell below the $0.6900 mark but bears struggled to force a breach of yesterday's worst levels. Selling pressure materialised as BBG Commodity Index plunged to its lowest point since Mar 29.

- Today's data highlights include a suite of PMI readings from across the world as well as U.S. jobless claims. Fed Chair Powell will testify on the Hill, while ECB's Nagel & Villeroy are set to deliver speeches. Norges Bank will announce its rate decision.

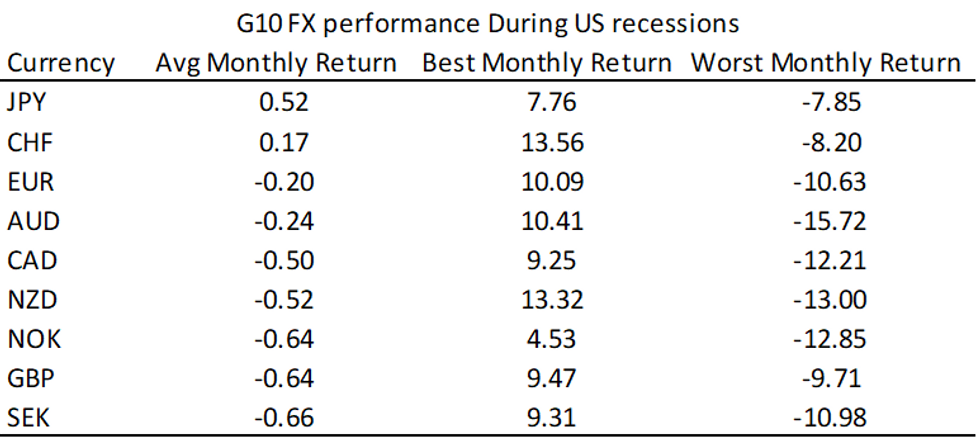

FOREX: JPY Historically The Best Performer In US Recessions

US recession fears continue to rise. Fed Chair Powell recognized the threat of such an eventuality in remarks to the US Senate on Wednesday, while former NY Fed Governor Bill Dudley stated that a US recession is inevitable in the next 12-18 months. A number of sell-side analysts are also stating a recession is a strong risk for 2023. As we outline below, from a G10 FX standpoint, JPY is the best performer, historically, during US recessions.

- The table below presents average G10 FX performance during US recessions. Note we use NBER dates for recession months and our sample goes back to the start of the 1990s.

- The first column represents average monthly returns by currency against the USD. We also present the best monthly performance during US recessions and also worst performing month, again by currency.

- JPY has the highest average monthly returns of just over +0.5%. This is followed by the other traditional safe haven CHF, at just under +0.2%.

- The rest of the G10 FX complex falls, with EUR outperforming the likes of GBP, NOK and SEK. Commodity FX also fall, but on average see outperformance again some of the EU currencies.

- For most currencies we tend to see larger falls than rises during recession periods, which is to be expected. The best monthly returns tend to come towards the end of the recession dates.

Table 1: G10 FX Performance During US Recessions (1990-2020)

Source: NBER/MNI - Market News/Bloomberg

Source: NBER/MNI - Market News/Bloomberg

- The clear caveat in the current cycle for JPY is a less favorable external trade balance position. However, the trade position also deteriorated sharply through the 2008 recession, as oil prices spiked, but this didn't prevent JPY rallying sharply during this period.

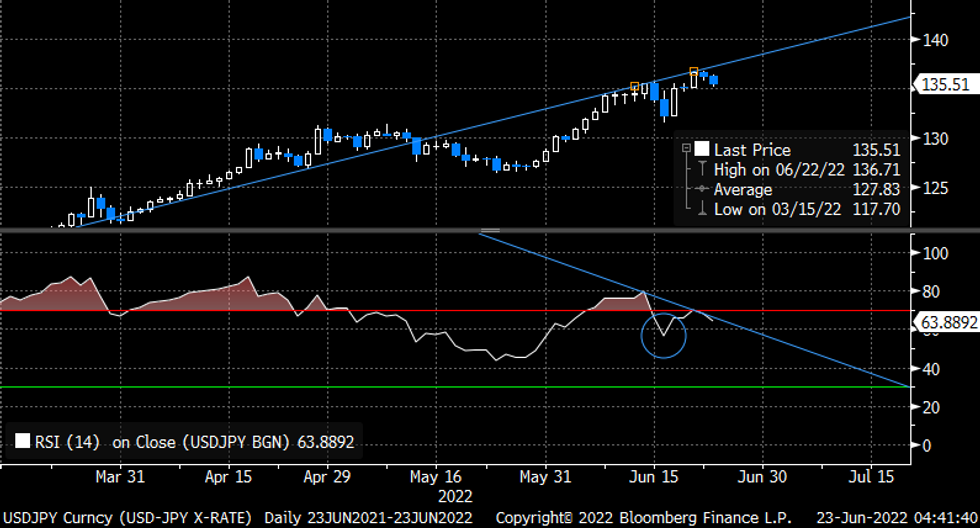

JPY: JPY Extends Gains On Remarks From Ex-FX Off'l, RSI Comes Under Scrutiny

The yen has extended gains as BBG ran comments from Japanese FinMin FX czar Nakao, who dubbed currency intervention a "possibility."

