Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- BIDEN, TRUMP CLINCH NOMINATIONS, KICKING OFF BRUISING PRESIDENTIAL REMATCH - RTRS

- ECB’s VILLEROY SEES BROAD AGREEMENT ON SPRING CUT - MNI BRIEF

- JUNE CUT NOT DONE DEAL - ECB'S HOLZMANN - MNI INTERVIEW

- TOYOTA AGREES TO BIGGEST WAGE HIKE IN 25 YEARS IN SIGN OF JAPAN INC'S BIG PAY BUMP - RTRS

- HAINAN BONDS TO FUND WORLD'S LARGEST FREEPORT - MNI INTERVIEW

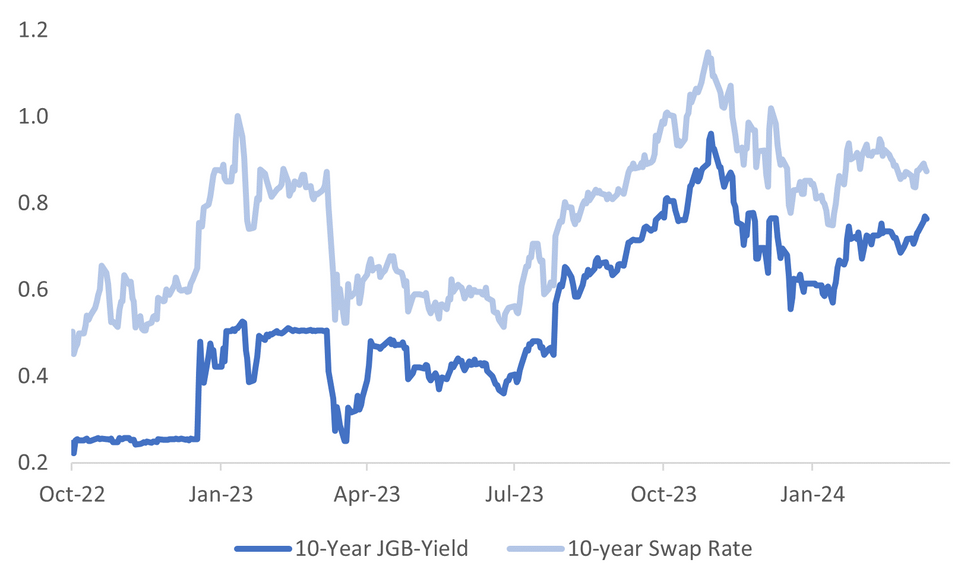

Fig. 1: Japan 10yr JGB Yield & 10yr Swap Rate

Source: MNI - Market News/Bloomberg

U.K.

BOE (MNI BRIEF): Bank of England Governor Andrew Bailey noted Tuesday some encouraging signs that the inflation shocks from Covid re-opening and the Russian invasion of Ukraine have not de-anchored inflation expectations, making him less concerned about second round effects.

EUROPE

ECB (MNI BRIEF): Bank of France Governor Francois Villeroy said Tuesday there is very “broad agreement” in the ECB Governing Council for a rate cut in the spring, pointing out the season lasts until June 21.

ECB (MNI INTERVIEW): The European Central Bank is more likely to cut rates in June than April, but cuts will depend on inflation projections being confirmed, the governor of the Austrian National Bank told MNI in an interview, stressing that wage data and geopolitical risk are key and that the ECB should remain data-dependent.

ECB (BBG): European Central Bank Governing Council member Pierre Wunsch reiterated that policymakers will eventually have to lower borrowing costs without being completely sure that inflation is returning to the 2% target. At some point, “we’ll have just to say, okay, we believe it’s going to work and we’re going to take a decision and I don’t think it’s going to be, you know, before so long,” the Belgian central bank chief said.

POLAND (BBG): Polish President Andrzej Duda said Russian President Vladimir Putin will attack other states if the Kremlin wins its war in Ukraine as he sought to convince the US to approve further assistance for Kyiv.

RUSSIA (BBG): President Vladimir Putin said Russia would demand security guarantees to consider talks to end the war in Ukraine, telling a state news agency that “realities on the ground” should be the basis of any negotiation

ITALY (BBG): Giorgia Meloni’s government is demanding that a bigger share of investments made by chipmaker STMicroelectronics NV go to Italy, the latest sign of tension over business ties with France.

U.S.

POLITICS (RTRS): President Joe Biden won enough delegates on Tuesday to seal the Democratic Party's nomination, with a face-off against former President Donald Trump looming in what would be the first U.S. presidential election rematch in nearly 70 years.

