Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Markets were generally restrained for most of the Asia-Pac session, before news that gas had started to flow through the Nord Stream 1 pipeline (at ~30% of capacity) supported the EUR. The currency will have to navigate the seeming impending resignation of Italian President Draghi and ECB monetary policy decision (with the 25/50bp rate hike debate and details surrounding the ECB’s anti-fragmentation tool providing the two key points of focus there)

- Presidents Xi & Biden are set to speak in the next 10 days, per Biden.

- Outside of the ECB decision and political developments, Thursday will see the release of the U.S. Philly Fed survey & weekly jobless claims data. We will also hear from BoE Chief Economist Pill. Also remember that comments/developments surrounding the Nord Stream pipeline present headline risk after the aforementioned resumption of flows.

MNI ECB Preview - July 2022: Tightening As Economic Headwinds Build

EXECUTIVE SUMMARY

- The ECB is likely to hike policy rates by 25bp in July as already telegraphed. While there does not appear to be enough momentum behind a larger move for now, it should not be discounted entirely. Indeed, it may prove easier to hike aggressively now, than attempt to do so later in the year should economic activity abruptly deteriorate.

- The ability of the ECB to provide additional guidance on the path for policy rates from September onwards has become more challenging.

- The ECB needs to credibly signal its commitment to rein in inflation at a time when it has fallen far behind its peers in tightening policy. However, pre-committing now to specific policy outcomes at future meetings when there is a growing risk of outright recession, would be a risky play from a credibility perspective.

- We expect the ECB to reiterate that it anticipates a gradual but sustained path for further increases in policy rates, alongside being data dependent, while not providing any further specific rate guidance for now.

- A sufficiently large (likely limitless) and flexible anti-fragmentation tool is expected to be announced at the July meeting. Delaying the announcement would be risky for spreads given the previous market disappointment at the unscheduled mid-June meeting for discussing fragmentation risks.

US TSYS: Tight Pre-ECB Trade

Tsys stuck to a narrow range in Asia-Pac dealing, initially nudging higher on a modest downtick in e-mini futures (aided by Microsoft becoming the latest tech giant to pullback on hiring plans).

- That was before the confirmation of the resumption of gas flows through the Nord Stream 1 pipeline running between Russia & Europe, which took place on time after the end of the line’s maintenance period. That news flow sees the space back from best levels, with e-minis back to neutral levels.

- Still, TYU2 operates in a very narrow 0-05+ range, printing +0-03+ at 117-28+ ahead of London hours, on light volume of ~50K as the proximity to the ECB decision keeps many sidelined. Cash Tsys run 0.5-1.0bp richer across the curve.

- Italian political matters (with PM Draghi’s official resignation seemingly due on Thursday) & the ECB monetary policy decision will shape early trade today (with the 25/50bp rate hike decision and details surrounding the ECB’s anti-fragmentation tool providing the two key points of focus for the latter). Meanwhile, Thursday’s NY docket is headlined by the latest Philly Fed survey, weekly jobless claims data & 10-Year TIPS supply.

- Also remember that comments/developments surrounding the Nord Stream pipeline present headline risk after the aforementioned resumption of flows.

JGBS: A Little Firmer, No Surprises From BoJ

JGBs futures extended on a modest morning uptick after the BoJ provided no surprises, leaving its monetary policy settings unchanged, alongside a mark higher in its inflation expectations, mark lower in immediate GDP forecast and changes to language that reflected those dynamics e.g. inflation expectations have risen. Note that the central mantra of the Bank’s monetary policy outlook remains unchanged, as it reiterated its forward guidance (including the dovish bias within), while it flagged the risks that commodity prices and swings in FX movements pose to inflation.

- Elsewhere, local press reports pointed to PM Kishida reshuffling his cabinet in September, which isn’t a new idea.

- JGB futures have nudged away from best levels ahead of the close, aided by the resumption of gas flows through the Nord stream 1 pipeline that runs between Russia & Europe. The contract is +!0 last, while cash JGBs run little changed to 2bp richer on the day, bull flattening.

- National CPI data and a liquidity enhancement auction for off-the-run 5- to 15.5-Year JGBs.

AUSSIE BONDS: Off Best Levels

Aussie bonds have pared an earlier bid heading into European hours, with a lack of domestic headline flow and a limited uptick in U.S. Tsys providing little directional impetus for ACGBs (keeping in mind that the ECB’s impending monetary policy decision may be keeping participants on the sidelines). Cash ACGBs run 0.5-1.5bp richer across the curve, with the belly underperforming at the margin. YM is +1.5, a little below best levels after testing its overnight lows while XM is +0.5, coming nowhere near to testing the boundaries of its overnight session range. Bills run 1-3 ticks richer through the reds.

