Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

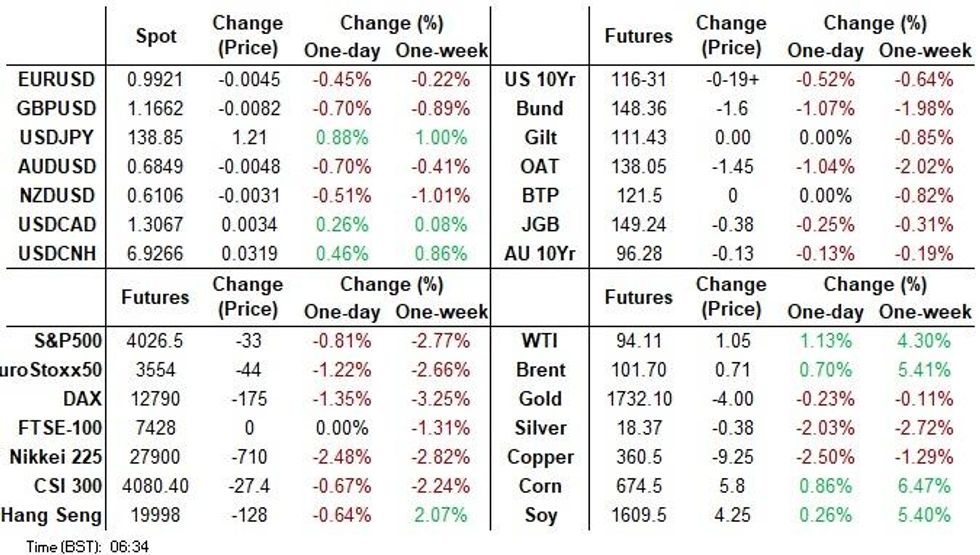

- Broad based USD strength prevailed post Jackson Hole. The USD DXY index firmed above 109.40, fresh highs back to 2002. USD/JPY gained 0.85%, and is pushing up towards 139.00. The A$ was not too far behind, down -0.75%, despite a strong retail sales beat. EUR/USD fell as well but remains above 0.9900 for now.

- Moves were aided by higher US yields, with the 2y touching 3.48%. The message from Jackson Hole around US rates going higher and staying elevated for longer being a major driver of sentiment today. Asia Pac equities were weaker across the board, while US futures fell further. Eminis are not too far away from the 50-day MA at 4005, versus 4022.50 last. Commodities were mostly softer, except for oil.

- Today's economic calendar is relatively light, with a speech from ECB Chief Economist Lane due, followed by the release of Dallas Fed m’fing activity data and Fedspeak from Fed Vice Chair Brainard (‘22 voter) some time after. Markets in the UK will be closed for a bank holiday.

US TSYS: Tsys Cheapen In Asia; 2s Hit 15-Year Highs

Tsys are just off session lows, having cheapened throughout the Asia-Pac session as hawkish remarks from central bankers at Jackson Hole over the weekend took focus, adding to spillover from weakness observed in Tsys on Friday after Fed Chair Powell’s speech amidst a lack of meaningful macro headline drivers.

- Cash Tsys run 6.0-10.0bp cheaper across the curve, with 7s leading the way lower after driving Friday’s weakness. 2s are ~8.0bp cheaper, with 2-Year yields operating just shy of fresh 15-year highs above the 3.47% mark.

- TYU2 is -0-22+ at 116-28 on volume of ~95K lots, operating a shade above freshly-made two-month lows at typing.

- Looking ahead, ECB Chief Economist Lane will speak ahead of the release of Dallas Fed m’fing activity data, with Fedspeak from Fed Vice Chair Brainard (‘22 voter) due after.

- Note that markets in the UK will be closed for a bank holiday today.

JGBS: Futures Soften

JGB futures have extended their earlier weakness, printing -35 last, a little off worst levels as the impetus from the cheapening in core FI markets accelerated the move lower in futures during the Tokyo afternoon. Wider cash JGBs run 1.0-4.5bp cheaper across the curve, with 30s leading the way lower.

- Looking ahead, labour market data for July and 2-Year JGB supply will headline the domestic data docket for Tuesday.

AUSSIE BONDS: A Little Off Cheaps

ACGBs have edged lower as we have worked our way through the Sydney day, with better-than-expected retail sales data for July (+1.3% M/M vs. BBG median +0.3%) exacerbating pressure from a downtick in U.S. Tsys.

- Cash ACGBs run 8.0-17.5bp cheaper across the curve, with the 3- to 5-Year zone leading the way lower. YM is-18.5 and XM is -13.5, a little off their respective session lows. EFPs have narrowed a little, with the 3-/10-Year box steepening, while Bills run 4 to 21 ticks cheaper through the reds.

- Australian retail sales for July rose at the fastest pace in four months, with the ABS suggesting that households are continuing to spend “despite cost-of-living pressures”, raising expectations from some quarters re: further RBA tightening amidst resilient consumer spending.