FISCAL (MNI BRIEF): The U.S. government has racked up a USD828 billion budget deficit in the first five months of fiscal year 2024, up USD105 billion dollars relative to the same time period in the previous fiscal year, the Treasury Department reported Tuesday.

US/CHINA (BBG): “We’ll always stand against China’s unfair practices — and as long as I am president, I’ll fight for US workers and jobs,” President Biden says in a post on social media platform X.

OTHER

BRAZIL (MNI POLICY): Details of February’s Brazilian inflation data, showing an easing of services inflation, are likely to strengthen the case of those on the central bank’s monetary policy committee (Copom) who argue that wage rises are not feeding inflationary pressures, MNI understands.

JAPAN (RTRS): Toyota Motor agreed to give factory workers their biggest pay increase in 25 years on Wednesday, heightening expectations that bumper pay raises will give the central bank leeway to make a key policy shift next week.

JAPAN (BBG): A wide range of unions are poised to release results from negotiations, with the Japanese Association of Metal, Machinery and Manufacturing Workers saying Wednesday that 60 affiliated unions secured an average pay increase of 5.32%, exceeding last year’s tally by a large margin.

JAPAN (BBG): RBC BlueBay Asset Management has made selling Japanese government bonds a top wager on expectations the central bank is likely to raise interest rates next week.

AUSTRALIA (BBG): Australian vinters and lawmakers said China proposed lifting punitive tariffs on the nation’s wine, signaling the end is near to a three-year trade dispute as both countries seek to strengthen ties.

THAILAND (BBG): Thailand’s Prime Minister Srettha Thavisin will relinquish his role as finance minister in a soon-to-be effected cabinet reshuffle that may burnish his government’s image amid clashes with the central bank on monetary policy, according to a local media report.

CHINA

DEBT (MNI INTERVIEW): China plans to invest hundreds of billions of yuan in building up the world’s largest free-trade port in Southeast Hainan by 2025 and aims to pay for much of it with local government bond sales at home and abroad, a high-ranking provincial official told MNI, adding that authorities will closely monitor the use of the funds as risk management is now being prioritised over stimulating GDP growth.

TRADE (MNI INTERVIEW): China will use Hainan as a testing ground for the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) trade rules before it considers rolling them out across the country, the head of the province’s fiscal department told MNI.

PBoC (Economic Information Daily): The People’s Bank of China will likely cut the reserve requirement ratio and the medium-term lending facility rate in Q2, said Wang Qing, chief macro analyst at Golden Crediting Rating. PBOC Governor Pan Gongsheng signaled further RRR cuts last week after pointing out the current 7% average.

PROPERTY (BBG): Country Garden Holdings Co. missed a coupon payment on a yuan bond for the first time, according to people familiar with the matter, adding to the woes of the Chinese developer that is now facing a lawsuit seeking its liquidation offshore.

ECONOMY (21st Century Business Herald): Policymakers should expand support of new productive forces to include new types of business models and demand behaviours, according to Liu Zhongfan, member of the Standing Committee of the CPPCC National Committee. Liu said developing new productive forces will need institutional reforms to enhance integration between the science and innovation sector with the wider economy and industry. Officials need to protect the intellectual property value of researchers, Liu added. (Source: 21st Century Business Herald)

LGFV (BBG): Chinese local government financing vehicles are turning to more diverse fixes for spiraling debt, trying to avoid becoming the first such entity to default in public markets as their borrowing habits become a top economic agenda in Beijing.

CHINA MARKETS

MNI: PBOC Drains Net CNY7 Bln Via OMO Weds; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY3 billion via 7-day reverse repo on Wednesday, with the rates unchanged at 1.80%. The reverse repo operation has led to a net drain of CNY7 billon after offsetting CNY10 billion maturity today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8661% at 09:33 am local time from the close of 1.8696% on Tuesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 46 on Tuesday, compared with the close of 45 on Monday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.0930 on Wednesday, compared with 7.0963 set on Tuesday. The fixing was estimated at 7.1769 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND FEB FOOD PRICES M/M -0.6%; PRIOR 1.2%

AUSTRALIA FEB CBA HOUSEHOLD SPENDING M/M -0.3%; PRIOR 3.2%

AUSTRALIA FEB CBA HOUSEHOLD SPENDING Y/Y 3.5%; PRIOR 3.8%

SOUTH KOREA FEB UNEMPLOYMENT RATE SA 2.6%; MEDIAN 3.0%; PRIOR 3.0%

SOUTH KOREA FEB BANK LENDING TO HOUSEHOLDS 1100.3T; PRIOR KR1098.4T

MARKETS

US TSYS: Treasury Futures Steady, Trade In Tight Ranges Ahead Of 30Y Auction

- Jun'24 10Y futures are having another very quiet Asia trading session, ranges have remained very tight hitting lows on the open of 111-06, highs of 111-08+ and now trade right in the middle at 111-07+, +02 for the day.

