Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- ONE MORE FED HIKE LIKELY, THEN HOLD FOR SOME TIME - MESTER- MNI

- REPUBLICAN GAETZ MOVES TO FORMALLY REMOVE MCCARTHY AS SPEAKER - BBG

- BOE’S MANN SAYS UK INTEREST RATE MAY REMAIN PERMANENTLY HIGH - BBG

- UK STORES CUT FOOD PRICES FOR FIRST TIME IN MORE THAN TWO YEARS - BBG

- RBA HOLDS AT 4.1%, BULLOCK HOLDS STEADY - MNI BRIEF

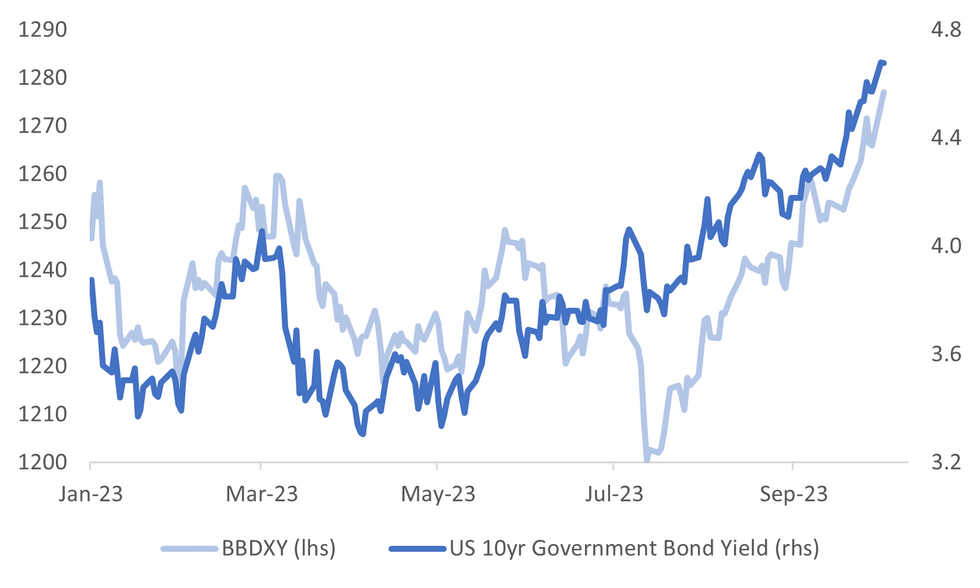

Fig. 1: US Nominal 10-yr Treasury Yield & BBDXY Index

Source: MNI - Market News/Bloomberg

U.K:

BOE: “Bank of England rate-setter Catherine Mann warned against letting up in the fight against inflation as she disparaged the central bank’s forecasts and predicted permanently higher interest rates.” (BBG)

PRICES: “British shoppers enjoyed the first monthly drop in food prices in more than two years as retailers cut the cost of dairy products, fish and vegetables amid “fierce competition” between stores, a survey found.” (BBG)

EUROPE:

FRANCE/GERMANY: “A lack of consensus within the Franco-German tandem that has been at the core of EU decision-making is causing delays in multiple issues — from financing Ukraine to rules overseeing national budgets.” (FT)

UKRAINE: EU foreign ministers expressed support for Ukraine during a meeting in Kyiv on Monday, their first in a non-member country, after a pro-Russian candidate won an election in Slovakia and the U.S. Congress left Ukraine war aid out of its spending bill. (RTRS)

HUNGARY: “The European Commission is preparing to release billions of euros in EU funds to Hungary currently frozen because of rule of law concerns, in a move that could secure Budapest’s support for an increase to the bloc’s budget and significant financial assistance to Ukraine.” (FT)

TECH: “Would people pay nearly $14 a month to use Instagram on their phones without ads? How about nearly $17 a month for Instagram plus Facebook -- but on desktop? That is what Meta Platforms wants to charge Europeans for monthly subscriptions if they don't agree to let the company use their digital activity to target ads, according to a proposal the social-media giant has made in recent weeks to regulators.” (WSJ)

U.S.

