Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- FED'S WALLER: US BANK ISSUES TO HAVE LIMITED IMPACT (MNI)

- FED'S BOWMAN: FED IS FOCUSED ON LOWERING INFLATION (RTRS)

- FED'S HARKER SEES MORE CENTRAL BANK ACTION TO QUASH INFLATION PRESSURES (RTRS)

- FED'S LOGAN WANTS FURTHER INFLATION IMPROVEMENT (MNI)

- FED'S MESTER EXPECTS 'SOMEWHAT FURTHER' TIGHTENING (MNI)

- FED'S BOSTIC SEES TIGHTER CREDIT CONDITIONS HELPING TO DO FED’S WORK (BBG)

- FED EMERGENCY LOANS TO BANKS POST FIRST RISE IN FIVE WEEKS (BBG)

- ECB’S SCHNABEL SAYS HEADLINE INFLATION SLOWING, CORE IS STICKY (BBG)

- BOE OFFICIAL TELLS HAWKS THAT RATES ARE TOO HIGH FOR ECONOMY TO WITHSTAND (BBG)

- G7 NATIONS CONSIDERING NEAR-TOTAL BAN ON EXPORTS TO RUSSIA (KYODO)

- US COULD BEGIN TO REFILL THE STRATEGIC PETROLEUM RESERVE IN FALL, ENVOY SAYS (BBG)

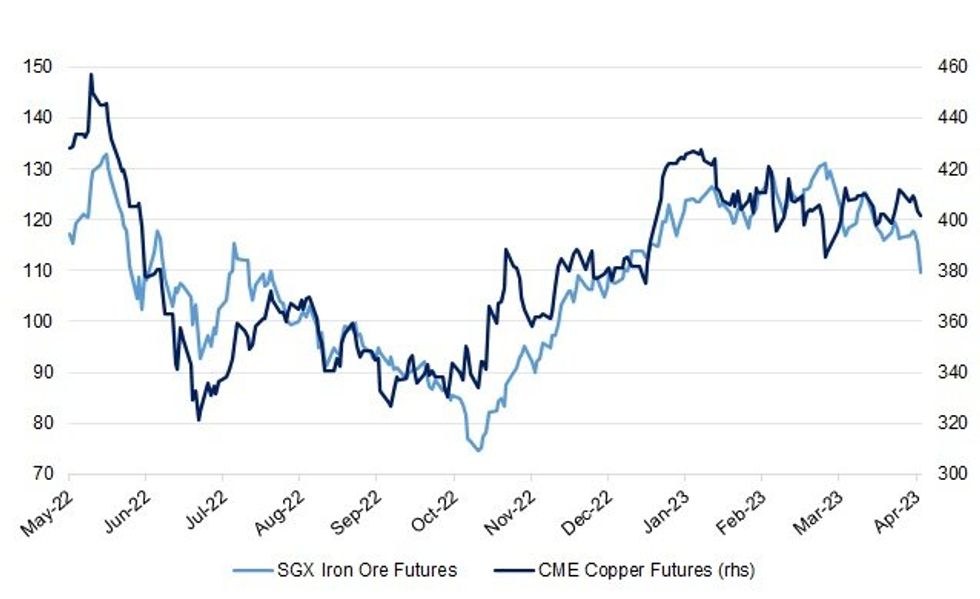

Fig. 1: SGX Iron Ore Futures Vs. CME Copper Futures

Source: MNI - Market News/Bloomberg

UK

BOE: Bank of England policy maker Silvana Tenreyro compared her hawkish colleagues to a “fool in the shower” who scolds himself by being too impatient to wait for the water to warm up, saying interest rates are already too high for the economy to bear. (BBG)

RATINGS: Potential sovereign credit rating reviews of note scheduled for after hours on Friday include:

- Moody’s on the United Kingdom (current rating: Aa3; Outlook Negative)

- S&P on the United Kingdom (current rating: AA; Outlook Negative)

EUROPE

ECB: The European Central Bank publishes slides of a speech by Executive Board member Isabel Schnabel at the Stanford Graduate School of Business. (BBG)

NORWAY: A strike by private-sector workers in Norway has ended after four days after unions and employers agreed on an average wage rise of 5.2%, set to be a nationwide benchmark in upcoming negotiations, two unions said on Thursday. (RTRS)

RATINGS: Potential sovereign credit rating reviews of note scheduled for after hours on Friday include:

- Moody’s on France (current rating: Aa2; Outlook Stable) & Ireland (current rating: A1; Outlook Positive)

- S&P on Greece (current rating: BB+; Outlook Stable), Italy (current rating: BBB; Outlook Stable) & the Netherlands (current rating: AAA; Outlook Stable)

U.S.