- Looking at technicals, initial supports holds at 111-03+ (20-day EMA), below there 110-21 (Mar 4 low), to the upside, initial resistance is 112-04+ (Mar 8 highs) while above is 112-10+ (61.8% retracement of the Feb 1 - 23 bear leg)

- Cash yields are have slghly bull-flattened with the 2Y +0.4bp to 4.590%, 10Y -0.4bp to 4.147%, while the 2y10y is -0.797 at -44.557

- Looking ahead: Mortgage Applications and a Treasury bond sales the main focus is on Thursday's Retail Sales and PPI data.

JGBS: Choppy Session, Corporate Wage Outcomes Crossing, 20Y Supply Tomorrow

JGB futures are holding a downtick, -2 compared to the settlement levels, after a choppy Tokyo session.

- Today, the local calendar has been empty.

- However, several headlines have crossed today from a variety of Japanese companies and organizations outlining agreements made with unions on this year's wage demands. For the most part companies are stating that wage demands are being met in full. Headlines from industry heavyweight Toyota was one of the first to cross.

- Local media reported yesterday that if wage gains are 'significantly' above last year's 3.8% it will prompt a BoJ exit from NIRP. Still, a shift in March from the BoJ is by no means a sell-side consensus viewpoint at this stage.

- Cash US tsys are dealing ~1bp richer in today’s Asia-Pac session after yesterday’s 5-6bps cheapening following February’s US CPI print. Looking ahead, the main focus is on Thursday's Retail Sales and PPI data.

- Cash JGBs are slightly mixed, with yield movements bounded by +/- 1bp. The benchmark 10-year yield is 0.2bp lower at 0.768% versus the yearly high of 0.779% set yesterday.

- Swaps are slightly richer. Swap spreads are mixed.

- Tomorrow, the local calendar sees weekly International Investment Flow data, along with 20-year supply.

AUSSIE BONDS: Roll-Impacted Dealings, Narrow Ranges, Light Local Calendar Tomorrow

In roll-impacted dealings, ACGBs (YM -7.2 & XM -7.7) are holding weaker and at or near Sydney session lows. Trading ranges have been however relatively narrow.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined CBA Household Spending. This represented the final data update before the forthcoming RBA Policy Decision scheduled for next Tuesday.

- (Bloomberg) -- Australia’s household spending declined in February, the nation’s largest lender said, as the Reserve Bank’s interest-rate increase late last year weighed further on consumer activity. (See link)

- Cash US tsys are dealing ~1bp richer in today’s Asia-Pac session after yesterday’s 5-6bps cheapening following February’s US CPI print. Looking ahead, the main focus is on Thursday's Retail Sales and PPI data.

- Cash ACGBs are 7-8bps cheaper, with the AU-US 10-year yield differential 2bps higher at -12bps.

- Swap rates are 7-8bps higher.

- The bills strip has bear-steepened, with pricing -2 to -8.

- RBA-dated OIS pricing is flat to 5bps firmer across meetings, with late-24 leading. A cumulative 44bps of easing is priced by year-end.

- Tomorrow, the local calendar is empty.

NZGBS: Closed On A Weak Note, Net Migration Data & RBNZ Conway Speech Tomorrow

NZGBs closed on a weak note, with benchmark yields 4bps higher. With the domestic calendar light, local participants appear to have been content to follow the weak overnight lead from US tsys following hotter-than-expected US CPI data.

- NZGBs have matched their $-bloc counterparts today, after yesterday’s underperformance, with the NZ-US and NZ-AU 10-year yield differentials unchanged.

- Cash US tsys are dealing ~1bp richer in today’s Asia-Pac session after yesterday’s 5-6bps cheapening following February’s US CPI print. Looking ahead, the main focus is on Thursday's Retail Sales and PPI data.

- Swap rates closed 3bps higher.

- RBNZ dated OIS pricing is slightly firmer across meetings. A cumulative 63bps of easing is priced by year-end.

- Tomorrow, the local calendar sees Net Migration data, along with a speech from RBNZ Chief Economist Conway at a Kiwibank event.

- Tomorrow, the NZ Treasury plans to sell NZ$275mn of the 0.25% May-28 bond and NZ$225mn of the 2% May-32 bond.

