Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- KEY SENTIMENT, CAPEX PLANS SOLID - BOJ TANKAN - MNI

- BUSINESS INFLATION EXPECTATIONS SOLID - BOJ TANKAN - MNI BRIEF

- RBNZ REFORM TO ADD URGENCY TO INFLATION FIGHT - MNI INTERVIEW

- NEW ZEALAND ANNUAL, FUEL, ALCOHOL PRICE INFLATION SLOWS - BBG

- NZ GOV DROPS EMPLOYMENT FROM RBNZ REMIT - MNI BRIEF

- CHINA DISAPPOINTS INVESTORS BY SKIPPING SIGNALS FOR BIG STIMULUS- BBG

- ARGENTINA DEVALUES PESO BY 54% IN FIRST BATCH OF SHOCK PLANS - BBG

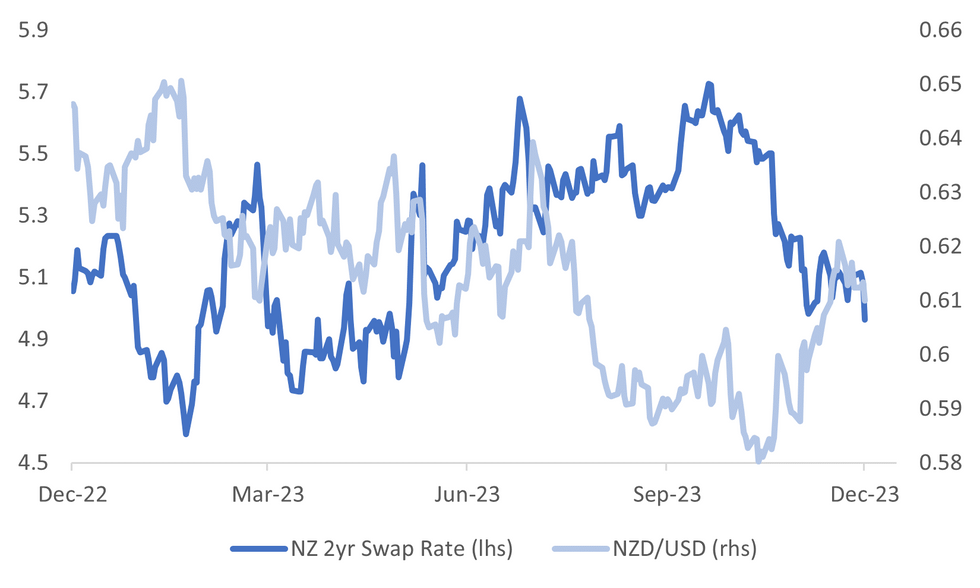

Fig. 1: NZD/USD Versus NZ 2yr Swap Rate

Source: MNI - Market News/Bloomberg

U.K.

POLITICS (BBG): Prime Minister Rishi Sunak staved off a potential rebellion from members of his Conservative Party, winning a parliamentary vote on legislation designed to green-light his signature plan to deport asylum-seekers to Rwanda.

FISCAL (BBC): Eight million people on means-tested benefits will receive a cost-of-living payment in February to help with high bills - the last scheduled instalment. The £299 payment will be made directly into bank accounts, without the need to make a claim, between 6 February and 22 February.

CORPORATE (BBG): Walgreens Boots Alliance Inc. is reviving discussions on a potential exit from its UK drugstore chain Boots, people with knowledge of the matter said, nearly 18 months after a sale process was scrapped.

EUROPE

UKRAINE (RTRS): President Joe Biden warned Republicans on Tuesday that they would give Russia a "Christmas gift" if they failed to provide additional military aid to Ukrainian President Volodymyr Zelenskiy, whose meeting with a top U.S. lawmaker concluded without a commitment for more support.

HUNGARY (BBG): Hungary is prepared to lift its veto on a massive European Union funding proposal for Ukraine in return for billions in financing the bloc has been withholding from Budapest over democratic backsliding, Prime Minister Viktor Orban’s chief political adviser said.

POLAND (BBC):New Polish PM Donald Tusk has laid out his programme for government, promising major change after eight years of nationalist government. The plans include improving relations with the European Union and pledging to restore the rule of law, the focus of a long-running row with Brussels.

ECB (BBG): Europe needs a plan to deepen its financial and economic unity if it is to emerge from crises affecting its democracy and society, the chief of France’s central bank said.