FED: Federal Reserve Governor Christopher Waller Thursday said panic in the banking system after the failure of Silicon Valley Bank and other lenders has subsided and suggested he sees limited damage to the real economy. (MNI)

FED: The Federal Reserve is focused on reducing inflation so as to support a growing economy and rising incomes, Fed Governor Michelle Bowman said on Thursday, adding that the strong labor market has made it hard for growing businesses to find workers. (RTRS)

FED: Federal Reserve Bank of Philadelphia President Patrick Harker said Thursday the U.S. central bank will have to do more on the policy front to get still high inflation pressures back down to the 2% target. (RTRS)

FED: Dallas Federal Reserve President Lorie Logan said on Thursday inflation has been much too high and will assess whether the central bank has made enough progress by looking for a clear change in underlying supply and demand that has caused the tight jobs market. (MNI)

FED: Federal Reserve Bank of Cleveland President Loretta Mester on Thursday endorsed a May interest rate increase and said she's prepared to adjust her views on how much higher and for how much longer rates will need to rise based on changing economic and banking conditions. (MNI)

FED: Cleveland Federal Reserve Bank President Loretta Mester said on Thursday that U.S. central bankers will be assessing at their next meeting the extent and duration of credit tightening stemming from last month's failure of two regional banks. Even before the March stresses, banks were beginning to tighten credit given the Fed's interest-rate hikes, Mester told Yahoo Finance, and the Fed is doing surveys and engaging with bankers to assess how that develops. (RTRS)

FED: Federal Reserve Bank of Atlanta President Raphael Bostic said he continues to favor raising interest rates once more and then pausing as banking strains generate a headwind for the US economy. (BBG)

FED: Banks increased emergency borrowings from the Federal Reserve for the first time in five weeks, indicating that financial stresses are lingering after a string of bank collapses last month. (BBG)

FISCAL: U.S. House Speaker Kevin McCarthy has begun working in earnest to persuade his fellow Republicans to support a $1.5 trillion increase in the nation's debt ceiling, amid early indications of a possible revolt in his thin majority. (RTRS)

FISCAL: Representative Bryan Steil, a Republican from Wisconsin discusses Speaker McCarthy's debt limit proposal and gives his insights on the proposals next steps within the Republican party. He also gives his remarks on the potential reelection announcement from President Biden that may occur some time next week. (BBG)

POLITICS: President Biden and his team are preparing to announce his reelection campaign next week, with aides finalizing plans to release a video for the president to officially launch his campaign, according to three people briefed on the plans. (Washington Post)

MONEY MARKETS: The amount parked at US money-market funds plunged by the most in more than two years as tax bills came due in the past week, tumbling from an unprecedented high. (BBG)

OTHER

GLOBAL TRADE: Almost nothing has been done to address Russia's concerns over the Black Sea grain deal, Foreign Minister Sergei Lavrov said on Thursday, the latest in a series of downbeat comments by top Moscow officials about the pact that enabled Ukraine to resume exports. (RTRS)

GLOBAL TRADE: West Coast dockworkers reached a tentative agreement with employers regarding automated machinery at cargo terminals, according to sources familiar with the negotiations, clearing one major hurdle in negotiations on a new contract covering workers at some of the country’s biggest seaports. (WSJ)

U.S./CHINA: President Joe Biden aims to sign an executive order in the coming weeks that will limit investment in key parts of China’s economy by American businesses, people familiar with the internal deliberations said. (BBG)

U.S./CHINA/TAIWAN: Spooked by the threat that China might invade Taiwan, the US wants to cut its dependence on the island’s world-beating microchips. Officials in Taipei believe the Biden administration is going too far. (BBG)

CHINA/TAIWAN: Recent allegations that China undermines peace and stability of the Taiwan Strait run against historical and international common sense, Chinese Foreign Minister Qin Gang says. (BBG)

GEOPOLITICS: U.S. President Joe Biden, in a call with Emmanuel Macron on Thursday, discussed the French leader's recent trip to China and reaffirmed the importance of maintaining peace and stability across the Taiwan Strait, the White House said in a statement. Biden and Macron also reiterated their support for Ukraine, it said. (RTRS)