FED: A final interest rate hike will likely be needed to boost the fed funds rate to its cycle peak, where it will sit for some time to stabilize prices, Federal Reserve Bank of Cleveland President Loretta Mester said Monday. The FOMC will carefully monitor economic, banking and financial market developments amid "considerable uncertainty" around the outlook so it can set monetary policy in a way that balances the costs of overtightening and under-tightening, she said. The slowdown in the Chinese economy, the possibility of an extended United Auto Workers strike and a potential government shutdown later this year all pose some risks. (MNI)

POLITICS: “Republican Matt Gaetz officially moved to topple House Speaker Kevin McCarthy on Monday evening, teeing up a high-stakes vote likely to dramatically shift the balance of power in Washington whatever the outcome.” (BBG)

POLITICS: “A defiant Donald Trump attacked New York's attorney general and the judge overseeing his civil fraud trial as it began on Monday, with a state lawyer accusing the former president of generating more than $100 million by lying about his real estate empire.” (RTRS)

US/CHINA: “A bipartisan group of US senators hopes to meet with President Xi Jinping on a visit to China next week, Senator Mike Crapo said.” (BBG)

OTHER

JAPAN: “Pandemic, war and an assassination have defined Japanese Prime Minister Fumio Kishida’s two years in office, yet his chances of staying in the top job are likely to be determined by more mundane issues such as rising prices.” (BBG)

AUSTRALIA: The Reserve Bank of Australia board held the cash rate steady at 4.1% for the fourth consecutive month Tuesday. In a sign of stability, newly installed Governor Michelle Bullock made little change to the previous Governor Philip Lowe’s Sept 5 statement. However, Bullock did highlight rising services and fuel prices as areas of concern. (MNI BRIEF)

AUSTRALIA: “Australia's new loan commitments for housing rose 2.2% month over month to AU$24.82 billion in August. New loan commitments for owner-occupier loans rose 2.6% to AU$16.07 billion, according to data released Tuesday by the Australian Bureau of Statistics.” (BBG)

NEW ZEALAND: “Christina Leung, principal economist at New Zealand Institute of Economic Research comments on the 3q Quarterly Survey of Business Opinion. General business confidence improved although firms remain downbeat and pessimistic about demand in the 4q.” (BBG)

CHINA

TOURISM: “China’s tourism industry had a fruitful holiday weekend with 395 million domestic tourist trips, according to a CCTV report citing government data. In the three days leading up to the mid-autumn festival and National Day celebrations, tourism revenue was 342.24 billion yuan ($46.9 billion), marking a year-on-year increase of 125%.” (BBG)

PROPERTY: “Chinese developer stocks such as Sunac China decline, with analysts saying September’s contracted sales showing no solid recovery and may require more stimulus by authorities.” (BBG)

MARKET DATA

JAPAN SEPTEMBER MONETARY BASE Y/Y 5.6%; MEDIAN 1.6%; PRIOR 1.2%

AUSTRALIA AUGUST HOME LOANS M/M 2.2%; MEDIAN 0.2%; PRIOR -1.1%

AUSTRALIA AUGUST OWNER-OCCUPIER LOAN VALUE M/M 2.6%; PRIOR -1.6%

AUSTRALIA AUGUST INVESTOR LOAN VALUE M/M 1.6%; PRIOR -0.3%

AUSTRALIA AUGUST BUILDING APPROVALS M/M 7.0%; MEDIAN 2.5%; PRIOR -7.4%

AUSTRALIA AUGUST PRIVATE SECTOR HOUSES M/M 5.8%; PRIOR -0.4%

AUSTRALIA SEPTEMBER ANZ-INDEED JOB ADS M/M -0.1%; PRIOR 1.7%

MARKETS

US TSYS: Unchanged, Off Session Cheaps Instigated By Fed Mester

TYZ3 is currently trading at 107-10+, unchanged from NY closing levels.

- Cash tsys have moved off Asia-Pac cheaps instigated by Fedspeak from Mester and are sitting little changed across benchmarks.

- There has been no meaningful headlines outside the previously outlined Fedspeak from Mester.

- Limited data releases on Tuesday, with the focus on ADP on Wednesday ahead of Friday's September Jobs data.

JGBS: Futures Holding Near Session Highs After 10Y Supply Results

During the Tokyo afternoon session, JGB futures are trading close to their session highs, +17 compared to the settlement levels. JGB futures shifted into positive territory around lunchtime in Tokyo and continued to gain strength following the conclusion of the 10-year auction.

- The 10-year supply saw mixed demand metrics. The low price beat wider expectations and the tail shortened. However, the cover ratio declined to 3.934x from 4.019x at the September auction.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined monetary base data.

