Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- OIL DECLINES AS ISRAEL DELAYS GAZA INVASION AMID HOSTAGE TALKS - BBG

- BOJ MAY REVIEW YIELD-CURVE CONTROL POLICY AS RATES RISE - NIKKEI

- JAPAN CORP. LOAN DEMAND RISES - BOJ SURVEY - MNI BRIEF

- CHINA TO REACH TARGET OF 5% GDP GROWTH - LOU JIWEI - MNI BRIEF

- CHINA FINANCIAL SECTOR TO BOOST TECH INNOVATION - MNI BRIEF

- SWISS TURN TO RIGHT AT ELECTION AS IMMIGRATION FEARS WEIGH - RTRS

- ARGENTINA’S PERONISTS SOAR IN ELECTION TO SEAL RUN-OFF WITH RADICAL MILEI - RTRS

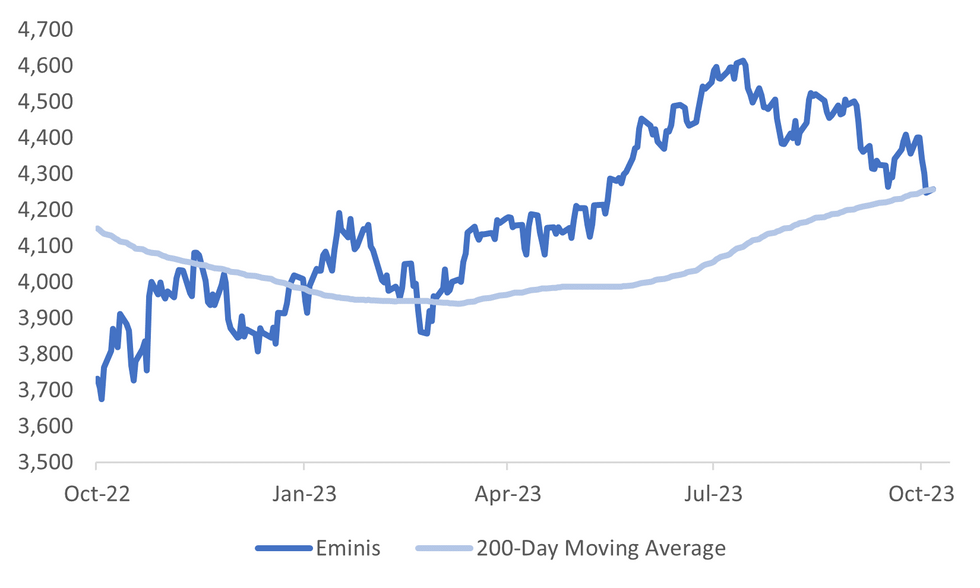

Fig. 1: US Eminis Index Versus Simple 200-day Moving Average

Source: MNI - Market News/Bloomberg

EUROPE

SWITZERLAND (RTRS): Switzerland looked set to shift to the right in national elections on Sunday, as concerns about immigration trumped fears about climate change and melting glaciers, though the vote is unlikely to change the make-up of the Swiss government.

ECB (BBG): Some of the biggest money managers in Europe say traders are wrong to bet the European Central Bank is done hiking interest rates.

U.S.

POLITICS (BBG): House Republicans set up a nine-man contest for the speaker’s post on Sunday, signaling what may be a drawn-out vote to fill the vacancy this week.

OTHER

MIDEAST (RTRS): Israeli aircraft struck two Hezbollah cells in Lebanon early on Monday, which were planning to launch anti-tank missiles and rockets toward Israel, its military said, as fighting flared across the two countries' shared border.

MIDEAST (RTRS): A second convoy of 14 aid trucks entered the Rafah crossing from the Egyptian side to the besieged Gaza Strip on Sunday night, Juliette Touma, director of communications at the U.N. Relief and Works Agency (UNRWA), told Reuters in Gaza by phone from Amman.

MIDEAST (BBG): Oil declined, tracking losses in wider equity markets, as Israel held off on its ground invasion of Gaza amid diplomatic efforts to secure the release of more hostages.

JAPAN (NIKKEI/BBG): Bank of Japan officials are pondering the question of whether to tweak the settings of the yield-curve control program as domestic long-term interest rates float higher in tandem with those in the US, the Nikkei newspaper reported on Sunday, without saying where it obtained the information.

