Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- TOP FED OFFICIAL WARNS OF MORE PERSISTENT PRICE PRESSURES (WSJ)

- KWASI KWARTENG TO BRING FORWARD DEBT-CUTTING PLAN AFTER TAX U-TURN (FT)

- LIZ TRUSS TAKES ON TORY REBELS IN BATTLE TO REIN IN BENEFITS (TELEGRAPH)

- BOE'S MANN SAYS STERLING, INFLATION, ENERGY INFLUENCED HER RATE HIKE VOTE (RTRS)

- RBA RETURNS TO ‘BUSINESS AS USUAL’ 0.25PC RATE RISE (AFR)

- NORTH KOREA FIRES IRBM OVER JAPAN (YONHAP)

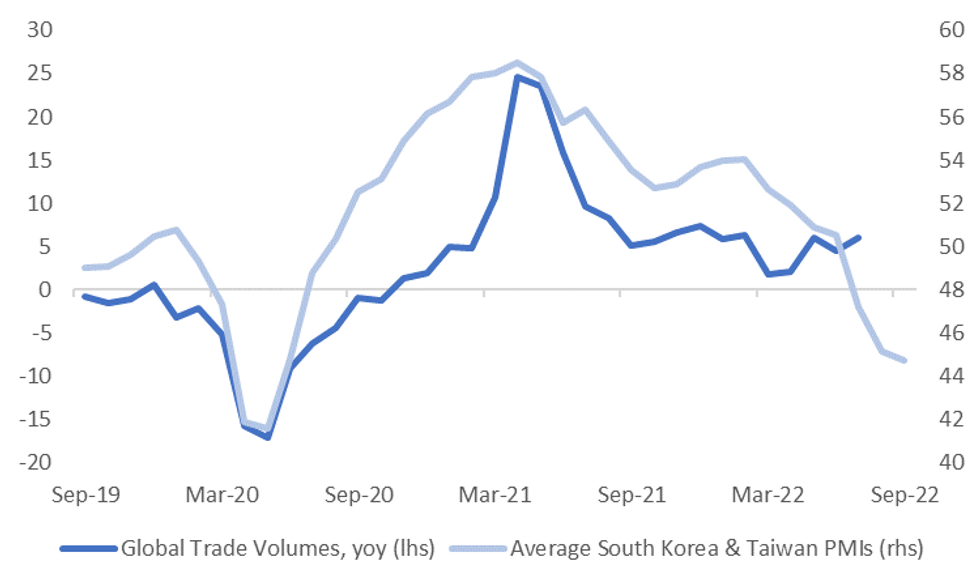

Fig. 1: Global Trade Volumes Vs. Average South Korea & Taiwan PMI Readings

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

UK

BOE: The Bank of England will start asking market makers to identify who is looking to sell gilts to its temporary bond-buying program, a move that looks aimed at helping financial stability rather than speculators. (BBG)

BOE: Bank of England policymaker Catherine Mann said her vote last month to raise Bank Rate by 0.75 percentage points reflected a weak currency, rising inflation expectations and the boost to household incomes from an energy price cap. (RTRS)

FISCAL: Kwasi Kwarteng on Monday promised “no more distractions” as he was forced to fight off calls to resign over the Government’s 45p tax rate U-turn. (Telegraph)

FISCAL: Chancellor Kwasi Kwarteng is to accelerate the publication of his plan to cut Britain’s debt in an attempt to reassure markets after he was forced to make a humbling U-turn on a key part of his “mini-Budget”. (FT)

FISCAL/POLITICS: Liz Truss is facing a new battle with Tory MPs over reducing benefits in real terms, after being forced to abandon the abolition of the 45p top rate of tax. (Telegraph)

FISCAL/POLITICS: Liz Truss will struggle to drive through key parts of the economic revolution she’s planning for the UK because her standing in the ruling party is already so damaged, members of her Cabinet said. (BBG)

