Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- YELLEN SEES PATH FOR COOLER PRICES WITHOUT JUMP IN JOBLESS RATE (BBG)

- ECB’S SCHNABEL SEES INFLATION PRESSURE IN ‘ALL PARTS’ OF ECONOMY (BBG)

- BOE'S HASKEL SEES TENSION WITH GOVERNMENT FISCAL EXPANSION (RTRS)

- BOE'S HASKEL SAYS HE IS NOT WORRIED BY STERLING (RTRS)

- JAPAN PM KISHIDA SAYS READY TO ACT AGAIN TO SUPPORT YEN (RTRS)

- NIGERIAN OIL MINISTER: OPEC MAY CUT OUTPUT IF PRICES FALL MORE (BBG)

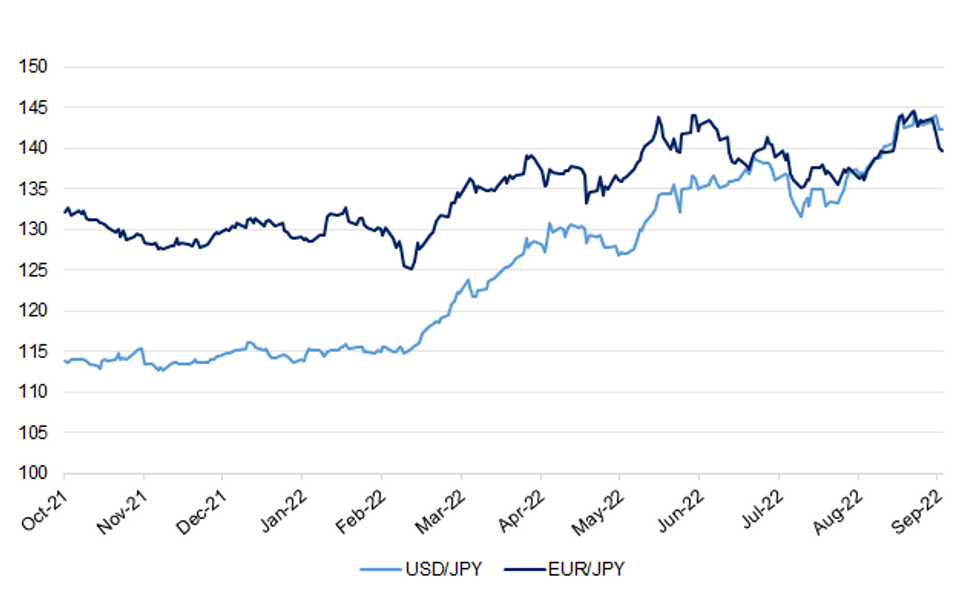

Fig. 1: USD/JPY & AUD/JPY

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

UK

FISCAL: UK chancellor Kwasi Kwarteng will on Friday attempt to deliver shock treatment to Britain’s stagnating economy, with a 30-point growth package to turn “the vicious cycle of stagnation into a virtuous circle of growth”. (FT)

BOE: Bank of England (BoE) policymaker Jonathan Haskel said the central bank was in a difficult position as the government's expansionary fiscal policy appeared to place it at odds with the BoE's efforts to cool inflation. (RTRS)

BOE: Bank of England policymaker Jonathan Haskel said he was not very concerned about the level of sterling, after being challenged about the currency's weakness. (RTRS)

EUROPE

ECB: Upward pressure on consumer pressures has spread from energy to engulf the whole euro-zone economy, according to European Central Bank Executive Board member Isabel Schnabel. (BBG)

ITALY: Italy’s two largest right-wing parties are already locked in a tussle over ministerial appointments in what polls indicate is almost certain to be their shared government after Sunday’s elections, with likely future prime minister Giorgia Meloni trying to keep the nationalist League out of positions which could cause trouble with the European Union, senior officials at the parties involved told MNI. (MNI)

RATINGS: Potential rating reviews of note scheduled for after hours on Friday include:

- Moody’s on Hungary (current rating: Baa2; Outlook Stable) and Sweden (current rating: Aaa; Outlook Stable)

- S&P on Germany (current rating: AAA; Outlook Stable)

- DBRS Morningstar on Finland (current rating: AA (high); Stable Trend) and the European Union (current rating: AAA; Stable Trend)

U.S.