GEOPOLITICS: China is building sophisticated cyber weapons to “seize control” of enemy satellites, rendering them useless for data signals or surveillance during wartime, according to a leaked US intelligence report. (FT)

GEOPOLITICS: The United States takes its defense commitment to South Korea "very, very seriously," a White House official said Thursday, following Russia's threat to arm North Korea if South Korea sends lethal assistance to Ukraine. (Yonhap)

JAPAN: Goldman Sachs is looking into environmental investment opportunities in Japan as part of a new $1.6 billion fund, the head of the group's sustainable investing told Nikkei. (Nikkei)

AUSTRALIA/CHINA: China's coal imports from Australia rose to the highest level since Dec. 2021 in March after Beijing removed barriers on coal trade with the country and Chinese traders rushed to make profits off falling overseas prices. (RTRS)

BOJ: The Bank of Japan's new chief Kazuo Ueda will not start unwinding its ultra-easy policy at April 27-28 meeting, nearly 90% of economists polled by Reuters said, as the chance of a surprise tweak at his first rate-review subsided. (RTRS)

JAPAN: Japan investors bought about 140 billion yen ($1 billion) of Credit Suisse Group AG’s bonds that were written off when the Swiss bank was suddenly sold last month, Finance Minister Shunichi Suzuki said. (BBG)

AUSTRALIA: Treasurer Jim Chalmers says the federal government will work with energy investors to design a program to issue sovereign green bonds from next year. (AFR)

RBNZ: The RBNZ has teased next month’s Financial Stability Report by releasing a section on the links between financial inclusion and financial stability. It said its regulatory functions aimed to protect and promote the stability of New Zealand’s financial system. (NBR)

BOK: A new member of the South Korean central bank's policy board said on Friday the economy is experiencing difficulties after rapid interest rate increases and needs monetary policy appropriate for the domestic situation. (RTRS)

NORTH KOREA: North Korea's foreign minister said Friday that the United States and the West have no right to argue about its status as a global nuclear weapons power, slamming a recent joint statement by the Group of Seven (G-7) diplomats as an interference in internal affairs. (Yonhap)

BOC: Bank of Canada Governor Tiff Macklem on Thursday gave one of his most detailed defenses yet in favor of keeping a 2% inflation target while being questioned about a higher goal during a Senate hearing. (MNI)

TURKEY: Turkish President Recep Tayyip Erdogan promised discounted natural gas bills for households for a year in his latest financial giveaway ahead of elections in less than a month. (BBG)

BRAZIL: Brazil’s Monetary Council, known as CMN, updated rules for credit default swaps and total return swaps carried out by banks, according to a statement from the central bank. (BBG)

RUSSIA: The Group of Seven (G7) countries are considering a near-total ban on exports to Russia, Kyodo news agency reported on Friday, citing Japanese government sources. (RTRS)

RUSSIA: Russian banks' profits rose to 330 billion roubles ($4.05 billion) in March, the central bank said on Thursday, recovering from the impact of Western sanctions on Russia's financial sector that sharply squeezed profits in 2022. (RTRS)

RUSSIA: Europe’s air-traffic control agency said Thursday that it was under attack from pro-Russian hackers amid fears that Moscow could interfere with the region’s critical infrastructure as its confrontation with the West escalates. (WSJ)

SOUTH AFRICA: President Cyril Ramaphosa will be asked to speak to his counterparts in countries offering South Africa $8.5 billion of climate finance to close coal-fired power plants to explain why the nation will depend on the dirtiest fuel for longer. (BBG)

COLOMBIA: Colombia needs to see a trend of slowing inflation and a consolidated drop in inflation expectations before cutting interest rates, central bank co-director Roberto Steiner said in a conference organized by BTG Pactual. (BBG)

CHILE: Chile’s government delivered its long-awaited lithium development policy in which the state will partner with companies in projects to tap more of the world’s biggest reserves of the battery metal. (BBG)

ARGENTINA: Argentina's central bank hiked the benchmark interest rate a sharper-than-expected 300 basis points on Thursday after inflation soared past expectations in March to hit 104% on an annual basis, the monetary authority said in a statement. (RTRS)

ARGENTINA: Argentina’s central bank issued measures that require companies to defer FX payments for imports of services, according to an emailed statement. (BBG)