JAPAN (MNI BRIEF): Demand for financing by Japanese corporates via banks rose from three months ago, reflecting the increase of capital investment and internal reserves, according to the Bank of Japan's senior loan officer opinion survey on bank lending practices.

AUSTRALIA (BBG): Australia will suspend its case at the World Trade Organization over China’s tariffs on wine imports ahead of Prime Minister Anthony Albanese’s first trip to the country next month.

ARGENTINA (RTRS):Argentina's ruling Peronist coalition smashed expectations to lead the country's general election on Sunday, setting the stage for a polarized run-off vote next month between Economy Minister Sergio Massa and far-right libertarian radical Javier Milei.

CHINA

GROWTH (MNI BRIEF): China can achieve its annual economic growth target of about 5% set at the beginning of the year despite headwinds, while the financial sector should enhance support to the economy to better serve global economic resilience and stability, said China's former Minister of Finance Lou Jiwei during the 2023 Shanghai Suhewan Conference on Sunday.

GROWTH (YICAI): China should continue to stimulate the economy and not just settle on achieving the annual growth target of 5%, wrote Guan Tao, former director at the State Administration of Foreign Exchange in an article published by Yicai. (YICAI)

FINANCIAL SECTOR (MNI BRIEF): China should guide long-term funds to invest in technological innovation, increase the equity financing and support for eligible tech companies engaged in cross-border financing with Belt and Road Initiative countries, said Shang Fulin, former head of the China Securities Regulatory Commission and China Banking Regulatory Commission on Sunday during the 2023 Shanghai Suhewan Conference.

STOCKS (21st Century Business Herald): Authorities will likely introduce policies to stabilise the stock market with greater intensity after the Shanghai Composite Index dipped below the 3,000 mark last week, said Yang Delong, chief economist at First Seafront Fund.

CAPITAL MARKETS (BBG): China will further promote the implementation of policies to boost its capital markets and will prudently resolve default risks among large property developers, central bank chief Pan Gongsheng said in a report on the work of financial regulators to legislators.

TECH (BBG): Key iPhone assembler Hon Hai Precision Industry Co. said it will collaborate with Chinese authorities on unspecified probes, following a report that officials are conducting tax audits and reviewing land use by parent Foxconn Technology Group Co.

HOUSING (SECURITIES TIME/BBG): China should relax price controls in the property market after previous easing measures showed positive effects, the Securities Times wrote in a commentary Monday.

CHINA MARKETS

MNI: PBOC Injects Net CNY702 Bln Via OMO Mon; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY808 billion via 7-day reverse repo on Monday, with the rate unchanged at 1.80%. The operation has led to a net injection of CNY702 billion after offsetting the maturity of CNY106 billion reverse repos today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8000% at 09:24 am local time from the close of 2.3108% on Friday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 54 on Friday, compared with the close of 50 on Thursday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

PBOC Yuan Parity Lower At 7.1792 Monday vs 7.1793 Friday.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1792 on Monday, compared with 7.1793 set on Friday. The fixing was estimated at 7.3111 by Bloomberg survey today.

MARKET DATA

SOUTH KOREA OCT EXPORTS 20 DAYS Y/Y 4.6%; PRIOR 9.8%

SOUTH KOREA OCT IMPORTS 20 DAYS Y/Y 0.6%; PRIOR -1.5%

MARKETS

US TSYS: Pressured In Asia

TYZ3 deals at 105-19, -0-13, a 0-11 range has been observed on volume of ~125k.

- Cash tsys sit ~5bps cheaper across the major benchmarks.

- Tsys have been pressured in today's Asian session, local participants faded Friday's richening alongside weakness in Oil and Gold as escalation fears in the Israel/Hamas conflict eased.

- In early dealing spillover from JGBs weighed after a Sunday article in the Nikkei newspaper reported that BOJ officials are pondering whether to tweak the settings of the yield-curve control program at the upcoming policy meeting.

- Support in TY comes in at 105-10+, low from Oct 19 then 104-27+ 2.0% 10-DMA Envelope.

- The docket is thin today with just the Chicago Fed National Activity Index due.