ECONOMY: US Treasury Secretary Janet Yellen continues to see a path to lower inflation without a significant increase in unemployment, even as the Federal Reserve maintains an aggressive rate-hike strategy that could trigger a growth slowdown or a recession. (BBG)

TSYS: Reduced Treasury liquidity since the beginning of the year has served as a daily reminder that regulators need to be vigilant in monitoring market risks and continue to explore ways to enhance Treasury market resilience, Treasury Under Secretary for Domestic Finance Nellie Liang said Thursday. (MNI)

OTHER

JAPAN: Japanese Prime Minister Fumio Kishida said on Thursday excessive movement in the yen due to speculation cannot be overlooked and that his government would act "with a high level of vigilance" and intervene to support the currency again if necessary. (RTRS)

JAPAN: The US Treasury stopped short of explicitly endorsing Japan’s action to intervene in the foreign-exchange market Thursday, while saying it understood the move. (BBG)

HONG KONG: Hong Kong set to announce on Friday end to mandatory hotel quarantine for overseas arrivals. (SCMP)

BRAZIL: Brazil's presidential frontrunner Luiz Inacio Lula da Silva slightly boosted his lead over incumbent President Jair Bolsonaro to 14 percentage points in a poll published on Thursday by pollster Datafolha, less than two weeks before the Oct. 2 first-round vote. (RTRS)

BRAZIL: Brazil’s Economy Ministry projected on Thursday a primary budget surplus of 13.548 billion reais ($2.63 billion) for the central government this year, according to its latest bi-monthly revenue and expenditure report. (RTRS)

SOUTH AFRICA: The African Development Bank has suggested a plan to South Africa that will help the nation use the $8.5 billion in climate financing pledged by some of the world’s richest nations to raise even more funds. (BBG)

IRAN: Speaking to reporters, a senior U.S. State Department official rejected putting pressure on the IAEA to close those investigations unless Iran provides satisfactory answers. "In a nutshell, we’ve hit a wall because of Iran’s position and I think their position is so unreasonable in terms of what they’re asking for with regards to the IAEA probe into the unexplained presence of traces of uranium particles," he said. (RTRS)

CHILE: Chile estimates it will issue $12 billion in total debt next year and the largest budget increases will be in social protection and science and technology, Finance Minister Mario Marcel told Reuters on Thursday. (RTRS)

ENERGY: Iranian President Ebrahim Raisi on Thursday called on gas and oil producers to work together to stabilise energy markets. (RTRS)

ENERGY: A temporary brake on gas and electricity derivatives when prices spike could improve how energy markets operate, the European Union's securities watchdog proposed on Thursday, along with more fundamental changes over time. (RTRS)

ENERGY: European authorities have played down their ability to intervene in the region’s derivatives markets to help stretched energy companies after privately admitting energy price volatility was not due to the “market malfunctioning”. (FT)

OIL: European Union member states are racing to clinch a political agreement within weeks that would impose a price cap on Russian oil. (BBG)

OIL: A planned Western price cap on Russian oil is already making a difference, U.S. Treasury Secretary Janet Yellen said on Thursday, noting that Russia was now offering China and India "enormous discounts" while looking for other outlets for its oil. (RTRS)

OIL: Poland will only help supply oil to Germany's PCK Schwedt refinery if Russia's Rosneft is completely removed as a shareholder, Poland's climate ministry said, raising pressure on Germany to completely nationalise the refiner. (RTRS)

OIL: Russian President Vladimir Putin and Saudi Crown Prince Mohammed bin Salman spoke on Thursday and praised efforts within the OPEC+ framework, confirming their intention to stick to existing agreements, the Kremlin said. (RTRS)

OIL: The production cartel may be “forced” to make additional production cuts if crude prices fall below current levels, Nigeria’s oil minister said in an interview in New York. (BBG)

CHINA

YUAN: There is no reason for a sharp depreciation of the yuan against the U.S. dollar following this week's Federal Reserve rate hike, the 21st Century Business Herald reported. (MNI)

ECONOMY: Local governments are required to effectively implement pro-growth policies and stabilize the economy, according to a statement on the government's website following the State Council executive meeting chaired by Premier Li Keqiang. (MNI)

EQUITIES: The impact of the Federal Reserve’s tightening on China’s A-share market is expected to be relatively limited, the China Securities Journal reported citing analysts. (MNI)

CHINA MARKETS

PBOC NET INJECTS CNY21 BILLION VIA OMOS FRIDAY

The People's Bank of China (PBOC) on Friday injected CNY2 billion via 7-day reverse repos and CNY21 billion via 14-day reverse repos with the rates unchanged at 2.00% and 2.15%, respectively. The operations have led to a net injection of CNY21 billion after offsetting the maturity of CNY2 billion reverse repos today, according to Wind Information.

