Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- CHINA SERVICES EXPANSION PICKS UP TO STRONGEST IN 10 MONTHS - BBG

- JAPAN MARCH NEGATIVE REAL WAGE NARROWS TO -0.7% - MNI BRIEF

- RBA WARNS AGAINST RELIANCE ON MONTHLY CPI PRINT - MNI BRIEF

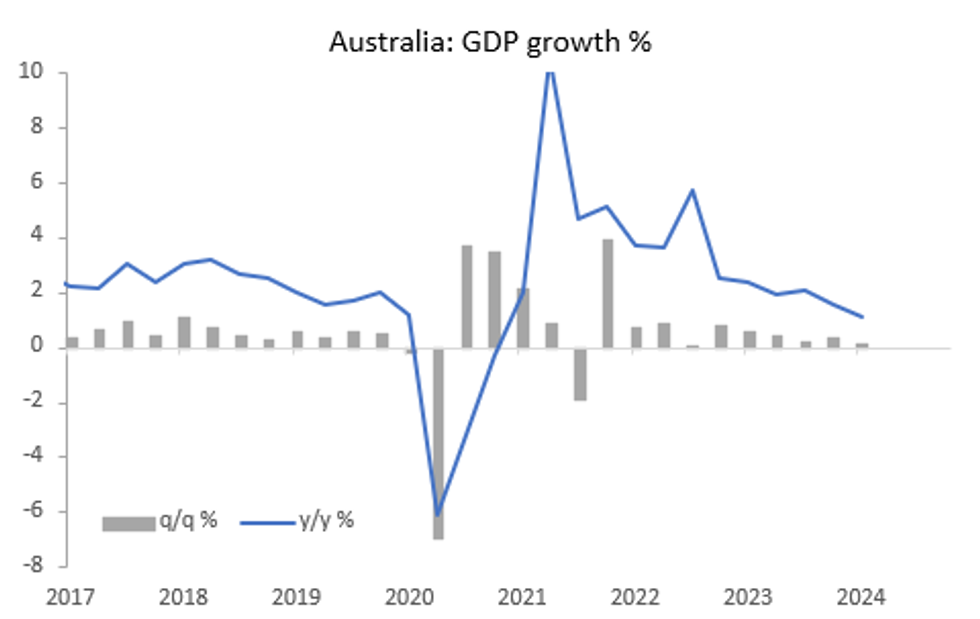

- AUSSIE Q1 GDP PRINTS AT 0.1% Q/Q - MNI BRIEF

Fig. 1: Australian GDP Growth

Source: MNI - Market News/Bloomberg

UK

POLITICS (RTRS): British Prime Minister and Conservative Party Leader Rishi Sunak won the first televised election debate by a wafer thin margin, a YouGov snap poll for Sky News showed on Tuesday. The poll showed 51% thought Sunak performed better, compared to 49% for his Labour Party rival Keir Starmer.

EUROPE

EU (BBG): Chancellor Olaf Scholz said Germany would only support European Commission President Ursula von der Leyen for a second term if her center-right European People’s Party can build a stable majority in the next European Parliament without support of the far right.

EU/CHINA (YICAI): Minister of Commerce Wang Wentao hopes Madrid can encourage the EU to maintain a rational and open attitude in the field of green new energy, in comments made to Spanish counterparts recently. The minister stressed EU concerns over excess capacity and market distortions stemmed from “excess anxiety” and a “distorted mentality”.

EU/CHINA (MNI INTERVIEW): MNI discusses Euro firms' market access into China --On MNI Policy MainWire now.

UKRAINE (FRANCE24): French President Emmanuel Macron will host Ukraine's leader Volodymyr Zelensky on Friday in Paris for talks on the war-battered nation's needs, the Elysee palace announced.

RUSSIA (FRANCE24): French military instructors training soldiers in Ukraine would be a "legitimate target" for Russian strikes, Moscow's top diplomat said Tuesday, amid reports France could send trainers to the country.

US

LABOUR MARKET (MNI INTERVIEW): U.S. job growth appears to have slowed in May but the labor market and wages are likely to remain too hot this year for the Federal Reserve, preventing it from lowering borrowing costs, Toby Dayton, head of job market data firm LinkUp, told MNI.

US/MEXICO (RTRS): U.S. President Joe Biden on Tuesday instituted a broad asylum ban on migrants caught illegally crossing the U.S.-Mexico border, a major enforcement move in the run-up to November elections that will decide control of the White House.

USD (RTRS): The dollar's relentless strength in the recent past will make way for minor weakness over the next 12 months, according to FX strategists in a Reuters poll, who generally agreed the dollar was overvalued.