U.S.

US/ISRAEL (BBG): Divisions between President Joe Biden and Israeli Prime Minister Benjamin Netanyahu over the conflict in Israel spilled into public view, with the leaders’ competing visions for the post-war Gaza Strip underscoring a deepening split between the allies.

US/CHINA (BBG): A bipartisan group of US lawmakers recommended raising tariffs on goods from China and further restricting investment into the country, underscoring the growing support from both sides of the aisle for a more confrontational approach to Beijing.

CORPORATE (BBG): SpaceX will sell insider shares at $97 apiece in a tender offer, a price increase that boosts the value of Elon Musk’s space and satellite company closer to $180 billion, according to people familiar with the matter.

OTHER

MIDEAST (RTRS): Israel faced growing diplomatic isolation in its war against Hamas as the United Nations demanded an immediate humanitarian ceasefire in Gaza and U.S. President Joe Biden told the longtime ally its "indiscriminate" bombing of civilians was hurting international support.

COMMODITIES (RTRS): The COP28 Presidency released a proposed text of a final climate deal on Wednesday that would, for the first time, push nations to transition away from fossil fuels to avert the worst effects of climate change.

JAPAN (MNI): Japanese benchmark business sentiment rose over Q4 for the third straight increase thanks to the recovery of automobile production due to eased supply-side restrictions and despite global economic uncertainty, the Bank of Japan's December Tankan business sentiment survey showed on Wednesday.

JAPAN (MNI BRIEF): Japanese firm inflation expectations remained unchanged at 2.2% for three years and a 2.1% over five, while corporate output prices remained strong, supporting the Bank of Japan's view that the economy's disinflationary norm is changing, the BOJ December Tankan survey released on Wednesday showed.

NEW ZEALAND (MNI INTERVIEW): Proposed reforms of the Reserve Bank of New Zealand will lead to greater accountability and add urgency to its fight against inflation, a former governor told MNI. The Reserve’s recent record has seen inflation persist above the 1-3% target for some time while the central bank racked up balance-sheet losses due to its bond-buying programme and "nobody is held accountable,” said Don Brash, governor between 1988-2002. Stressing the importance of preserving central bank independence, Brash said it should nonetheless be easier to remove poorly-performing governors.

NEW ZEALAND (MNI BRIEF): New Zealand’s Minister of Finance Nicola Willis has amended the Remit for the Reserve Bank of New Zealand’s Monetary Policy Committee, removing the objective to support maximum sustainable employment. “The amendment is consistent with advice the Reserve Bank has given in the past and helps to reiterate our focus on achieving low and stable consumer price inflation,” said Board Chair Professor Neil Quigley.

NEW ZEALAND (BBG): Statistics New Zealand reports price indexes for selected goods and services for November, in statement. Food, fuel and alcohol prices, comprising ~27% of CPI, rose at a slower annual pace.

AUSTRALIA (BBG): Australia’s budget update showed the government’s books are in better shape than anticipated due to persistent strength in commodity prices and a tight labor market, though global risks are clouding the outlook.

ARGENTINA (BBG): Argentina devalued the peso by 54% and announced a swath of spending cuts as the first steps of President Javier Milei’s shock-therapy program, moves welcomed by the International Monetary Fund.

CHINA

ECONOMY (BBG): China’s top leaders including President Xi Jinping vowed to make industrial policy their top economic priority next year, a letdown for investors hoping to see more forceful stimulus to boost growth.

FISCAL (YICAI): The Central Economic Work Conference indicated next year’s fiscal stance remained unchanged and the deficit ratio could exceed 3% with the central government taking the lead, according to Luo Zhiheng, chief economist at Yue Kai Securities. Authorities will maintain positive fiscal policy to support the expansion of total demand and prevent economic and social risks, Luo added

MONETARY POLICY (21st Century Business Herald): The People’s Bank of China will likely cut interest rates and the reserve requirement ratio next year to keep the growth rate of M2 and social financing at a high level, while the Central Economic Work Conference indicated monetary policy will need to support the rebound of prices and the return to the potential growth level.

TECH (CSJ/BBJ): Artificial intelligence, biomanufacturing, commercial aerospace, low-altitude economy and quantum computing are among the areas that could benefit most from the country’s industrial policy drive, China Securities Journal reports, citing experts.