- The operation aims to keep liquidity stable at quarter-end, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.6905% at 09:43 am local time from the close of 1.5962% on Thursday.

- The CFETS-NEX money-market sentiment index closed at 47 on Thursday vs 45 on Wednesday.

PBOC SETS YUAN CENTRAL PARITY AT 6.9920 FRI VS 6.9798 THURS

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher for a sixth trading day at 6.9920 on Friday, compared with 6.9798 set on Thursday.

OVERNIGHT DATA

AUSTRALIA SEP, P S&P GLOBAL MANUFACTURING PMI 53.9; AUG 53.8

AUSTRALIA SEP, P S&P GLOBAL SERVICES PMI 50.4; AUG 50.2

AUSTRALIA SEP, P S&P GLOBAL COMPOSITE PMI 50.8; AUG 50.2

Latest S&P Global PMI Flash data brought about mixed feelings towards the current and future health of Australia’s private sector economy. (S&P Global)

SOUTH KOREA AUG PPI +8.4% Y/Y; JUL +9.2%

UK SEP GFK CONSUMER CONFIDENCE -49; MEDIAN -42; AUG -44

MARKETS

SNAPSHOT: Risk Negative Tone Reverberates In Asia

Below gives key levels of markets in the second half of the Asia-Pac session:

- Nikkei 225 is closed

- ASX 200 down 147.023 points at 6553.2

- Shanghai Comp. down 33.576 points at 3075.334

- JGBs are closed

- Aussie 10-Yr future down 24 ticks at 96.045, yield up 25.3bp at 3.918%

- U.S. 10-Yr future -0-03+ at at 112-20+, cash Tsys are closed

- WTI crude down $0.55 at $82.95, Gold down $2.27 at $1668.95

- USD/JPY down 15 pips at Y142.24

- YELLEN SEES PATH FOR COOLER PRICES WITHOUT JUMP IN JOBLESS RATE (BBG)

- ECB’S SCHNABEL SEES INFLATION PRESSURE IN ‘ALL PARTS’ OF ECONOMY (BBG)

- BOE'S HASKEL SEES TENSION WITH GOVERNMENT FISCAL EXPANSION (RTRS)

- BOE'S HASKEL SAYS HE IS NOT WORRIED BY STERLING (RTRS)

- JAPAN PM KISHIDA SAYS READY TO ACT AGAIN TO SUPPORT YEN (RTRS)

- NIGERIAN OIL MINISTER: OPEC MAY CUT OUTPUT IF PRICES FALL MORE (BBG)

US TSYS: Futures Little Changed To A Touch Lower, Cash Closed On Japanese Holiday

Tsy futures sit little changed to marginally below Thursday’s settlement levels, after recovering from their respective Asia-Pac session bases. TYZ2 is -0-03 at 112-21, 0-02+ off the base of its 0-07 overnight range, through Thursday’s low.

- Note that cash Tsys are closed until London hours owing to the observance of a Japanese national holiday.

- Thursday saw fresh cycle highs for all of the major U.S. Tsy benchmark yield metrics, as the 10-Year Tsy yield broke decisively through the upper end of the upward sloping channel that we have identified on several occasions. Consolidation above allows Tsy bears to switch focus to the ’11 high at (3.7760%). A move beyond that level would expose the psychological 4.00% area, as well as the double top from ‘09/’10, which resides just above the round number.

- There wasn’t much in the way of market moving headline flow observed in Asia, which left regional reaction to the latest leg of global core FI cheapening at the fore.

- Friday’s NY docket will see the release of flash S&P PMI data. Elsewhere, Fed Chair Powell is set to give opening remarks at a Fed Listens event as the post-FOMC blackout comes to an end.

- Flash PMI data out from across Europe & the UK mini budget prevent some areas of interest in pre-NY hours.

AUSSIE BONDS: Sharp Sell Off After Holiday, RBA Terminal Pricing Jumps

Aussie yields surged as domestic participants played catch up after Thursday’s holiday, with bearish pressure increasing on technical breaks in YM & XM futures, which allowed bears to switch focus to the June cycle lows in the respective contracts. YM -21.5 & XM -24.0 at typing.