POLITICS: The UK’s opposition Labour Party surged to a 25-point lead over the ruling Conservatives in a Savanta ComRes poll on Monday that highlights the damage done to Liz Truss’s Tories by her economic strategy 10 days ago. (BBG)

PROPERTY: Three UK asset managers have said they are unable to handle heavy demand from investors seeking to withdraw from property funds, in another sign of how an accelerating decline in government bond prices is forcing pension funds to reallocate holdings. (FT)

EUROPE

FISCAL: European Commissioners Thierry Breton and Paolo Gentiloni said the current energy crisis requires solidarity among European member states including the issuance of joint-guaranteed debt similar to what was done during the pandemic .(BBG)

U.S.

FED: Despite some signs of easing inflation, underlying price pressures have too much momentum and will likely require a period of higher interest rates, a top Federal Reserve official said Monday. (WSJ)

FED: Federal Reserve Bank President Thomas Barkin said that shifts taking place in the post-pandemic economy could potentially lead to more inflationary headwinds that require tighter monetary policy. (BBG)

ECONOMY: U.S. manufacturing could be on a path to a contraction in the first half of 2023 after activity grew at the slowest pace in more than two years in September, Institute for Supply Management chair Timothy Fiore told MNI Monday. (MNI)

OTHER

CENTRAL BANKS: The Federal Reserve and other central banks risk pushing the global economy into recession followed by prolonged stagnation if they keep raising interest rates, a United Nations agency said Monday. (WSJ)

CENTRAL BANKS: Central banks will find climate change disrupts the global economy in a way similar to the Covid pandemic, the head of the Toronto Centre that trains global financial supervisors told MNI. (MNI)

U.S./CHINA: The Biden administration is expected to announce new measures to restrict Chinese companies from accessing technologies that enable high-performance computing, according to several people familiar with the matter, the latest in a series of moves aimed at hobbling Beijing’s ambitions to craft next-generation weapons and automate large-scale surveillance systems. (New York Times)

RBA: The Reserve Bank of Australia returned to a “business as usual” 0.25 percentage point increase in the official interest rate on Tuesday, as it decelerated to assess the economic outlook. (AFR)

NEW ZEALAND: The latest NZIER Quarterly Survey of Business Opinion (QSBO) suggests that businesses are still feeling downbeat in the September quarter, but they are also starting to see the light at the end of the tunnel. (NZIER)

SOUTH KOREA: Finance Minister Choo Kyung-ho said Tuesday the government will implement appropriate responses preemptively by reviewing all options available in accordance with possible scenarios of financial and foreign exchange market instabilities. (Yonhap)

SOUTH KOREA: South Korea is expected to activate stock stabilization fund in mid-Oct. to prevent volatility increase in financial markets, Yonhap News reports, citing unidentified sources. (BBG)

NORTH KOREA: North Korea fired an intermediate-range ballistic missile (IRBM) over Japan on Tuesday in its first launch of an IRBM in eight months, according to South Korea's military. (Yonhap)

HONG KONG: China has demanded the floor plans of all properties rented by foreign missions in Hong Kong, in a move diplomats believe reflects Beijing’s paranoia about overseas interference in the Asian financial hub’s turbulent politics. (FT)

BRAZIL: Luiz Inacio Lula da Silva huddled in Sao Paulo with his top advisers as the leftist former Brazilian president sought to pivot his campaign to the northeast of the country and the key state of Sao Paulo after a narrower-than-expected first round vote. (BBG)

RUSSIA: Ukraine appears on course to achieve several key battlefield objectives it set for itself, a senior Pentagon official said on Monday, as Ukrainian forces made fresh gains along the Dnipro River. (RTRS)

RUSSIA: President Putin is set to demonstrate his willingness to use weapons of mass destruction with a nuclear test on Ukraine’s borders, defence sources have warned. (The Times)