PROPERTY (CCTV/BBG): China will satisfy the reasonable financing needs of builders and prevent their debts from defaulting collectively, Vice Minister of Housing and Urban-rural Development Dong Jianguo says in conference on Wednesday, China Central Television reports.

CHINA MARKETS

MNI: PBOC Injects Net CNY25 Bln Weds; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY265 billion via 7-day reverse repo on Wednesday, with the rate unchanged at 1.80%. The operation has led to a net injection of CNY25 billion after offsetting the maturity of CNY240 billion reverse repos today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.7709% at 09:26 am local time from the close of 1.8812% on Tuesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 42 on Tuesday, compared with the close of 48 on Monday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

PBOC Yuan Parity lower At 7.1126 Wednesday vs 7.1174 Tuesday

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1126 on Wednesday, compared with 7.1174 set on Tuesday. The fixing was estimated at 7.1732 by Bloomberg survey today.

MARKET DATA

SOUTH KOREA NOV EXPORT PRICES Y/Y -7.2%; PRIOR -9.3%

SOUTH KOREA NOV IMPORT PRICES Y/Y -8.5%; PRIOR -9.9%

SOUTH KOREA NOV UNEMPLOYMENT RATE 2.8%; MEDIAN 2.6%; PRIOR 2.5%

SOUTH KOREA NOV BANK LENDING TO HOUSEHOLDS KR 1091.9t; PRIOR KR1086.5t

NEW ZEALAND 3Q CURRENT ACCOUNT GDP RATIO YTD -7.6%; MEDIAN -7.4%; PRIOR -7.6%

NEW ZEALAND NOV FOOD PRICES M/M -0.2%; PRIOR -0.9%

JAPAN Q4 TANKAN LARGE MFG INDEX 12; MEDIAN 10; PRIOR 9

JAPAN Q4 TANKAN LARGE NON-MFG INDEX 30; MEDIAN 27; PRIOR 27

JAPAN Q4 TANKAN LARGE MFG OUTLOOK 8; MEDIAN 9; PRIOR 10

JAPAN Q4 TANKAN LARGE NON-MFG OUTLOOK 24; MEDIAN 25; PRIOR 21

JAPAN Q4 TANKAN ALL INDUSTRY CAPEX 13.5%; MEDIAN 12.7%; PRIOR 13.6%

MARKETS

US TSYS: Slightly Richer Ahead Of The FOMC Decision

TYH4 is currently trading at 110-20, +0-02+ from NY closing levels.

- Cash tsys are dealing ~1bp richer in the Asia-Pac session ahead of tonight’s FOMC rate decision at 1300ET and Fed Chair Powell's presser at 1430ET. PPI data is released beforehand.

- The Fed will likely lower its median "dot plot" estimate for policy interest rates at the end of 2024 to around 4.9%, former officials and staffers told MNI, as expectations build for the first rate cut to come as early as the year's first half.

- There has been no meaningful newsflow so far today.

JGBS: Bull-Flattening Gathers Momentum In The Afternoon Session Ahead Of The FOMC Decision

JGB futures are richer, +48 compared to settlement levels, and near the Tokyo session high. Futures had initially softened following a stronger-than-expected Q4 Tankan Survey, but that softness has been more than reversed.

- Outside of the Tankan survey, the only potential domestic driver has been today’s BOJ Rinban operations covering 1-3-year, 5-10-year, and 25-year+ JGBs. The operations showed mixed results, with negative spreads but higher offer cover ratios.

- Japan PM Kishida will front the local media today (6:15 pm local time) in which a funding scandal involving his ruling LDP party is expected to feature.

- Cash tsys are dealing ~1bp richer in the Asia-Pac session ahead of tonight’s FOMC rate decision. PPI data is released beforehand.

- Today’s bull-flattening of the cash JGB curve has gathered momentum in the afternoon session following the BOJ Rinban operations, with yields 0.6bp to 5.4bps lower. The benchmark 10-year yield is 1.7bps lower at 0.704% versus the morning’s high of 0.735%.

- The swaps curve has also bull-flattened, with swap spreads mixed.

- Tomorrow, the local calendar will show Core Machine Orders, International Investment Flow, IP and Capacity Utilisation data. The MOF also plans to sell Y1.2tn of 20-year JGBs.

