Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- ISRAEL INTERCEPTS ROCKET AS GUNFIRE, EXPLOSIONS IN NORTH GAZA REPORTED - RTRS

- ISRAEL AND HAMAS'S TRUCE ENDS WITH NO ANNOUNCEMENT OF EXTENSION - BBG

- CAIXIN NOV MANUFACTRUING PMI HITS THREE-MONTH HIGH - MNI BRIEF

- INFLATION MOVE GOOD NEWS, BUT RISKS REMAIN - NAGEL - MNI BRIEF

- BOE APPOINTMENTS NEED MORE TRANSPARENCY -BRIDGES - MNI INTERVIEW

- RBNZ CAN'T AFFORD TO IGNORE IMMIGRATION SURGE, HAWKESBY SAYS - BBG

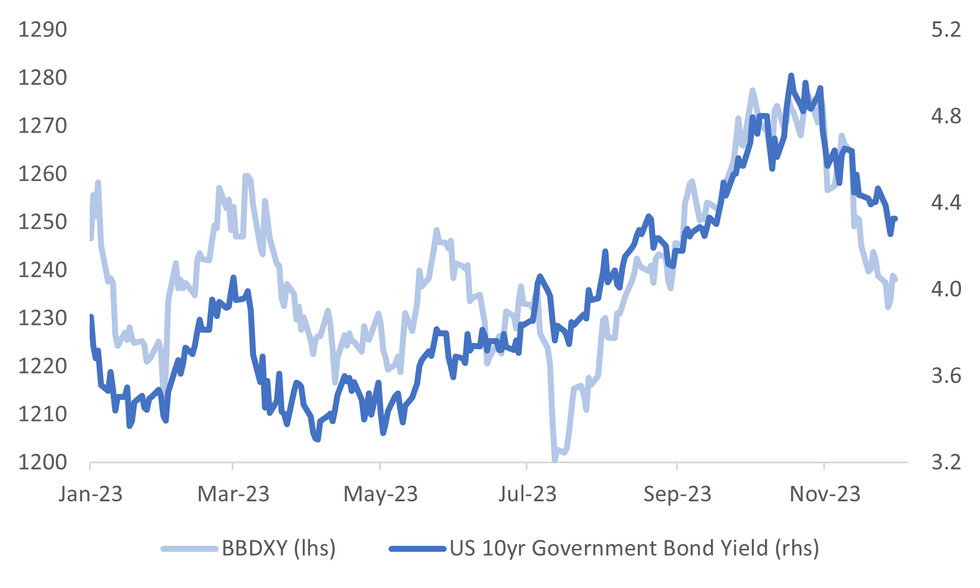

Fig. 1: USD BBDXY INDEX & 10yr Government Bond Yield

Source: MNI - Market News/Bloomberg

U.K.

BOE (MNI INTERVIEW): A reformed process of appointing members to the Bank of England’s Monetary Policy Committee should be more transparent, but not so transparent as to deter applicants, Lords Economic Affairs Committee chair Lord Bridges told MNI, stressing that it was crucial to ensure greater diversity of thinking among policymakers while steering clear of the dangers of politicisation.

ECONOMY (BBG): UK business bosses are growing slightly less pessimistic about the economy but overall sentiment “remains firmly entrenched in negative territory” despite big tax cuts announced last week, the Institute of Directors found.

CLIMATE (BBG): Rishi Sunak will pledge to spend £1.6 billion ($2 billion) on climate projects, as the British premier arrives at the COP28 summit trying to show leaders the UK remains committed to the cause after he watered down his government’s green agenda and promised to boost oil and gas exploration.

EUROPE

ECB (MNI BRIEF): The slowdown of inflation in September and October, followed by November’s headline inflation print of 2.4% in the eurozone and 2.3% in Germany is “encouraging,” Bundesbank president Joachim Nagel said in a speech Thursday, but uncertainty over the outlook remains “high,” with risks “pointing upwards” due to geopolitical uncertainty and strong wage dynamics.

FISCAL (MNI BRIEF): A deal on EU fiscal rules is “not so far away”, EU Budget Commissioner Johannes Hahn said Thursday, noting that the EC’s proposal for reform which was issued in April was “something that could be supported” by all countries.

RUSSIA (BBG): Russia’s seaborne coal exports to China and India — which became key markets in the wake of Moscow’s invasion of Ukraine — have slumped back to where they were at the start of the war as demand for Russian supplies dwindles.