LATAM: Brazil’s government, seeking to increase competition and reduce costs in transactions in local currency, decided on Thursday to simplify procedures of the local currency payment system (SML), an infrastructure that brings together the central banks of Brazil, Argentina, Paraguay and Uruguay. (RTRS)

METALS: Global miner BHP Group Ltd BHP.AX said on Friday its third-quarter iron ore output fell 0.7% from a year earlier, hurt by a 24-hour suspension of its Western Australia operations due to a fatality at the site. (RTRS)

METALS: Codelco, the world’s biggest copper producer, is becoming one of the supply-side’s largest headaches as its rush to renew aging mines in Chile endures setbacks that have sent output tumbling. (BBG)

METALS: The world's appetite for copper to build most electronic devices will exceed supply over the next decade and imperil climate targets unless dozens of new mines are built, executives and analysts said this week at a key industry conference. (RTRS)

OIL: The US could begin to refill its Strategic Petroleum Reserve as soon at the third quarter of 2023 — if the price is right, the US official responsible for energy diplomacy said. (BBG)

OIL: An oil tanker company heavily involved in moving Russian oil lost industry standard insurance for its fleet after falling foul of a Group of Seven price cap relating to the transportation of the nation’s barrels. (BBG)

OIL: Pemex's Matamoros-Brownsville pipeline, which moves refined products from the U.S. into Mexico, remains closed due to maintenance, the state-owned oil company told OPIS on Thursday. (WSJ)

CHINA

ECONOMY: China can not sustain March's strong export performance beyond the initial rapid resumption of production after the Spring Festival, according to Huo Jianguo, former president of the International Trade Research Institute of the Ministry of Commerce. (MNI)

ECONOMY: China must boost household incomes to ensure the consumption rebound is sustainable, according to Guo Liyan, director of the Comprehensive Situation Research Office of the China Macroeconomic Research Institute. (MNI)

PBOC: China’s current loan rates are within a reasonable zone as the monetary policies that have pushed bank loan rates down in recent years already helped support the economy’s rebound, according to a Shanghai Securities News report Friday which cites Zeng Gang, director of the Shanghai Institute For Finance & Development. (BBG)

YUAN: China's forex regulator on Friday pledged to fend off risks from external market shocks while maintaining prudent operations of the forex market and financial safety. (RTRS)

PROPERTY: China’s real-estate market will continue its steady Q1 recovery into Q2, according to Chai Qiang, chairman of the Chinese Society of Real Estate Appraisers. (MNI)

CHINA MARKETS

PBOC NET INJECTS CNY73 BILLION VIA OMOS FRIDAY

The People's Bank of China (PBOC) conducted CNY88 billion via 7-day reverse repos on Friday, with the rates unchanged at 2.00%. The operation has led to a net injection of CNY73 billion after offsetting the maturity of CNY15 billion reverse repos today, according to Wind Information.

- The operation aims to keep banking system liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) fell to 2.1122% at 09:33 am local time from the close of 2.1327% on Thursday.

- The CFETS-NEX money-market sentiment index closed at 53 on Thursday, compared with the close of 50 on Wednesday.

PBOC SETS YUAN CENTRAL PARITY AT 6.8752 FRI VS 6.8987 THURS

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 6.8752 on Friday, compared with 6.8987 set on Thursday.

OVERNIGHT DATA

JAPAN MAR CPI +3.2% Y/Y; MEDIAN +3.2%; FEB +3.3%

JAPAN MAR CPI EXCL. FRESH FOOD +3.1% Y/Y; MEDIAN +3.0%; FEB +3.1%

JAPAN MAR CPI EXCL. FRESH FOOD & ENERGY +3.8% Y/Y; MEDIAN +3.6%; FEB +3.5%

JAPAN APR, P JIBUN BANK MANUFACTURING PMI 49.5; MAR 49.2

JAPAN APR, P JIBUN BANK SERVICES PMI 54.9; MAR 55.0

JAPAN APR, P JIBUN BANK COMPOSITE PMI 52.5; MAR 52.9

Japan’s private sector continued to expand solidly at the start of Q2, according to latest Flash PMI data, with a resurgent service economy helping to offset a weak manufacturing sector performance. Furthermore, inflows of total new business increased at the quickest pace for nearly a year-and-a-half as services companies registered a steep upturn in sales amid reports of stronger demand conditions and improved customer numbers. There were also signs of cost pressures easing, with overall input costs rising to the weakest extent in 15 months in April. However, the sustained and strong increases in expenses in recent months fed through to another round of selling price inflation, with output charges rising at the joint-quickest rate on record. (S&P Global)