- Yields run 21-27bp higher across the curve, with the 3- to 5-Year sector leading the weakness.

- The 3-/10-Year EFP box has flattened, with 3-Year EFP the best part of 5bp wider and 10-Year EFP little changed.

- Bills run 5-26bp lower through the reds, steepening.

- RBA dated OIS sees a bit of a reluctance to price much more into the Oct meeting (last ~44bp), given the Bank’s reference to a need to slow the pace of hikes at some point and pre-meeting outline of discussions surrounding 25 & 50bp hikes. Further out, terminal rate pricing moves up to 4.15%, sharply higher on the day, although nowhere near challenging the cycle peaks of ~4.50% printed back in June.

- Next week’s domestic data docket is headlined by retail sales, job vacancies and the new monthly CPI print.

- Nothing really stands out when it comes to next week’s AOFM issuance slate, outside of a chunky A$2.5bn return of Note issuance after this week’s holiday-inspired hiatus.

EQUITIES: Asia Pac Tech Underperforms

It's a sea of red across the Asia Pac equity space. Asian markets have taken their cue from negative offshore leads overnight, with tech sensitive sectors underperforming. Weaker US futures, which are only marginally off session lows (around -0.20% currently), has also weighed.

- Note Japan markets are closed today, which has probably impacted regional liquidity to a degree.

- Hong Kong stocks have taken little comfort, in an aggregate sense, from an end to hotel quarantine for overseas arrivals, although the move was well flagged earlier in the week.

- The main HSI bourse is off around -0.85%, while the tech sub-index is down 1.90%, at the time of writing. Mainland China stocks haven't fared much better, down around 1% at this stage for the Shanghai Composite.

- The Kospi is off by 1.6%, offshore investors selling -$333.6mn in local stocks today. Higher core yields (particularly US real yield yields) are weighing on the regional tech backdrop. TWSE losses are now close to 1.20% for the session.

- The ASX 200 is off over 2.2%, but this reflects some catch up after onshore markets were closed for a public holiday yesterday.

OIL: Brent Eyeing Fresh Test Of $90/bbl

Early resilience in Brent crude didn't last, we are now back close to $90/bbl. It's a similar story for WTI, back to the low $83/bbl region. Overall ranges have been modest, albeit with a downside bias. Tighter policy from major central banks and clouds over the global economic outlook remain the main concerns on the demand outlook.

- Brent is on track for its fourth straight weekly decline. Focus is likely to remain on whether we can break below the $90/bbl and trend down further. Dips sub this level have been supported so far in September.

- Still, the sell-side consensus is for a recovery in oil prices through Q4 (see this Bloomberg article for more details).

- Nigeria's oil minister stated that OPEC+ may be forced to make additional production cuts if prices continue to fall. A call between Russian President Putin and Saudi Crown Prince Mohammed bin Salman also committing to maintaining current OPEC+ agreements.

- Earlier headlines, from Reuters, also suggested little progress in terms of a fresh US-Iran nuclear deal.

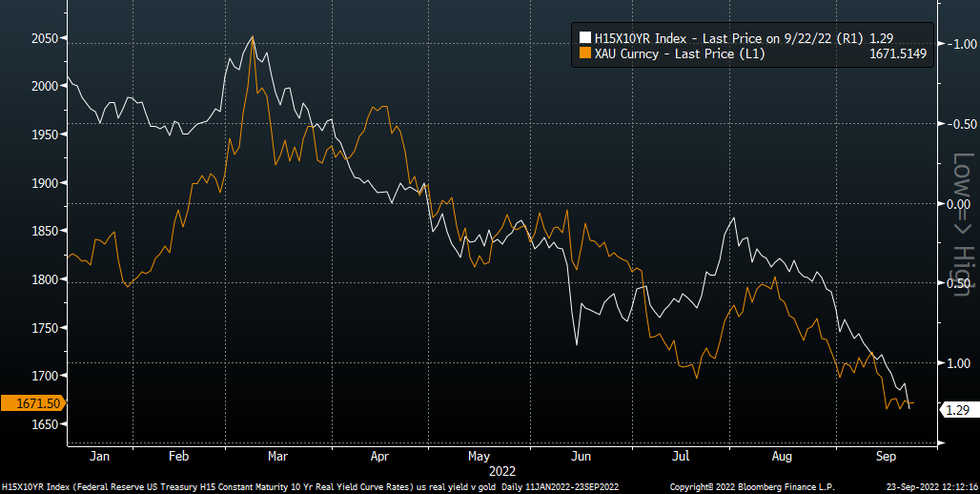

GOLD: Respecting Recent Ranges

Gold continues to respect recent ranges, as it has done for much of the past week. We currently sit in the middle of the recent range at $1670, down slightly from NY closing levels. The precious metal has spent little time outside of $1660/$1680 this past week.