ARGENTINA: Argentina’s government will allow tech companies to hold 30% of their dollars when they increase exports, the country’s Knowledge Economy Secretary Ariel Sujarchuk said in a press conference. (BBG)

IMF: Global recession can be avoided if governments' fiscal policies were consistent with monetary policy tightening, but likely there would be countries falling into recession next year, the International Monetary Fund's managing director said on Monday. (RTRS)

ENERGY: Turkish officials have asked Russia to delay a portion of Ankara’s payments due for natural gas, according to people familiar with the matter, as Turkey seeks to mitigate economic damage from higher energy prices. (BBG)

OIL: Russian Deputy Prime Minister Alexander Novak is set to attend the OPEC+ meeting in Vienna, according to people familiar with the situation, as the alliance prepares for a show of unity and the biggest production cut since 2020. (BBG)

OVERNIGHT DATA

JAPAN SEP TOKYO CPI +2.8% Y/Y; MEDIAN +2.8%; AUG +2.9%

JAPAN SEP TOKYO CPI EX-FRESH FOOD +2.8% Y/Y; MEDIAN +2.8%; AUG +2.6%

JAPAN SEP TOKYO CPI EX-FRESH FOOD & ENERGY +1.7% Y/Y; MEDIAN +1.6%; AUG +1.4%

JAPAN SEP MONETARY BASE -3.3 Y/Y; AUG +0.4%

JAPAN SEP MONETARY BASE Y618.1TN; AUG Y645.0TN

AUSTRALIA AUG HOME LOAN VALUE -3.4% M/M; MEDIAN -3.0%; JUL -8.5%

AUSTRALIA AUG BUILDING APPROVALS +28.1% M/M MEDIAN +10.0%; JUL -18.2%

AUSTRALIA SEP ANZ JOB ADVERTISEMENTS -0.5% M/M; AUG +1.5%

ANZ Australian Job Ads1 declined by 0.5 per cent m/m in September, following a small downward revision of the August result. But this is only 0.8 per cent below the recent peak in June. This suggests tightness in the labour market is not yet letting up, which is consistent with other indicators. (ANZ)

AUSTRALIA WEEKLY ANZ-ROY MORGAN CONSUMER CONFIDENCE 85.5; PREV. 87.8

The weakness in global financial markets through last week weighed on Australian consumers. A plethora of negative news last week ranging from the UK’s mini budget to hawkish Fed commentary impacted the AUD, which weakened to its two-year lows. (ANZ)

SOUTH KOREA SEP S&P GLOBAL MANUFACTURING PMI 47.3; AUG 47.6

Given the rapid deterioration in global manufacturing conditions, it's unsurprising to see business conditions in an open economy like South Korea trend lower. Goods production slumped at its sharpest rate since the beginning of the COVID-19 pandemic in the first half of 2020, reflecting weak demand, client order cancellations and overstocked inventory levels at both producers and their customers alike. (S&P)

MARKETS

SNAPSHOT: RBA Starts To Ease Off Brake

Below gives key levels of markets in the second half of the Asia-Pac session:

- Nikkei 225 up 747.35 points at 26963.14

- ASX 200 up 242.435 points at 6699.3

- Shanghai Comp. is closed

- JGB 10-Yr future up 48 ticks at 149.04, yield down 1.5bp at 0.231%

- Aussie 10-Yr future up 20 ticks at 96.25, yield down 17.2bp at 3.727%

- US 10-Yr future up 0-07 at 113-13+, yield down 1.37bp at 3.625%

- WTI crude up $0.20 at $83.83, Gold down $1.56 at $1698.33

- USD/JPY up 30 pips at Y144.85

- TOP FED OFFICIAL WARNS OF MORE PERSISTENT PRICE PRESSURES (WSJ)

- KWASI KWARTENG TO BRING FORWARD DEBT-CUTTING PLAN AFTER TAX U-TURN (FT)