RUSSIA (BBG): Russia will seize stakes in St. Petersburg Pulkovo airport owned by Fraport and Qatari sovereign fund and transfer them to a new domestic entity, according to President Vladimir Putin’s order published late Nov. 30.

EU/CHINA (SCMP): EU officials will urge Chinese President Xi Jinping to act against 13 Chinese entities accused of getting around sanctions on Russia at a summit in Beijing next week, South China Morning Post reports, citing people familiar with the matter.

FRANCE (BBG): A year after President Emmanuel Macron received a warning that France’s credit status faced closer scrutiny, the possibility of a humbling downgrade is looming ever larger.

U.S.

FED (MNI INTERVIEW): A steady decline in U.S. inflation is jacking up real borrowing costs in a way that could force the Federal Reserve to start cutting interest rates by spring, former IMF economist Brett House told MNI.

US/CHINA (BBG): Treasury Secretary Janet Yellen reiterated that the US needs to reduce over-reliance on China in key supply chains as she touted major investments in US productive capacity in a pitch for Bidenomics Thursday.

OTHER

ISRAEL (RTRS): Israel's military said it intercepted a rocket fired from Gaza early on Friday while Hamas-affiliated media reported sounds of gunfire and explosions in the north of the coastal strip shortly before a deadline to extend a seven-day truce was set to expire.

ISRAEL (BBG): A truce between Israel and Hamas ended without the warring sides announcing an extension, increasing the possibility of fighting resuming soon in the Gaza Strip.

JAPAN (BBG): Japan’s businesses increased investment modestly over the summer as profits continued to grow in a sign of resilience even as the economy shrank.

JAPAN (BBG): Japanese life insurers have cut currency hedging by the most in more than a decade, signaling receding concern of a rebound in the yen that would wipe out returns from overseas assets.

NEW ZEALAND (BBG): New Zealand’s central bank can’t afford to ignore a surge in immigration, even though it’s expected to subside next year, because inflation has been above target for so long, Deputy Governor Christian Hawkesby said.

TURKEY (BBG): Republic of Turkiye/The's long-term foreign currency debt rating was affirmed by S&P at B. Outlook to positive from stable.

CHINA

ECONOMY (MNI BRIEF): China's Caixin manufacturing PMI rose by 1.2 points to register 50.7 in November from October, rising back to the expansionary zone above the breakeven 50 mark and hitting a three-month high, the financial publisher said Friday.

ECONOMY (YICAI): China's manufacturers face insufficient market demand according to Zhao Qinghe, a senior statistician at the Service Industry Survey Center of the National Bureau of Statistics. Zhao noted 60% of respondents in the PMI survey said demand remained low.

PROPERTY (YICAI): Zheshang Bank, China Construction Bank, Bank of Communications and others have successively held meetings with major real-estate companies to understand better their financing needs, fueling market expectations of a fresh round of support policies, Yicai.com reported. Authorities have not issued an official "white list" or ordered banks to increase their proportion of real-estate loans, the newspaper said citing an unnamed source from a local branch of a major state-owned bank.

IRON ORE (DCE): The Dalian Commodity Exchange (DCE) will strengthen market supervision and crack down on illegal trading in key products such as iron ore futures, according to a statement on the DCE website. In response to large fluctuations in iron-ore futures, the exchange will continue to watch for violations such as spreading incorrect information and making false hedging transactions.

MARKETS (CSJ/BBG): The 50 billion yuan private fund firm to be set up by two major Chinese insurers to invest in listed companies is meant to help stabilize the stock market as regulators have urged, China Securities Journal reported.

CHINA MARKETS

PBOC Drains Net CNY545 Bln Fri; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY119 billion via 7-day reverse repo on Friday, with the rate unchanged at 1.80%. The operation has led to a net drain of CNY545 billion after offsetting the maturity of CNY664 billion reverse repos today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.7941% at 09:31 am local time from the close of 2.1753% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 40 on Thursday, compared with the close of 44 on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

PBOC Yuan Parity Higher At 7.1104 Friday vs 7.1018 Thursday

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1104 on Friday, compared with 7.1018 set on Thursday. The fixing was estimated at 7.1436 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND NOV CORE LOGIC HOUSE PRICES Y/Y -4.5%; PRIOR -5.7%