- Nakao's comments came with a caveat that "coordinated intervention is generally very difficult unless there's a very excessive movement in the market, or a kind of crisis mode."

- The latest leg lower has allowed USD/JPY to sink past yesterday's low to a fresh session trough at Y135.13. It has now clawed back some of these losses and trades at Y135.52, 74 pips lower on the day.

- As USD/JPY pulls back from recent 24-year highs, one can spot a bearish divergence unfolding on the daily chart of price action plotted alongside the RSI. This occurs when price keeps making higher highs, but its RSI fails to follow suit and prints a lower high.

- Watch this space, as the RSI may soon generate a more powerful bearish signal. On the previous swing higher, the indicator moved into overbought territory, but failed to repeat that on a second attempt. If it now dips past the recent fail point (56.2 or blue circle in the chart), a failure swing top will be confirmed.

- Options trades appear to be getting more bullish on the yen as well, with USD/JPY 1-month risk reversal extending this week's losses today.

- Still, it is worth paying close attention to fundamentals. Relative yield dynamics, largely driven by monetary policy matters, have been a key driver of JPY price action in the recent weeks.

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

FX OPTIONS: Expiries for Jun23 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0455-65(E2.1bln), $1.0500(E1.8bln), $1.0595-00(E1.1bln)

- USD/JPY: Y132.00($1.2bln), Y132.80-00($1.0bln), Y134.00($641mln), Y135.00($999mln)

- GBP/USD: $1.2280-00(Gbp530mln), $1.2380-00(Gbp1.1bln), $1.2495-15(Gbp570mln)

- EUR/GBP: Gbp0.8515(E1.2bln), Gbp0.8575-90(E531mln), Gbp0.8620(E531mln)

- EUR/JPY: Y143.00(E541mln)

- USD/CAD: C$1.2800($1.4bln), C$1.2915($1.2bln)

- USD/CNY: Cny6.60($1.5bln), Cny6.70($1.6bln), Cny6.75($840mln), Cny6.80($1.4bln)

MNI Norges Bank Preview - June 2022: To Stick to Gradual Approach

EXECUTIVE SUMMARY

- Tighter policy has been well signposted for the June meeting

- Board may opt for faster, not larger, rate hikes

- Path projections likely to show policy above neutral by year-end

Tighter policy has been well signposted for the June meeting, with the bank signalling a rate hike is “most likely” to be delivered. The size of the hike is less forecastable. Markets have fully priced a 25bps rate rise to 1.00% - and partially a 50bps rise – leaving markets at risk of a ‘dovish’ disappointment from a mere 25bps hike. While inflationary pressures, rates among trade partners and firm oil prices argue in favour of a more sizeable 50bps hike this month, the board are likely to stick to their predictable, steady, “gradual” 25bps due to a unique transmission mechanism and a firm preference for credibility-driven policy.

To counter any ‘dovish’ messages of a 25bps hike this week, the board will likely steepen their path projections further this quarter, introducing – for the first time this cycle – the likelihood of rate hikes at inter-policy report meetings. The bank could reinforce this message by stating that the next rate hike “will likely” follow in August.

ASIA FX: USD/Asia Pairs Mixed, Awaiting Central Bank Decisions

USD/Asia pairs have been mixed, PHP and IDR are relatively steady ahead of central bank decisions later today. CNH remains resilient, while KRW has weakened past 1300.

- CNH: USD/CNH has been range bound today. Dips sub 6.7100 have been supported, but we haven't pushed above 6.7200. The CNY fixing was close to neutral, while China/HK equities continue to outperform. Fresh stimulus hopes, as President Xi has pushed for China to meet its 2022 economic goals, is helping sentiment.

- KRW: USD/KRW spot pushed above 1300 fresh highs going back to 2009. The Finance Ministry stated that will stabilize FX markets if needed, but this didn't impact won sentiment a great deal. The Kospi is weaker, while offshore investors have sold a further $180mn of local equities. The 1 month NDF is back above 1300, but below overnight highs of 1304.5.