AUSTRALIA APR, P JUDO BANK MANUFACTURING PMI 48.1; MAR 49.1

AUSTRALIA APR, P JUDO BANK SERVICES PMI 52.6; MAR 48.6

AUSTRALIA APR, P JUDO BANK COMPOSITE PMI 52.2; MAR 48.5

The flash PMI readings for April reveal a growing divergence between the performance of Australia’s manufacturing sector and the broader service industries. Manufacturing activity remains soft, a reflection of weaker demand for goods and a gradual slowdown in construction activity in Australia. The April flash results for the services sector have bounced strongly, bringing into question the broader economic slowdown. All the key activity indicators are up in the month. (Judo Bank)

SOUTH KOREA MAR PPI +3.3% Y/Y; FEB +4.8%

SOUTH KOREA APR 1-20 EXPORTS -11.0% Y/Y

SOUTH KOREA APR 1-20 IMPORTS -11.8% Y/Y

SOUTH KOREA APR 1-20 TRADE BALANCE -US$4.14BN

UK APR GFK CONSUMER CONFIDENCE -30; MEDIAN -35; MAR -36

MARKETS

US TSYS: Tight Ranges, Back From Block Buy-Inspired Bests

Cash Tsys saw a light extension of Thursday’s bull steepening theme during Asia-Pac hours, with the major benchmarks last 0.5-1.5bp richer. TYM3 is +0-04 at 120-25 into London hours, just off the top of a tight 0-04 range, on modest volume of ~49K.

- A round of activity surrounding a block buy of TU futures (+6.4K) provided the highlight of the session and promoted the early bull steepening.

- The space looked through a story from Japan’s Kyodo News, which suggested that countries are considering a near-total ban on exports to Russia. A reminder that BBG ran a similar story on Thursday.

- There was no impact from the latest round of firmer than expected core CPI data out of Japan, as it isn’t seen as much of a needle mover when it comes to next week’s BoJ monetary policy meeting.

- The weekly update from the Fed saw a modest uptick in both discount window and BTFP usage, while FIMA usage nudged lower.

- Fedspeak from Harker & Bostic stuck to the respective, well-documented views.

- Preliminary PMI data from across the globe headlines Friday. There will also be a range of ECB speakers and comments from Fed Governor Cook (with the Fed going into pre-meeting blackout this weekend).

JGBS: At Bests, Look Past Higher Than Expected CPI

JGB futures (147.76, +28 compared to settlement levels) have climbed above overnight highs in the afternoon session, despite a stronger-than-anticipated Japanese CPI. This behaviour likely stems from the market's confidence that the data will have little impact on next week's BoJ monetary policy meeting. The move to session highs appeared to have been assisted by a slight strengthening by US Tsys in Asia-Pac trade and robust Rinban operations.

- Cash JGBs remain mixed across the curve with yields 0.8bp higher to 2.1bp lower with the 2-year benchmark the weakest and the 7-year the strongest. The 10-year JGB is 0.5bp richer at 0.467%, below the BoJ's YCC limit of 0.50%.

- Low to average offer/cover ratios in today's BoJ Rinban operations (covering 1- to 25-Year JGBs) have provided some light support in early afternoon trade. The exception has been the 1-3-year zone.

- The swaps curve flattening in the morning session has given way to a steepening. Swap spreads are tighter across the curve, apart from the 7-year zone.

- Looking ahead, next week’s economic calendar is relatively heavy ahead of the BOJ policy decision on Friday with the Tokyo CPI, Retail Sales and Industrial Production as the highlights. 2-year JGB supply is also scheduled.

JGBS AUCTION: 3-Month Bill Auction Results

The Japanese Ministry Of Finance (MOF) sells Y5.12515tn 3-Month Bills:

- Average Yield: -0.1779% (prev. -0.1816%)

- Average Price: 100.0478 (prev. 100.0488)

- High Yield: -0.1619% (prev. -0.1675%)

- Low price: 100.0435 (prev. 100.0450)

- % Allocated At High Yield: 62.2923% (prev. 93.4287%)

- Bid/Cover: 3.199x (prev. 3.296x)

AUSSIE BONDS: Stronger, Tight Range, Underperforms US Tsys

ACGBs sit richer (YM +3.0 & XM +2.5) after trading in a relatively narrow range for the Sydney session. The bid tone was assisted by a slight richening in global bonds in Asia-Pac trade. US Tsy yields sit 1-2bp lower in Asia-Pac trade.