- STIR markets continue to price in ~56bp of tightening for the RBA’s Aug meeting after speeches by RBA Gov Lowe and Reserve Gov Bullock on Tue and Wed, sitting little changed from levels observed at the beginning of the week.

- Friday will see the Australian composite and services flash PMIs for July headline the data docket, while A$700mn of ACGB Sep-26 will be on offer ahead of the release of the AOFM’s weekly issuance slate.

BOJ: Decision & Tweaks To Forecasts Meet Wider Expectations

At first glance there isn’t much to shock when it comes to the latest BoJ decision, with the usual 8-1 vote split (Kataoka being the usual dovish dissenter) as the Bank left its monetary policy settings unchanged. Its headline and core CPI forecasts were marked higher alongside a downgrade to the GDP projection covering the current FY (as expected). Note that the BoJ maintained its forward guidance surrounding interest rates, while tweaking its wording surrounding the overall economic assessment and inflationary picture in the wake of its forecast adjustments. The Bank did note that inflation expectations have risen, while it highlighted the risks that FX market gyrations and commodity price moves could have on inflation.

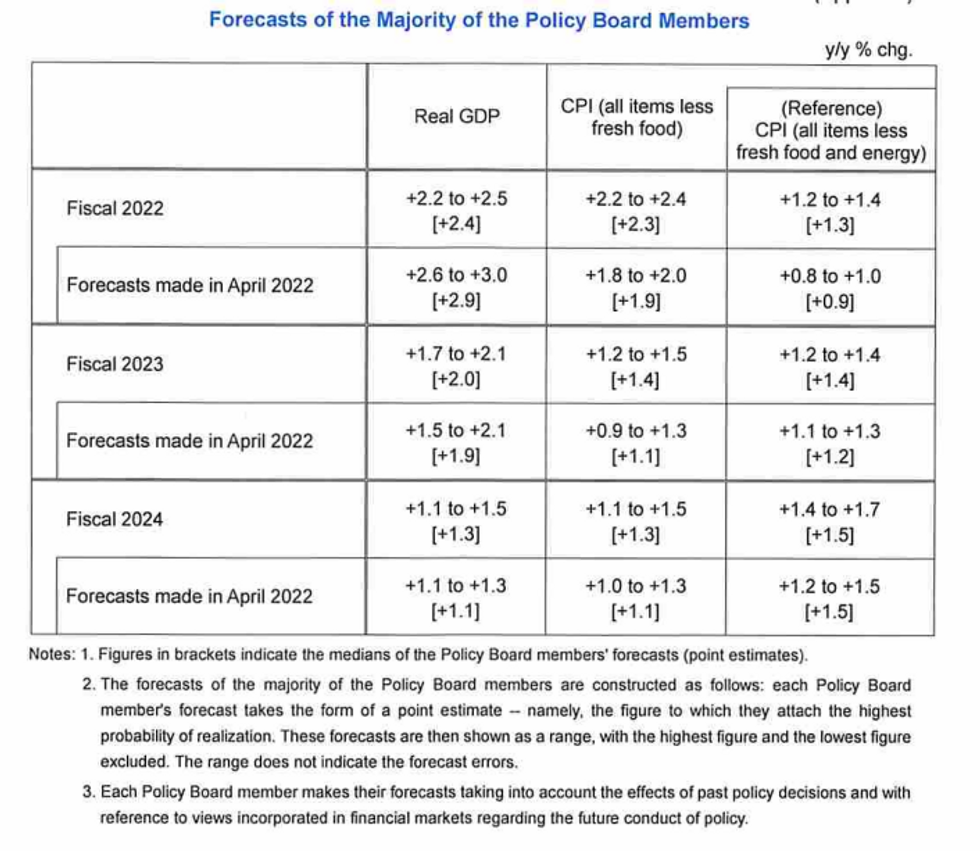

Fig. 1: Major Economic Forecasts From The BoJ’s Outlook for Economic Activity & Prices

Source: Bank of Japan

Source: Bank of Japan

- Note that regular references to recent JPY movements (coupled with the previously alluded to comments surrounding the risks that FX market moves could pose to inflation), including phrases such as “sharp fluctuations in FX markets have been observed” and the BoJ stressing that it needs to pay attention to the impact of FX movements on the economy seemed to create some mild volatility in JPY crosses. However, there wasn’t much in the way of new information in those phrases, which allowed USD/JPY to retrace to pre-decision levels after operating in a ~50 pip range around the decision.