NEW ZEALAND NOV ANZ CONSUMER CONFIDENCE 91.9; PRIOR 88.1

NEW ZEALAND NOV NZ CONSUMER CONFIDENCE M/M 4.3%; PRIOR 2.0%

AUSTRALIA NOV CORELOGIC HOUSE PRICES M/M 0.6%; PRIOR 0.9%

AUSTRALIA NOV F JUDO BANK PMI MFG 47.7; PRIOR 47.7

JAPAN OCT JOBLESS RATE 2.5%; MEDIAN 2.6%; PRIOR 2.6%

JAPAN OCT JOB-TO-APPLICANT RATIO 1.30; MEDIAN 1.29; PRIOR 1.29

JAPAN 3Q CAPITAL SPENDING Y/Y 3.4%; MEDIAN 3.4%; PRIOR 4.5%

JAPAN 3Q CAPITAL SPENDING EX SOFTWARE Y/Y 1.7%; MEDIAN 3.4%; PRIOR 4.4%

JAPAN 3Q COMPANY PROFITS Y/Y 20.1%; MEDIAN 13.8%; PRIOR 11.6%

JAPAN 3Q COMPANY SALES Y/Y 5.0%; MEDIAN 4.5%; PRIOR 5.8%

JAPAN NOV F JUDO BANK PMI MFG 48.3; PRIOR 48.1

SOUTH KOREA NOV EXPORTS Y/Y 7.8%; MEDIAN 5.0%; PRIOR 5.1%

SOUTH KOREA NOV IMPORTS Y/Y -11.6%; MEDIAN -8.6%; PRIOR -9.7%

SOUTH KOREA TRADE BALANCE $3800mn; MEDIAN $1000mn; PRIOR $1627mn

SOUTH KOREA NOV S&P PMI MFG 50.0; PRIOR 49.8

CHINA NOV CAIXIN MPI MFG 50.7; MEDIAN 49.6; PRIOR 49.5

MARKETS

US TSYS: Subdued Asia-Pac Dealings Ahead Of Fed Chair Powell’s Fireside Chat

TYH4 is trading at 109-30, +0-04+ from NY closing levels, after dealing in a relatively narrow range in today’s Asia-Pac session.

- The session has been subdued with newsflow light. Accordingly, local participants have been content to sit on the sidelines ahead of Fed Chair Powell’s fireside chat later today. The FOMC media blackout begins Friday at midnight ET.

- Today’s US calendar also sees the release of the ISM Manufacturing Index. Chicago PMI strength and other manufacturing surveys point to some upside risk.

- Cash tsys are dealing flat to 1bp cheaper in the Asia-Pac session, with a slight steepening bias apparent, after yesterday’s month-end selling.

JGBS: Futures At Session Lows, Sharp Reversal Off Yesterday’s High, Tokyo CPI Next Week

JGB futures are weaker and near Tokyo session lows, -28 compared to settlement levels.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined labour market and IP data.

- At 146.18, today’s price action looks technically driven after JGB futures reversed off the 200-day moving average (continuation contract) at yesterday’s high of 147.16. According to MNI’s technicals team, 143.44, the Oct 31 low, marks key support should 144.93 give way.

- Cash tsys are dealing flat to 1bp cheaper in the Asia-Pac session after yesterday’s month-end selling. The session has been subdued for US tsys with newsflow light. Accordingly, local participants have been content to sit on the sidelines ahead of Fed Chair Powell’s fireside chat later today.

- The cash JGBs are generally cheaper, led by the belly, with yields 1.3bp lower (2-year) to 4.5bps higher (10-year). The benchmark 10-year yield is 0.716% versus yesterday’s low of 0.638%.

- Swap rates are higher along the curve. Swap spreads are wider apart from the 7- to 30-year zone.

- Next week, the local calendar sees Monetary Base data on Monday, ahead of Tokyo CPI and Jibun Bank Japan Composite & Services PMI data on Tuesday.

- Monday sees BOJ Rinban operations covering 1- to 25-year+ JGBs.

AUSSIE BONDS: Cheaper, Subdued Session Ahead Of Fed Chair’s Chat, RBA Decision On Tuesday

ACGBs (YM -5.0 & XM -7.0) are cheaper and at or near Sydney session lows. The session has been subdued with the domestic data drop failing to provide a market-moving event. Local participants have been content to sit on the sidelines ahead of Fed Chair Powell’s fireside chat later today. The FOMC media blackout begins Friday at midnight ET. The US calendar also sees the release of the ISM manufacturing index.