- The metal has found support on a number of occasions around the $1655 in recent weeks, so this level is offering some support on the downside.

- Still, a test and potential break remains a medium term risk. The chart below overlays spot gold against the US 10yr real yield (which is inverted on the chart). Higher real yields should weigh further on gold, all else equal.

- The metal outperformed the continued run higher in core yields overnight, although did find some relief from firmer yen levels.

- Also note the continued fall in gold ETF holdings, which paints a negative flow picture. Such holdings are still above lows from the beginning of the year.

Fig 1: Gold & US Real Yield (10yr)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

FOREX: Risk Comes Under Pressure, Yuan Sell-Off Continues

Risk appetite was subdued as the dust settled after Wednesday's hawkish Fed monetary policy decision and a marathon of central bank decisions on "Super Thursday." Japan observed a public holiday, which came in between markets closures in Australia (Thursday) and New Zealand (Monday), limiting regional activity. Riskier currencies sold off as e-mini futures slipped into the red.

- The likes of USD, JPY and CHF capitalised on their safe-haven status, albeit yen volatility was very limited relative to Thursday, when Japanese authorities intervened in currency markets after the BoJ kept its ultra-loose monetary policy settings unchanged. Heightened risk of repeated intervention on Monday likely gave the yen an edge over its safe-haven peers.

- Selling pressure hit the Antipodeans, albeit nearby cycle lows in AUD/USD and NZD/USD remained intact. Regional risk barometer AUD/JPY was the big mover overnight, shedding ~45 pips through the session.

- Yuan depreciation showed no signs of exhaustion, despite the 22nd consecutive stronger-than-expected PBOC fixing. The mid-point of permitted USD/CNY trading band was set 838 pips below sell-side estimate, not enough to promote yuan recovery. Spot USD/CNH climbed to a new cyclical high (CNH7.1134), which may have had knock-on effect on the Antipodeans.

- Fed's Powell, SNB's Jordan, as well as ECB's Nagel & Kazaks will speak later on Friday. Data highlights include a slew of PMI readings and Canadian retail sales.

FX OPTIONS: Expiries for Sep23 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9900(E536mln), $0.9950(E724mln), $0.9986-00(E3.1bln), $1.0150(E1.2bln)

- USD/JPY: Y139.85-00($513mln)

- AUD/USD: $0.6675(A$751mln), $0.6865(A$554mln)

- USD/CNY: Cny6.9500($940mln), Cny7.0000($828mln)

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/09/2022 | 0715/0915 | ** |  | FR | IHS Markit Services PMI (p) |

| 23/09/2022 | 0715/0915 | ** | | FR | IHS Markit Manufacturing PMI (p) |

| 23/09/2022 | 0730/0930 | ** |  | DE | IHS Markit Services PMI (p) |

| 23/09/2022 | 0730/0930 | ** | | DE | IHS Markit Manufacturing PMI (p) |

| 23/09/2022 | 0800/1000 | ** |  | EU | IHS Markit Services PMI (p) |

| 23/09/2022 | 0800/1000 | ** | | EU | IHS Markit Manufacturing PMI (p) |

| 23/09/2022 | 0800/1000 | ** | | EU | IHS Markit Composite PMI (p) |

| 23/09/2022 | 0830/0930 | *** |  | UK | IHS Markit Manufacturing PMI (flash) |

| 23/09/2022 | 0830/0930 | *** | | UK | IHS Markit Services PMI (flash) |

| 23/09/2022 | 0830/0930 | *** | | UK | IHS Markit Composite PMI (flash) |

| 23/09/2022 | 1000/1100 | ** | | UK | CBI Distributive Trades |

| 23/09/2022 | 1230/0830 | ** |  | CA | Retail Trade |

| 23/09/2022 | 1345/0945 | *** |  | US | IHS Markit Manufacturing Index (flash) |

| 23/09/2022 | 1345/0945 | *** | | US | IHS Markit Services Index (flash) |

| 23/09/2022 | 1800/1400 | | US | Fed Listens Event |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.