FX OPTIONS: Expiries for Jul21 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0000(E1.2bln), $1.0200-10(E1.8bln)

- NZD/USD: $0.6300(N$500mln)

- USD/CAD: C$1.2900($885mln)

FOREX: European FX Space Back On Its Feet

G10 FX space saw some unwinding of yesterday's price action, with the European FX bloc finding poise. Headline flow was sparse and did not provide anything to diffuse concerns related to Italy's political turmoil and Europe's energy crisis.

- Shipment orders data published by Nord Stream AG showed that gas flows through the pipeline will resume at ~40% of capacity, slightly more than expected, with the planned maintenance due to finish at 06:00 CET. Still, actual volumes remain clouded by uncertainty until realised, while the risk of further weaponisation of gas shipments by Russia remains.

- Yen volatility briefly spiked (USD/JPY seesawed within a 50-pip range) as the BoJ kept its monetary policy settings and forward guidance unchanged, but tweaked economic forecasts to reflect stronger headwinds to growth and upside risks to inflation. The Bank flagged concern with sharp fluctuations in FX and commodity markets. As the dust settles, JPY is roughly where it was before the announcement.

- Traditional safe havens were out of favour despite questionable performance from regional stock markets. The greenback and yen were broadly softer, while the CHF lagged its European peers.

- The kiwi dollar landed at the bottom of the G10 pile, despite the lack of any obvious domestic catalysts. Correction of yesterday's outperformance may have played a role here.

- Central bank activity will remain in high gear, with the ECB preparing to announce its monetary policy decisions & BoE Chief Economist Pill due to speak. In the EM space, rate reviews are due in Indonesia, Turkey and South Africa.

- On the data front, focus turns to U.S. initial jobless claims & Philadelphia Fed Business Outlook.

ASIA FX: Weaker USD Only Benefits Some Asian Currencies

USD/Asia pairs have been mixed today. CNH, KRW and SGD all firmer, but MYR, THB, INR and IDR have struggled. Weaker USD sentiment against the majors has only benefited some currencies within the region.

- CNH: USD/CNH is back sub 6.7700, last trading just under 6.7650. Sentiment has been aided by a weaker USD, although CNH has lagged the likes of EUR, AUD etc. The USD/CNH fix was close to neutral, while onshore equities are trading modestly lower.

- KRW: 1 month USD/KRW has slipped back below 1310 this afternoon, after spending much of the session in a 1312/1315 range. Higher equities have helped, with the Kospi up +0.75% at this stage. Earlier the first 20 days of export data for July showed on-going export growth (14.5%), but a still large trade deficit.

- INR: USD/INR spot is back above 80.00, ignoring the weaker USD trend evident elsewhere. There is some talk of increased hedging behavior as the pair breaches the 80.00 figure level.

- IDR: Spot USD/IDR is above 15000, (last 15017). 22 out of 36 economists in a Bloomberg survey expect Bank Indonesia to keep the 7-Day Reverse Repo Rate unchanged but the rest have pencilled in a 25bp hike. We think the Bank is more likely to stand pat this time (see https://marketnews.com/mni-bi-preview-july-2022-on-the-cusp-of-hike ). That said, a pre-emptive rate rise cannot be ruled out and remains a hawkish risk.

- THB: Spot USD/THB has resumed gains, hitting fresh cyclical highs earlier today. We got close to 36.80, before easing back to 36.75 now. Political jitters may be adding pressure to the baht as Thai parliament resumes the no-confidence debate against PM Prayuth and 10 other ministers. Lawmakers will vote on the motion this Saturday.

- SGD: USD/SGD is lower, down to the low 1.3910 region. The pair has found a base ahead of 1.3900 in recent sessions. The NEER is still higher though, per Goldman Sachs estimates.