- Cash ACGBs are 6-8bps cheaper, with the AU-US 10-year yield differential 7bps wider at +16bps.

- Swap rates are 5bps higher, with EFPs around 2bps tighter.

- The bills strip bear-steepens, with pricing -1 to -8.

- RBA-dated OIS pricing is flat to 3bps softer across meetings.

- Next week, the local calendar sees Q3 Inventories and Company Profits on Monday, along with Melbourne Institute Inflation Gauge, Home Loans and ANZ-Indeed Job Ads monthly data. Judo Bank Composite & Services PMIs and Q3 BOP data drops on Tuesday ahead of the RBA Policy Decision. 23/24 economists surveyed expect the RBA to leave the cash rate at 4.35%. The market attaches a 9% chance of a 25bp hike next week. Q3 GDP is due for release on Wednesday.

- The AOFM plans to sell A$700mn of the 3.75% April 2037 on Wednesday.

NZGBS: Closed With Curve Sharply Steeper Ahead Of Fed Chair Powell’s Fireside Chat

NZGBs closed flat to 10bps cheaper, with the 2/10 curve steeper. The benchmarks finished 2bps off the session’s worst levels after a quiet session. With the domestic data calendar relatively light, local participants have been content to sit on the sidelines ahead of Fed Chair Powell’s fireside chat later today.

- Swap rates closed 6-11bps higher, with the 2s10s curve steeper and implied swap spreads wider.

- RBNZ dated OIS pricing closed little changed, with terminal OCR expectations at 5.53%.

- The RBNZ can’t afford to ignore a surge in immigration, even though it’s expected to subside next year, because inflation has been above target for so long, Deputy Governor Christian Hawkesby said. “When you’re an environment where inflation is at target and inflation expectations are well anchored, you’ve got the luxury to look through things and bide your time,” however we “don’t have that luxury.” (See Bloomberg link)

- The local calendar sees the release of the Terms of Trade Index on Monday.

- Later today sees the release of the ISM manufacturing index before Fed Chair Powell's fireside chat at 1100ET including text. Chicago PMI strength and other manufacturing surveys point to some upside risk. The FOMC media blackout begins Friday at midnight ET.

EQUITIES: Hong Kong Index Close To Recent Lows, Despite Caixin PMI Beat

Regional equities are mixed in the first part of Asia Pac Friday trade. Hong Kong and China markets are weaker at the break, despite a Caixin manufacturing PMI beat. Trends are mixed elsewhere. US futures sit modestly lower at this stage, having tracked tight ranges for much of the session. Eminis were last near 4574, -0.07%, while Nasdaq futures sit off 0.20%, at 15953.

- US yields recovered from an earlier dip, while US real yields rebounded on Thursday, which may be tempering equity sentiment to a degree. This comes ahead of more US data (including ISM) and Fed Chair Powell speak later.

- At the break, the CSI 300 is off 0.91%, with the real estate sub index off a more modest 0.36%, although this the 6th straight session loss for the index. BBG noted that sales data from the top 100 real estate companies continued to show weakness in homes sales through Nov.

- The HSI is off 0.69% at the break. The index is not too far from recent lows sub 16900. The Caixin PMI beat only provided a brief respite for sentiment.

- Japan's Topix is up 0.50%, while the Nikkei is closer to flat. Earlier data showed better company profits data for Q3, while capex data points to positive GDP revisions next week.

- The Kospi is underperforming, down 1%, with offshore investors selling local stock. The Taiex is close to flat.

- In SEA, most markets are firmer (gains are under 0.50% though), although Indonesia stocks are down 0.45% at this stage.

FOREX: Dollar Claws Back Earlier Losses, NZD Still Best Performer In The Past Week

The USD has clawed some losses as the Friday Asia Pac session has progressed. The BBDXY sits back close to unchanged at 1238.60. Earlier lows were at 1236.62.

- US yields have ticked up from earlier lows, which has helped. The 10yr last approaching 4.34%, against earlier lows sub 4.31%.

- Slightly better data out of Japan (implying upside GDP revisions from the capex side next week), haven't had a lasting positive impact on sentiment. Earlier lows in USD/JPY were at 147.61, and we now sit back at 148.10/15, close to unchanged for the session.

- NZD/USD remains slightly higher, last 0.6160, but drew selling interest on an earlier move above 0.6190. This high coincided with the Caixin China PMI beat.