- Cash ACGBs are 2-3bp richer with the 3/10 curve unchanged and the AU-US 10-year yield differential +2bp at -6bp.

- Swap rates are 5bp lower with EFPs little changed.

- Bills strip is marginally flatter with pricing +2 to +5.

- RBA-dated OIS pricing is flat to 4bp softer across meetings with 19bp of cumulative tightening priced by August.

- Next week sees the release of the much-awaited Q1 CPI data. With the almost a full 25bp rate hike priced by August, market pricing may need to be reassessed if the quarterly lends further support to the notion that inflation has peaked, as flagged by the CPI monthly release. BBG consensus expects Trimmed Mean CPI to be +1.4% Q/Q and +6.7% Y/Y versus +1.7% and +6.9% in Q4.

- Until then, participants will eye US Tsys’ response to the US earnings season, Fedspeak and global Flash PMIs.

- Elsewhere, Treasurer Chalmers commented in a statement that Australia is set to introduce a Sovereign Green Bond Program in Mid-2024.

AUSSIE BONDS: AOFM Weekly Issuance Slate

The AOFM has released its weekly issuance slate:

- On Thursday 27 April it plans to sell A$1.0bn of the 23 June 2023 Note & A$500mn of the 8 September 2023 Note.

NZGBS: Closed At Bests, Add to Post-CPI Rally

NZGBs have strengthened through the session to close at bests with the 2- and 10-year benchmark yields 9bp lower. Today’s move comes after yesterday’s 7-9bp richening sparked by a lower-than-expected print for Q1 CPI. The move to session highs has been assisted by a slight bid tone to global bonds in Asia-Pac trade. US Tsys sit 1-2bp lower in Asia-Pac trade. NZGBs have nonetheless outperformed their $-bloc peers with the NZ/US and NZ/AU 10-year yield differentials respectively 3bp and 4bp lower.

- Swap rates are 11bp lower with implied swap spreads narrower.

- RBNZ dated OIS closed 3-13bp softer across meetings with Apr-24 leading. 19bp of tightening priced for the May meeting versus 24bp before the. Easing expectations for Feb-24, off the expected terminal OCR of 5.52% (July), are currently 46bp.

- RBNZ Deputy Governor Hawkesby's speech notes from today's address covered familiar ground stating that the extent of moderation in the domestic economy will determine the direction of future monetary policy.

- The local calendar is light next week with ANZ Business and Consumer Confidence (Thu) as the highlights. In Australia, Q1 CPI is scheduled for Wednesday.

- Until then, participants will eye US Tsys’ response to the US earnings season, Fedspeak and global Flash PMIs.

EQUITIES: China Equities Slump, Amid Likely Fresh US Investment Curbs

Regional Asia Pac equities are tracking lower to end the week. This follows negative leads from US/EU stocks through Thursday. China shares are among the weakest performers, off by a little over 1%. Likely US curbs on investment in China, have weighed. US futures have largely tracked sideways.

- The CSI 300 is off by 1%, the Shanghai Composite by a slightly more. US President Biden is reportedly looking at introducing curbs on US investment into China, within the next few weeks (reportedly with G-7 backing per BBG reports).

- The HSI has seen some negative spill over, off by 0.64%, with the tech sub-index off by 1.81% at this stage.

- The Kospi is down by 1.00%, the Kosdaq around 1.75%, as onshore analysts have warned of an over heating market amid heavy retail positioning. The Taiex is down by 0.41%, while the Topix is down around 0.30% at this stage.

- The ASX 200 is down by 0.43%, with miner BHP leading the move lower amid weaker commodity prices.

- In SEA most markets are down a touch, but note Indonesia, Malaysia and the Philippines are closed.

GOLD: Holding Above $2000, Flat Versus Levels A Week Ago

Gold has drifted a little lower through the course of today's session. We were last near $2002, down 0.15% for the session and only reversing part of Thursday's 0.50% gain. This is consistent with a slightly firmer USD backdrop (ex JPY). The weaker tone to regional equities hasn't aided safe haven demand, although moves in US futures and yields have been more muted.

- We got above $2010 post the Asia close on Thursday, an +$40 rebound from Wednesday session lows. Still, gold is currently tracking close to flat for the week.