AUSSIE BONDS: Richer, MYEFO Signals Improved Fiscal Position, Jobs Report Tomorrow

In futures roll-impacted dealings, ACGBs (YM +2.2 & XM +5.5) are stronger but slightly off Sydney session best levels. The key domestic event today was the publication of the government’s Mid-Year Economic and Fiscal Outlook (MYEFO).

- As expected, the budget and debt ratio projections improved compared with May’s budget. A surplus is not yet forecast for this financial year, with a small deficit of $1.1bn projected (a $12.8bn improvement). It is however a negligible share of the economy. The MYEFO shouldn’t change the RBA’s view that fiscal policy is currently not inflationary.

- Elsewhere, CBA’s household spending index rose 4.1% y/y in November versus a revised +2.4% in October. Household spending rose 1.8% m/m versus a revised -0.6% in October.

- US tsys are dealing ~1bp richer in the Asia-Pac session ahead of tonight’s FOMC rate decision.

- Cash ACGBs are 2-6bps richer, with the AU-US 10-year yield differential 4bps tighter at +8bps.

- Swap rates are 2-4bps lower, with EFPs slightly wider.

- The bills strip is flat to +1 across contracts.

- RBA-dated OIS pricing is slightly softer across meetings.

- Tomorrow, the local calendar sees the November Employment Report. Bloomberg consensus is expecting a gain of 11.5k jobs, with an uptick in the unemployment rate to 3.8% from 3.7%.

NZGBS: Closed With A Significant Bull-Flattening Price Indices Data

NZGBs have bull-flattened into the close of the local session, with yields flat to 9bps lower. After dealing in narrow ranges for much of the session, 5-10-year NZGBs rallied 5-7bps after Statistics NZ reported price indexes for selected goods and services for November.

- Food, fuel and alcohol prices, comprising ~27% of CPI, rose at a slower annual pace.

- The strengthening of the market was aided by downward revisions from sell-side banks. Westpac NZ economists cut their forecast for Q4 CPI inflation. Westpac now sees CPI rising 0.3% q/q versus the previous projection of 0.6%. Separately, ASB Bank said that the selected price index data suggested annual inflation through November had slowed. “Prices were down 0.5% in November, with annual inflation a smidgen below 5%... and consistent with our core view that there is considerable downside risk to the 5.0% y/y RBNZ pick”.

- Swap rates closed 11-13bps lower, with the 5-year outperforming.

- RBNZ dated OIS pricing is 4-11bps softer across meetings beyond Apr’24, with Nov’24 leading. The market now has 65bps of easing priced by Nov’24.

- Tomorrow, the NZ Treasury plans to sell NZ$200mn of the 4.5% May-30 bond, NZ$225mn of the 3.5% Apr-33 bond and NZ$75mn of the 2.75% May-51 bond.

FOREX: NZD Falters On Slower Inflation Data, USD Mildly Firmer Elsewhere

The USD index sits marginally higher as the FOMC comes into view. The BBDXY index was last near 1242, +0.10% firmer for the session. Earlier lows were at 1240.35, which leaves us within recent ranges.

- The main focus point in Asia Pac trade has been NZD weakness. This followed earlier monthly price data, which suggests inflation is cooling more than the RBNZ expects.

- A number of local banks have lowered their inflation projections as a result.

- NZD/USD has test sub 0.6100 and sits close to this level in recent dealings, which is 0.55% weaker for the session. Note the 20-day EMA isn't too far away (0.6093), while the 200-day sits at 0.6075. NZ swap rates closed 11-13bps lower.

- As widely expected, the new NZ government passed laws returning the RBNZ to a signal price mandate.

- AUD/USD sits marginally lower, last near 0.6555, but has outperformed NZD by around 0.45%. The AUD/NZD was last near 1.0745/50. The mid year fiscal update from the government didn't impact sentiment, while CBA data showed a firmer spending in November.

- USD/JPY got to 145.19 in early trade, but now sits back at 145.60/65, slightly above NY closing levels from Tuesday. The Q4 Tankan survey was at the margin better than expected, showing solid business conditions and Capex intensions.

- The main upcoming focus will be the US FOMC decision. Prior to that we have UK monthly GDP figures.

EQUITIES: China Markets Weaker, Japan Outperforms Modestly

Most regional equity markets are under pressure in Wednesday Asia Pac dealing. China markets are among the weakest performers, while Japan markets are outperforming at the margin. US futures are modestly higher as the US FOMC decision later comes into view. Eminis last near 4702, +0.11%, while Nasdaq futures have firmed +0.15%.