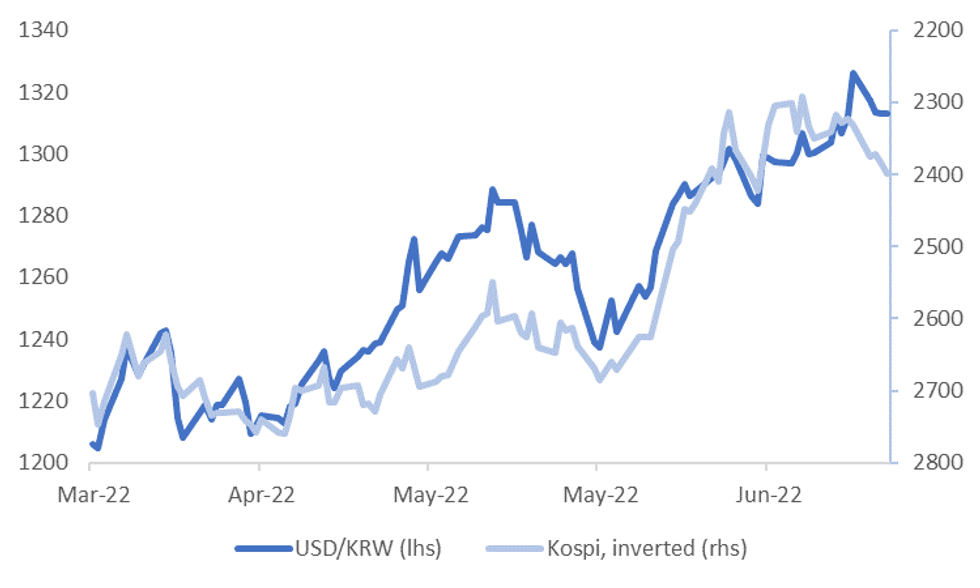

KRW: Won Still Lagging Firmer Equities, Correlations With CNH & JPY Remain High

USD/KRW has tracked recent ranges during today's session. We saw an earlier high of above 1316 in terms of onshore spot but have stayed within a 1313/1315 range for the most part.

- The won continues to lag the broader improvement in risk appetite, as reflected in the improvement in local equities, see the chart below.

- The rebound in local equities, which has continued today, suggests USD/KRW should be somewhere roughly closer to 1300.

- Part of this divergence likely reflects higher USD/CNH and USD/JPY levels. Won correlation with both currencies remains fairly high. USD/KRW and USD/CNH sits at over 90% for the past 6 months, while the equivalent correlation with USD/JPY is at similar levels.

- Hence, we may see this divergence between KRW and the Kospi persist in the near term, at least from a levels standpoint and potentially until we have a more definitive USD peak.

- Earlier, the first 20 days export data painted a fairly resilient picture for July, which should lower fears of a sharp slowdown in external growth, although not surprisingly export growth to China remains quite weak. The trade position also remains comfortably in deficit.

- From a longer-term technical standpoint, all major moving averages for USD/KRW continue to trend higher. The 50-day MA, which comes in at 1285, has been a strong support point since mid 2021. Breaks below this level have proven false and represented a buying opportunity in the pair.

Fig 1: USD/KRW & Kospi Performance

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

EQUITIES: Mostly Lower In Asia; Chinese Chip Makers Sidestep Carnage In Developers

Most major Asia-Pac equity indices are lower at typing, bucking a positive lead from Wall St., with the MSCI Asia Pac index on track to break a three-day streak of losses.

- The Nikkei sits 0.2% better off at writing, bucking the broader trend of losses and narrowly building on Wednesday’s 2.7% higher close. Financials and real estate equities pared losses in the wake of the BoJ’s monetary policy announcement, adding to earlier gains in industrials and major exporters.

- The Hang Seng brings up the rear amongst regional peers, dealing 1.4% weaker at typing. The financials (-2.1%) and property (-2.3%) sub-indices contributed the most to drag in the index, coming under pressure from the latest round of worry surrounding Chinese real estate, with suppliers and homeowners across hundreds of projects continuing to withhold payment of bills and mortgages.

- The CSI300 sits 0.5% weaker at typing, with shallow losses across most sectors dragging the index lower (although the CSI300 Real Estate index predictably leads losses at -2.7%). Chinese tech stocks outperformed (particularly chipmakers), seeing the STAR50 index trade 2.0% higher, with participants eyeing an upcoming Biden-Xi call, and progress towards the lifting of U.S. tariffs.

- The ASX200 is virtually unchanged at typing, with gains in tech and healthcare equities neutralised by losses in commodity-related sectors. While the S&P/ASX All Tech Index deals 2.7% firmer at typing, a decline in major crude benchmarks and industrial metals has seen the likes of the major miners trade 1.7-3.3% lower, with the energy sub-index (-3.2%) leading losses.

- E-minis are off worst levels, sitting 0.1-0.3% weaker apiece at typing.