JGBS: Futures Weaker, BOJ Tweak Fears Weigh, Curve Bear Steepens

JGB futures are holding cheaper, -18 compared to the settlement levels, after gapping lower at the open following a Sunday article in the Nikkei newspaper that reported BOJ officials are pondering whether to tweak the settings of the yield-curve control program at the upcoming policy meeting. The article didn’t say where it obtained the information.

- The local calendar was empty today, apart from BOJ Rinban operations covering 1- to 25-year JGBs. These operations saw positive spreads and generally higher cover ratios, which, as expected, has generated some pressure in the Tokyo afternoon session.

- The cash JGB curve has bear-steepened, with yields 0.1bp to 6.1bps higher. The benchmark 10-year yield is 1.2bps higher at 0.854%, above BOJ's YCC soft limit of 0.50% but below its hard limit of 1.0%. It is also slightly lower than the fresh cycle high of 0.866% set today.

- The swaps curve has also bear-steepened, with rates 0.6bp to 3.5bps higher. Swap spreads are mixed across maturities.

- Tomorrow the local calendar sees Jibun Bank Japan PMI and Department Store Sales data.

- The US docket is thin today, with just the Chicago Fed National Activity Index due.

AUSSIE BONDS: Near Session Cheaps As US Tsys & JGBs Weaken, RBA Governor Speech Tomorrow

ACGBs (YM -2.0 & XM -4.5) sit near Sydney session cheaps. With the domestic data calendar empty today, the local market has likely been on headlines and US tsys watch.

- To that end, US tsys are continuing to tick lower through the Asian session, as participants continue to fade Friday's richening. Weakness in JGBs is also weighing after a Sunday article in the Nikkei newspaper reported that BOJ officials are pondering whether to tweak the settings of the yield-curve control program at the upcoming policy meeting. Cash tsys sit 5-7bps cheaper. TYZ3 deals at 105-18+, -0-13+ compared to the NY closing level on Friday.

- Cash ACGBs are 2-5bps cheaper, with the AU-US 10-year yield differential unchanged at -19bps.

- Swap rates are 2-5bps higher, with the 3s10s curve steeper and EFPs little changed.

- The bills strip is little changed, with pricing -2 to +1.

- RBA-dated OIS pricing is flat across meetings, with terminal rate expectations at 4.36% (+29bps) ahead of Wednesday's Q3 CPI data.

- Tomorrow, the local calendar sees Judo Bank PMI data and RBA Governor Bullock’s speech at CBA’s Annual Conference. This event could be an opportunity to set out her thinking about the outlook or the framework for policy, given it is her first set-piece speech since becoming Governor.

EQUITIES: Eminis At Simple 200-day MA, China Equity Weakness Continues

Asia Pac equities have been under pressure in the first part of Monday trade. All the major indices are lower, although note Hong Kong markets have been closed today for a public holiday, which has likely had some impact on broader liquidity. Higher US futures have probably provided some offset, but this hasn't been enough to turn markets back into positive territory. Eminis are +0.18%, last near 4256, which is close to the simple 200-day MA. Nasdaq futures are up by a similar amount.

- Risk appetite has improved modestly, as Israel is yet to invade Gaza, as hostage negotiations continue. This has seen oil prices move lower, but the USD and US Tsy yields have firmed.

- China equity weakness remains a focus point. The CSI 300 is off another 0.60% to the break. This puts the index sub 3500 and below November 2022 lows.

- The Taiex is off nearly 1%. Broader tech headwinds are weighing, while a reported probe by China into key Apple supplier Hon Hai (a subsidiary of Foxconn) is also likely impacting sentiment negatively.

- The Kospi is down as well, but a more modest 0.50%. Japan benchmark indices are off by a similar amount.

- In SEA, Indonesian markets are close to -1.2% lower, continuing their recent pull back (following last week's surprise rate hike). Malaysian stocks are faring better, sitting around flat at this stage.

FOREX: Greenback Marginally Firmer, Narrow Ranges In Asia

The USD is a touch firmer in Asia however ranges have been narrow and there has been little follow through on moves thus far. BBDXY is up ~0.1%. Oil and Gold have ticked lower alongside US Tsys as escalation fears in the Middle East softened. US Equity Future are firmer.

- USD/JPY printed a high at ¥150.11 in early dealing amid thin liquidity before paring gains to sit unchanged from Friday's closing levels at ¥149.90/95. Technically the outlook remains bullish, resistance sits at ¥150.16, Oct 3 high and bull trigger. Support comes in at ¥149.08 the 20-Day EMA.