- LIZ TRUSS TAKES ON TORY REBELS IN BATTLE TO REIN IN BENEFITS (TELEGRAPH)

- BOE'S MANN SAYS STERLING, INFLATION, ENERGY INFLUENCED HER RATE HIKE VOTE (RTRS)

- RBA RETURNS TO ‘BUSINESS AS USUAL’ 0.25PC RATE RISE (AFR)

- NORTH KOREA FIRES IRBM OVER JAPAN (YONHAP)

US TSYS: Bull Steepening, Aided By Dovish RBA Surprise

TYZ2 deals +0-10 at 113-16+, 0-03 off the recently printed session high. The contract has operated in a 0-12+ range, on above average volume of ~179K, even with Hong Kong & China observing holidays.

- Early Asia-Pac trade saw Tsys rally on the latest North Korean missile launch, which flew over Japanese airspace. Although the lack of damage to Japanese assets and fact that the missile landed outside of Japan’s EEZ, in the Pacific Ocean, allowed the space to retrace the related bid. The retrace was further aided by a block sale in FV futures (-5.7K).

- A fresh bid came back in later in the session on the back of a dovish surprise from the RBA, as the Bank delivered a 25bp hike vs. the widely expected and largely priced 50bp step.

- This saw all of the major Tsy benchmarks register fresh session lows in yield terms, with the front end continuing to outperform, as it has all session (albeit as the curve flipped between bullish and twist steepening on a couple of occasions). A couple of block sales in TU futures (-1.4K & -1.3K) may have limited the post-RBA uptick.

- Looking ahead, Tuesday’s NY docket will be headlined by final durable goods readings, JOLTS job opening data and Fedspeak from Jefferson, Williams, Mester, Logan & Daly

JGBS: Futures Outperform, 10-Year JGB Supply Goes Well

JGBs have regained some poise in the wake of today’s 10-Year JGB auction. That leaves cash JGBS running unchanged to 4bp richer across the curve, while futures have managed to punch through their overnight high, last dealing +48, just off best levels.

- Futures (and therefore 7s) outperformed all day, while the longer end has unwound the weakness that was observed in the latter rounds of Tokyo morning trade (which came as the Nikkei 225 rallied, and some space was made for the impending round of JGB supply).

- Early Tokyo trade saw a bid on the back of the latest North Korean missile test, which flew over Japan, before landing in the Pacific Ocean, outside of the country’s EEZ, causing no damage. The lack of damage saw JGBs off their morning peaks and allowed the Nikkei 225 to rally further.

- The latest round of 10-Year JGB supply was well received, with the cover ratio jumping to the highest level witnessed at a 10-Year auction since the multi-year high observed in May, as the price tail narrowed and low price matched wider expectations.

- Spill over from the RBA-driven bid in the ACGB space would have helped JGBs during the Tokyo afternoon.

- Local data had no tangible impact on the space, with Tokyo CPI virtually in line with wider exp.

JGBS AUCTION: Japanese MOF sells Y2.1947tn 10-Year JGBs:

The Japanese Ministry of Finance (MOF) sells Y2.1947tn 10-Year JGBs:

- Average Yield: 0.248% (prev. 0.235%)

- Average Price: 99.53 (prev. 99.66)

- High Yield: 0.250% (prev. 0.239%)

- Low Price: 99.51 (prev. 99.62)

- % Allotted At High Yield: 14.1495% (prev. 66.2307%)

- Bid/Cover: 5.552x (prev. 4.014x)

AUSSIE BONDS: RBA Only Delivers 25bp Hike, Triggering Repricing Of Terminal Rate

A surprise 25bp hike from the RBA (~45bp of tightening was priced into dated OIS covering today’s RBA meeting) put an immediate bid into the Aussie fixed income space, with terminal rate pricing reassessed, falling back to ~3.60% vs. the ~4.10% level seen late Friday/early today (some of that was attributable to spill over from the moves in market pricing re: BoE hikes on Monday).