GOLD: Fresh Cycle Lows In Asia; ETF Outflows Add To Gloom

Gold deals ~$3/oz weaker, printing ~$1,693/oz at typing. The precious metal sits a little above 15-month lows ($1,690.2/oz) recorded earlier in the session, with a limited downtick in the USD (DXY) and nominal U.S. Tsy yields likely helping to put a floor on the move lower for now.

- To recap, gold closed ~$15/oz weaker on Wednesday amidst a rise in U.S. real yields and the DXY, with the latter snapping a three-session streak of lower daily closes.

- Known ETF holdings of gold compiled by BBG points to approx. four weeks of outflows so far, taking the measure to levels last witnessed in early-Mar ‘22, while gold holdings in SPDR’s GLD ETF has fallen to six-month lows.

- From a technical perspective, gold appears to be approaching a zone that has acted as support since Apr ‘20 (approx. $1,670/oz to $1,690/oz) after a breakout from its COVID-induced trough.

- Looking to technical levels, gold’s earlier move lower has breached initial support at $1,690.6/oz (Aug 9 ‘21 low), exposing further support at $1,680.5/oz (1.764 proj of the Mar8-29-Apr18 price swing). On the other hand, resistance is situated at $1,745.4/oz (Jul 13 high).

NATURAL GAS: Russia Resumes Nord Stream Gas Shipments, Physical Flow at ~21.4 GWh/h

Russian gas flows through the Nord Stream pipeline resumed on Thursday morning after the completion of a 10-day maintenance, the operator of the pipeline said. Nord Stream 1 physical flow between 06:00 - 07:00 is 21,388,236 kWh/h vs. nominations of 29,284,591 kWh/h, per the operator's website.

- A spokesperson for Nord Stream AG earlier told Bloomberg that restoring the volume of shipments to requested levels will take some time, but the fact that Moscow has turned the taps back will see many breathe a sigh of relief.

- As mentioned, orders/nominations are for about 29.3 GWh/h through the whole day but this does not need to match actual physical deliveries. The capacity of Nord Stream 1 pipeline is about 73 GWh/h, which means orders are for about 40% of capacity.

- The president of Germany's Federal Network Agency earlier tweeted that the pipeline was running at about 30% of capacity this morning, which was guaranteed for two hours and usually does not change within a day.

OIL: Lower In Asia As Growth Worry Edges Ahead

WTI and Brent are ~$0.70 worse off apiece, edging away from their respective session lows made after China reported fresh COVID case counts that have remained around two-month highs (826 for Wed vs. 935 for Tue), raising lockdown fears from some quarters.

- Looking into the details, although COVID hotspots are centred away from major cities, Shenzhen has enacted lockdowns in some neighbourhoods, while Shanghai continues to find cases outside of quarantine.

- Contributing to wider growth worry, the Asian Development Bank (ADB) cut ‘22 growth forecasts for “Developing Asia” (includes China and India) from 5.2% to 4.6%, citing Fed tightening, issues stemming from China’s pandemic control measures, and fallout from the ongoing war in Ukraine.

- To recap Wednesday’s price action, WTI and Brent rose from session lows after the release of EIA inventory data on Wed, with crude and distillate stockpiles posting surprise declines, while there was a build in Cushing hub stocks. Both benchmarks failed to make headway above neutral levels however, with debate re: demand destruction doing the rounds after a much larger-than-expected build in gasoline stocks was observed (also larger than Tuesday’s reports of API estimates), raising worry re: demand destruction despite a decline in pump prices.

- Elsewhere, the International Energy Agency (IEA) released their monthly Electricity Market Report on Wednesday, sharply lowering their forecast for electricity demand growth in ‘22 on “slower economic growth” and “higher energy prices”.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 21/07/2022 | 0600/0700 | *** |  | UK | Public Sector Finances |

| 21/07/2022 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 21/07/2022 | 0800/0900 | | UK | BOE Pill Intro at BOE & ECB Conference | |

| 21/07/2022 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 21/07/2022 | 1215/1415 | *** |  | EU | ECB Deposit Rate |

| 21/07/2022 | 1215/1415 | *** | | EU | ECB Main Refi Rate |

| 21/07/2022 | 1215/1415 | *** | | EU | ECB Marginal Lending Rate |

| 21/07/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 21/07/2022 | 1230/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 21/07/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 21/07/2022 | 1245/1445 | | EU | ECB Press Conference | |

| 21/07/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 21/07/2022 | 1515/1715 | | EU | ECB Lagarde Presents Policy Decision via Podcast | |

| 21/07/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 21/07/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 21/07/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 10 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.