- STIR market pricing re: tightening for the RBA’s Sep meeting have pared an earlier, limited blip higher, and now point to ~46bp of tightening at that meeting (an ~84% chance of a 50bp hike), a marginal change from the ~45bp observed prior to the domestic retail sales print for July.

- Looking ahead, July building approval data will headline the domestic data docket.

AUSTRALIA DATA: Consumers Handling Rate Hikes

The strength of July retail sales show that Australians, at least until recently, have been able to absorb the rate hikes and the increased cost of living thanks to savings and the tight labour market. So far, what consumers are saying in consumer surveys and what they are doing are two different things.

- This data is likely to give the RBA confidence to continue on its current tightening path.

- July retail sales rose 1.3%mom - the highest rate in 4 months and above the highest market forecast of 1%. This resulted in sales growing 16.5% on the year but this is boosted strong base effects as July 2021 fell 2.6%mom (June 12%yoy).

- The strength was broad based across sectors with only household goods retailing falling for the second consecutive month. Cafes and restaurants recorded their 6th consecutive rise up 1.8% mom.

FOREX: USD Index To Fresh Cyclical Highs

The USD DXY index has touched fresh cyclical highs of close to 109.40. We have to go back to 2002 for higher levels. Dollar strength has been broad based against both the majors and Asian FX. JPY, GBP and NOK have been the weakest performers in the G10 space, although AUD is not far behind.

- Focus has rested on US yield moves, with the 2yr getting back to levels last seen in 2007 (+7% to 3.466% today). It has been slightly shaved on the day by the 10yr (+8bps to 3.12%).

- This remains a key source of USD support, while other cross asset signals have remained supportive as well. Asia Pac equities are a sea of red, with tech related bourses down sharply, while China has seen some outperformance in the equity space.

- US futures are in the red but away from worst levels (last 4030.25, versus earlier low of around 4005).

- The weaker equity backdrop has little to support the yen. USD/JPY is back to 138.60/65, highs back to July 21 of this year.

- GBP/USD is down to sub 1.1670, fresh lows going back to early 2020, while USD/NOK is back close 9.8200.

- Commodities are also weaker (ex Oil). This has weighed on AUD/USD, along with the factors outlined above. There is some support below 0.6850, with the strong retail sales beat of +1.3% versus +0.3% expected, helping at the margin. NZD/USD has seen support emerge around 0.6110.

- EUR/USD is lower, but stabilized after breaching 0.9920.

- Coming up, note that it is the UK Bank holiday today. Further out, a speech from ECB Chief Economist Lane is due, followed by the Dallas Fed m’fing activity data, and Fedspeak from Fed Vice Chair Brainard.

FX OPTIONS: Expiries for Aug29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0000-10(E1.6bln), $1.0020-25(E502mln)

- USD/JPY: Y137.00-10($808mln), Y138.00($570mln)

- AUD/USD: $0.6940-50(A$737mln)

- USD/CNY: Cny6.7750($706mln)

ASIA FX: ADXY Index Challenging 2020 Lows

Asian FX is weaker across the board, with the J.P. Morgan ADXY Index now close to 2020 lows, see the chart below. USD/CNH is just under 6.9300, while spot USD/KRW is at 1350. Broad based USD strength continues, fuelled by higher yields and weaker regional equity market sentiment.

- CNH: USD/CNH was pressing higher in early trade amidst broad USD strength against the majors. We got through 6.9000 and then 6.9200 not long after. There was a slight pause in the lead up to the CNY fixing, which was once again on the strong side of expectations (nearly 100 pips), but this support didn't last. The pair got through 6.9300, before settling back below this level, which is where we currently sit. China equities have modestly outperformed the broader sell-off elsewhere in the region.

- KRW: Spot USD/KRW sits at 1350 currently, which is +1.35% above closing levels from last week. Weakness in onshore equities has not helped, while rhetoric from the South Korean authorities around one-sided FX moves has also done little to stem USD buying pressure today.

- INR: USD/INR has pushed to new record highs above 80.00. We opened around 80.10/15 before drifting a little lower. Equities slumped at the open, but have pared losses now (still down -1.3%). India's data calendar swings back into gear this week, with Q2 GDP out on Wednesday.

- SGD: USD/SGD broke above 1.4000 in early trade but is now back below this level. We have seen modest SGD FX outperformance, which has helped the NEER edged higher. According to the Goldman Sach's estimate we aren't too far away from recent highs (just under 132.50 for the NEER).

- THB: Baht gapped lower at the open and hasn't found much traction since. USD/THB is close to 36.43, over 1% higher on closing levels form last week. Onshore equities are down 1.3% at this stage, in line with the region trend.

- MYR: Malaysian CPI, for July, came out in line with market expectations, at +4.4% YoY. We are almost back at 2021 highs. Transport and food were the main sources of inflation pressure. USD/MYR has managed to avoid fresh cyclical highs. The pair has stopped short of a move through 4.4900 for now (last at 4.4893).