OTHER

MIDEAST (RTRS): Hamas cannot agree to any deal unless Israel makes a "clear" commitment to a permanent ceasefire and a complete withdrawal from the Gaza Strip, a senior official from the Palestinian militant group said on Tuesday.

JAPAN (MNI BRIEF): The year-on-year drop of inflation-adjusted real wages, a barometer of households' purchasing power, narrowed to 0.7% in April from a 2.1% fall in March, preliminary data released by the Ministry of Health, Labour and Welfare on Wednesday showed.

AUSTRALIA (MNI BRIEF): The Reserve Bank of Australia Governor Michele Bullock has warned against focusing too heavily on volatile monthly inflation reads, noting June’s quarterly print will offer a far more comprehensive view on the direction of prices.

AUSTRALIA (MNI BRIEF): The Australian economy grew 0.1% in the March quarter, 10 basis points less then expected, while household spending rose 0.4% q/q, according to the National Accounts published by the Australian Bureau of Statistics Wednesday.

THAILAND (BBG): Thai Prime Minister Srettha Thavisin’s administration is discussing ways to exert more control over the country’s central bank after repeatedly clashing with the monetary authority on economic policy, according to people familiar with the matter.

BRAZIL (MNI BRIEF): Brazil should aim for economic growth combined with falling inflation, Economy Minister Fernando Haddad told a press conference in Rome on Thursday in which he said that Q1’s 0.8% GDP growth was in line with government projections.

CANADA (MNI BRIEF): Vancouver home sales dropped 20% in May from a year ago while the number of properties listed for sale climbed almost 50%, reflecting the transition between the Bank of Canada's 10 rate hikes through last year and reductions that could start at Wednesday's meeting.

CHINA

SERVICES (BBG): China’s services sector expanded at its fastest pace since July last year, a private survey showed, pointing to resilience that may alleviate concerns over the economy’s outlook after weak official figures.

EQUITIES (SECURITIES TIMES): More listed companies have been issued warnings under stringent new delisting rules aimed at promoting the high-quality development of the A-share market, Securities Times reported.

NEVS (ECONOMIC INFORMATION DAILY): Chinese consumers’ willingness to buy NEVs has significantly increased, driven by a policy encouraging trade-ins, the Economic Information Daily reported, citing salespeople, consumers and experts.

CHINA MARKETS

MNI: PBOC Net Drains CNY248 Bln Via OMO Weds; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY2 billion via 7-day reverse repo on Wednesday, with the rates unchanged at 1.80%. The operation has led to a net drain of CNY248 billion after offsetting the CNY250 billion maturity today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.8025% at 09:29 am local time from the close of 1.7870% on Tuesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 47 on Tuesday, compared with the close of 48 on Monday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1097 on Wednesday, compared with 7.1083 set on Tuesday. The fixing was estimated at 7.2421 by Bloomberg survey today.