- 3-Year ACGB yields plummeted to near 3.00% vs. the ~3.45% see ahead of the decision, before rebounding to trade around the 3.25% mark into the close. Cash ACGBs run 13-35bp richer across the curve, with 3s leading as the curve bull steepens. YM is +26.0 & XM is +23.

- Bills have surged on the repricing of expectations surrounding the RBA’s terminal rate, running 37-62bp firmer on the day through the reds into the close, off of best levels, with IRH3 & M3 outperforming.

- The Bank noted that it expects to increase interest rates further in the period ahead (previously it flagged in “the months ahead”), while it highlighted the speed of the previously deployed tightening and the deteriorating global conditions in its post meeting statement. Household consumption remains key, and it seems that the lagged impact of monetary policy was integral to the RBA’s thought process when it came to slowing rates, which is understandable given the level of debt in the Australian economy.

- The Bank also dropped the reference to monetary policy not being on a pre-set path.

NZGBS: NZGBs Bull Steepen Ahead Of RBNZ

NZGBs extended their early richening on the back of the latest North Korean missile launch, which crossed Japanese airspace, but ultimately failed to cause any damage to Japanese assets before landing in the Pacific Ocean, outside of Japan’s EEZ.

- The lack of damage allowed core FI to pull away from richest levels of the session, facilitating a similar move in NZGBs.

- The major NZGB benchmarks finished 7-10bp richer, with some light bull steepening in play.

- The latest NZIER QSBO had no real impact on the space, with a notable number of businesses outlining their intentions to deploy further price hikes in Q4.

- Looking ahead, early Wednesday trade will likely be shaped by the trans-Tasman impetus derived from today’s shock RBA decision (25bp hike vs. the consensus 50bp, which triggered a repricing of RBA terminal rate exp.). However, the impact from the RBNZ decision will dominate as we work through Wednesday’s session.

- A reminder that all of those surveyed by BBG look for a 50bp hike to the OCR tomorrow, with such a move fully priced into the OIS strip. The RBNZ’s guidance will be key, with a terminal rate of ~4.65% now priced after a pullback alongside today’s richening in NZGBs/in lieu of yesterday’s pullback in pricing surrounding BoE tightening expectations (this could be adjusted further post-RBA).

EQUITIES: Australian Stocks Outperform On Lower Than Expected RBA Hike

The regional equity space has been quieter today, with China and Hong Kong markets closed. All major indices, that are open, are in positive territory though, following firm leads from US markets overnight. US futures have continued this positive momentum during today's session, up a further 0.80-0.901% across the major futures.

- Australian stocks are a standout, up over 3.50%, for the strongest daily gain since June 2020.

- Markets were already in positive territory but were aided by the lower than expected RBA hike (25bps versus 50bps expected). The major banks led the move higher (+4%), but consumer related stocks have also gained by 4-5%.

- Tech sensitive markets like the Nikkei 225, Kospi and Taiex are the other strong performers. The Kospi has gained just under 2.50%, while the TWSE is +2% for the session so far. Electronic sub-sectors have led the way following strong tech gains in US markets.

- The authorities may launch the Korean stock stabilization fund this month.

- Gains elsewhere have been lower, but still positive. Indian shares are the next best performer, up over 1.8% in the first part of trading.

OIL: Holding Close To Recent Highs

Brent is holding above $89/bbl, slightly firmer than NY closing levels. WTI is just below recent highs above $84/bbl (last $83.70), consolidating following yesterday's +5% gain. This comes ahead of tomorrow's OPEC+ meeting, which will decide production targets for November.

- As we noted last week, the strong sense is a production cut will be announced, it's just a question of how large it will be. This comes after Q3 saw the largest drop in oil prices since Q1 2020.

- Analysts from Goldman Sachs and ANZ have stated a cut of more than 1 million bpd could be realized. This is what RBC stated as a risk last week.