Y Index Close To 2020 Lows

Source: J.P. Morgan/Bloomberg/MNI/Market News/Bloomberg

Source: J.P. Morgan/Bloomberg/MNI/Market News/Bloomberg

EQUITIES: China Outperforms, Tech Sensitive Markets Slump

Asia-Pac equities are in the red, with losses varying from less than -1% to close to -3%. This follows the Asia-Pac equities are in the red, with losses varying from less than -1% to close to -3%. This follows the sharp falls in US markets on Friday night, as US Fed Chair Powell struck a hawkish tone with markets (higher rates and for longer), which has filtered through into US fixed income moves today (US 2yr yield to 3.468%, +7bps, fresh highs since 2007) US futures are lower, albeit away from worst levels. Eminis were last at 4025, compared with earlier lows around 4005 (still -0.85% for the session). The 50-day MA comes in at 4005.38 at the moment.

- China and Hong Kong markets have outperformed on a relative basis. The Hang Seng is down around 0.65% currently, with the tech sub-index only down a touch (-0.05%). Positive spill-over from Friday's preliminary agreement, which will allow the US to audit China firms and possibly prevent delistings, has likely helped. The NASDAQ Golden Dragon China Index closed down 0.65% on Friday but outperformed the broader tech sell-off.

- The CSI 300 is down 0.40%, while the Shanghai Composite is around flat. China equities typically trade with a much lower beta to offshore moves, particularly on risk-off days. Still, the real estate sub-index remains a drag (off 1.88% for the CSI 300)

- The Kospi and Taiex are down sharply, by markets off by over 2.3%. This fits with the weaker tech lead from US markets on Friday night and the further gains in US yields today. The tech sector has shown strong sensitivity to US yield moves in 2022. The South Korean authorities have announced they will launch an investigation into short-selling of stocks this week.

- The ASX200 has also slumped, down over 2%. Outside of IT weakness, heavyweights in the materials and financial sub-sectors have fallen by slightly more than the headline index. Commodity prices have remained on the back foot (ex Oil). CMX copper is now off by 2%, iron ore down by 4% to $101.45/tonne. Gold is also down by 0.65% to $1727.

GOLD: One-Month Lows In Asia As Dollar Rallies

Gold is ~$12/oz worse off to print $1,726/oz, sitting a little above freshly made one-month lows at writing after breaking below Friday’s trough earlier.

- The move lower comes amidst an uptick in nominal U.S. Tsy yields and the USD (DXY), with the latter hitting its own fresh cycle highs above the 109.00 mark.

- The precious metal remains firmly on track for a fifth consecutive lower monthly close, the longest such losing streak since 2018.

- To recap Friday’s price action, gold closed ~$20/oz lower following Fed Chair Powell’s hawkish (and relatively short) speech at the Jackson Hole Symposium, with participants focusing on comments re: keeping rates restrictive “for some time”.

- From a technical perspective, gold has broken initial support at $1,727.8/oz (Aug 22 low), exposing further support at $1,711.7/oz (Jul 27 low). Further declines will see gold approach support at $1,681.0/oz, the Jul 21 low and bear trigger. On the other hand, initial resistance is seen at ~$1,765.5/oz (20-Day EMA).

OIL: Higher In Asia As OPEC Production Cut Speculation Grows

WTI and Brent are $1.10 firmer apiece, building on a move off of their respective post-Powell lows observed on Friday.

- To recap Friday’s price action, both benchmarks reversed losses observed after Fed Chair Powell warned of “pain to households and businesses” ahead, ultimately closing ~$0.50 higher apiece amidst signs that OPEC may be considering output cuts.

- To elaborate on the latter, speculation over the prospect of output quota cuts continues to simmer as RTRS source reports have pointed to UAE support for such a measure, adding to recent, similar comments from the Saudi Energy Minister and the current OPEC President.

- A note that RTRS sources had suggested last week that OPEC production cuts would likely “coincide” with the return of Iranian crude to global supplies.

- On that topic, Iran will take until “at least” Sep 2 to respond to the latest U.S. reply re: a U.S.-Iran nuclear deal. Kpler and Vortexa have pointed to >70mn bbls of Iranian crude stored on vessels in various locations, ready for delivery upon a successful agreement.

- Elsewhere, Libya’s capital of Tripoli witnessed a surge in violence over the weekend (a result of ongoing political unrest as factions struggle for control of the capital), raising worry from some quarters re: the stability of recently-restored Libyan crude production (>1.2mn bpd).

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/08/2022 | 0600/0800 | *** |  | SE | GDP |

| 29/08/2022 | 0600/0800 | ** | | SE | Retail Sales |

| 29/08/2022 | 1300/1500 |  | EU | ECB Chief Economist Philip Lane Speaks at CEBRA | |

| 29/08/2022 | 1430/1030 | ** |  | US | Dallas Fed manufacturing survey |

| 29/08/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 29/08/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 29/08/2022 | 1815/1415 | | US | Fed Vice Chair Lael Brainard |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.