- Cash JGBs are mixed across benchmarks, with the belly outperforming. The benchmark 10-year yield is 1.6bps lower at 0.761% versus the cycle high of 0.785% set earlier today.

- The swap curve has bull-flattened to the 10-year, with rates 0.2bp to 2.9bps lower. Swaps rates are 1.3-1.5bp lower beyond. Swap spreads are generally tighter.

- Tomorrow the local calendar sees Jibun Bank PMIs (Final), along with BoJ Rinban operations covering 1- to 25-year JGBs.

AUSSIE BONDS: Cheaper But Slightly Richer After The RBA Decision

ACGBs (YM -2.0 & XM -6.5) sit slightly stronger after the RBA leaves the cash rate target at 4.10%, for the fourth consecutive meeting. This was Michele Bullock’s first meeting as Governor. The statement was little changed, which says something in itself - for now it is business as usual at the Reserve Bank. By choosing the Deputy Governor to replace Philip Lowe continuity appears to have been preserved. The Board retained its tightening bias and so has kept its options open for the November 7 decision given updated forecasts and Q3 CPI due on October 25.

- Cash ACGBs are 2-3bps richer after the RBA decision to be 1-6bps cheaper on the day. The 3/10 curve is steeper, with the AU-US 10-year yield differential at -13bps.

- The swaps curve has twist-steepened, with rates 2bps lower to 3bps higher.

- The bills strip has twist-steepened, with pricing +3 to -4. Ahead of the RBA, the strip had bear-steepened.

- RBA-dated OIS pricing is little changed after the RBA decision. The market had only attached a 12% chance of a 25bp hike today. Terminal rate expectations sit at 4.38%, the highest since late July.

- Tomorrow the local calendar sees Judo Bank PMIs (Final) released.

- Tomorrow the AOFM plans to sell A$800mn of the 2.75% 21 June 2035 bond.

NZGBS: Cheaper, Mid-Ranges Across Benchmarks, RBNZ Policy Decision Tomorrow

NZGBs closed mid-range, with benchmark yields 4-6bps higher ahead of tomorrow’s RBNZ policy decision. Bloomberg consensus expects the RBNZ to leave the cash rate unchanged at 5.50%.

- There wasn’t much in the way of domestic drivers, other than the previously outlined Q3 NZIER survey of business opinion.

- Accordingly, local participants were likely on headlines and US tsys watch. It is worth noting that the local market closed at the same time as the RBA delivered its policy decision.

- Swap rates closed 2-4bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing is mostly firmer across meetings, with a 17% chance of a 25bp hike tomorrow priced.

- Terminal OCR expectations sit at 5.85%, the highest since late May. A full 25bp hike is priced by Feb'24.

- Tomorrow the local calendar also sees CoreLogic House Prices.

FOREX: USD Index To Fresh Highs, AUD & NZD Hit By Hong Kong Equity Weakness

The USD has remained on the front foot in the first part of Tuesday trade. The BBDXY hitting fresh cyclical highs above 1277. This is +0.20% above NY closing levels on Monday.

- Early impetus came from a further rise in US yields, as Cleveland Fed President Mester stated another rate hike may be needed. US yields hold higher, but are away from session highs. The 10yr yield is near 4.69%.

- Weaker regional equity sentiment has weighed noticeably on the antipodean currencies. NZD/USD initially led moves lower, the pair last near 0.5910, 0.60% weaker for the session.

- As the afternoon session has progressed, AUD/USD has played catch up to the downside. The pair to fresh 2023 lows, sub 0.6330, which is also off 0.60% (last near 0.6325). The spill over from weaker HK equities (which has led by renewed China property concerns) has been evident in terms of lower iron ore and copper prices.

- As widely expect the RBA held rates at 4.10%, with a largely unchanged statement. This didn't impact AUD though.

- JPY is outperforming modestly. USD/JPY sits at 149.85 currently, little changed for the session. Further verbal jawboning was evident from the Japan FinMin but the rhetoric on FX didn't appear as an escalation compared with recent commentary.

- EUR/USD is down further last near 1.0460.

- Looking ahead, we have the ECB's Lane speaking, then later on, Fed’s Bostic speaks on the economic outlook and inflation. On the data front, there are US JOLTS job openings for August, which are expected to be steady.

