Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- TYU2 operates comfortably off of worst levels of the Asia session on a combination of post-RBA ACGB spill over, e-minis moving back from highs, Chinese equities pushing lower on the day, crude operating back from best levels and no real progress observed in the latest phone call between senior U.S. & Chinese policymakers (after a knee jerk risk-on move was seen on the back of confirmation that the phone call between Yellen & Liu He took place). This comes after early catch up to Mondays core EGB & Gilt cheapening and an early uptick in e-minis.

- Much firmer than expected Caixin services PMI data out of China (in line with what was seen in the official PMI release) and some tweaks to the RBA's statement also provided some points of note.

- Final services PMI data from across the globe and an address from BoE's Tenreyro headline the wider docket on Tuesday.

US TSYS: Bear Flattening But Off Cheaps

TYU2 operates comfortably off of worst levels of the Asia session on a combination of post-RBA ACGB spill over, e-minis moving back from highs, Chinese equities pushing lower on the day, crude operating back from best levels and no real progress observed in the latest phone call between senior U.S. & Chinese policymakers (after a knee jerk risk-on move was seen on the back of confirmation that the phone call between Yellen & Liu He took place). That leaves the contract -0-11 at 118-29+, 0-06+ off the base of its 0-16+ overnight range on volume of ~115K during Asia hours. Meanwhile, cash Tsys run 7-11bp cheaper across the curve, bear flattening, with some catch up to Monday’s cheapening in the core EGB & Gilt space observed as cash markets re-opened after the Independence Day holiday.

- Overnight flow was headlined by a 7.5K block sale of the TYQ2 119.50/118.00 put spread, which saw a slightly overweighted delta hedge via TY futures (-2K).

- Tuesday’s domestic docket will be headlined by factory orders and final durable goods data.

JGBS: 10-Year Supply Goes Well, Swap Flows Aid Curve Steepening

JGB futures have stuck to a much tighter range than their global peers, operating -8 ahead of the Tokyo close, largely in line with late overnight session levels.

- 10s outperformed on the curve all day, even ahead of today’s 10-Year JGB auction, representing the only point on the cash JGB curve that is firmer (to the tune of ~1bp), while the remaining benchmarks run little changed to 3.5bp cheaper, with the super-long end leading the weakness, once again aided by payside swap flow as 20+-Year swap spreads widen.

- In terms of auction specifics, 10-Year supply went well, with the low price matching wider expectations (as proxied by the BBG dealer poll), as the tail held narrow and the cover ratio moved further above the 6-auction average. As we flagged in our preview, the BoJ’s defence of its YCC parameters and the short base of the international investor sphere likely provided 2 major sources of demand.

- Slightly softer than expected domestic wage data failed to impact the space.

- In domestic news, former BoJ chief economist Seisaku Kameda suggested that inflationary impulses will be stronger and longer lasting than the BoJ currently envisages, which will likely result in a markup of its inflation expectations when it convenes later this month.

- BoJ Rinban operations headline domestic matters tomorrow.

AUSSIE BONDS: Further Support As RBA Removes Reference To Low Level Of Rates

Aussie bonds have extended their move away from session lows in the wake of the latest RBA decision after the Bank delivered the expected 50bp rate hike, reaffirmed its previous guidance re: further normalisation in the months ahead, but removed the reference to interest rates being at low levels, while explicitly noting that higher interest rates are impacting household spending. The Bank still feels that the strong domestic economy will provide it with a base to tighten further, but there was a slightly more cautious feel to the post meeting statement given the above tweaks. Well-defined global risks were once again highlighted in the statement. We would suggest that a combination of the U.S. Federal Reserve decision i.e. the magnitude of the hike deployed by the Fed & the domestic Q2 CPI print will figure heavily in the Bank’s August deliberations (when it is set to debate implementing a 25 or 50bp hike).

- Note that the space was already moving away from its early Sydney troughs, tracking the beat of the wider core global FI space. The initial move away from lows came with e-minis moving back from highs, Chinese equities pushing lower on the day, crude back from best levels and no real progress observed in the latest phone call between senior U.S. & Chinese policymakers (after a knee jerk risk-on move was seen on the back of confirmation that the phone call between Yellen & Liu He took place).

- That leaves YM -3.5 and XM -1.5 at typing, at little shy of their respective post-RBA peaks, while the longer end of the cash curve is ~1.5bp cheaper on the day, with a fairly parallel shift observed in the 7+-Year zone. Bills run flat to -4 through the reds, bear flattening.

- Tomorrow’s domestic docket is headlined by A$800mn of ACGB Apr-33 supply.