- INR: Spot USD/INR is lower in early trade, back to a 78.25 handle, after closing yesterday near 78.40. A further dip in oil prices is helping, while onshore equities are +1% higher at this stage. The 1 month NDF is around 78.45, after trading above 78.55 yesterday.

- IDR: USD/IDR is down slightly in spot terms to just below 14838, while the 1 month NDF is slightly higher at 14853. The market awaits the BI decision, although no change is expected at this stage.

- PHP: An early USD/PHP dip has largely reversed, with the pair back up to 54.48 from sub 54.40. We retain our call for a 25bps hike at today's BSP meeting. The peso has not received much benefit from lower oil prices, perhaps that will come post BSP.

- THB: USD/THB is down slightly from recent highs, we touched 35.325, but sit back at 35.43 now. A former finance minister stated the BoT outlook needs to turn more hawkish to aid the baht. Fitch affirmed Thailand's sovereign credit rating at BBB+ with a stable outlook, citing the nation's "sustained external finance strengths and strong macroeconomic policy framework."

EQUITIES: Mixed Bag As Hong Kong and Chinese Equities Outperform; Commodities Continue Decline

Major Asia-Pac equity indices are virtually unchanged to higher at writing, bucking a mildly negative lead from Wall St.

- The Japanese Nikkei 225 has shed early gains to sit a little below neutral levels at typing, with materials and energy-related equities underperforming amidst a continued decline in major commodity benchmarks (BCOM: -1.3%). Financials posted a largely flat performance, while major exporters are mostly lower amidst the latest round of gains in the yen.

- The Hang Seng Index outperformed regional peers, dealing 1.0% firmer to revisit session highs after rebounding from neutral levels mid-way through the morning session. China-based tech leads the bid after BBG source reports late in Wednesday’s Asian session pointed to Ant Group applying for a license with the PBoC to become a financial holding company, with sentiment in the likes of Alibaba Group (+4.7%), Tencent Holdings (+1.8%), and Baidu Inc (+1.4%) benefitting from the development.

- The CSI300 sits 0.5% better off at typing, outpacing most regional peers as remarks delivered by Chinese President Xi Jinping to the BRICS summit re: meeting China’s economic goals for ‘22 have again raised hopes for policy stimulus, given the country’s well-documented growth difficulties in the face of the standing COVID-zero policy.

- The ASX200 deals 0.2% higher at writing on strength in tech-related names, with the S&P/ASX All Technology Index sitting 0.8% better off, led by gains in favoured names such as Block Inc (+3.9%) and Xero Ltd (+2.0%). Major mining stocks were generally worse off, with the ASX300 Metals and Mining Index shedding 2.8% on aforementioned weakness in commodity benchmarks.

- U.S. e-minis sit 0.2% worse off apiece at typing, off worst levels, but struggling to rise above neutral levels throughout Asia-Pac dealing with previously-flagged worry re: a Fed-led recession evident.

GOLD: Lower In Asia; Little Changed In June

Gold sits ~$4/oz weaker to print $1,833/oz, operating around session lows, and extending a pullback from Wednesday’s best levels at writing.

- To recap, the precious metal reversed earlier losses to close ~$5/oz higher on Wednesday, with a downtick in U.S. real yields and the USD (DXY) providing limited support to the space.

- Bullion ultimately sits little changed in June, keeping within a relatively narrow ~$45/oz trading band with debate re: the possibility of a Fed-led recession increasingly taking focus.

- To elaborate, the latest round of Fedspeak on Wednesday saw Fed Chair Powell acknowledge that a soft landing for the U.S. economy would be “very challenging”, while declining to rule out a potential 100bp rate hike in July. Elsewhere, Chicago Fed Pres Evans (due to retire in early ‘23) said that rates would need to rise “a good deal more” in the Fed’s inflation fight, highlighting their potential negative impact on labour markets, while flagging data-dependence for rate hikes further out.

- Looking ahead, Powell is due to speak before the House Financial Services Panel later on Thursday (1500 BST).

- July FOMC dated OIS now price in ~82bp of tightening for that meeting after above-mentioned comments from Powell re: a 100bp hike, suggesting a ~30% chance of a 100bp move in July, up from ~70-75bp seen over the rest of the week prior.

- From a technical perspective, previously outlined support and resistance levels remain intact at $1,787.0/oz (May 16 low) and $1,889.1/oz (trendline resistance from Mar 8 high) respectively.

OIL: Lower In Asia On Growth Worry; WTI Eyes $100

WTI and Brent are $3.00 worse off apiece, operating a short distance above their respective multi-week lows made on Wednesday. Both benchmarks appear on track for a second straight day of losses, with debate re: recessionary risks continuing to do the rounds.