- At the break, the CSI 300 sits just over 0.90% lower, and is back sub 3400 in index terms. Losses are fairly broad based at this stage, although some tech plays are outperforming. The Hang Seng China Enterprise Index is down 1.0%.

- Market disappointment around the lack of fresh stimulus measures from the Central Economic Work Conference has weighed on sentiment in the space.

- The HSI is off 0.74% at the break in Hong Kong, with the tech sub index is off -0.82%, only partially unwinding yesterday's 1.74% gain. The broader trend is still quite soft.

- In Japan, the Nikkei 225 is up +0.35%, while the Topix is around flat. Tech names are outperforming so far, which is in line with trends from US trade, with the SOX index breaking higher in recent sessions.

- The same moves haven't been enough to drive the Kospi higher (off nearly 0.60%), while the Taiex is around flat.

- NZ's market is +0.82% higher, after partial data showed signs inflation is cooling more than the RBNZ forecast.

- In SEA most markets are down. Thailand stocks continue to underperform, the SET off a further 0.80%. This puts the index back to levels last seen in late 2020.

OIL: Crude Lower Ahead Of Fed And OPEC Report

Oil prices are moderately lower in APAC trading today after falling around 3.5% on Tuesday on growing evidence of rising supply while demand is lacklustre. Prices are off their intraday highs with Brent down 0.3% from yesterday’s close finding support around $73/bbl and WTI is -0.2% to $68.48. The USD index is 0.1% higher ahead of the Fed decision and updated forecasts later.

- Bloomberg shipping data showed Russian exports at their highest since July and the EIA revised up 2023 US supply by 30kbd but revised down 2024 by 40kbd and expected global output by 1.36mbd from last month. OPEC’s monthly report is today and the IEA’s on Thursday. There is significant scepticism in the market that OPEC’s new quotas will be adhered to.

- Futures contracts continue to point to a widening market surplus and according to Bloomberg the 12 month WTI spread moved into contango yesterday for the first time in 2023.

- Bloomberg reported that US crude inventories fell 2.35mn barrels in the latest week, according to people familiar with the API data. Product stocks rose though with gasoline up 5.8mn and distillate 276k. The official EIA data is out later today.

- Later the Fed decision is announced but it is widely expected to leave rates unchanged (see MNI Fed Preview). There will also be updated forecasts and a press conference, which will be important for oil markets. On the data front there’s US November PPI data and UK & euro area IP.

GOLD: Consolidating Ahead Of The FOMC Decision

Gold is showing minimal movement in the Asia-Pacific session, maintaining its position after a marginal 0.1% decline to $1979.54 on Tuesday.

- Yesterday's market activity is best characterised as a consolidation following Monday's notable slide, setting the stage for the upcoming FOMC decision at 1300 ET and Fed Chair Powell's press conference at 1430 ET.

- The Fed will likely lower its median "dot plot" estimate for policy interest rates at the end of 2024 to around 4.9%, former officials and staffers told MNI, as expectations build for the first rate cut to come as early as the year's first half.

- US Treasuries finished slightly richer following an in-line US CPI print on Tuesday.

- Bullion has experienced a wide ride in the latter part of this year, witnessing a dip in September followed by a surge to a record earlier this month. The metal's trajectory has been significantly influenced by trader speculation on future US monetary policy, with lower rates typically positive for gold.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/12/2023 | 0700/0700 | ** |  | UK | UK Monthly GDP |

| 13/12/2023 | 0700/0700 | ** | | UK | Index of Services |

| 13/12/2023 | 0700/0700 | *** | | UK | Index of Production |

| 13/12/2023 | 0700/0700 | ** | | UK | Trade Balance |

| 13/12/2023 | 0700/0700 | ** | | UK | Output in the Construction Industry |

| 13/12/2023 | 1000/1100 | ** |  | EU | Industrial Production |

| 13/12/2023 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 13/12/2023 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 13/12/2023 | 1330/0830 | * |  | CA | Household debt-to-income |

| 13/12/2023 | 1330/0830 | *** | | US | PPI |

| 13/12/2023 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 13/12/2023 | 1900/1400 | *** | | US | FOMC Statement |

| 14/12/2023 | 2145/1045 | *** |  | NZ | GDP |

| 14/12/2023 | 2350/0850 | * |  | JP | Machinery orders |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.