MARKET DATA

AUSTRALIA 1Q GDP RISES 0.1% Q/Q; EST. +0.2%; PRIOR +0.3%

AUSTRALIA 1Q GDP RISES 1.1% Y/Y; EST. +1.2%; PRIOR +1.6%

AUSTRALIA JUDO BANK MAY COMPOSITE PMI 52.1; APRIL 53

AUSTRALIA JUDO BANK MAY SERVICES PMI 52.5; APRIL 53.6

NEW ZEALAND 1Q TERMS OF TRADE RISES 5.1% Q/Q; EST. +3.2%; PRIOR -7.8%

NEW ZEALAND 10-MONTH BUDGET DEFICIT NZ$6.51B - BBG

NEW ZEALAND 10-MONTH BUDGET DEFICIT IS NZ$1.71B NARROWER THAN FORECAST

JAPAN APRIL LABOR CASH EARNINGS RISE 2.1% Y/Y; EST. +1.8%; PRIOR +1.0%

JAPAN APRIL CASH WAGES FROM SAME SAMPLE +1.7% Y/Y%; EST. +2.1%; PRIOR +1.9%

JAPAN APRIL SAME BASE REGULAR FULL-TIME PAY +2.1% Y/Y; EST. +2.1%; PRIOR +2.1%

JAPAN APRIL REAL CASH EARNINGS FALL 0.7% Y/Y; EST. -0.9%; PRIOR -2.1%

JAPAN JIBUN BANK MAY SERVICES PMI 53.8; APRIL 54.3

JAPAN JIBUN BANK MAY COMPOSITE PMI 52.6; APRIL 52.3

CHINA MAY CAIXIN SERVICES PMI 54.0; APRIL 52.5

CHINA MAY CAIXIN COMPOSITE PMI 54.1; APRIL 52.8

SOUTH KOREA 1Q GDP EXPANDS 1.3% Q/Q, PRE +1.3% Q/Q; Q4 +0.5%

SOUTH KOREA 1Q GDP EXPANDS 3.3% Y/Y, PRE +3.4%; Q4 +2.1%

MARKETS

US TSYS: Tsys Futures Off Morning Highs, Ranges Tight Ahead Of ADP Emply Data

- Treasury futures have done very little today, ranges have been tight. TU is trading at 102-02+ vs morning highs of 102-03.375. TY saw earlier buying at 110-00 to 110-00+ area, although we trade off those levels now down -02 at 109-30+.

- Volumes: TU 46k, FV 64k, TY 101k

- Tsys Flow: Block Buyer FV at 106-16.75, while there was TYN4 Option structure blocked, 3 strikes of calls and a put. Calls 10k 109/109.5/110.25, Put 10k 108.75

- The 5-10y tenors have been the best performing part of the curve over the past week with the 10y yield has rallying 30bps in the past four trading sessions. Rate cut projections continue to gain, while the BBG Surprise Index reaches multi year lows - See Chart 1.

- Cash treasuries are 1-2bp higher, the 2Y +1.2bps to 4.783%, the 10Y +1.6bps at 4.342%, 2s10s is +0.114 at -44.342

- APAC Rates: ACGB yields are 4-8bps lower, curve flatter. NZGB yields 3-7bps lower, with better buying through the belly, JGB yields a 1-4bps lower, with the 10Y -2.6bps and back below 1% at 0.993%

- Late year rate cut projections continue to gain vs. late Monday levels (*): June 2024 at -1.3% w/ cumulative rate cut -.3bp at 5.328%, July'24 at -16% w/ cumulative at -4.3bp at 5.288%, Sep'24 cumulative -19.3bp (-17.2bp), Nov'24 cumulative -27.8bp (-25.3bp), Dec'24 -44.3bp (-40.6bp).

- Looking ahead; MBA Mortgage Applications, ADP Employment Change, S&P Global US PMI & ISM Services Index

Source - BBG

JGBS: Futures Richer & At Session Highs, BoJ Nakamura Speech & 30Y Supply Tomorrow

JGB futures are sharply higher and at session highs, +41 compared to the settlement levels.

- Outside of the previously outlined Labour and Real Cash Earnings and Jibun Bank PMIs, there hasn't been much in the way of domestic drivers to flag.

- (Dow Jones) Japan labour survey data for April confirms that the gradual increase in wage growth continues, ING economists say. "We expect real wage growth to turn positive by June, giving the BoJ more confidence for another rate hike," Robert Carnell and Min Joo Kang say. ING now expects a 15bp BOJ rate hike in July.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session. The US calendar today will see MBA Mortgage Applications, ADP Employment Change and S&P Global US PMI & ISM Services Index.

- Cash JGBs are richer across benchmarks, with yields flat (1-year) to 4.4bps lower (5-year). The benchmark 10-year yield is 3.3bps lower at 0.997% versus the cycle high of 1.101% set last week.

- Swaps are richer apart from the 20-30-year zone, with rates 2bps lower to 2bp higher. Swap spreads are mostly wider.

- Tomorrow, the local calendar will see Weekly International Investment Flow and Tokyo Avg Office Vacancies data along with a speech from BoJ Board member Nakamura in Sapporo. The MoF also plans to sell Y900mn of 30-year JGBs.

AUSSIE BONDS: Richer, RBA Bullock Neutral, Q1 GDP Miss, Productivity Stalled

ACGBs (YM +4.0 & XM +7.5) are richer but have retreated from the Sydney session's best levels. Following a positive lead from US tsys, the domestic market focused on two key events today.

- RBA Governor Bullock remained neutral in her Senate testimony and reiterated the Board’s stance of not “ruling anything in or out” and that policy is “restrictive”.

- Q1 GDP rose 0.1% q/q, the slowest quarterly rate since Q3 2022. Economic growth slowed to 1.1% y/y from 1.6%, the lowest since Q4 2020 and excluding Covid Q1 1992. Imports and investment were a drag on the economy while government and private consumption plus inventories made solid contributions. The RBA was expecting a weak outturn and so this data is unlikely to change its current on-hold stance.

- After two straight quarters of growth, productivity improvements stalled in Q1. GDP per hour worked was flat on the quarter and compared to a year ago but that was up on Q4’s -0.4% y/y.