- Crude seemingly came under pressure in Asia from spillover owing to the release of the latest round of U.S. API inventory data late on Wednesday, with reports pointing to a relatively large, surprise build in crude inventories (reported to be largest since mid-Feb ‘22), and a surprise increase in gasoline stockpiles as well. On the other hand, a drawdown was seen in distillate and Cushing hub stocks.

- Elsewhere, worry re: a Fed-led recession continues to see crude operate around its lowest levels for the month, with remarks from Fed Chair Powell that a soft landing for the U.S. economy would be “very challenging” taking focus.

- Turning to the U.S., the gasoline tax holiday proposed by U.S. President Biden continues to draw discussion (keeping in mind that recent news re: the proposed measure has coincided with recent weakness in crude), with some pointing out that the corresponding support for gasoline demand would likely exacerbate tightness in gasoline and crude supplies.

- Looking to OPEC, supply worry remains elevated, with the International Energy Agency (IEA) earlier this week pointing out that Nigeria (largest producer in Africa) and Angola (third largest) are unlikely to meet their OPEC output quotas in ‘22. S&P Global estimates have put Nigerian crude production in May at >30 year lows, while Angolan output has fallen from 1.8mn bpd in 2017, to ~1.2mn bpd.

- Up next, an expected release of U.S. crude inventory data later by the EIA will be delayed until at least next week, owing to “systems” issues faced by the agency. Elsewhere, Energy Secretary Granholm is due to meet U.S. oil executives later on Thursday.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/06/2022 | 0600/0700 | *** |  | UK | Public Sector Finances |

| 23/06/2022 | 0600/0800 | ** |  | SE | PPI |

| 23/06/2022 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 23/06/2022 | 0715/0915 | | FR | Flash Manufacturing, Services PMI | |

| 23/06/2022 | 0715/0915 | ** | | FR | IHS Markit Services PMI (p) |

| 23/06/2022 | 0715/0915 | ** | | FR | IHS Markit Manufacturing PMI (p) |

| 23/06/2022 | 0730/0930 | ** |  | DE | IHS Markit Services PMI (p) |

| 23/06/2022 | 0730/0930 | ** | | DE | IHS Markit Manufacturing PMI (p) |

| 23/06/2022 | 0800/1000 | *** |  | NO | Norges Bank Rate Decision |

| 23/06/2022 | 0800/1000 |  | EU | ECB Economic Bulletin | |

| 23/06/2022 | 0800/1000 | | EU | Flash Manufacturing, Services PMI | |

| 23/06/2022 | 0800/1000 | ** | | EU | IHS Markit Services PMI (p) |

| 23/06/2022 | 0800/1000 | ** | | EU | IHS Markit Manufacturing PMI (p) |

| 23/06/2022 | 0800/1000 | ** | | EU | IHS Markit Composite PMI (p) |

| 23/06/2022 | 0830/0930 | *** | | UK | IHS Markit Manufacturing PMI (flash) |

| 23/06/2022 | 0830/0930 | *** | | UK | IHS Markit Services PMI (flash) |

| 23/06/2022 | 0830/0930 | *** | | UK | IHS Markit Composite PMI (flash) |

| 23/06/2022 | 1000/1100 | ** | | UK | CBI Distributive Trades |

| 23/06/2022 | 1100/0700 | * |  | TR | Turkey Benchmark Rate |

| 23/06/2022 | - | | EU | ECB Lagarde at European Council Meeting | |

| 23/06/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 23/06/2022 | 1230/0830 | * | | US | Current Account Balance |

| 23/06/2022 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 23/06/2022 | 1345/0945 | *** | | US | IHS Markit Services Index (flash) |

| 23/06/2022 | 1400/1000 | | US | Fed Chair Jerome Powell | |

| 23/06/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 23/06/2022 | 1500/1100 | ** | | US | DOE weekly crude oil stocks |

| 23/06/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 23/06/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 23/06/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 5 Year Note |

| 23/06/2022 | 1800/1400 | *** |  | MX | Mexico Interest Rate |

Why Subscribe to

MarketNews.com

MNI is the leading provider

of news and intelligence specifically for the Global Foreign Exchange and Fixed Income Markets, providing timely, relevant, and critical insight for market professionals and those who want to make informed investment decisions. We offer not simply news, but news analysis, linking breaking news to the effects on capital markets. Our exclusive information and intelligence moves markets.Our credibility

for delivering mission-critical information has been built over three decades. The quality and experience of MNI's team of analysts and reporters across America, Asia and Europe truly sets us apart. Our Markets team includes former fixed-income specialists, currency traders, economists and strategists, who are able to combine expertise on macro economics, financial markets, and political risk to give a comprehensive and holistic insight on global markets.