- Still, NZD/USD is the best G10 performer in the past week, up 1.45% over this period (CHF is the next best at +0.91%.

- AUD/USD is back close to 0.6600, underperforming the NZD so far today. We have option expiries at nearby levels, which may be influencing spot. HK and China equities have generally remained weaker, which may be weighing as well (despite the PMI beat outlined above).

- Looking ahead, we have various final PMI prints in the EU/UK, while some ECB speak is due as well. Later in the US, the ISM prints, along with remarks from Fed Chair Powell.

OIL: Lower On Skepticism Around OPEC Voluntary Cuts

WTI (CLF4) tracks slightly weaker at $75.72/bbl in Friday Asain trade, after a steeper fall on Thursday (off 2.44%). We are close to unchanged for this benchmark on week-ago levels.

- OPEC announced additional voluntary cuts following Thursday's meeting, with a total reduction of 2.2m b/d, OPEC said in a statement. See this link for more details.

- The cuts were met with market scepticism. Crude regained some ground after further details of the cuts were revealed, but it remained lower on the day. The resumption of loadings from Black Sea Ports has added some further downside.

- For WTI, on the downside, the bear trigger lies at $72.37, the Nov 16 low. Clearance of this level would resume the downtrend.

- Headlines crossed earlier that the US has bought 2.73 million barrels for its reserves at $79/bbl (see this BBG link).

GOLD: On Track For Third Weekly Gain

Gold is 0.1% higher in the Asia-Pac session, after closing 0.4% lower at $2036.41 on Thursday on the back of a firmer USD and higher US Treasury yields.

- Cash tsys finished 4-7bps cheaper, with the 10-year leading. The US tsy 10-year yield rose 7bps to 4.33% but is still down 65bps from the cycle high of 5.01%.

- Nevertheless, bullion is on track for a third weekly rise amid growing market expectations that the US Federal Reserve has achieved peak funds rate and that the next move will be a cut. This expectation was supported yesterday by the release of the core PCE inflation data, which printed in line with expectations, and continuing jobless claims data that rose more than expected.

- However, with around 100bps of easing priced in by the market, Fedspeak pushed back against the market's dovish policy outlook ahead of Fed Chair Powell’s fireside chat later today. Fed Daly said that she is not thinking about rate cuts, and it is too early to call an end to hikes. Fed Williams noted that monetary conditions are restrictive but should remain so for some time to bring inflation back to 2%.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 01/12/2023 | 0800/0900 | *** |  | CH | GDP |

| 01/12/2023 | 0800/0300 |  | US | Fed Vice Chair Michael Barr | |

| 01/12/2023 | 0815/0915 | ** |  | ES | IHS Markit Manufacturing PMI (f) |

| 01/12/2023 | 0845/0945 | ** |  | IT | S&P Global Manufacturing PMI (f) |

| 01/12/2023 | 0850/0950 | ** |  | FR | IHS Markit Manufacturing PMI (f) |

| 01/12/2023 | 0855/0955 | ** |  | DE | IHS Markit Manufacturing PMI (f) |

| 01/12/2023 | 0900/1000 | *** | | IT | GDP (f) |

| 01/12/2023 | 0900/1000 | ** |  | EU | IHS Markit Manufacturing PMI (f) |

| 01/12/2023 | 0930/0930 | ** |  | UK | S&P Global Manufacturing PMI (Final) |

| 01/12/2023 | 1000/1100 | | EU | ECB's Elderson participates in ECB forum panel | |

| 01/12/2023 | 1130/1230 | | EU | ECB's Lagarde conversation at 5th ECB Forum | |

| 01/12/2023 | - | *** | | US | Domestic-Made Vehicle Sales |

| 01/12/2023 | 1330/0830 | *** |  | CA | Labour Force Survey |

| 01/12/2023 | 1445/0945 | *** | | US | IHS Markit Manufacturing Index (final) |

| 01/12/2023 | 1500/1000 | *** | | US | ISM Manufacturing Index |

| 01/12/2023 | 1500/1000 | * | | US | Construction Spending |

| 01/12/2023 | 1500/1000 | | US | Chicago Fed's Austan Goolsbee | |

| 01/12/2023 | 1600/1100 | | US | Fed Chair Jerome Powell | |

| 01/12/2023 | 1800/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

| 01/12/2023 | 1900/1400 | | US | Fed Chair Powell, Gov. Cook |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.