- AUD is little changed from opening level, AUD/USD prints at $0.6310/15. Q3 CPI on Wednesday is in focus with the RBA closely watching the release. The trend for AUD/USD is bearish, support comes in at $0.6286 which is the bear trigger. Resistance is at $0.6393, high from Oct 18.

- Kiwi is dealing in narrow ranges and is a touch below from Friday's closing level. A $0.5820/30 range has been observed today.

- Elsewhere in G-10 CHF is down ~0.3%, however liquidity is generally poor in Asia.

- The data docket is thin on Monday.

OIL: Crude Lower Today As Gaza Invasion On Hold For Now

Oil prices have trended lower today falling almost a percent as negotiations to release Israeli hostages has put the ground invasion of Gaza on hold. There has been little new news during the APAC session but there has been a pullback in risk sentiment with equity markets down across the region. The USD index is 0.1% higher but off its intraday high.

- WTI is down 0.9% to $87.25/bbl and Brent -0.8% to $91.42. Both are off their intraday lows of $87.03 and $91.14 respectively. Brent has spent most of the session below $92.

- Later the US Chicago Fed index for September is released and is forecast to improve marginally. There are no Fed or ECB speakers on the schedule. This week the data focus is on US preliminary October PMIs and core consumption for September. The main sensitivity for crude markets is likely to be developments in the Middle East; an expansion to other countries remains the key risk.

GOLD: Retreats From A Five Month High As Middle East Tensions Ease

Gold is 0.5% lower in the Asia-Pac session, retreating from the five-month high of $1997.22 set on Friday. This move can be attributed to easing fears over the weekend that Middle East tensions would spread to major powers after the release of two US citizens held hostage in Gaza and the US pushing Israel to delay its invasion.

- The precious metal has also been pressured by US Treasuries in today's Asia-Pac session. Cash tsys are 5-7bps cheaper across the major benchmarks after Friday's bull-steepening.

- Bullion closed +0.4% at $1981.40 on Friday, holding its clearance of resistance of $1982.4 (Jul 20 high), according to MNI’s technicals team.

- Next resistance is seen at $2003.4 (76.4% retrace of May 4 – Oct 6 bear leg).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/10/2023 | 1400/1600 | ** |  | EU | Consumer Confidence Indicator (p) |

| 23/10/2023 | 1530/1130 | * |  | US | US Treasury Auction Result for 13 Week Bill |

| 23/10/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 24/10/2023 | 2200/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

| 24/10/2023 | 0030/0930 | ** |  | JP | Jibun Bank Flash Japan PMI |

| 24/10/2023 | 0600/0800 | * |  | DE | GFK Consumer Climate |

| 24/10/2023 | 0600/0700 | *** |  | UK | Labour Market Survey |

| 24/10/2023 | 0715/0915 | ** |  | FR | S&P Global Services PMI (p) |

| 24/10/2023 | 0715/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 24/10/2023 | 0730/0930 | ** | | DE | S&P Global Services PMI (p) |

| 24/10/2023 | 0730/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 24/10/2023 | 0800/1000 | | EU | ECB Bank Lending Survey (Q3 2023) | |

| 24/10/2023 | 0800/1000 | ** | | EU | S&P Global Services PMI (p) |

| 24/10/2023 | 0800/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 24/10/2023 | 0800/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 24/10/2023 | 0830/0930 | *** | | UK | S&P Global Manufacturing PMI flash |

| 24/10/2023 | 0830/0930 | *** | | UK | S&P Global Services PMI flash |

| 24/10/2023 | 0830/0930 | *** | | UK | S&P Global Composite PMI flash |

| 24/10/2023 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 24/10/2023 | 0900/0500 | * | | US | Business Inventories |

| 24/10/2023 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 24/10/2023 | 1230/0830 | ** | | US | Philadelphia Fed Nonmanufacturing Index |

| 24/10/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 24/10/2023 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 24/10/2023 | 1345/0945 | *** | | US | S&P Global Services Index (flash) |

| 24/10/2023 | 1400/1000 | ** | | US | Richmond Fed Survey |

| 24/10/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 24/10/2023 | 1700/1300 | * | | US | US Treasury Auction Result for 2 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.