- Cash ACGBs are 5-7bps richer, with the AU-US 10-year yield differential at -10bps.

- Swap rates are 5-6bps lower, with the 3s10s curve flatter.

- The bills strip has bull-flattened, with pricing flat to +6.

- RBA-dated OIS pricing is 3-5bps softer for meetings beyond September.

- Tomorrow, the local calendar will see Home Loans Value and Trade Balance data.

NZGBS: Closed Mid-Range, Richer, US ADP Data Later Today

NZGBs closed in the middle of the session’s range, 3-6bps richer across benchmarks.

- Outside of the previously outlined Terms of Trade and the Government’s 10-month Financial Statements, there hasn't been much in the way of domestic drivers to flag.

- The move away from the session’s best levels aligns with a ~1bp cheapening in cash US tsys in today’s Asia-Pac session ahead of the release of ADP Private Employment data later today.

- Swap rates closed 2-6bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed 1-4bps softer for meetings beyond August. A cumulative 24bps of easing is priced by year-end.

- Tomorrow, the local calendar will see May CoreLogic House Prices, Q1 Volume of All Buildings and May ANZ Commodity Price data.

- Today, the NZ Treasury launched the syndicated tap of May 2028 nominal bonds, seeking at least NZ$2bn this week. Transaction will be capped at NZ$4bn and priced tomorrow. Initial guidance 3-6 bps under April 2027 nominal bond. The June 6 bond auction is cancelled.

FOREX: Yen Unwinds Some Of Tuesday's Bounce, A$ & NZD Slightly Higher

The BBDXY USD index sits little changed, last near 1252.65. This has masked some divergences within the G10 space though. Most notable has been yen unwinding some of Tuesday's outcomes.

- USD/JPY sits back near 155.50, around 0.40% weaker in yen terms and close to session highs. We had mixed April wages data, with better headline results (boosted by annual wage outcomes of +5%), but the same sample basis was softer than forecast (see this link).

- For the FX pair we still remain comfortably off earlier Tuesday highs near 156.50. US yields are up a little over 1bps, while US equity futures sit higher.

- AUD and NZD are firmer against the USD by around 0.15%/ AUD/USD last at 0.6660, NZD/USD near 0.6185.

- We had a better than expected Caixin services PMI print in China, although follow through has been limited in terms of risk appetite. China equities are lower and HK markets sits comfortably off earlier highs.

- AUD/JPY sits just off session highs, last near 103.55/60. Earlier highs this week were above 104.70. Australian Q1 GDP was slightly below expectations (0.1% q/q, versus 0.2% projected), although private consumption proved more resilient than expected.

- Looking ahead, US ADP, the BOC and ISM Services are coming up. The ECB decision on Thursday and NFP Friday remain key event risks for the remainder of the week.

ASIA STOCKS: HK Equities Outperform Although Off Earlier Highs, China PMI Jumps

Hong Kong & Chinese equities are mixed today, with Hong Kong markets outperforming for the second straight session after a weak US jobs reading increased the hopes for a Federal Reserve interest rate cut. China Caixin PMI grew at the fastest growth in 10 months

- Hong Kong equities are higher today although well of morning highs, tech stocks are the top performers today with the HSTech Index up 0.80% and now trading back above all major EMAs. Property Indices are now lower for the day with the Mainland Property Index down 1.10%, the HS Property Index down 0.60%, the wider HSI is up 0.33%.

- China equites have underperformed today, the CSI300 is now down 0.20% with small-cap indices the CSI1000 and CSI2000 are down 0.30% and 1.10% respectively, the CSI300 Real Estate Index is off 1.80% while the growth focused ChiNext Index is up 0.12%

- Data: Hong Kong S&P Global PMI was 49.2 in May dropping from 50.6 in April, while China Caixin PMI composite for May was 54.1 up from 52.8 in April, and Services PMI was 54.0 vs 52.5 est.

- In the property space, DaFa Properties group have had their wind-up hearing adjourned until June 24.

- (MNI): MNI China Press Digest June 05: A-shares, EU-China, SOEs (See link)

- Looking ahead: Tomorrow we have China Trade Balance data.

ASIA PAC STOCKS: Equities Mixed, Japan Equities Lower On Higher Yen, AU & SK GDP Miss

Asian equities are mixed today, Japan is the worst performing region as the yen strengthens and hurts export names, while other markets edge higher on hopes of a fed rate cut. The Philadelphia Semiconductor index was 0.70% lower overnight, although news that Nvidia is working to certify Samsung's AI memory chips has seen Samsung rally about 3% this morning and helped other region semiconductor names. Indian equity markets have stabilized after selling off over 5% on Tuesday as election results look to be much closer than expected. Earlier, SK & Australian GDP came in just below estimates.