EQUITIES: Hong Kong Stocks To Fresh YTD Lows, Property Concerns Weigh

Major regional equity markets are mostly lower. Hong Kong markets have returned from the long weekend, but sentiment has been firmly on the back foot. The HSI is off around 3% at this stage. A number of other regional markets are also tracking weaker, including Japan and Australian stocks. At this stage, US futures are down a touch, Eminis last near 4322.

- The HSI is tracking 3% lower at this stage, which puts the index back to fresh lows from late November last year.

- The mainland properties index is down 4.14%, more than reversing Friday's +3.48% gain. The Hang Seng properties index is down 3.90%. Bloomberg reported that China property sales for end September still remain deeply negative in y/y terms, albeit not as low as August (see this link).

- A reminder that China onshore markets remain closed all of this week. South Korean markets also remain shut today, returning tomorrow.

- Japan's main equity indices are off by over 1%. Losses are broad based, with bellwether Toyota a drag on aggregate performance. The ASX 200 is also down, off -1.20%. Weakness in commodity prices is weighing on the materials. Markets haven't reacted to the as expected RBA outcome.

- In South East Asia, Thailand stocks are the weakest performers, down 1.70% at this stage. This puts the index down sub 1450, which is levels last seen in early 2021. Indonesian and Malaysian stocks are modestly outperforming.

OIL: Crude Falls Through Support Levels On Fed Fears

Oil prices are down around a percent so far in APAC trading with Brent falling below $90 and WTI below $88 on a stronger greenback and a general pullback in risk driven by expectations that Fed policy will need to remain restrictive for longer. Brent is now down 5% since last Wednesday but market fundamentals remain positive. The USD index is up 0.2% after 0.8% on Monday.

- Brent broke through support at $90.41 opening up $87.37, the 50-day EMA. It is currently trading around $89.72/bbl, close to the intraday low. WTI is below initial support of $88.19 opening up $84.19. It reached an intraday low of $87.76 and is now around $87.91.

- According to Bloomberg, OPEC will have an online meeting on Wednesday to discuss the current position of global markets. Output was constant in September and its current stance is unlikely to be altered.

- The US is seeing an increase in oil output supported by the rise in prices since June but despite this inventories have continued to be run down. Later today US stock data from API is released.

- Later the Fed’s Bostic speaks on the economic outlook and inflation. On the data front, there are US JOLTS job openings for August, which are expected to be steady.

GOLD: Heavy Again In Asia-Pac After A Very Heavy Monday

Gold is 0.4% weaker in the Asia-Pac session, after starting the week on a bearish note (-1.1% at 1828.03). This came after bullion saw its biggest weekly decline in eight months last week, with the higher-for-longer interest rate environment taking its toll on the precious metal.

- US Treasury yields climbed on Monday, pressuring the yellow metal after a US government shutdown was averted over the weekend and markets shifted focus back to the future path for interest rates. US Treasuries finished the NY session 6-11bp cheaper, with the belly underperforming. The 10-year yield climbed to test the 4.70% cycle high before finishing at 4.68%.

- From a technical standpoint, the recent move lower has resulted in a break of support at $1901.10. According to MNI’s technicals team, this was followed by a breach of further support at $1884.9, the Aug 21 low. This has confirmed a resumption of the downtrend that started off the early May high. On the upside, initial firm resistance is at $1905.5, the 20-day EMA.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 03/10/2023 | 0610/0810 |  | EU | ECB's Lane speaks at Annual Economics Conference | |

| 03/10/2023 | 0630/0830 | *** |  | CH | CPI |

| 03/10/2023 | 0700/0300 | * |  | TR | Turkey CPI |

| 03/10/2023 | 0835/1035 | | EU | ECB's Lane participates in panel at Annual Economics Conference | |

| 03/10/2023 | 1145/0745 |  | CA | BOC Deputy Nicolas Vincent speech in Montreal | |

| 03/10/2023 | 1200/0800 |  | US | Atlanta Fed's Raphael Bostic | |

| 03/10/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 03/10/2023 | 1400/1000 | ** | | US | IBD/TIPP Optimism Index |

| 03/10/2023 | 1400/1000 | ** | | US | JOLTS jobs opening level |

| 03/10/2023 | 1400/1000 | ** | | US | JOLTS quits Rate |

| 03/10/2023 | - | *** | | US | Domestic-Made Vehicle Sales |

| 03/10/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 03/10/2023 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 04/10/2023 | 2200/0900 | * |  | AU | IHS Markit Final Australia Services PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.