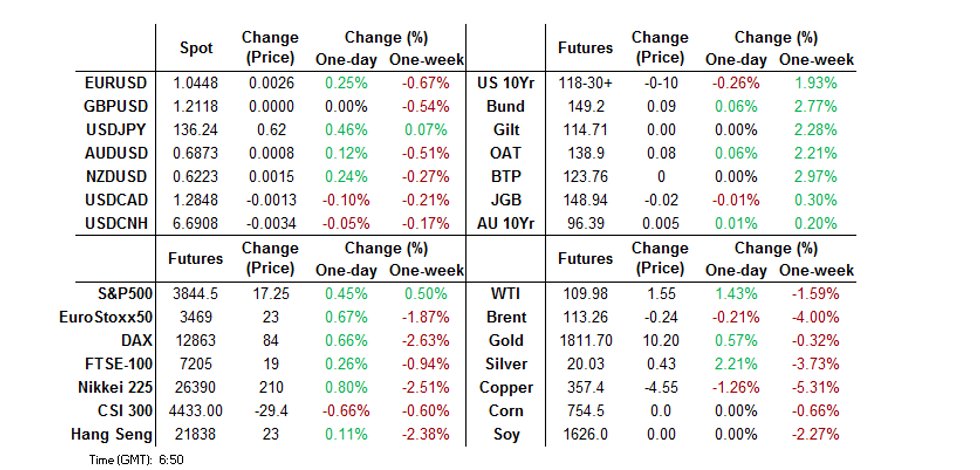

FOREX: JPY Weakens As Yields Rebound, A$ Lower Post RBA

The USD DXY index is holding comfortably above 105, largely thanks to higher USD/JPY levels as yields rebound. AUD/USD has fallen post the RBA statement, while most other currencies are slightly firmer against the USD.

- USD/JPY has been supported by a rebound in US Cash Tsy yields, as these markets re-opened, with the 2yr back up to 2.94%, nearly +11bps on the day. This follows a strong bounce overnight in EU markets. USD/JPY reached close to 136.40, but is back to 136.25, +0.45% for the session.

- The RBA raised the cash rate by 50bps to 1.35%, as widely expected. AUD/USD dipped post the RBA announcement as the central bank sounded more cautious on the outlook and removed a reference to rates being low in the accompanying statement. We dipped to the low 0.6850 region before sentiment stabilized. Earlier highs were at 0.6895.

- Elsewhere, much of the focus has been US-China talks and the potential for tariff relief, although nothing concrete has emerged yet. China equities couldn't rise though, despite this news and a strong upside beat on the China Caixin services PMI (54.5 versus 49.6 expected). USD/CNH has remained range bound, last at 6.6925.

- US equity futures are tracking higher, although are well down on earlier session highs. This has helped JPY underperform at the margin, particularly on a cross basis.

- Other pairs are sticking to recent ranges. EUR/USD is holding above 1.0430, while NZD/USD is around 0.6210, largely ignoring a poor Q2 NZIER business survey.

FX OPTIONS: Expiries for Jul05 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0450-70(E981mln), $1.0500-05(E596mln), $1.0600(E508mln)

- USD/JPY: Y137.00($1.7bln), Y139.00($2.2bln)

- EUR/GBP: Gbp0.8670-85(E1.5bln), Gbp0.8850(E1.1bln)

- EUR/JPY: Y144.00(E1.6bln), Y146.00(E1.6bln)

- USD/CAD: C$1.2900($675mln)

ASIA FX: Inflation Continues To Surprise On The Upside

USD/CNH has remained within recent ranges despite talk of lower tariffs and another solid data beat. Still, CNH is outperforming its Asian peers and the likes of JPY. Higher US yields and yen weakness weighed on regional FX sentiment elsewhere. On the data front, South Korea, Philippines and Thailand inflation prints were all stronger than expected.

- CNH: USD/CNH dipped towards 6.6800 following reports of a video call between China's Vice Premier Liu and US Treasury Secretary Yellen. We didn't see much follow through though, the US Treasury account of the meeting didn't mention tariffs either. China equities are down on the day as well, despite a nice Caixin services PMI beat (54.5 versus 49.6). Rising domestic covid cases is likely weighing at the margin. USD/CNH has spent much of the afternoon session just above 6.6900.

- KRW: USD/KRW tried to break lower sub 1295 on a couple of occasions but failed. We are now back close to 1300, around +0.25% above yesterday's closing levels. Won weakness has ignored the outperformance of local equities, up 1.6% for the Kospi. The June inflation data was +6% YoY, which was above market expectations, and could trigger a 50bps hike at the next BoK meeting.

- INR: USD/INR is drifting higher in early trade, back above 79.05, versus yesterday's close of 78.95. Higher oil is weighing, although onshore equities are up close to 1%. Earlier, the services PMI printed at 59.2 for June, versus 58.9 previously.

- PHP: USD/PHP tried to drift lower in early trade but is now back to 55.10, slightly above yesterday's closing levels. Inflation printed stronger than expected for June, 6.1% versus 6.0% expected. BSP Governor Medalla said we could see a 50bps hike in August if MoM inflation is strong enough. The policy rate may also be at 3.5% by year's end (from the current 2.5%).

- SGD: The SGD NEER has recovered some ground, as per the Goldman Sachs estimate. USD/SGD is slightly lower, tracking back sub 1.3960. Retail sales were strong for May, printing at 17.8% YoY, versus 13.4% expected.

- THB: Thailand inflation printed stronger than expected. YoY headline to 7.66% from 7.10% previously, and 7.45% expected. Core inflation pushed up, but from a low base to 2.50%. The next policy meeting is August 10th, with pressure growing for BoT to act. USD/THB remains close to recent highs but is finding some selling interest above 35.70 (last was 35.685).