- In terms of levels, recent highs come in between $2010/$2015, while on the downside, the 20-day EMA comes in just under $1989.

- Gold ETF holdings have flatlined somewhat over the past week.

OIL: Tracking Down Sharply For the Week Amid Demand Concerns

Brent crude is unchanged versus Thursday closing levels, last around $81.10. We lost nearly 4.5% through the Wednesday/Thursday sessions. At this stage, Brent is down ~6% for the week, tracking for the first weekly loss since mid March. WTI is slightly above $77/bbl, with this level holding through the tail end of Thursday's session.

- Brent is now sub the 50-day EMA (just under $82.40/bbl), with bears likely to target a break back sub $80/bbl, highs from late March.

- Demand concerns remain a clear headwind in the near term. A South Korean refinery plans to trim run rates in July.

- Weakness in other commodities, like iron ore today, amid signs of weaker China demand, are also likely weighing on oil sentiment at the margins.

- Looking ahead to next week, there isn't much in the way of oil specific event risks outside of the weekly inventory readings.

FOREX: Multiple Supports For Yen, Slumping Iron Ore Hurts The A$

Yen has outperformed today. USD/JPY is back sub 134.00 (we touched a low of 133.76, last 133.80/90). The stronger than expected core CPI print for March (3.8%y/y versus 3.6% expected), drove the initial round of yen strength. Headlines that the G7 were considering a full export ban on Russia drove the next round of strength, although there wasn't much follow through.

- These headlines were largely in line with what Bloomberg reported yesterday, which may have capped the market reaction.

- Still, weaker regional equities, led by China (-1%) have aided yen safe haven demand. This, coupled with a further slump in iron ore prices (off by 5%), amid demand concerns has hurt A$ sentiment. AUD/USD is back to 0.6710/15, -0.45% for the session and the weakest G10 performer.

- AUD/JPY is back to 89.90, against recent highs near 90.80. Note the 50-day MA comes in just under 90.00. NZD/USD has been dragged lower, last under 0.6160, which is slightly under the simple 200-day MA.

- EUR/USD and GBP/USD have been offered slightly, while the BBDXY is a touch higher to 1225.80.

- In the cross asset space, US yields are down a touch, while US equity futures have been close to flat for much of the session.

- Looking ahead, preliminary PMI data from across the globe will cross, along with UK retail sales. There will also be a range of ECB speakers and comments from Fed Governor Cook (with the Fed going into pre-meeting blackout this weekend).

FX OPTIONS: Expiries for Apr21 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0973-80(E920mln), $1.1050(E1.7bln)

- GBP/USD: $1.2350(Gbp545mln)

- USD/JPY: Y134.00-20($829mln)AUD/USD: $0.6795-00(A$521mln), $0.6845(A$1.4bln)

- USD/CAD: C$1.3520-40($670mln)

- USD/CNY: Cny7.0100($740mln)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 21/04/2023 | 0600/0700 | *** |  | UK | Retail Sales |

| 21/04/2023 | 0700/0900 |  | EU | ECB de Guindos Remarks at Fundacion La Caixa | |

| 21/04/2023 | 0715/0915 | ** |  | FR | S&P Global Services PMI (p) |

| 21/04/2023 | 0715/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 21/04/2023 | 0730/0930 | ** |  | DE | S&P Global Services PMI (p) |

| 21/04/2023 | 0730/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 21/04/2023 | 0800/1000 | ** | | EU | S&P Global Services PMI (p) |

| 21/04/2023 | 0800/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 21/04/2023 | 0800/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 21/04/2023 | 0830/0930 | *** | | UK | S&P Global Manufacturing PMI flash |

| 21/04/2023 | 0830/0930 | *** | | UK | S&P Global Services PMI flash |

| 21/04/2023 | 0830/0930 | *** | | UK | S&P Global Composite PMI flash |

| 21/04/2023 | 1230/0830 | ** |  | CA | Retail Trade |

| 21/04/2023 | 1345/0945 | *** |  | US | IHS Markit Manufacturing Index (flash) |

| 21/04/2023 | 1345/0945 | *** | | US | S&P Global Services Index (flash) |

| 21/04/2023 | 1430/1630 | | EU | ECB Elderson at Peterson Institute Climate Event | |

| 21/04/2023 | 1745/1945 | | EU | ECB de Guindos at Colegio de Economistas de Madrid Event | |

| 21/04/2023 | 2035/1635 | | US | Fed Governor Lisa Cook |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.