- Japanese equities are lower today, the yen is off overnight highs, but still 1.46% higher over the past week. Earlier, Labor Cash Earnings were 2.1% vs 1.8%, while Jibun Bank Japan PMI Composite was 52.6 vs 52.4 prior and Services were 53.8 vs 53.6. The Topix is down 1.47% and now testing the 20-day EMA support at 2,750, The Bank Index is down 2.29%, while the Nikkei 225 is down 1.12%

- Taiwan equities have edged higher throughout the day, the local market has seen the majority of outflows in the region, with another $528m outflows on Tuesday. Looking ahead we have CPI on Thursday. The Taiex is up 0.50%.

- South Korean equities have gained on fed rate cut expectation gains and Samsung rallying on the back of news that Nvidia is working to certify their AI memory chips. Earlier, GDP came in slightly below consensus at 3.3% vs 3.4%. The Kospi is up 1.20% and now testing the 20-day EMA resistance at 2,690, while the Kosdaq is up 0.47%.

- Australian equities are slightly higher today, Banking stocks are the top performing sector today, while metals and mining underperform. Earlier Judo Bank PMI showed a slightly decline, with composite at 51.1 vs 52.6 prior and services 52.5 vs 53.1 prior, while GDP came in below consensus at 1.1% y/y vs 1.2% est. The ASX200 is 0.38% higher.

- Elsewhere in SEA, New Zealand Equities are 1% higher, Singapore equities are 0.25% higher, Indonesian equities are down 1%, Philippines equities are down 0.10% after CPI came in below consensus at 3.9% vs 4% est, Malaysian equities are 0.20% lower, while Indian equities have found some support after the 5% sell-off on Tuesday and trade little changed today.

OIL: Crude Steady, EIA US Inventory Data Out Later

Oil prices are little changed during APAC trading today after falling for the last few days after OPEC decided on the weekend to reduce output cuts from October, which was earlier than expected. Higher US stockpiles have not put further downward pressure on crude today. WTI is around $73.21/bbl after a high of $73.34 and Brent is $77.52/bbl after reaching $77.64 and both benchmarks are down around 5% this week. The USD index is slightly higher.

- Oil prices are likely to face headwinds through 2024 as demand from China is looking soft and the Fed may not cut rates until year end pressuring US demand. There is also strong supply from non-OPEC countries and increased output from OPEC+ in Q4 will add to that, but the group may change its plan to reduce production cuts if prices look weak.

- Bloomberg reported a 4.1mn barrels crude inventory build in the US compared with a 6.5mn drawdown the previous week according to people familiar with the API data. Gasoline rose 4.0mn barrels and distillate 2mn. The official EIA data is released later today.

- Later US May ADP employment, final May US & European composite/services PMIs/ISM, euro area April PPI and the Bank of Canada decision are released. The focus for the oil market now the OPEC meeting is behind it will be Friday’s US May payrolls and the June 12 Fed decision.

GOLD: Weaker Despite Softer US Labour Market Data

Gold is 0.4% higher in the Asia-Pacific session, after closing 1% lower at $2327.01 on Tuesday.

- Tuesday’s move came despite softer US labour market data. JOLTS Job Openings printed 8.059M vs. 8.350M est and 8.488M prior. The result was the lowest since Feb 2021.

- US Treasuries rallied for the fourth successive day, although they finished slightly off session highs amid late position squaring ahead today’s ADP private employment data risk, a precursor to Friday's headline employment report.

- Silver underperformed, falling by ~4.0%, its lowest level since May 17. Silver is now trading within a key support zone between $30.116 - 28.494, the 20- and 50-day EMA values, according to MNI’s technicals team.

- (Bloomberg) UBS Group AG sees gold hitting $2,800 an ounce over the next two years, with continued macro uncertainty and geopolitical risks set to drive continuing strong demand from global central banks. (See link)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 05/06/2024 | 0645/0845 | * |  | FR | Industrial Production |

| 05/06/2024 | 0900/1100 | ** |  | EU | PPI |

| 05/06/2024 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 05/06/2024 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 05/06/2024 | 1215/0815 | *** | | US | ADP Employment Report |

| 05/06/2024 | 1345/0945 | *** |  | CA | Bank of Canada Policy Decision |

| 05/06/2024 | 1400/1000 | *** | | US | ISM Non-Manufacturing Index |

| 05/06/2024 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 05/06/2024 | 1430/1030 | | CA | BOC Governor Press Conference |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.