FOREX: Yen Gains Pared Despite Signs Of Strong Wage Momentum

The USD BBDXY Index sits little changed for the Wednesday session so far, last near 1230.75. Overall ranges have been fairly tight in the FX space, with JPY, AUD and NZD all moderately higher at this stage.

- USD/JPY has again been a focus point, spending the first part of the session drifting lower. We hit session lows of 147.24, not long after headlines crossed that Toyota had agreed to the full union demands around this year's wage negotiations. Similar headlines from other major corporates followed.

- Wages momentum appears to be building, and recall local media reported yesterday that if wage gains are 'significantly' above last year's 3.8% it will prompt a BoJ exit from NIRP. Still, a shift in March from the BoJ is by no means a sell-side consensus viewpoint at this stage.

- Prevailing sentiment indicates a 60-70% probability of a move occurring in Mar/Apr, with 100% priced by June, based off market pricing.

- USD/JPY has firmed this afternoon, back to 147.55/60. Note there is an option expiry for NY cut close to session lows from earlier - Y147.25-35($1.6bln), which may have influence market price action.

- AUD and NZD have drifted higher with NZD outperforming modestly. Secon tier data outcomes didn't impact sentiment for either FX rate. NZD/USD was last near 0.6160, up around 0.20%, while AUD has edged above 0.6610.

- These moves come despite equity sentiment being mixed throughout the region, while iron ore prices are down sharply further. This may have helped curb AUD/NZD gains, with the cross back to 1.0730/35, against earlier highs near 1.0750.

- Looking ahead, we have UK data first up, headlined by monthly GDP, while crude stocks and a 30yr bond sale will be the focus in the US Session.

ASIA PAC EQUITIES: Equities Mixed, Higher Wages & Stronger Yen Hurts Japan Equities

Asian equities markets are mixed as Japanese equities opened higher but turned negative due to yen strength following reports of Toyota meeting union demands to raise wages, causing speculation about a potential BoJ exit from NIRP. In South Korea, efforts to eliminate the "Korea Discount" are highlighted, with the Kospi just 0.05% higher; Taiwan plans measures to prevent irrational buying, and its equity market is unchanged after being up as much as 1.00%. Australian equities are slightly higher, with the ASX200 up 0.16%, while New Zealand's market closes down 0.17%. In Southeast Asia, Singapore equities are up 0.60%, Indonesia trades 0.30% higher after a two-day break, the PSEi in the Philippines is the top performer, up 1.30%, and Malaysia is the worst performer, down 0.96%.

- Japanese equities opened higher this morning but turned negative after strength in the yen. The yen has been strengthening after it was reported that Toyota will meet the union's demands to raise wages, including a bonus of 7.6 months of workers' salaries. It should be noted that Jiji stated that the BoJ would exit NIRP if this year's wage gains were significantly above last year's 3.8%. Since Toyota's announcement, multiple other firms have agreed to raise wages. The BoJ's decision to refrain from purchasing ETFs despite a market decline is fueling speculation that the bank might cease such acquisitions to enhance market health by improving liquidity and reducing price distortion, signaling a potential shift toward policy normalization. Currently, the Topix is down 0.50%, while the Nikkei 225 is down 0.40%.

- South Korean Financial Services Commission Vice Chairman Kim Soyoung said on Tuesday the importance of eliminating the "Korea Discount" by aiming to boost corporate valuations through initiatives encouraging retail investors and companies to utilize equities for wealth creation and capital, with plans to potentially ease taxes on dividend income and upgrade capital markets. Equities markets are mostly unchanged today with the Kospi just 0.05% higher, the top performer has been Samsung electronics which increased 0.70%

- Taiwan is looking to implement measures, such as financial inspections and heightened scrutiny on new ETFs, to prevent irrational buying, along with tighter regulations on marketing and ad campaigns by Internet influencers. The Taiwan equity markets are off earlier highs and the Taiex is now unchanged after being up as much at 1.00%

- Australian equities are slightly higher today, with household spending data showing a decline of 0.3% for the month, well below the prior month's gain of 3.1%. Financials are the top-performing sector, followed by consumer discretionary stocks, offsetting losses in miners. While China has announced earlier that they would lift the tariff imposed on Australian wine, with Treasury Wine Estate trading up 4.00% after the announcement. The ASX200 is 0.16%

- Elsewhere in SEA, NZ equities closed down 0.17% after food price data showed the smallest annual price jump since May 2021. Singapore equities are up 0.60%, Indonesia is back for their two-day break and is trading 0.30% higher and the top performer in the region in is the PSEi up 1.30%, while Malaysia is the worst performer in the region, down 0.96%.