- Such a move, in terms of its actual impact on the supply/demand balance, may be muted though given a number of OPEC+ countries are already producing their current quota.

- The other focus point will be EU looking to finalize fresh sanctions on Russia, including an oil price cap.

GOLD: Consolidates Just Shy Of $1700

Gold has consolidated post yesterday's 2.37% gain. We last sat around $1697, down from earlier highs above $1700, and -0.20% below NY closing levels. This is line with a modestly stronger USD through the course of today's session.

- Yesterday's daily gain in the precious metal was the strongest since March. We also haven't been above the $1700 level since the first half of September.

- On the topside, the 50-day comes in at $1724, which we have spent very little time above since April of this year.

- On the downside, recent highs around the $1685/88 region could offer some support.

- Gold continues to follow broader USD sentiment for the most part. The overnight pull back in US real yields (10yr to 1.43% from 1.68% on Friday) aided sentiment.

FOREX: Aussie Depreciates As RBA Raises Cash Rate Target By Less Than Expected

The Aussie dollar depreciated in reaction to the RBA's decision to raise its cash rate target by just 25bp, although most analysts expected it to hike by twice as much, after four straight 50bp moves. The Bank said it expects to keep pushing interest rates higher, while tipping hat to the speed of previously deployed tightening and the deteriorating global conditions. Failure to tighten monetary conditions by the expected increment put a firm bid into ACGBs, while market pricing surrounding the terminal rate shifted lower.

- AUD/USD bounced off its post-RBA lows ($0.6451) amid apparent profit-taking, but the recovery proved short-lived. The rate now hovers just above its worst levels of the day. The kiwi retreated on trans-Tasman contagion, becoming the second-worst G10 performer.

- Selling pressure hit AUD/NZD in sync with a sharp move lower in Australia/New Zealand 2-year swap spread. The RBNZ is broadly expected to raise its key policy rate by 50bp at its interim monetary policy review tomorrow.

- North Korea fired an intermediate-range ballistic missile (IRBM) over Japan, triggering an alert system which issued "duck-and-cover" warnings in some less populated areas for the first time since 2017. The yen posted a negligible uptick, but USD/JPY appreciated as the session progressed, approaching the Y145.00 mark, seen as the threshold of heightened intervention risk.

- Focus turns to U.S. factory orders & final durable goods orders, as well as comments from Fed's Logan, Williams, Mester, Jefferson & Daly and ECB's Lagarde, de Cos & Centeno.

FX OPTIONS: Expiries for Oct4 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9645-55(E2.1bln), $0.9700(E835mln), $0.9750(E830mln), $0.9800-05(E679mln)

- USD/JPY: Y142.00($546mln), Y145.00($562mln)

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 04/10/2022 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 04/10/2022 | 0900/1100 | ** |  | EU | PPI |

| 04/10/2022 | - | | EU | ECB de Guindos at ECOFIN Meeting | |

| 04/10/2022 | 1255/0855 | ** |  | US | Redbook Retail Sales Index |

| 04/10/2022 | 1300/0900 | | US | Dallas Fed's Lorie Logan | |

| 04/10/2022 | 1315/0915 | | US | Cleveland Fed's Loretta Mester | |

| 04/10/2022 | 1400/1000 | ** | | US | factory new orders |

| 04/10/2022 | 1400/1000 | ** | | US | JOLTS jobs opening level |

| 04/10/2022 | 1400/1000 | ** | | US | JOLTS quits Rate |

| 04/10/2022 | 1500/1700 | | EU | ECB Lagarde Q&A with Students Event | |

| 04/10/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 04/10/2022 | 1545/1145 | | US | Fed Governor Philip Jefferson | |

| 04/10/2022 | 1700/1300 | | US | San Francisco Fed's Mary Daly | |

| 05/10/2022 | 2200/0900 | * |  | AU | IHS Markit Final Australia Services PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.