EQUITIES: Mostly Higher In Asia; Initial Lift From U.S.-China Tariff Optimism Wanes

Major Asia-Pac equity indices are mostly higher at typing, tracking a positive lead from Wall St. Asian equity indices are nonetheless mostly off of their best levels for the session, with major Chinese stock index benchmarks sitting below neutral levels after opening higher.

- The CSI300 sits 0.4% worse off at typing after reversing opening gains, whipping between +0.8% and -1.2% across the Asian session. Shallow gains observed in energy and materials equities were countered by weakness in consumer staples and consumer discretionary stocks, while travel-related equities underperformed, led lower by China Tourism Group Duty Free (-2.3%) amidst the ongoing COVID outbreak in the country’s east.

- The Hang Seng Index sits 0.6% firmer at typing, paring gains after opening higher. The early bid was initially driven by optimism surrounding the U.S. potentially lifting tariffs on Chinese goods in the wake of a WSJ source report and a Liu-Yellen video call, with the impetus fading later into the session. A better than expected Caixin services PMI print (54.5 vs 49.6 BBG median) did little to aid equities, with both the HSI and CSI300 trading lower since then.

- The ASX200 trades 0.6% higher at writing, hitting fresh session highs in the wake of the RBA decision to hike rates by 50bp. The late rally was aided by outperformance in tech names (S&P/ASX All Tech Index: +2.0%) and a recovery in the financials sub-index, which erased earlier losses of as low as 0.8% after the RBA decision.

- U.S. e-mini equity index futures deal 0.3% to 0.5% firmer at typing, paring an earlier bid that saw NASDAQ contracts trade as much as 1.0% firmer near the beginning of the Asian session.

GOLD: Little Changed In Asia; $1,800/oz Remains In Focus

Gold prints $1,811/oz at typing, sitting a little below best levels of the session. The precious metal operates within the upper end of Monday’s trading range at typing, with an uptick in nominal U.S. Tsy yields possibly putting a cap on the space.

- Gold was little changed on headlines pointing to a call between Chinese Vice Premier Liu He and U.S. Treasury Sec. Yellen earlier in the session, with reports highlighting that the pair had discussed U.S. tariffs on Chinese consumer goods (among a wide range of other matters). A note that the call comes after a previously-flagged WSJ source report on Monday said that a lifting of tariffs could come as soon as this week, pointing to the potential for an easing in U.S. inflation.

- Nominal U.S. Tsy yields have pushed higher on the news, and broadly sit around the upper end of their pre-Independence Day ranges at typing.

- From a technical perspective, gold sits between support at $1,784.6/oz (Jul 1 low), and resistance at ~$1,830.5/oz (20-Day EMA).

OIL: Back From Best Levels; $110 Test Eyed For WTI

WTI is ~+$1.80 (owing to having no settlement on Monday due to the U.S. Independence Day holiday) and Brent is virtually unchanged at typing, with the former backing away from one-week highs made earlier in the session, operating a shade above $110 at typing.

- Brent’s prompt spread has risen above $4 at typing, pointing to still-intensifying backwardation in oil markets amidst elevated worry re: tightness in global crude supplies.

- Previously-flagged strikes in Norway’s O&G sector will begin today. While earlier RTRS reports have estimated crude output to decline by ~130K bpd, the offshore managers' union Lederne expanded their demands on Monday, with closures at three more facilities scheduled for Jun 9 (estimated additional ~160K reduction in crude output).

- Elsewhere, Ecuador has announced that crude production is back above 90% of pre-shutdown levels, at ~462K bpd.

- Turning to China, while the eastern province of Anhui (current outbreak epicentre) reported fewer fresh COVID cases for Monday, daily case counts have continued to tick a little higher across the rest of the economically important Yangtze Delta region, particularly in Jiangsu province (bordering Shanghai).

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 05/07/2022 | 0645/0845 | * |  | FR | Industrial Production |

| 05/07/2022 | 0715/0915 | ** |  | ES | IHS Markit Services PMI (f) |

| 05/07/2022 | 0745/0945 | ** |  | IT | IHS Markit Services PMI (f) |

| 05/07/2022 | 0750/0950 | ** | | FR | IHS Markit Services PMI (f) |

| 05/07/2022 | 0755/0955 | ** |  | DE | IHS Markit Services PMI (f) |

| 05/07/2022 | 0800/1000 | ** |  | EU | IHS Markit Services PMI (f) |

| 05/07/2022 | 0830/0930 | ** |  | UK | IHS Markit/CIPS Services PMI (Final) |

| 05/07/2022 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 05/07/2022 | 0930/1030 | | UK | BOE Financial Stability Report | |

| 05/07/2022 | 1230/0830 | * |  | CA | Building Permits |

| 05/07/2022 | 1400/1000 | ** |  | US | Factory new orders |

| 05/07/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 05/07/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 05/07/2022 | 1630/1730 | | UK | BOE Tenreyro Panels Qatar Centre Conference |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.