ASIA EQUITIES: Hong Kong Equities Outperforms, China Vanke In Debt Swap Talks

- Hong Kong equities are slightly higher today with the HStech Index the top performer up 0.80%, while property names are down 0.69%, the Country Garden default doesn't seem to have had much of an impact as the Mainland Property Index is up 10.72% since March 7th. Elsewhere the Biotech Index is down 1.44%, while the HSI is up 0.24%. In China, equities indices are mostly lower with the CSI300 down 0.58%, the CSI1000 is up 0.41% while the ChiNext is down 0.42%

- China Northbound flows were 4.2 yuan on Thursday, with the 5-day average at 3.38b, while the 20-day average sits at 3.02b yuan.

- In the property space, China Vanke is reportedly in discussions with banks for a debt swap that could avert its first-ever bond default, involving the conversion of tens of billions of yuan in bond holdings into secured debt. The talks, coordinated by China's financial regulators and the Shenzhen government, are ongoing, with the potential plan subject to change, and Vanke faces liquidity pressure amidst declining property sales and a Moody's credit rating downgrade to junk status. Elsewhere is has been reported that Country Garden onshore bondholders have not received coupon payment due on March 12th. China Garden plans to raise money for the payment within the 30-day grace period.

- Elsewhere, China may cut banks RRR and lower the MLF rate in the second quarter and also offer more pledged supplementary loans to meet capital requirements according to China Chief Economist Forum.

OIL: Higher, But Within Recent Ranges, Focus On US Inventory Data Later

Oil benchmarks remain within recent ranges. Brent (K4), was last near $82.40/bbl, up around 0.6% so far today. This is offsetting Monday's 0.35% fall, but we remain sub recent highs. WTI (J4) was last near $78.05/bbl, up 0.65%, and looking to end a run of four straight session falls for the benchmark. Like Brent though we remain largely range bound.

- OPEC+ supply weighed on sentiment during Tuesday trade. OPEC raised oil output 200,000 bpd to 26.6 mln bpd in February, it also overshot its production target by 200,000 bpd.

- At the margin broader USD strength/higher interest rates post the US CPI print, would have also been a headwind, like elsewhere in the commodity space.

- Some offset has come from reports earlier today that US crude inventories fell last week (see this BBG link for more details). We get official inventory figures in the US later today.

GOLD: Sharp Pullback After US CPI Data

Gold is little changed in the Asia-Pac session, after closing 1.1% lower at $2158.34 following Tuesday’s release of hotter-than-expected US CPI data. Bullion has now shed ~$40/oz off the all-time high posted last Friday.

- USD strength and a return higher for US yields drove price action. US Treasury yields finished 5-6bps higher across benchmarks, with projected rate cut pricing receding as the CPI data was deemed unlikely to provide the FOMC with confidence that inflation will return to 2% in the near term.

- CPI m/m (0.4% vs. 0.4% est), y/y (3.2% vs. 3.1% est); CPI Ex Food and Energy m/m (0.4% vs. 0.3% est) y/y (3.8% vs. 3.7% est). Meanwhile, Real Avg Hourly Earning y/y (1.1% vs. prior 1.3% (rev)).

- According to MNI’s technicals team, a further pullback would encounter first strong support at $2145.40 - the 23.6% retracement for the Feb - Mar up leg. Initial resistance is at $2195.2, the March 8 high.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/03/2024 | 0700/0700 | ** |  | UK | UK Monthly GDP |

| 13/03/2024 | 0700/0700 | ** | | UK | Trade Balance |

| 13/03/2024 | 0700/0700 | ** | | UK | Index of Services |

| 13/03/2024 | 0700/0700 | *** | | UK | Index of Production |

| 13/03/2024 | 0700/0700 | ** | | UK | Output in the Construction Industry |

| 13/03/2024 | 1000/1100 | ** |  | EU | Industrial Production |

| 13/03/2024 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 13/03/2024 | 1145/1245 | | EU | ECB's Cipollone at conference in Milan | |

| 13/03/2024 | - | *** |  | CN | Money Supply |

| 13/03/2024 | - | *** | | CN | New Loans |

| 13/03/2024 | - | *** | | CN | Social Financing |

| 13/03/2024 | 1230/0830 | * |  | CA | Household debt-to-income |

| 13/03/2024 | 1400/1000 | * | | US | Services Revenues |

| 13/03/2024 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 13/03/2024 | 1700/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.